You might also like

- Taxation (Malawi) : Tuesday 4 June 2013Document10 pagesTaxation (Malawi) : Tuesday 4 June 2013angaNo ratings yet

- Taxation (Malawi) : Tuesday 3 June 2014Document11 pagesTaxation (Malawi) : Tuesday 3 June 2014angaNo ratings yet

- Taxation (Malawi) : Tuesday 3 December 2013Document10 pagesTaxation (Malawi) : Tuesday 3 December 2013angaNo ratings yet

- Taxation (Malawi) : Tuesday 2 June 2015Document13 pagesTaxation (Malawi) : Tuesday 2 June 2015angaNo ratings yet

- F6mwi QPDocument15 pagesF6mwi QPangaNo ratings yet

- MWI Taxation Paper F6Document10 pagesMWI Taxation Paper F6angaNo ratings yet

- Taxation (Malawi) : Specimen Questions For June 2015Document10 pagesTaxation (Malawi) : Specimen Questions For June 2015angaNo ratings yet

- Taxation Paper for Malawi Insurance CompanyDocument9 pagesTaxation Paper for Malawi Insurance CompanyangaNo ratings yet

- Taxation (Malawi) : Monday 2 June 2008Document9 pagesTaxation (Malawi) : Monday 2 June 2008angaNo ratings yet

- F6mwi 2007 Dec QDocument8 pagesF6mwi 2007 Dec Qanga100% (1)

- Malawi Taxation Paper F6Document10 pagesMalawi Taxation Paper F6angaNo ratings yet

- Taxation - Malawi (TX - Mwi) : Applied SkillsDocument15 pagesTaxation - Malawi (TX - Mwi) : Applied SkillsangaNo ratings yet

- Txmwi 2018 Dec Q PDFDocument15 pagesTxmwi 2018 Dec Q PDFangaNo ratings yet

- Taxation (Malawi) : Thursday 7 June 2018Document11 pagesTaxation (Malawi) : Thursday 7 June 2018angaNo ratings yet

- Business Taxation: (Malawi)Document10 pagesBusiness Taxation: (Malawi)angaNo ratings yet

- Travel Agency Feasibility Study ReportDocument30 pagesTravel Agency Feasibility Study ReportShahaan ZulfiqarNo ratings yet

- 2015 Jun Ans-8Document1 page2015 Jun Ans-8何健珩No ratings yet

- Za Deloitte 2023 Tax CardDocument11 pagesZa Deloitte 2023 Tax CardNgozaNo ratings yet

- Fac2601-2013-6 - Answers PDFDocument9 pagesFac2601-2013-6 - Answers PDFcandiceNo ratings yet

- Malawi tax answers and marking schemeDocument7 pagesMalawi tax answers and marking schemeangaNo ratings yet

- CMAC Section A, B Mid-Term Q.PaperDocument5 pagesCMAC Section A, B Mid-Term Q.PaperWaseim khan Barik zaiNo ratings yet

- Business Taxation: (Malawi)Document8 pagesBusiness Taxation: (Malawi)angaNo ratings yet

- Accounting 22 - Final Exam - 2023Document9 pagesAccounting 22 - Final Exam - 2023LaurenNo ratings yet

- Maltex Capital AllowancesDocument11 pagesMaltex Capital AllowancesangaNo ratings yet

- Facn311 Test 1 Solution 2019Document10 pagesFacn311 Test 1 Solution 20196lackzamokuhleNo ratings yet

- Service Sector Idea: Initial InvestmentDocument4 pagesService Sector Idea: Initial InvestmentMohammad Adil ChoudharyNo ratings yet

- Assumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4Document2 pagesAssumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4PranshuNo ratings yet

- Lian's financial statements for year ended 31 March 2013Document2 pagesLian's financial statements for year ended 31 March 2013StpmTutorialClassNo ratings yet

- ACC 401-2023 GA 2-EvenDocument3 pagesACC 401-2023 GA 2-EvenOhene Asare PogastyNo ratings yet

- Cloud Kitchen - ViseshamDocument34 pagesCloud Kitchen - ViseshamadiarunaaNo ratings yet

