You might also like

- Experimental Verification of The Greenhouse Effect - Harde-Schnell-GHE-mDocument16 pagesExperimental Verification of The Greenhouse Effect - Harde-Schnell-GHE-mKarsten BrezinskyNo ratings yet

- The Investment Function in Banking and Financial-Services ManagementDocument18 pagesThe Investment Function in Banking and Financial-Services ManagementHaris FadžanNo ratings yet

- Economic Growth - The Loanable Funds DiagramDocument15 pagesEconomic Growth - The Loanable Funds DiagrammacromacronNo ratings yet

- Project ReportDocument59 pagesProject ReportAnuj YeleNo ratings yet

- RSKMGT Module II Credit Risk CH 2-Credit Scoring and Rating MethodsDocument12 pagesRSKMGT Module II Credit Risk CH 2-Credit Scoring and Rating MethodsAstha PandeyNo ratings yet

- 2022 LI MacroeconomicsDocument102 pages2022 LI MacroeconomicsAnshulNo ratings yet

- Madurai Kamaraj University: Capital Market Efficiency and Development of Capital Market in IndiaDocument11 pagesMadurai Kamaraj University: Capital Market Efficiency and Development of Capital Market in Indiachanus92No ratings yet

- Firm Attributes and Financial Reporting Timeliness of Consumer Goods Firms Listed in Nigeria Stock ExchangeDocument7 pagesFirm Attributes and Financial Reporting Timeliness of Consumer Goods Firms Listed in Nigeria Stock ExchangeInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- A Case Study of Greenfield Bangalore InternationalDocument11 pagesA Case Study of Greenfield Bangalore InternationalPrajitha Jinachandran T KNo ratings yet

- Lanco Capital BudgetDocument78 pagesLanco Capital BudgetDeepak AroraNo ratings yet

- Investment Decision - IciciDocument8 pagesInvestment Decision - Icicimohammed khayyumNo ratings yet

- Msme FinanceDocument55 pagesMsme FinanceGauri MittalNo ratings yet

- Plant-based meat startup Blue Tribe launches in IndiaDocument16 pagesPlant-based meat startup Blue Tribe launches in Indiaideation12345No ratings yet

- Bosch LTDDocument50 pagesBosch LTDmanishsngh24No ratings yet

- New Approaches To SME Finance Using Bank Account Information (Big Data)Document19 pagesNew Approaches To SME Finance Using Bank Account Information (Big Data)ADBI EventsNo ratings yet

- (Routledge Research in Journalism) Arjen Van Dalen, Helle Svensson, Antonis Kalogeropoulos, Erik Albæk, Claes H. de Vreese - Economic News - Informing The Inattentive Audience-Routledge (2018)Document215 pages(Routledge Research in Journalism) Arjen Van Dalen, Helle Svensson, Antonis Kalogeropoulos, Erik Albæk, Claes H. de Vreese - Economic News - Informing The Inattentive Audience-Routledge (2018)Nicholas WoyshnerNo ratings yet

- Hamden Audit FY20Document131 pagesHamden Audit FY20Helen BennettNo ratings yet

- Group 3 ProjectDocument27 pagesGroup 3 ProjectAbhishek DhruvNo ratings yet

- MPX 9.100 Quarter 4 PDFDocument1 pageMPX 9.100 Quarter 4 PDFsrinuvoodiNo ratings yet

- The Impact of Rural Banking On Poverty and Employment in IndiaDocument64 pagesThe Impact of Rural Banking On Poverty and Employment in IndiaKunal BagdeNo ratings yet

- Chapter 14 Portfolio Analysis CbcsDocument17 pagesChapter 14 Portfolio Analysis CbcsShivanshNo ratings yet

- GST Study on Consumer Behavior in MumbaiDocument85 pagesGST Study on Consumer Behavior in MumbaiSalil SarvagodNo ratings yet

- Corporate Law Scam in Yes BankDocument14 pagesCorporate Law Scam in Yes BankGeetha Revathi p100% (1)

- Investment Banking Financial Services 14MBAFM302Document59 pagesInvestment Banking Financial Services 14MBAFM302khushbuNo ratings yet

