You might also like

- Workshop Book 2019Document62 pagesWorkshop Book 2019Book JokerNo ratings yet

- Barmax Mpre Study Guide: V. Duty of Competence (6% To 12%) - A Lawyer Shall Provide Competent Representation To ADocument1 pageBarmax Mpre Study Guide: V. Duty of Competence (6% To 12%) - A Lawyer Shall Provide Competent Representation To ATestMaxIncNo ratings yet

- Activity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Document11 pagesActivity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Paupau100% (1)

- Management Accounting Techniques CompilationDocument40 pagesManagement Accounting Techniques CompilationGracelle Mae Oraller100% (1)

- Activities For English Language Learners Across The CurriculumDocument136 pagesActivities For English Language Learners Across The CurriculumJulio César González100% (3)

- 21 Degrees SagittariusDocument11 pages21 Degrees Sagittariusstrength17No ratings yet

- Business Continuity Management Systems: Implementation and certification to ISO 22301From EverandBusiness Continuity Management Systems: Implementation and certification to ISO 22301No ratings yet

- 20201st Sem Syllabus Auditing Assurance PrinciplesDocument10 pages20201st Sem Syllabus Auditing Assurance PrinciplesJamie Rose AragonesNo ratings yet

- Activity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0Document6 pagesActivity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0PaupauNo ratings yet

- PAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesDocument9 pagesPAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesPaupauNo ratings yet

- ACP 314 Auditing and Assurance Principle Rev. 0 1st Sem SY 2020-2021Document12 pagesACP 314 Auditing and Assurance Principle Rev. 0 1st Sem SY 2020-2021Jerah TorrejosNo ratings yet

- The Impact of Technology On Learning EnvironmnentDocument7 pagesThe Impact of Technology On Learning EnvironmnentAhmad Ali75% (4)

- BSMA STRAT AUD SyllabusDocument7 pagesBSMA STRAT AUD SyllabusDSAW VALERIO100% (3)

- The Whig Interpretation of History: Herbert Butterfield's CritiqueDocument82 pagesThe Whig Interpretation of History: Herbert Butterfield's CritiqueBetina PeppinaNo ratings yet

- Meditation To Bring Prosperity To Your Life - KundaliniDocument5 pagesMeditation To Bring Prosperity To Your Life - KundaliniErica Yang100% (1)

- MAS-04 Relevant CostingDocument10 pagesMAS-04 Relevant CostingPaupauNo ratings yet

- 1st Semester AY2022-2023 - ACCO 30053 - AUDITING AND CONCEPTS PART 1 - Revised - SyllabusDocument5 pages1st Semester AY2022-2023 - ACCO 30053 - AUDITING AND CONCEPTS PART 1 - Revised - Syllabusrachel banana hammockNo ratings yet

- ACC 213 Strategic Cost Management Rev. 0 1st Sem SY 2019-2020Document9 pagesACC 213 Strategic Cost Management Rev. 0 1st Sem SY 2019-2020Jel-Anndrei LopezNo ratings yet

- Barangay Health Workers' Benefits and Incentives ActDocument2 pagesBarangay Health Workers' Benefits and Incentives ActColleen De Guia Babalcon100% (1)

- Financial Analysis and Reporting SyllabusDocument9 pagesFinancial Analysis and Reporting SyllabusJpoy Rivera100% (4)

- Philippine College of Science and Technology Detailed Teaching SyllabusDocument14 pagesPhilippine College of Science and Technology Detailed Teaching SyllabusCharo Gironella67% (6)

- Detailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Document15 pagesDetailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Charo Gironella100% (3)

- Activity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Document12 pagesActivity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Paupau0% (1)

- Aud 4Document13 pagesAud 4PaupauNo ratings yet

- Answer in Act. 2 For Cash-receivables-InventoriesDocument10 pagesAnswer in Act. 2 For Cash-receivables-InventoriesPaupauNo ratings yet

- BSA 3104 - Governance, Business Ethics, Risk Management and Internal ControlDocument17 pagesBSA 3104 - Governance, Business Ethics, Risk Management and Internal ControlGERWIN REQUIROSO100% (1)

- Activity - Consolidated Financial Statement Part 1Document10 pagesActivity - Consolidated Financial Statement Part 1PaupauNo ratings yet

- Audit 4 - Audit in Specialized IndustryDocument7 pagesAudit 4 - Audit in Specialized IndustryPaupauNo ratings yet

- Detailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Document15 pagesDetailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Charo Gironella100% (1)

- Detailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Document12 pagesDetailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Charo Gironella100% (3)

- Assessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerDocument12 pagesAssessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerPaupauNo ratings yet

