You might also like

- Problem 2-6 (Book)Document11 pagesProblem 2-6 (Book)Cherry Doong CuantiosoNo ratings yet

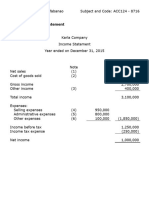

- Masay Company's Statement of Comprehensive IncomeDocument24 pagesMasay Company's Statement of Comprehensive Incomejake doinog88% (16)

- A. Masay Company Statement of Cost of Goods Manufactured Year Ended XX 2020Document6 pagesA. Masay Company Statement of Cost of Goods Manufactured Year Ended XX 2020Jay Ann DomeNo ratings yet

- Cost of Goods Manufactured for Christian CompanyDocument10 pagesCost of Goods Manufactured for Christian CompanyAira Santos VibarNo ratings yet

- Chapter 4 - Ia3Document10 pagesChapter 4 - Ia3Xynith Nicole RamosNo ratings yet

- Act 4 Masay Company (Is)Document4 pagesAct 4 Masay Company (Is)Reginald MundoNo ratings yet

- Cost of Gooods Manufactured 5,060,000Document5 pagesCost of Gooods Manufactured 5,060,000yayayaNo ratings yet

- Chapter 6 Exercise Activity With AnswersDocument25 pagesChapter 6 Exercise Activity With Answers乙คckคrψ YTNo ratings yet

- Act 4 Masay Company (SCGS)Document4 pagesAct 4 Masay Company (SCGS)Reginald MundoNo ratings yet

- Problem 9-1: Net IncomeDocument16 pagesProblem 9-1: Net IncomeHerlyn Juvelle SevillaNo ratings yet

- Jao Company's Comprehensive Income StatementDocument9 pagesJao Company's Comprehensive Income StatementJesiah PascualNo ratings yet

- Statement of Financial Position/Retained EarningsDocument5 pagesStatement of Financial Position/Retained EarningsShane TabunggaoNo ratings yet

- Net Cash Flows From Operating ActivitiesDocument7 pagesNet Cash Flows From Operating ActivitiesShaneNiñaQuiñonezNo ratings yet

- 4-2 Endless CompanyDocument3 pages4-2 Endless CompanyyayayaNo ratings yet

- Intermediate Accounting Volume 3 ValixDocument12 pagesIntermediate Accounting Volume 3 ValixVyonne Ariane Ediong0% (1)

- Lor, 6-1,6-2Document7 pagesLor, 6-1,6-2KC Hershey Lor100% (4)

- Masay Company Cost of Sales Method StatementDocument11 pagesMasay Company Cost of Sales Method StatementAce NetbookNo ratings yet

- Sample Problems Cash Flow AnalysisDocument2 pagesSample Problems Cash Flow AnalysisTeresa AlbertoNo ratings yet

- Masay Company Cost of Sales MethodDocument11 pagesMasay Company Cost of Sales MethodE.D.J60% (5)

- Abellano - Activity 1 & 2Document4 pagesAbellano - Activity 1 & 2Nelia AbellanoNo ratings yet

- Sujide, Kendrew Statement of Comprehensive IncomeDocument5 pagesSujide, Kendrew Statement of Comprehensive IncomeKendrew SujideNo ratings yet

- Solution Accounting 2Document3 pagesSolution Accounting 2Hanzo vargasNo ratings yet

- Answers FAR - CASE ANALYSISDocument4 pagesAnswers FAR - CASE ANALYSISJaquelyn ClataNo ratings yet

- Problem Solving 1: RequirementsDocument4 pagesProblem Solving 1: RequirementsMariz TimarioNo ratings yet

- Cost Accounting (De Leon) Chapter 3 SolutionsDocument9 pagesCost Accounting (De Leon) Chapter 3 SolutionsLois Alveez Macam85% (26)

- Homework Chapter 2 - Phuong AnhDocument5 pagesHomework Chapter 2 - Phuong AnhNguyễn Ánh NgọcNo ratings yet

- 10E - Build A Spreadsheet 02-44Document2 pages10E - Build A Spreadsheet 02-44MISRET 2018 IEI JSCNo ratings yet

- Ronald Company 2019 Costs, Sales, IncomeDocument3 pagesRonald Company 2019 Costs, Sales, IncomeKean Brean GallosNo ratings yet