- Customer Satisfaction and Awarness On Public Sector Bank Sectors in TiruchirappalliDocument8 pagesCustomer Satisfaction and Awarness On Public Sector Bank Sectors in TiruchirappalliIAEME PublicationNo ratings yet

- A Study On Working Capital Management at Berger Paints LTDDocument6 pagesA Study On Working Capital Management at Berger Paints LTDdanny kanniNo ratings yet

- LSA Group launches Children's Education FundDocument20 pagesLSA Group launches Children's Education Fundlinda zyongweNo ratings yet

- SBI CRA - Regular Non-Trade ModelDocument24 pagesSBI CRA - Regular Non-Trade Modelaruntce_kumar9286No ratings yet

- Role of Investment Bankers in Indian Stock Market: An Empirical StudyDocument28 pagesRole of Investment Bankers in Indian Stock Market: An Empirical StudyashishNo ratings yet

- CP Project FinalDocument102 pagesCP Project FinalPriyanka PandeyNo ratings yet

- Investors Perception Towards Investment in Derivative SecuritiesDocument8 pagesInvestors Perception Towards Investment in Derivative SecuritiesStella OktavianiNo ratings yet

- Icici 1Document36 pagesIcici 1Yash AnandNo ratings yet

- Talent management roadmap for SMB growth and expansionDocument10 pagesTalent management roadmap for SMB growth and expansionElio ZerpaNo ratings yet

- A Comparative Study On Debt Mutual Funds With Reference To SBI and HDFC BanksDocument5 pagesA Comparative Study On Debt Mutual Funds With Reference To SBI and HDFC BanksEditor IJTSRDNo ratings yet

- TiC CMS RecsDocument4 pagesTiC CMS RecsJakob EmersonNo ratings yet

- SEBI Draft Regulations Investment AdvisorsDocument51 pagesSEBI Draft Regulations Investment AdvisorspbdkpkNo ratings yet

- An Extraordinary Company-HDFCDocument35 pagesAn Extraordinary Company-HDFCPrachi JainNo ratings yet

- An Analysis of The Indian Stock Market With GDP, Interest Rates and InflationDocument15 pagesAn Analysis of The Indian Stock Market With GDP, Interest Rates and InflationAadyaNo ratings yet

- A Study On Risk and Return Analysis On Selected Equities With Reference To Shriram InsighDocument14 pagesA Study On Risk and Return Analysis On Selected Equities With Reference To Shriram InsighEditor IJTSRDNo ratings yet

- Effect of Investment Appraisal On The Profitability of Quoted Consumer Goods Companies in NigeriaDocument61 pagesEffect of Investment Appraisal On The Profitability of Quoted Consumer Goods Companies in NigeriaPrecious Chioma AgulukaNo ratings yet

- FM CG Final PaperDocument4 pagesFM CG Final PaperAndy ShamNo ratings yet

- As 13 Accounting of InvestmentsDocument6 pagesAs 13 Accounting of InvestmentsSamridhi SinghalNo ratings yet

- BSC CSIT Final Year Project Report On Sword of Warrior Game Project ReportDocument52 pagesBSC CSIT Final Year Project Report On Sword of Warrior Game Project ReportGrey OldNo ratings yet

- Gold ETFDocument22 pagesGold ETFSaroj KhadangaNo ratings yet

- NISM IX Merchant Banking Short NotesDocument39 pagesNISM IX Merchant Banking Short NotesMayank KhuranaNo ratings yet

- Managerial Approaches and Organizational Performance of Multinational Enterprises in NigeriaDocument13 pagesManagerial Approaches and Organizational Performance of Multinational Enterprises in NigeriaCentral Asian StudiesNo ratings yet

- INTL729 Mod 02 ActivityDocument6 pagesINTL729 Mod 02 ActivityIshtiak AmadNo ratings yet

- Lloyds - Choice of Law, Choice of Jurisdiction and Service of SuitDocument5 pagesLloyds - Choice of Law, Choice of Jurisdiction and Service of SuitJose MNo ratings yet

- MPA AssignmentDocument14 pagesMPA AssignmentShreya RajkumarNo ratings yet

- MM2 Final Report Group 05Document16 pagesMM2 Final Report Group 05Himanshu Goyal100% (1)

