You might also like

- COA Management Letter On Lanao Del Sur 2nd District Infrastructure ProjectsDocument64 pagesCOA Management Letter On Lanao Del Sur 2nd District Infrastructure ProjectsRappler75% (4)

- General Accounting Plan Local Government Units: Table 1Document1 pageGeneral Accounting Plan Local Government Units: Table 1Pee-Jay Inigo UlitaNo ratings yet

- AOM NO. 01-Stale ChecksDocument3 pagesAOM NO. 01-Stale ChecksRagnar Lothbrok100% (2)

- Commission On Audit 1, .-: %LV.. ') Tz. Itepublit of The 1:11tilimaints Peiv EDocument2 pagesCommission On Audit 1, .-: %LV.. ') Tz. Itepublit of The 1:11tilimaints Peiv Eerrol100% (1)

- APMT 2016 - FinalDocument17 pagesAPMT 2016 - FinalmarivicNo ratings yet

- Audit Report Real Property TaxDocument6 pagesAudit Report Real Property TaxJomar Villena0% (1)

- 95-505 Test Audit Scheme and Simplified Sampling SchemeDocument30 pages95-505 Test Audit Scheme and Simplified Sampling SchemeHaryeth CamsolNo ratings yet

- IPCRFDocument5 pagesIPCRFchandy Rendaje100% (1)

- COA Process Flow Diagram PDFDocument3 pagesCOA Process Flow Diagram PDFMonica AtizadoNo ratings yet

- The Audit Case Study (Fin)Document2 pagesThe Audit Case Study (Fin)Arslan KhalidNo ratings yet

- B07 UTP & WT Non Routine and Estimation ProcessDocument8 pagesB07 UTP & WT Non Routine and Estimation ProcessJamey SimpsonNo ratings yet

- Financial Management Assessment QuestionnaireDocument12 pagesFinancial Management Assessment QuestionnaireMario Francisco100% (1)

- Ppe One Time CleansingDocument7 pagesPpe One Time CleansingKimberly RelatorresNo ratings yet

- DISPOSALDocument33 pagesDISPOSALSheed Chiu100% (1)

- Disposal PresentationDocument33 pagesDisposal PresentationMary Jane Katipunan Calumba100% (2)

- Property Management and Supply SystemDocument61 pagesProperty Management and Supply SystemTLNo ratings yet

- Commonwealth Avenue, Quezon CityDocument3 pagesCommonwealth Avenue, Quezon CityAngeli Lou Joven VillanuevaNo ratings yet

- COA Circular 89-296 Dtd. 1-27-89Document6 pagesCOA Circular 89-296 Dtd. 1-27-89Andrew GarciaNo ratings yet

- AOM 2020-005 (16-19) Ila Iyam ReimbursementsDocument2 pagesAOM 2020-005 (16-19) Ila Iyam Reimbursementsvivian cavidaNo ratings yet

- Coa Circular No. 2009-001 PDFDocument10 pagesCoa Circular No. 2009-001 PDFdemosreaNo ratings yet

- Audit Observations and RecommendationsDocument43 pagesAudit Observations and RecommendationsJonson PalmaresNo ratings yet

- Sample-Narrative-Report-on-Cash-Examination Sir MarkDocument3 pagesSample-Narrative-Report-on-Cash-Examination Sir MarkJean Monique TolentinoNo ratings yet

- Committee For Disposal For National and LGUDocument2 pagesCommittee For Disposal For National and LGUjohnisfly100% (1)

- 2016 QAR TemplateDocument36 pages2016 QAR TemplateRobehgene Atud-JavinarNo ratings yet

- COA Cir No. 2009-001-Submission of Pos, ContractsDocument28 pagesCOA Cir No. 2009-001-Submission of Pos, Contractscrizalde de dios100% (1)

- Updates About COA Strategic Plan and ProjectsDocument3 pagesUpdates About COA Strategic Plan and ProjectsJulie Khristine Panganiban-ArevaloNo ratings yet

- Doh 2011 Coa Observation RecommendationDocument71 pagesDoh 2011 Coa Observation RecommendationAnthony Sutton87% (15)

- Exercise 4 CASE AOMDocument3 pagesExercise 4 CASE AOMNaye TomawisNo ratings yet

- COA Presentation - RRSADocument155 pagesCOA Presentation - RRSAKristina Dacayo-Garcia100% (1)

- RATA, Hard Pay, Per Diem, AOM and Disallowance - 2Document110 pagesRATA, Hard Pay, Per Diem, AOM and Disallowance - 205261995No ratings yet

- The Accounting Policies: Government Accounting Manual For Local Government UnitsDocument259 pagesThe Accounting Policies: Government Accounting Manual For Local Government UnitsKyla Ramos Diamsay100% (1)