- Assignment 5 - Statement of Cash FlowsDocument2 pagesAssignment 5 - Statement of Cash FlowsJezza Mae Gomba RegidorNo ratings yet

- Chapter 14Document22 pagesChapter 14Dan ChuaNo ratings yet

- Intermediate Accounting 3 Comprehensive Income ProblemsDocument2 pagesIntermediate Accounting 3 Comprehensive Income ProblemsDarlyn Dalida San PedroNo ratings yet

- TP1-W2-S3-R0 Sri Annisa KatariDocument3 pagesTP1-W2-S3-R0 Sri Annisa Katarisri annisa katariNo ratings yet

- Karla Company Income Statement Year Ended December 31, 2008 NoteDocument8 pagesKarla Company Income Statement Year Ended December 31, 2008 NoteROCHELLE ANNE VICTORIANo ratings yet

- AE 112 - Midterm Summative Assessment (Quiz 1) Suggested Answers and SolutionsDocument3 pagesAE 112 - Midterm Summative Assessment (Quiz 1) Suggested Answers and SolutionsDjunah ArellanoNo ratings yet

- Manufacturing Costs and COGSDocument4 pagesManufacturing Costs and COGSNia BranzuelaNo ratings yet

- Synthesis ReportingDocument3 pagesSynthesis ReportingJason Dwight CamartinNo ratings yet

- 105 - Activity 1 - Cash FlowDocument11 pages105 - Activity 1 - Cash FlowElla DavisNo ratings yet

- Intermediate Accounting 3 Activity 2 ProblemsDocument4 pagesIntermediate Accounting 3 Activity 2 ProblemsLars FriasNo ratings yet

- Chapter 2 - 1 - IllustrationDocument6 pagesChapter 2 - 1 - IllustrationYonas BamlakuNo ratings yet

- Answer Key Chapter 3Document5 pagesAnswer Key Chapter 3Donna Zandueta-TumalaNo ratings yet

- ACC124 Part2Document6 pagesACC124 Part2Christine LigutomNo ratings yet

- Assignment1_Profit and loss exercise E financeDocument8 pagesAssignment1_Profit and loss exercise E financees.eldeebNo ratings yet

- 4-6 Dahlia CompanyDocument1 page4-6 Dahlia CompanyyayayaNo ratings yet

- Financial Statement Analysis of Sales, Expenses, Income and Comprehensive IncomeDocument5 pagesFinancial Statement Analysis of Sales, Expenses, Income and Comprehensive IncomeMariella Antonio-NarsicoNo ratings yet

- Corp AccountsDocument8 pagesCorp AccountsShreyNo ratings yet

- Cost Accounting de Leon Chapter 3 SolutionsDocument9 pagesCost Accounting de Leon Chapter 3 SolutionsRichelle SangatananNo ratings yet

- Solutions To Chapter 9Document10 pagesSolutions To Chapter 9Luzz Landicho100% (1)

- Cost Accounting (Tooba)Document6 pagesCost Accounting (Tooba)Ali AbbasNo ratings yet

- Chapter 2Document40 pagesChapter 2ellyzamae quiraoNo ratings yet

- ACC124 - Assignment On Income StatementDocument6 pagesACC124 - Assignment On Income StatementRuzuiNo ratings yet

- Statement of Comprehensive Income - PROBLEMSDocument20 pagesStatement of Comprehensive Income - PROBLEMSSarah GNo ratings yet

- Conceptual Framework Valix 2019 8-1, 9-1 PDFDocument6 pagesConceptual Framework Valix 2019 8-1, 9-1 PDFTenshi Aina SantosNo ratings yet

- Income Statement Hide Corp. Seek Corp. Dr. CR.: Book Value of Stocholders' Equity of Seek CorpDocument11 pagesIncome Statement Hide Corp. Seek Corp. Dr. CR.: Book Value of Stocholders' Equity of Seek CorpmoreNo ratings yet

- Batch 18 1st Preboard (P1)Document14 pagesBatch 18 1st Preboard (P1)Jericho PedragosaNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Using Economic Indicators to Improve Investment AnalysisFrom EverandUsing Economic Indicators to Improve Investment AnalysisRating: 3.5 out of 5 stars3.5/5 (1)

