You might also like

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Sunway T4 (TX4014) - Tax Computation (Business Income)Document4 pagesSunway T4 (TX4014) - Tax Computation (Business Income)Ee LynnNo ratings yet

- Questions Business IncomeDocument8 pagesQuestions Business IncomeMbeiza MariamNo ratings yet

- Accounting assignment - Income statements and discontinued operationsDocument7 pagesAccounting assignment - Income statements and discontinued operationshananNo ratings yet

- Acb21103 Tutorial Business Income 2023Document8 pagesAcb21103 Tutorial Business Income 2023alifarhanah6No ratings yet

- Management Accounting (Regular) : Instructions: 1) Attempt All The Sections According To Internal ChoicesDocument32 pagesManagement Accounting (Regular) : Instructions: 1) Attempt All The Sections According To Internal ChoicesSudhir SoudagarNo ratings yet

- TAXN 1016 FE - Long ProblemsDocument11 pagesTAXN 1016 FE - Long ProblemsCrystel Kate MananganNo ratings yet

- Profit Prior To IncorporationDocument12 pagesProfit Prior To IncorporationKalash SharmaNo ratings yet

- PT Cagak financial statement 2020Document9 pagesPT Cagak financial statement 2020Laras sukma nurani tirtawidjajaNo ratings yet

- Ch.6-Tutorial 1Document3 pagesCh.6-Tutorial 1NURSABRINA BINTI ROSLI (BG)No ratings yet

- TF PARCOR FINAL QUIZ SOLUTIONSDocument3 pagesTF PARCOR FINAL QUIZ SOLUTIONSSam VNo ratings yet

- ICON College of Technology and Management Course: Btec HND in Business, Unit 12: TaxationDocument6 pagesICON College of Technology and Management Course: Btec HND in Business, Unit 12: TaxationmuhammadislamkhanNo ratings yet

- c4 Grande Finale Solving 2023 Nov (Set 1)Document7 pagesc4 Grande Finale Solving 2023 Nov (Set 1)charlesmicky82No ratings yet

- Illustrative Questions: Classic TutorsDocument20 pagesIllustrative Questions: Classic TutorsTbabaNo ratings yet

- Pre-Post Incorporation ProfitsDocument3 pagesPre-Post Incorporation ProfitsMahima tiwariNo ratings yet

- Far01 - The Financial Statements PresentationDocument10 pagesFar01 - The Financial Statements PresentationRNo ratings yet

- Assessment of Companies (Solution) : Solution 1 M/s John Morris IncDocument8 pagesAssessment of Companies (Solution) : Solution 1 M/s John Morris IncIQBALNo ratings yet

- Sample Problem IncomeDocument4 pagesSample Problem IncomeJoyce Ann Agdippa Barcelona100% (1)

- Tutorial 5 A212 Foreign OperationsDocument9 pagesTutorial 5 A212 Foreign OperationsFatinNo ratings yet

- VELLORE, CHENNAI-632 002: Answer The Following QuestionsDocument5 pagesVELLORE, CHENNAI-632 002: Answer The Following QuestionsJayanthiNo ratings yet

- Ventura, Mary Mickaella R - Comprehensive Income - p.88 - Group3Document7 pagesVentura, Mary Mickaella R - Comprehensive Income - p.88 - Group3Mary VenturaNo ratings yet

- Activity 1Document4 pagesActivity 1Louisa de VeraNo ratings yet

- Prepare SCI for Service and MerchandisingDocument10 pagesPrepare SCI for Service and MerchandisingJessamine Romano AplodNo ratings yet

- Soal Tugas Akm Is - ST o FP - CFDocument6 pagesSoal Tugas Akm Is - ST o FP - CFElyssa Fiqri Fauziah0% (1)

- H.B Commerce Classes operating activities worksheetDocument3 pagesH.B Commerce Classes operating activities worksheetPavan BachaniNo ratings yet

- Problem Ratio 2022Document1 pageProblem Ratio 2022Mohd shariqNo ratings yet

- Tutorial 2: Swedish CompanyDocument5 pagesTutorial 2: Swedish Companyszh saNo ratings yet

- Statement of Comprehensive IncomeDocument4 pagesStatement of Comprehensive Incomebobo tangaNo ratings yet

- Asdos Pert 2Document2 pagesAsdos Pert 2mutiaoooNo ratings yet

- Universiti Tunku Abdul Rahman Faculty of Business and Finance Ubaf 2113 Advanced Financial Accounting (Jan 2021) Tutorial 2Document3 pagesUniversiti Tunku Abdul Rahman Faculty of Business and Finance Ubaf 2113 Advanced Financial Accounting (Jan 2021) Tutorial 2KAY PHINE NGNo ratings yet

- Business Income TutorialDocument5 pagesBusiness Income TutorialzulfikriNo ratings yet