- Kaplan - Reading RicoeurDocument0 pagesKaplan - Reading RicoeuryopertNo ratings yet

- OBE Syllabus Operations Management With TQM San Francisco CollegeDocument4 pagesOBE Syllabus Operations Management With TQM San Francisco CollegeJerome SaavedraNo ratings yet

- Conceptual Framework Basic Acctngt 1 OBE SyllabusDocument6 pagesConceptual Framework Basic Acctngt 1 OBE SyllabusPatricia may RiveraNo ratings yet

- Managerial Accounting SyllabusDocument5 pagesManagerial Accounting SyllabusJpoy RiveraNo ratings yet

- OBE Acctg 15 BSA 2019Document15 pagesOBE Acctg 15 BSA 2019Airalyn PinlacNo ratings yet

- Republic Central Colleges: Bachelor of Science in Management Accounting / Bachelor of Science in AccountancyDocument11 pagesRepublic Central Colleges: Bachelor of Science in Management Accounting / Bachelor of Science in AccountancyPaupauNo ratings yet

- New Era University: Financial Accounting & Reporting (Acctg01-19) Course PlanDocument7 pagesNew Era University: Financial Accounting & Reporting (Acctg01-19) Course PlanEj UlangNo ratings yet

- ACC 111 Financial Accounting SyllabusDocument11 pagesACC 111 Financial Accounting SyllabusJhanna Vee DamaleNo ratings yet

- Acc 411 - AssuranceDocument9 pagesAcc 411 - AssurancemildredNo ratings yet

- Accounting Plus Syllabus Explains Finance, Management and Marketing ConceptsDocument7 pagesAccounting Plus Syllabus Explains Finance, Management and Marketing ConceptsLambaco Earl AdamNo ratings yet

- M. Mendoza - Aud03-Syllabus (Sy 2021-2022)Document9 pagesM. Mendoza - Aud03-Syllabus (Sy 2021-2022)Mark Domingo MendozaNo ratings yet

- Revised Obe SyllabusDocument19 pagesRevised Obe SyllabusFrances Mikayla EnriquezNo ratings yet

- ACT 1104 Intermediate Accounting - AY1920Document19 pagesACT 1104 Intermediate Accounting - AY1920adrianneNo ratings yet

- Jose Rizal Memorial State University: College of Business AdministrationDocument4 pagesJose Rizal Memorial State University: College of Business AdministrationJermebie LabadlabadNo ratings yet

- Accounting 1 BSA OBE Funda 1Document5 pagesAccounting 1 BSA OBE Funda 1Yuri Walter AkiateNo ratings yet

- IRLL Course File 2023Document14 pagesIRLL Course File 2023Hema LathaNo ratings yet

- College of Business and Accountancy: University of Nueva CaceresDocument23 pagesCollege of Business and Accountancy: University of Nueva CaceresJoy AlinoodNo ratings yet

- M. MENDOZA - AUD05-SYLLABUS 2nd SEM (SY 2021-2022)Document14 pagesM. MENDOZA - AUD05-SYLLABUS 2nd SEM (SY 2021-2022)Mark Domingo MendozaNo ratings yet

- ACT 1124 - Financial ManagementDocument13 pagesACT 1124 - Financial ManagementRonald LeabresNo ratings yet

- Acctg 150 Course Guide 1st Sem 21 22 Fin. Acctg. ReportingDocument19 pagesAcctg 150 Course Guide 1st Sem 21 22 Fin. Acctg. ReportingVivian TamerayNo ratings yet

- Syllabus - Introduction To Financial Accounting - SY 2023 2024Document11 pagesSyllabus - Introduction To Financial Accounting - SY 2023 2024Saila mae SurioNo ratings yet

- Bactng1 Syllabus UbDocument19 pagesBactng1 Syllabus UbvicenteferrerNo ratings yet

- Manual Final EditingDocument9 pagesManual Final EditingLyssseeeeNo ratings yet

- 1 BSMA ProgramDocument11 pages1 BSMA ProgramRichamieNo ratings yet

- New Era University: Auditing & Assurance: Concept and Applications 1 Course PlanDocument8 pagesNew Era University: Auditing & Assurance: Concept and Applications 1 Course PlanPilyo HizerNo ratings yet

- AC315 Auditing & Assurance Principles-RPT-OBE-sem17 Theory HalfDocument15 pagesAC315 Auditing & Assurance Principles-RPT-OBE-sem17 Theory HalfLalaine De JesusNo ratings yet

- Syllabus - ACCBP 100 CompleteDocument10 pagesSyllabus - ACCBP 100 CompleteCleah WaskinNo ratings yet