- Consolidation of BanksDocument20 pagesConsolidation of BanksParvinder vidanaNo ratings yet

- Project Topic:-Mutual Fund: Paper NameDocument18 pagesProject Topic:-Mutual Fund: Paper NameJYOTI VERMA100% (1)

- Impact of Financial Literacy On Investment Behavior and Consumption BehaviourDocument17 pagesImpact of Financial Literacy On Investment Behavior and Consumption BehaviourFadhil ChiwangaNo ratings yet

- SPL Risk Related To Trading Financial InstrumentsDocument18 pagesSPL Risk Related To Trading Financial InstrumentsDenis DenisNo ratings yet

- Financial Performance Analysis of RSPL LtdDocument108 pagesFinancial Performance Analysis of RSPL LtdAvneesh RajputNo ratings yet

- Junior Assistant NotificationDocument7 pagesJunior Assistant NotificationNDTVNo ratings yet

- InsuranceDocument19 pagesInsuranceVAR FINANCIAL SERVICESNo ratings yet

- Msme Advances: Canara Bank Officers' Association Promotion Study Material - 2018Document67 pagesMsme Advances: Canara Bank Officers' Association Promotion Study Material - 2018Majhar HussainNo ratings yet

- GRI2009 EBrochureDocument27 pagesGRI2009 EBrochurenjaloualiNo ratings yet

- Role of Financial Derivatives in Financial Risk ManagementDocument16 pagesRole of Financial Derivatives in Financial Risk ManagementTYBMS-A 3001 Ansh AgarwalNo ratings yet

- Cross Cultural Management Portfolio GuidelineDocument4 pagesCross Cultural Management Portfolio GuidelineSana UllahNo ratings yet

- Its Organizational Culture and ND Jeff Bezos's Leadership Style?Document20 pagesIts Organizational Culture and ND Jeff Bezos's Leadership Style?Sana UllahNo ratings yet

- Coursework 1 HRM Report - Assignment BriefDocument7 pagesCoursework 1 HRM Report - Assignment BriefSana UllahNo ratings yet

- Coursework 1 HRM Report - Assignment BriefDocument7 pagesCoursework 1 HRM Report - Assignment BriefSana UllahNo ratings yet

- Milos Sprcic PDFDocument26 pagesMilos Sprcic PDFbaby0310No ratings yet

- Required Studies: Part Two: Continue Planning For The Project Started in Week 4, Using Project Planning PartDocument1 pageRequired Studies: Part Two: Continue Planning For The Project Started in Week 4, Using Project Planning PartSana UllahNo ratings yet

- Module Code Module Title Credit: KnowledgeDocument42 pagesModule Code Module Title Credit: KnowledgeSana UllahNo ratings yet

- Required Studies: Part Two: Continue Planning For The Project Started in Week 4, Using Project Planning PartDocument1 pageRequired Studies: Part Two: Continue Planning For The Project Started in Week 4, Using Project Planning PartSana UllahNo ratings yet

- Accounting Information Systems Chapter 7Document19 pagesAccounting Information Systems Chapter 7J PNo ratings yet

- Cendana - CITYZEN HILLS - 291123-1Document5 pagesCendana - CITYZEN HILLS - 291123-1Oky Arnol SunjayaNo ratings yet

- Principles of Managerial Finance Chapter 5 Time Value of MoneyDocument45 pagesPrinciples of Managerial Finance Chapter 5 Time Value of MoneyJoshNo ratings yet

- Faq On NeftDocument3 pagesFaq On Neftagpatil234No ratings yet

- The Impact of Mobile Bank On Economic Development (Case Study Telecommunication and Banks in Mogadashu-Somalia)Document47 pagesThe Impact of Mobile Bank On Economic Development (Case Study Telecommunication and Banks in Mogadashu-Somalia)NguyenTrung KienNo ratings yet

- Frequently Used Finacle Commands Finacle Commands Finacle Wiki Finacle Tutorial Amp Finacle Training For BankersDocument5 pagesFrequently Used Finacle Commands Finacle Commands Finacle Wiki Finacle Tutorial Amp Finacle Training For BankersGeraldine NkankumeNo ratings yet