- 2019 Jun Ans-8Document1 page2019 Jun Ans-8何健珩No ratings yet

- Pfa3163 Set G QPDocument5 pagesPfa3163 Set G QPNur hidayah putriNo ratings yet

- Accounting (Modular Syllabus) : Pearson EdexcelDocument20 pagesAccounting (Modular Syllabus) : Pearson EdexcelAsma YasinNo ratings yet

- Session 7 Financial Analysis - Upto P & LDocument10 pagesSession 7 Financial Analysis - Upto P & LVismay WadiwalaNo ratings yet

- AAGB Quarter1 Ended 31.03.2021Document26 pagesAAGB Quarter1 Ended 31.03.2021NUR RAHIMIE FAHMI B.NOOR ADZMAN NUR RAHIMIE FAHMI B.NOOR ADZMANNo ratings yet

- Cash Flow Statement TemplateDocument20 pagesCash Flow Statement TemplateMuhammad AsadNo ratings yet

- Template M/S Laxmi Enterprises Dabur: Gross Profit (Income)Document10 pagesTemplate M/S Laxmi Enterprises Dabur: Gross Profit (Income)trisanka banikNo ratings yet

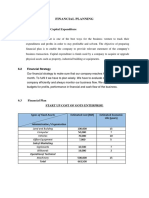

- Financial Planning: 6.1 Start-Up Cost and Capital ExpenditureDocument4 pagesFinancial Planning: 6.1 Start-Up Cost and Capital ExpenditurearefeenaNo ratings yet

- FAC3701 - 2021 - Additional QuestionsDocument54 pagesFAC3701 - 2021 - Additional QuestionsSibongileNo ratings yet

- Tesla FinModelDocument58 pagesTesla FinModelPrabhdeep DadyalNo ratings yet

- AnalystPresentn 2010Document25 pagesAnalystPresentn 2010Abhishek SinhaNo ratings yet

- Kim's Value Profit and Loss Account Notes Operating Capacity 1 2 3Document10 pagesKim's Value Profit and Loss Account Notes Operating Capacity 1 2 3sulthanhakimNo ratings yet

- Business Income Group Assignment...Document23 pagesBusiness Income Group Assignment...Brandon SibandaNo ratings yet

- Aadesh Financial AnalysisDocument8 pagesAadesh Financial Analysisदेवीना गिरीNo ratings yet

- Source - Bookletfull and Final Accoujting - 2 - Mcok - 1-MergedDocument12 pagesSource - Bookletfull and Final Accoujting - 2 - Mcok - 1-MergedAnonymous hrjVVKNo ratings yet

- Quotation GaugesDocument1 pageQuotation Gaugesshubhamagrawal_agarwal80No ratings yet

- Practical 7:: Prepare Annual Budget For An Industry of CompanyDocument10 pagesPractical 7:: Prepare Annual Budget For An Industry of CompanyAshish WalleNo ratings yet

- ProblemSet Cash Flow EstimationQA-160611 - 021520Document25 pagesProblemSet Cash Flow EstimationQA-160611 - 021520Jonathan Punnalagan100% (2)

- Cash Flow Estimation Problem SetDocument25 pagesCash Flow Estimation Problem SetCucumber IsHealthy96No ratings yet

- 9706 Accounting: MARK SCHEME For The March 2016 SeriesDocument8 pages9706 Accounting: MARK SCHEME For The March 2016 SeriesEn DimunNo ratings yet

- SK Budget Forms 2023Document4 pagesSK Budget Forms 2023Djaenzel Ramos0% (1)

- Q2FY19 Investor Update - PGCILDocument19 pagesQ2FY19 Investor Update - PGCILHemant SharmaNo ratings yet

- Project ReportsminesDocument13 pagesProject ReportsminesSmriti GargNo ratings yet

- Lanka Realty Investments PLC: Interim Financial Statements 31ST DECEMBER 2021Document12 pagesLanka Realty Investments PLC: Interim Financial Statements 31ST DECEMBER 2021girihellNo ratings yet

- B20F Exam Scenario and RequiredDocument13 pagesB20F Exam Scenario and RequiredNicolasNo ratings yet