- Department of Accounting Education ACC 111 - Course SyllabusDocument10 pagesDepartment of Accounting Education ACC 111 - Course Syllabuslhyn JasarenoNo ratings yet

- ACCN13B Management Advisory Services 1 Course SyllabusDocument4 pagesACCN13B Management Advisory Services 1 Course SyllabusKathrine Nicole FernanNo ratings yet

- ACC 225 Syllabus Explains Business Laws CourseDocument13 pagesACC 225 Syllabus Explains Business Laws CourseFRAULIEN GLINKA FANUGAONo ratings yet

- MA Masters SyllabusDocument12 pagesMA Masters SyllabusRock BottomNo ratings yet

- Act1102 - Cfas - Course SyllabusDocument19 pagesAct1102 - Cfas - Course SyllabusFrancein CequenaNo ratings yet

- ACT1122 Conceptual Framework and Accounting Standards - Revised - 2024Document14 pagesACT1122 Conceptual Framework and Accounting Standards - Revised - 2024Migz labianoNo ratings yet

- Syllabus ACP 312 Accounting For Business CombinationsDocument9 pagesSyllabus ACP 312 Accounting For Business CombinationsirahQNo ratings yet

- Syllabus Cost PDFDocument4 pagesSyllabus Cost PDFRongNo ratings yet

- Department of Accounting Education ACCBP 100 - Course SyllabusDocument13 pagesDepartment of Accounting Education ACCBP 100 - Course SyllabusKristine Joy EbradoNo ratings yet

- Document Course Code / Title: College of Business Administration and AccountancyDocument3 pagesDocument Course Code / Title: College of Business Administration and AccountancyJose MagallanesNo ratings yet

- 2020 FMGT 1013 - Financial Management RevisedDocument9 pages2020 FMGT 1013 - Financial Management RevisedYANIII12345No ratings yet

- 00 AAPRINCIPLES - SyllabusDocument13 pages00 AAPRINCIPLES - SyllabusSamuel GarciaNo ratings yet

- Detailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Document20 pagesDetailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Blecemie MonteraNo ratings yet

- La Salette University Management Accounting Course PlanDocument16 pagesLa Salette University Management Accounting Course PlanRolly BaniquedNo ratings yet

- ACCT 1046 - Intermediate Accounting 1Document10 pagesACCT 1046 - Intermediate Accounting 1Rhianne ManicapNo ratings yet

- ACCN02B Partnership and Corporation Accounting SyllabusDocument5 pagesACCN02B Partnership and Corporation Accounting SyllabusJoan TorresNo ratings yet

- Pe 1 - Path Fit1 - BsmaDocument10 pagesPe 1 - Path Fit1 - BsmaMary Joy Silverio MolinaNo ratings yet

- Far Eastern University: VisionDocument11 pagesFar Eastern University: VisionYoung MetroNo ratings yet

- Midterms Duration: Week 1 & 2: USL Expects You To Do The FollowingDocument52 pagesMidterms Duration: Week 1 & 2: USL Expects You To Do The FollowingZel BNo ratings yet

- ACC 124 - Conceptual Framework and Intermediate Accounting 1 SyllabusDocument15 pagesACC 124 - Conceptual Framework and Intermediate Accounting 1 SyllabusTrisha AlmiranteNo ratings yet

- Acctg 201A Course GuideDocument13 pagesAcctg 201A Course GuideDomingo Bay-anNo ratings yet

- Activity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)Document1 pageActivity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)PaupauNo ratings yet

- Activity - Derivatives and Hedging Accounting (PFRS 9)Document8 pagesActivity - Derivatives and Hedging Accounting (PFRS 9)PaupauNo ratings yet

- Activity in E3 - LiabilitiesDocument9 pagesActivity in E3 - LiabilitiesPaupau100% (1)

- Actvity 4 in Auditing 4 - Biological AssetsDocument3 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Activity On Application ControlDocument5 pagesActivity On Application ControlPaupauNo ratings yet

- Accounting for Cash, Receivables and InventoriesDocument12 pagesAccounting for Cash, Receivables and InventoriesPaupau100% (1)

- Answer in Prelim Exam E4.Document12 pagesAnswer in Prelim Exam E4.PaupauNo ratings yet

- Activity 2 Audit On CISDocument4 pagesActivity 2 Audit On CISPaupauNo ratings yet

- Implement Strategy StructureDocument21 pagesImplement Strategy StructurePaupau100% (1)

- Answers - Partnership AccountingDocument14 pagesAnswers - Partnership AccountingPaupauNo ratings yet

- Assignment On PCF and Bank ReconDocument2 pagesAssignment On PCF and Bank ReconPaupauNo ratings yet