- TAX 667 TOPIC 7 Trade Association & ClubsDocument51 pagesTAX 667 TOPIC 7 Trade Association & Clubszarif nezuko100% (1)

- Malik Group of Companies (Disposal + Acquisition) : Cfap 1: A A F RDocument1 pageMalik Group of Companies (Disposal + Acquisition) : Cfap 1: A A F R.No ratings yet

- 02 Financing Decisions - Leverages - Practice SheetDocument22 pages02 Financing Decisions - Leverages - Practice SheetPatrick LoboNo ratings yet

- Lec3 - Chap3 - Class Exercise 3aDocument3 pagesLec3 - Chap3 - Class Exercise 3aMEGAKARTIKA MISRULNo ratings yet

- Lotus Income StatementDocument6 pagesLotus Income StatementJoseph AsisNo ratings yet

- Comprehensive Income & NcahsDocument6 pagesComprehensive Income & NcahsNuarin JJ67% (3)

- Chapter 2Document40 pagesChapter 2ellyzamae quiraoNo ratings yet

- ACC3024 Tutorial 4 Q (Apr 2023)Document3 pagesACC3024 Tutorial 4 Q (Apr 2023)Shermaine WanNo ratings yet

- Cash Flow ProblemsDocument10 pagesCash Flow Problemsmuhammad shamsadNo ratings yet

- 74752079-fdc8-433f-9bdf-7ebc80928004Document25 pages74752079-fdc8-433f-9bdf-7ebc80928004diviananaslinNo ratings yet

- Illustration 1Document9 pagesIllustration 1Thanos The titanNo ratings yet

- TP1-W2-S3-R0 Sri Annisa KatariDocument3 pagesTP1-W2-S3-R0 Sri Annisa Katarisri annisa katariNo ratings yet

- I1.2-Financial Reporting QPDocument8 pagesI1.2-Financial Reporting QPConstantin NdahimanaNo ratings yet

- Account 1srsDocument5 pagesAccount 1srsNayan KcNo ratings yet

- Comprehensive QuizDocument4 pagesComprehensive QuizBea LadaoNo ratings yet

- Statement of Changes in Comprehensive IncomeDocument33 pagesStatement of Changes in Comprehensive Incomeellyzamae quiraoNo ratings yet

- Ia Assignment 2Document2 pagesIa Assignment 2Shekinah SesbrenoNo ratings yet

- ACCT2062 SIM Final Assessment (Sem 2 2020)Document15 pagesACCT2062 SIM Final Assessment (Sem 2 2020)IkramNo ratings yet

- Intermediate Accounting 2 Topic: Unearned RevenuesDocument5 pagesIntermediate Accounting 2 Topic: Unearned RevenuesJhazreel BiasuraNo ratings yet

- FABM2 Chapter2Document7 pagesFABM2 Chapter2Archie CampomanesNo ratings yet

- ACC401-Basic Conso SPLDocument4 pagesACC401-Basic Conso SPLOhene Asare PogastyNo ratings yet

- Common Size Statement AnalysisDocument2 pagesCommon Size Statement AnalysisRevati ShindeNo ratings yet

- Tax317 Ctmay2022Document10 pagesTax317 Ctmay2022sharifah nurshahira sakinaNo ratings yet

- Special Allowable Itemized DeductionsDocument13 pagesSpecial Allowable Itemized DeductionsSandia EspejoNo ratings yet

- Pr. 4-146-Income StatementDocument13 pagesPr. 4-146-Income StatementElene SamnidzeNo ratings yet

- Jun 2019 QDocument9 pagesJun 2019 Qsiti dalinaNo ratings yet

- Patrice R. Barquilla 12 Gandionco Business Finance CHAPTER 2 ASSIGNMENTDocument12 pagesPatrice R. Barquilla 12 Gandionco Business Finance CHAPTER 2 ASSIGNMENTJohnrick RabaraNo ratings yet

- Statement of Comprehensive Income: Problem 1: True or FalseDocument17 pagesStatement of Comprehensive Income: Problem 1: True or FalsePaula Bautista100% (3)

- Acc5115 - Intermediate Financial Reporting Statement of Comprehensive Income and Changes in Owner'S Equity Problem ADocument6 pagesAcc5115 - Intermediate Financial Reporting Statement of Comprehensive Income and Changes in Owner'S Equity Problem ARachel LuberiaNo ratings yet

- Industrial Building Allowance (IBA)Document32 pagesIndustrial Building Allowance (IBA)Ee LynnNo ratings yet

- Sunway T3 (TX4014) Tax Computation 2020Document3 pagesSunway T3 (TX4014) Tax Computation 2020Ee LynnNo ratings yet

- Revision (CA MCQ)Document2 pagesRevision (CA MCQ)Ee LynnNo ratings yet

- Sunway T1 (TX4014) - Business IncomeDocument4 pagesSunway T1 (TX4014) - Business IncomeEe LynnNo ratings yet