- December 2022Document2 pagesDecember 2022Zolani100% (1)

- Appendices of Section B Bank Branch Audit Guidance NoteDocument151 pagesAppendices of Section B Bank Branch Audit Guidance Noteshyamsunder bajajNo ratings yet

- G.R. No. 217411 - PHILIPPINE BANK OF COMMUNICATIONS, PETITIONER, VS. RIA DE GUZMAN RIVERA, RESPONDENT.D E C I S I O N - Supreme Court E-LibraryDocument10 pagesG.R. No. 217411 - PHILIPPINE BANK OF COMMUNICATIONS, PETITIONER, VS. RIA DE GUZMAN RIVERA, RESPONDENT.D E C I S I O N - Supreme Court E-Librarymarvinnino888No ratings yet

- Snow Hill Wharf Phase 2&3Document11 pagesSnow Hill Wharf Phase 2&3cjchuaNo ratings yet

- Super Advantage SOCDocument3 pagesSuper Advantage SOCdip45150No ratings yet

- The Payment System and Financial InstrumentsDocument27 pagesThe Payment System and Financial InstrumentsAllen GonzagaNo ratings yet

- Receivables Factoring and Performance of Private Finance Companies in Kenya: A Case of Private Finance Companies in Nairobi City CountyDocument13 pagesReceivables Factoring and Performance of Private Finance Companies in Kenya: A Case of Private Finance Companies in Nairobi City CountyLong Ngọc GiangNo ratings yet

- Partnership Profits and LiabilitiesDocument7 pagesPartnership Profits and LiabilitiesHeavens MupedzisaNo ratings yet

- Fin 464 Final TSA PDF PDFDocument67 pagesFin 464 Final TSA PDF PDFArahf KashemiNo ratings yet

- Sources and Types of Short and Long Term Business FinancingDocument23 pagesSources and Types of Short and Long Term Business FinancingNishant TutejaNo ratings yet

- Canary - 2023-02-18 170231.l505964Document53 pagesCanary - 2023-02-18 170231.l505964SAID k sNo ratings yet

- (Studies in The Political Economy of Public Policy) Philip Mader-The Political Economy of Microfinance - Financializing Poverty-Palgrave Macmillan (2015)Document297 pages(Studies in The Political Economy of Public Policy) Philip Mader-The Political Economy of Microfinance - Financializing Poverty-Palgrave Macmillan (2015)VAY EntertainmentNo ratings yet

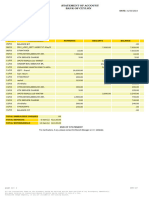

- Statement 28949Document4 pagesStatement 28949niyameddinagayev53No ratings yet

- StatementDocument1 pageStatementfert certNo ratings yet

- Financial Assets at Fair Value Through Profit or LossDocument13 pagesFinancial Assets at Fair Value Through Profit or LossALEJANDRE, Chris Shaira M.No ratings yet

- Fabm2 Q2 M3 - 4Document9 pagesFabm2 Q2 M3 - 4Zeus MalicdemNo ratings yet

- Account Opening Formalities at PBLDocument4 pagesAccount Opening Formalities at PBLMd Mohsin AliNo ratings yet

- Axis Bank Young Banker Programme Internship Diary: Suneet Kumar SinghDocument9 pagesAxis Bank Young Banker Programme Internship Diary: Suneet Kumar Singhsrinivas4949No ratings yet

- Varo Bank statement transaction detailsDocument2 pagesVaro Bank statement transaction detailsNatalie RichardsonNo ratings yet

- Wise Deposit Note 662136227 1003987913 enDocument2 pagesWise Deposit Note 662136227 1003987913 encavNo ratings yet

- Claim Process Rupay PMJDY Insurance Program 23-24Document21 pagesClaim Process Rupay PMJDY Insurance Program 23-24Chandan GuptaNo ratings yet

- Annual Report 2019Document306 pagesAnnual Report 2019Mohammad ShahjahanNo ratings yet

- BSP Receivership Authority Without Prior HearingDocument1 pageBSP Receivership Authority Without Prior HearingRoseller SasisNo ratings yet

- Rift Valley University Assela CampusDocument3 pagesRift Valley University Assela CampusTeshomeNo ratings yet