- AFAR ReviewDocument11 pagesAFAR ReviewPaupauNo ratings yet

- 6 Business StrategyDocument27 pages6 Business StrategyPaupauNo ratings yet

- Special Purpose Audit Procedures and ReportsDocument6 pagesSpecial Purpose Audit Procedures and ReportsPaupauNo ratings yet

- Activity 3 - CAATsDocument4 pagesActivity 3 - CAATsPaupauNo ratings yet

- Estimated transaction price methods and entries for consignment salesDocument7 pagesEstimated transaction price methods and entries for consignment salesPaupauNo ratings yet

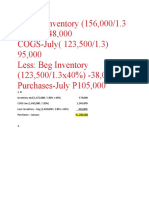

- Ending Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000Document1 pageEnding Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000PaupauNo ratings yet

- Home Office, Agency and Branch AccountingDocument17 pagesHome Office, Agency and Branch AccountingPaupauNo ratings yet

- Actvity 4 in Auditing 4 - Biological AssetsDocument2 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Assessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerDocument12 pagesAssessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerPaupauNo ratings yet

- Definition of Necessity EntrepreneurshipDocument8 pagesDefinition of Necessity EntrepreneurshipOmriNo ratings yet

- IATF 16949 Lead Auditor CourseDocument1 pageIATF 16949 Lead Auditor Coursemhaseeb359081No ratings yet

- Lighting - Education - Science-ZumtobelDocument60 pagesLighting - Education - Science-ZumtobelManoj IllangasooriyaNo ratings yet

- Elementary Teacher Resume ObjectiveDocument1 pageElementary Teacher Resume ObjectiveDolores Mayuga PanchoNo ratings yet

- Palompon College Thesis Advising ContractDocument10 pagesPalompon College Thesis Advising ContractLhielizette Claire P. SarmientoNo ratings yet

- Are Children OppressedDocument8 pagesAre Children Oppressedlaura simpsonNo ratings yet

- Analisis Kemampuan Literasi Matematika Siswa Kelas X Berdasarkan Kemampuan MatematikaDocument9 pagesAnalisis Kemampuan Literasi Matematika Siswa Kelas X Berdasarkan Kemampuan MatematikaDzulfiqor SatriaNo ratings yet

- Week 4 Discussion 1Document2 pagesWeek 4 Discussion 1api-528651903No ratings yet

- E-18 Why Do Children MisbehaveDocument2 pagesE-18 Why Do Children MisbehaveHermann Dejero LozanoNo ratings yet

- Dynamic Interactions of Environment, Brain and BehaviorDocument40 pagesDynamic Interactions of Environment, Brain and BehaviorLakshmi ManoharNo ratings yet

- Group 7: Hitesh Kumar Rachit Rathi Neha Aggarwal Shubhangi Asthana Abhishek DimriDocument16 pagesGroup 7: Hitesh Kumar Rachit Rathi Neha Aggarwal Shubhangi Asthana Abhishek DimriRachitNo ratings yet

- FijiTimes - Dec 14 2012 WebDocument48 pagesFijiTimes - Dec 14 2012 WebfijitimescanadaNo ratings yet

- Job EvaluationDocument5 pagesJob EvaluationShanna MillsNo ratings yet

- DAILY LESSON LOG OF M7NS-if-1 (Week Six - Day Four)Document4 pagesDAILY LESSON LOG OF M7NS-if-1 (Week Six - Day Four)Pablo JimeneaNo ratings yet

- ATC-19 Structural Response Modification FactorsDocument3 pagesATC-19 Structural Response Modification Factorsmassoud1282No ratings yet

- Planning For Resolving Conflict in The Workplace Final DraftDocument3 pagesPlanning For Resolving Conflict in The Workplace Final Draftapi-302123230No ratings yet

- Higher Unit 18 Topic TestDocument19 pagesHigher Unit 18 Topic TestLouis Sharrock50% (2)

- Evolution's First Philosopher: Continuity of Nature John Dewey and TheDocument170 pagesEvolution's First Philosopher: Continuity of Nature John Dewey and TheMicaela Silvestre Bastidas100% (1)

- Majina JKT Mujibu Kambi Zote 2016Document714 pagesMajina JKT Mujibu Kambi Zote 2016InnocentLuganoMbwaga67% (3)

- Unit IX - Educational Administration - Evaluation of Program - LearnersDocument14 pagesUnit IX - Educational Administration - Evaluation of Program - LearnersAitzaz IjazNo ratings yet

- Cadbury EVP HR MdelDocument34 pagesCadbury EVP HR MdelAlok PandeyNo ratings yet