- Sunway T2 Business Expense 1 2Document4 pagesSunway T2 Business Expense 1 2Ee LynnNo ratings yet

- 1703424245773Document142 pages1703424245773kpnandini12No ratings yet

- JP Morgan Top PicksDocument17 pagesJP Morgan Top PicksysnngncNo ratings yet

- Using Derivatives: What Seniors Must KnowDocument4 pagesUsing Derivatives: What Seniors Must KnowMohammad Sameer AnsariNo ratings yet

- How to Get Rich (It's Not What You ExpectDocument12 pagesHow to Get Rich (It's Not What You ExpectSaran BaskarNo ratings yet

- Suggested CAP II Group II June 2023Document61 pagesSuggested CAP II Group II June 2023pratyushmudbhari340No ratings yet

- Financial Management Core Concepts 3rd Edition Raymond Brooks Test Bank 1Document38 pagesFinancial Management Core Concepts 3rd Edition Raymond Brooks Test Bank 1tammie100% (42)

- FINAL Q4 22 Shareholder LetterDocument16 pagesFINAL Q4 22 Shareholder LetterJulia JohnsonNo ratings yet

- FIN081 - P2 - Q2 - Receivable Management - AnswersDocument7 pagesFIN081 - P2 - Q2 - Receivable Management - AnswersShane QuintoNo ratings yet

- The Harrod - Domar Growth Model and Its Implications For Economic Development in VietnamDocument7 pagesThe Harrod - Domar Growth Model and Its Implications For Economic Development in VietnamBery CoryNo ratings yet

- Cutting and shaping equipment optimizationDocument9 pagesCutting and shaping equipment optimizationLuiz HenriqueNo ratings yet

- Vat or NotDocument3 pagesVat or Notkim JinNo ratings yet

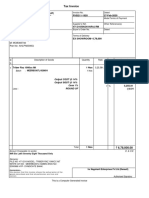

- Tax InvoiceDocument1 pageTax Invoicesourabh choubeyNo ratings yet

- Marketing NotesDocument4 pagesMarketing NotesChristineNo ratings yet

- LGU:IMELDA Province: Zamboanga Sibugay: I. Compliance To Revised BPLS StandardsDocument2 pagesLGU:IMELDA Province: Zamboanga Sibugay: I. Compliance To Revised BPLS StandardsLemuel MejaresNo ratings yet

- Wallstreetjournal 20180612 TheWallStreetJournal PDFDocument42 pagesWallstreetjournal 20180612 TheWallStreetJournal PDFDhananjayan JayabalNo ratings yet

- Group - 2 - NBFC REPORTDocument13 pagesGroup - 2 - NBFC REPORTSheetalNo ratings yet

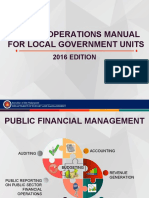

- DBM Bom2016sdgDocument17 pagesDBM Bom2016sdgFerdie RulonaNo ratings yet

- Dropship Suspend AppealDocument10 pagesDropship Suspend AppealenesahvalekinciNo ratings yet

- Break Even AnalysisDocument20 pagesBreak Even AnalysisstudentoneNo ratings yet

- Dalmia Bharat Sugar and Industries Ltd.Document19 pagesDalmia Bharat Sugar and Industries Ltd.Shweta GargNo ratings yet

- RA No. 10667Document16 pagesRA No. 10667Sab Amantillo BorromeoNo ratings yet

- ReviewerDocument7 pagesReviewerKaye Mariz TolentinoNo ratings yet

- Banking Law Syllabus For 2020-2021Document6 pagesBanking Law Syllabus For 2020-2021Sarah Cruz100% (2)

- Lesson 2: Learning ObjectiveDocument4 pagesLesson 2: Learning ObjectiveDante SausaNo ratings yet

- SE ContractDocument21 pagesSE Contractaugusta.mironNo ratings yet

- LAP App Form IDFC Bank Bucket 3 R3Document13 pagesLAP App Form IDFC Bank Bucket 3 R3jyotigunu817No ratings yet

- ICIS World Base Oils Outlook 2020Document18 pagesICIS World Base Oils Outlook 2020Sameh Radwan100% (1)

- Powerpoint Presentation On Usa EconomyDocument19 pagesPowerpoint Presentation On Usa EconomyPiyush_jain00450% (2)

- 3.3.1 Functions That Are Integral To Business: Financial Reporting SolutionDocument15 pages3.3.1 Functions That Are Integral To Business: Financial Reporting SolutionRITZ BROWNNo ratings yet

- Credit Card Enrollment Cabaluna 2022Document3 pagesCredit Card Enrollment Cabaluna 2022Tracy AdraNo ratings yet