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- PDF Morton Salt 1a17 - CompressDocument22 pagesPDF Morton Salt 1a17 - CompressLara FloresNo ratings yet

- 3 - Implementing Quality CostDocument3 pages3 - Implementing Quality CostLara FloresNo ratings yet

- Pdf-The CompressDocument3 pagesPdf-The CompressLara FloresNo ratings yet

- Answer Key: Chapter 06 Audit Planning, Understanding The Client, Assessing Risks, and RespondingDocument25 pagesAnswer Key: Chapter 06 Audit Planning, Understanding The Client, Assessing Risks, and RespondingRalph Santos100% (2)

- Basic Concept in Management AccountingDocument13 pagesBasic Concept in Management AccountingLara FloresNo ratings yet

- Chapter01.the Changing Role of Managerial Accounting in A Dynamic Business EnvironmentDocument13 pagesChapter01.the Changing Role of Managerial Accounting in A Dynamic Business EnvironmentEleia Cruz 吳玉青100% (2)

- Q2 Topic6 Determining-Textual-EvidencesDocument25 pagesQ2 Topic6 Determining-Textual-EvidencesLara FloresNo ratings yet

- Q2 Topic4 Formulating-Evaluative-StatementsDocument19 pagesQ2 Topic4 Formulating-Evaluative-StatementsLara FloresNo ratings yet

- Kami Export - Pdf-Reviewer-In-Management-Advisory-Services-Roque - CompressDocument500 pagesKami Export - Pdf-Reviewer-In-Management-Advisory-Services-Roque - CompressLara FloresNo ratings yet

- Final Project in Financal Accounting 2Document10 pagesFinal Project in Financal Accounting 2Lara FloresNo ratings yet

- Q2 - Topic3 - Critical Reading As Form of ReasoningDocument15 pagesQ2 - Topic3 - Critical Reading As Form of ReasoningLara FloresNo ratings yet

- PT 4 - The Mysterious Death of Mrs. HuffingtonDocument6 pagesPT 4 - The Mysterious Death of Mrs. HuffingtonLara FloresNo ratings yet

- Gen Bio1 2ND Q.module 1Document9 pagesGen Bio1 2ND Q.module 1Lara FloresNo ratings yet

- SPADE Analysis Globe Telecom Inc PDFDocument29 pagesSPADE Analysis Globe Telecom Inc PDFLara FloresNo ratings yet

- Chapter 13: Global Operations and Supply-Chain Management: True/FalseDocument22 pagesChapter 13: Global Operations and Supply-Chain Management: True/FalseLara FloresNo ratings yet

- GW01 F Industry Analysis Globe Telecom Inc. 1Document31 pagesGW01 F Industry Analysis Globe Telecom Inc. 1Lara FloresNo ratings yet

- Q2 Topic5 Formulating-Evaluative-StatementsDocument13 pagesQ2 Topic5 Formulating-Evaluative-StatementsLara FloresNo ratings yet

- Ch. 16 - Distribution To ShareholdersDocument28 pagesCh. 16 - Distribution To ShareholdersLara FloresNo ratings yet

- Homeroom Guidance ModuleDocument9 pagesHomeroom Guidance ModuleLara FloresNo ratings yet

- Ch. 20 - Hybrid FinancingDocument31 pagesCh. 20 - Hybrid FinancingLara FloresNo ratings yet

- End Dread, Stop SpreadDocument1 pageEnd Dread, Stop SpreadLara FloresNo ratings yet

- Analysis Paper Group3Document24 pagesAnalysis Paper Group3Lara FloresNo ratings yet

- Gen Bio1 2ND Q.module 2Document9 pagesGen Bio1 2ND Q.module 2Lara FloresNo ratings yet

- Home Office QuestionsDocument10 pagesHome Office QuestionsLara FloresNo ratings yet

- Advanced Accounting Part 2 Dayag 2015 Chapter 13Document22 pagesAdvanced Accounting Part 2 Dayag 2015 Chapter 13RafaelLee100% (2)

- Ch. 15 - Capital Structure & LeverageDocument45 pagesCh. 15 - Capital Structure & LeverageLara FloresNo ratings yet

- Home office and branch accounting questionsDocument13 pagesHome office and branch accounting questionsLara FloresNo ratings yet