- Cashflow Business Plan SampleDocument12 pagesCashflow Business Plan SampleSandeep MkhNo ratings yet

- Cash Flow EstimationDocument14 pagesCash Flow Estimation0241ASHAYNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Taxation Tax AdministrationDocument234 pagesTaxation Tax AdministrationmahmoudfatahabukarNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- HttpsDocument1 pageHttpsangaNo ratings yet

- 2018 Nov All FinalDocument105 pages2018 Nov All FinalangaNo ratings yet

- Txmwi 2018 Jun ADocument6 pagesTxmwi 2018 Jun AangaNo ratings yet

- FinalDocument104 pagesFinalEZEKIELNo ratings yet

- FinalDocument104 pagesFinalEZEKIELNo ratings yet

- Atec 2Document55 pagesAtec 2angaNo ratings yet

- F6mwi 2009 June QDocument8 pagesF6mwi 2009 June QangaNo ratings yet

- Advanced Engineering Mathematics 10th EditionDocument7 pagesAdvanced Engineering Mathematics 10th EditionsamuelNo ratings yet

- F6MWI 2014 Jun ADocument9 pagesF6MWI 2014 Jun AangaNo ratings yet

- F6mwi 2007 Dec QDocument8 pagesF6mwi 2007 Dec Qanga100% (1)

- F6MWI 2014 Dec ADocument9 pagesF6MWI 2014 Dec AangaNo ratings yet

- Txmwi 2018 Dec Q PDFDocument15 pagesTxmwi 2018 Dec Q PDFangaNo ratings yet

- Malawi tax answers and marking schemeDocument7 pagesMalawi tax answers and marking schemeangaNo ratings yet

- Malawi Taxation AnswersDocument7 pagesMalawi Taxation Answersanga100% (1)

- Taxation (Malawi) : Thursday 7 June 2018Document11 pagesTaxation (Malawi) : Thursday 7 June 2018angaNo ratings yet

- F6MWI 2015 Jun ADocument7 pagesF6MWI 2015 Jun AangaNo ratings yet

- Txmwi 2019 Jun ADocument9 pagesTxmwi 2019 Jun AangaNo ratings yet

- Taxation (Malawi) : Specimen Questions For June 2015Document10 pagesTaxation (Malawi) : Specimen Questions For June 2015angaNo ratings yet

- TX (MWI) Sept 20 Sample CBE QuestionsDocument31 pagesTX (MWI) Sept 20 Sample CBE QuestionsangaNo ratings yet

- S20 TX MWI Sample AnswersDocument8 pagesS20 TX MWI Sample AnswersangaNo ratings yet

- Taxation (Malawi) : Monday 2 June 2008Document9 pagesTaxation (Malawi) : Monday 2 June 2008angaNo ratings yet

- Malawi Taxation Paper F6Document10 pagesMalawi Taxation Paper F6angaNo ratings yet

- Taxation Answers for MalawiDocument12 pagesTaxation Answers for MalawiangaNo ratings yet

- Taxation - Malawi (TX - Mwi) : Applied SkillsDocument15 pagesTaxation - Malawi (TX - Mwi) : Applied SkillsangaNo ratings yet

- Taxation Answers for MalawiDocument11 pagesTaxation Answers for MalawiangaNo ratings yet

- Tax Invoice DetailsDocument2 pagesTax Invoice Detailsquality fluconNo ratings yet

- Expected Questions For Business Laws For June 22 ExamsDocument8 pagesExpected Questions For Business Laws For June 22 ExamsFREEFIRE IDNo ratings yet

- Grade 9 TLE LCPDocument8 pagesGrade 9 TLE LCPMJ Andrade67% (3)

- Eks 9 en 2015 01 14Document157 pagesEks 9 en 2015 01 14aykutNo ratings yet

- Use Investing in People Financial Impact of Human Resources Initiatives by Cascio and BoudreauDocument3 pagesUse Investing in People Financial Impact of Human Resources Initiatives by Cascio and BoudreauDoreen0% (1)

- Account Usage and Recharge Statement From 01-Jan-2023 To 29-Jan-2023Document9 pagesAccount Usage and Recharge Statement From 01-Jan-2023 To 29-Jan-2023Shubham VishwakarmaNo ratings yet