- Part IiDocument29 pagesPart IiHikasame JuschaNo ratings yet

- Aom - GafrDocument4 pagesAom - Gafrrussel1435No ratings yet

- LGU-NGAS TableofContentsVol1Document6 pagesLGU-NGAS TableofContentsVol1Pee-Jay Inigo UlitaNo ratings yet

- Part 2 - Brgy. IDocument16 pagesPart 2 - Brgy. IJonson PalmaresNo ratings yet

- Prescribing The Use of IASPPS & ICS For PPSDocument6 pagesPrescribing The Use of IASPPS & ICS For PPSJulie Khristine Panganiban100% (1)

- Baar LabelDocument61 pagesBaar LabelJerwin Cases TiamsonNo ratings yet

- Revised Audit Program - 20% DF Step by Step ProcessDocument8 pagesRevised Audit Program - 20% DF Step by Step ProcessEi Mi SanNo ratings yet

- CH 3.0-CONDUCT THE CASH EXAMINATIONDocument22 pagesCH 3.0-CONDUCT THE CASH EXAMINATIONBon Carlo Medina MelocotonNo ratings yet

- Liga AOM CollectionsDocument6 pagesLiga AOM CollectionsJonson PalmaresNo ratings yet

- New Laws and Rules On Expenditures and Disbursements (ATA)Document52 pagesNew Laws and Rules On Expenditures and Disbursements (ATA)Maria Julieta Stephanie TacogueNo ratings yet

- updated-AOM-No.-2019-015-SEF ReviewedDocument7 pagesupdated-AOM-No.-2019-015-SEF ReviewedGiovanni MartinNo ratings yet

- SAOR 2015 Additional AOM DO ZDNDocument9 pagesSAOR 2015 Additional AOM DO ZDNrussel1435No ratings yet

- COA - Circular2009-002.pre Audit ChecklistDocument30 pagesCOA - Circular2009-002.pre Audit ChecklistNaiv Guerra100% (1)

- 08 BLGUMAGSAYSAYHILL 2022 AAR Part2 Findings and RecommendationsDocument22 pages08 BLGUMAGSAYSAYHILL 2022 AAR Part2 Findings and RecommendationsGil DavinNo ratings yet

- Tugaya2020 Audit Report COADocument54 pagesTugaya2020 Audit Report COAMong AliNo ratings yet

- Developing The Overall Audit Strategy: Psa 300 Planning An Audit of Financial StatementsDocument14 pagesDeveloping The Overall Audit Strategy: Psa 300 Planning An Audit of Financial StatementssammycoombsNo ratings yet

- Annex N Coa 2005-027Document2 pagesAnnex N Coa 2005-027Naye TomawisNo ratings yet

- LRMPAT Final Version ManualDocument45 pagesLRMPAT Final Version ManualQuantity Survey SectionNo ratings yet

- 2K12 ARB-Lower DimalinaoDocument8 pages2K12 ARB-Lower DimalinaoJuan Luis LusongNo ratings yet

- Aapsi 2020Document9 pagesAapsi 2020Ragnar LothbrokNo ratings yet

- Sample Transmittal LetterDocument1 pageSample Transmittal LetterJonson PalmaresNo ratings yet

- Property and Supply Management in The Local GovernDocument2 pagesProperty and Supply Management in The Local GovernMaria Angelica PanongNo ratings yet

- Audit of Confidential Fund of LGUDocument16 pagesAudit of Confidential Fund of LGUBarwin Scott VillordonNo ratings yet

- PPSAS and The Revised Chart of AccountsDocument51 pagesPPSAS and The Revised Chart of Accountsmile100% (4)

- Unified Audit StrategyDocument8 pagesUnified Audit StrategyvangieNo ratings yet

- Property and Supply ManagementDocument50 pagesProperty and Supply ManagementLexa SpecterNo ratings yet

- Flowchart-Issuance of Supplies and Materials-Appen3Document2 pagesFlowchart-Issuance of Supplies and Materials-Appen3Melanie Ann100% (1)

- Government Auditing and Accounting For NPODocument65 pagesGovernment Auditing and Accounting For NPOAljon Fabrigas SalacNo ratings yet

- Revised IRR RA 9184 (Goods)Document27 pagesRevised IRR RA 9184 (Goods)jrcanlas100% (3)

- Flow Chart LGUDocument1 pageFlow Chart LGUjohnisflyNo ratings yet

- Inventory 2022 PipDocument10 pagesInventory 2022 PipGSS emb10100% (1)

- COA ADGP Workshop Day 1 - Qs 1-9Document3 pagesCOA ADGP Workshop Day 1 - Qs 1-9Atty. Lynn ElevadoNo ratings yet