- 42 PDFDocument35 pages42 PDFLara FloresNo ratings yet

- Solano Ruth Home Office SeatworkDocument11 pagesSolano Ruth Home Office SeatworkLara FloresNo ratings yet

- Topic 7 Linear ProgrammingDocument17 pagesTopic 7 Linear ProgrammingLara FloresNo ratings yet

- PAS 11: Long-term construction contractsDocument5 pagesPAS 11: Long-term construction contractsLester John Mendi0% (1)

- TVS Motor - Taxmann VersionDocument19 pagesTVS Motor - Taxmann VersionSripal JainNo ratings yet

- Noraini June 2023 Pay Slip PDFDocument2 pagesNoraini June 2023 Pay Slip PDFNoraini NasimamNo ratings yet

- Objective QuestionsDocument61 pagesObjective QuestionsAvijitneetika Mehta100% (1)

- Lecture 1 & 2Document35 pagesLecture 1 & 2Phill NamaraNo ratings yet

- What Are The Various Streams of AccountingDocument13 pagesWhat Are The Various Streams of AccountingvijaybhaskarreddymeeNo ratings yet

- Apartment Expense GuideDocument11 pagesApartment Expense GuideRay DoucetteNo ratings yet

- Accounting Concepts and ConventionsDocument38 pagesAccounting Concepts and Conventions727822TPMB005 ARAVINTHAN.SNo ratings yet

- Kec Internatinal Ltd.Document14 pagesKec Internatinal Ltd.Rahul RathoreNo ratings yet

- Sample Chart of AccountsDocument12 pagesSample Chart of AccountsjeffryNo ratings yet

- Module 1.1 - Property, Plant and EquipmentDocument6 pagesModule 1.1 - Property, Plant and EquipmentJaimell LimNo ratings yet

- Mission 200 Economics 100 FINALDocument67 pagesMission 200 Economics 100 FINALHari prakarsh NimiNo ratings yet

- IAR TarriffDocument60 pagesIAR Tarriffmib_santoshNo ratings yet

- Accountancy Worksheet 2020-21: Bright Riders School Abu DhabiDocument4 pagesAccountancy Worksheet 2020-21: Bright Riders School Abu DhabiwafaNo ratings yet

- CH 8Document20 pagesCH 8Firas HamadNo ratings yet

- Chapter 3Document30 pagesChapter 3SultanNo ratings yet

- Unit CDocument46 pagesUnit CKarl Lincoln TemporosaNo ratings yet

- Amortization of Computer SoftwareDocument5 pagesAmortization of Computer SoftwareAldz SumaoangNo ratings yet

- Practice QuestionsDocument133 pagesPractice QuestionsSarath KumarNo ratings yet

- Parle Working Capital AshishDocument72 pagesParle Working Capital Ashishkksomani21100% (1)

- BP Op Entpr S4hana2021 08 Co Master Data en XXDocument159 pagesBP Op Entpr S4hana2021 08 Co Master Data en XXVinay Borbachhi (IN)No ratings yet

- Babson Classic Collection: Starbucks CorporationDocument18 pagesBabson Classic Collection: Starbucks CorporationgogojamzNo ratings yet

- 145002883941Document3 pages145002883941Nathasya SahabatiNo ratings yet

- WRD 26e - Se PPT - CH 01Document19 pagesWRD 26e - Se PPT - CH 01Vĩnh TríNo ratings yet

- Financial Analysis of Au Small Finance BankDocument6 pagesFinancial Analysis of Au Small Finance BankSwetal SwetalNo ratings yet

- BUDGETING KNOWLEDGE AND CHALLENGES OF SHS LEARNERS IN BANHS 11.06.22 NewDocument14 pagesBUDGETING KNOWLEDGE AND CHALLENGES OF SHS LEARNERS IN BANHS 11.06.22 NewAngeline AbainzaNo ratings yet

- LLC PDFDocument13 pagesLLC PDFaaron myrick100% (1)

- Sas Certified Accounting Technician Level 1 Module 2Document29 pagesSas Certified Accounting Technician Level 1 Module 2Plame GaseroNo ratings yet

- CSTUPDocument8 pagesCSTUPsaurabh singhNo ratings yet

- Presentation 2 - Audit of Intangible AssetsDocument27 pagesPresentation 2 - Audit of Intangible AssetsPaula De RuedaNo ratings yet