- Sustainbook PDFDocument225 pagesSustainbook PDFjNo ratings yet

- ACCT3203 Week 5 Tutorial Questions Customer Profitability Analysis & Quality S2 2022Document12 pagesACCT3203 Week 5 Tutorial Questions Customer Profitability Analysis & Quality S2 2022Jingwen YangNo ratings yet

- CV-Agus Nugraha (For IUWASH PLUS - RC Surakarta)Document11 pagesCV-Agus Nugraha (For IUWASH PLUS - RC Surakarta)Agus NugrahaNo ratings yet

- MBA Akshay Arora: SAP ID:80511020627 - : Akshay - Arora27@nmims - Edu.in - Age: 23Document2 pagesMBA Akshay Arora: SAP ID:80511020627 - : Akshay - Arora27@nmims - Edu.in - Age: 23gautam keswaniNo ratings yet

- Marcopper Mining CorpDocument7 pagesMarcopper Mining CorpChristine Ivy Delos SantosNo ratings yet

- 2021 Remaining Ongoing CasesDocument2,517 pages2021 Remaining Ongoing CasesJulia Mar Antonete Tamayo AcedoNo ratings yet

- 50 MCQ SETS on JOB ANALYSISDocument14 pages50 MCQ SETS on JOB ANALYSISChaudhary AdeelNo ratings yet

- MRB Approves Nonconforming PartsDocument3 pagesMRB Approves Nonconforming PartsMiguel RodriguezNo ratings yet

- DetailsNewCreditAssigned Mar23 OthersecuritiesDocument16 pagesDetailsNewCreditAssigned Mar23 OthersecuritiesasamitarannumNo ratings yet

- 3.5 Additional Changes To Support Merchant and Acquirer Address in Visa Direct TransactionsDocument15 pages3.5 Additional Changes To Support Merchant and Acquirer Address in Visa Direct TransactionsYasir RoniNo ratings yet

- Se/Omc/Nalgonda - Pay Unit Code: 5112: Pay Slip For The Month of August - 2020Document1 pageSe/Omc/Nalgonda - Pay Unit Code: 5112: Pay Slip For The Month of August - 2020babu xeroxNo ratings yet

- Interbrand Breakthrough Brands 2020 ReportDocument44 pagesInterbrand Breakthrough Brands 2020 ReportThu Hà NguyễnNo ratings yet

- MICE - A New Paradigm For TourismDocument69 pagesMICE - A New Paradigm For TourismRoy Cabarles100% (1)

- K WaterDocument113 pagesK WaterAmri Rifki FauziNo ratings yet

- Motion To Reduce BondDocument4 pagesMotion To Reduce Bonderika barbaronaNo ratings yet

- Software Developement Life CycleDocument21 pagesSoftware Developement Life CycleJAI THAPANo ratings yet

- Experienced Hospitality Professional Seeking New OpportunitiesDocument2 pagesExperienced Hospitality Professional Seeking New OpportunitiesValeria SpasovaNo ratings yet

- Consumer Behaviour, 2nd Edition - Chapter 1Document42 pagesConsumer Behaviour, 2nd Edition - Chapter 1guptamadras100% (1)

- Design Books and Price Books for American Federal-Period Card TablesDocument16 pagesDesign Books and Price Books for American Federal-Period Card TablesJosh ChoughNo ratings yet

- Tax Invoice-Cum-Receipt: Railtel Corporation of India Limited. Gstin PanDocument1 pageTax Invoice-Cum-Receipt: Railtel Corporation of India Limited. Gstin PanAshihsNo ratings yet

- FMCSA Rules on Marking Commercial Motor VehiclesDocument3 pagesFMCSA Rules on Marking Commercial Motor VehiclesfreeNo ratings yet

- Grameen BankDocument28 pagesGrameen Bankalpha34567No ratings yet

- BioPharma Case StudyDocument4 pagesBioPharma Case StudyNaman Chhaya100% (3)

- Jurnal Rina Dan WisnuDocument41 pagesJurnal Rina Dan WisnuAnisa armadianaNo ratings yet