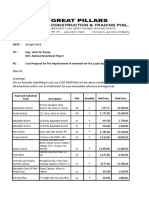

- Cost Pproposal For ToolsDocument12 pagesCost Pproposal For ToolsMarie A. ZednanrehNo ratings yet

- Paul & Tine: Save The Date!Document4 pagesPaul & Tine: Save The Date!Marie A. ZednanrehNo ratings yet

- Connectivity Network Including ICT Equipment in Ilocos Norte - TOR - 10 Mar 2022Document18 pagesConnectivity Network Including ICT Equipment in Ilocos Norte - TOR - 10 Mar 2022Marie A. ZednanrehNo ratings yet

- Welcome To Palawan State UniversityDocument2 pagesWelcome To Palawan State UniversityMarie A. ZednanrehNo ratings yet

- Quiz SolutionsDocument4 pagesQuiz SolutionsEDELYN PoblacionNo ratings yet

- Course Material 2 - The Unified Accounts Codes StructureDocument34 pagesCourse Material 2 - The Unified Accounts Codes StructureJayvee BernalNo ratings yet

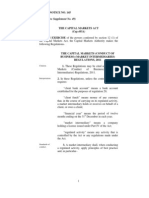

- Capital Markets (Conduct of Business) (Market Intermediaries) Regulations 2011Document29 pagesCapital Markets (Conduct of Business) (Market Intermediaries) Regulations 2011MchizziNo ratings yet

- Intermediate May 2011Document109 pagesIntermediate May 2011Adesoye AyodejiNo ratings yet

- Checklistand Sample Forms FinalDocument46 pagesChecklistand Sample Forms FinalDK DalusongNo ratings yet

- PTF Depo ExhibitsDocument57 pagesPTF Depo ExhibitsChristopher KingNo ratings yet

- Fraud Control Jul08Document46 pagesFraud Control Jul08hmedlamineNo ratings yet

- ICTMDocument6 pagesICTMElizer Robles Jr.No ratings yet

- AR 2020 Akasha Wira International TBK Rev 828-06-2021e ReportingDocument168 pagesAR 2020 Akasha Wira International TBK Rev 828-06-2021e ReportingYati Nurul HashfiNo ratings yet

- Fiscal PlanningDocument22 pagesFiscal PlanningRadha Sri100% (2)

- Ethical Issues in Business - A Case Study of Selected FirmsDocument16 pagesEthical Issues in Business - A Case Study of Selected FirmsdarshanNo ratings yet

- Psas and PapssDocument5 pagesPsas and PapssmageNo ratings yet

- Jaca V PeopleDocument41 pagesJaca V PeoplebernadetteNo ratings yet

- How Do I Apply For An API Monogram LicenseDocument3 pagesHow Do I Apply For An API Monogram Licensecoco_62No ratings yet

- Modern Auditing: Modern AuditingDocument27 pagesModern Auditing: Modern Auditingdhyah oktariantiNo ratings yet

- Management's Discussion and Analysis - Guidance On Preparation and DisclosureDocument56 pagesManagement's Discussion and Analysis - Guidance On Preparation and DisclosureMichael WangNo ratings yet

- Letter To Auditor General Timothy DeFoorDocument2 pagesLetter To Auditor General Timothy DeFoorPennLiveNo ratings yet

- Internal Environment Analysis: Prepared By: Limheya Lester Glenn R PCU-MBA ProgramDocument35 pagesInternal Environment Analysis: Prepared By: Limheya Lester Glenn R PCU-MBA ProgramXXXXXXXXXXXXXXXXXXNo ratings yet

- Chapter - 1 Introduction of 1) Meaning of AuditingDocument31 pagesChapter - 1 Introduction of 1) Meaning of AuditingRajesh GuptaNo ratings yet

- Factors Influencing Tax Avoidance PDFDocument6 pagesFactors Influencing Tax Avoidance PDFJoseNo ratings yet

- Company Name: Jcamua and Associates CoDocument5 pagesCompany Name: Jcamua and Associates CoDyk RuNo ratings yet

- Supplier Health Check Sheet - Rev 01ADocument9 pagesSupplier Health Check Sheet - Rev 01Amahesh KhatalNo ratings yet

- Gökhan Savas Tolu-CVDocument5 pagesGökhan Savas Tolu-CVGokhan Savas ToluNo ratings yet

- CAPE Accounting 2016 U1 P1Document10 pagesCAPE Accounting 2016 U1 P1DinaNo ratings yet

- Joe CMA - CV PDFDocument4 pagesJoe CMA - CV PDFAli AyubNo ratings yet

- Difference Between FA, CA - MADocument9 pagesDifference Between FA, CA - MARishabh MehtaNo ratings yet

- BBVA Roadmap and Benefits Case Development V7 - FinalDocument47 pagesBBVA Roadmap and Benefits Case Development V7 - FinalchrisystemsNo ratings yet