You might also like

- Certificate of Employment and CompensationDocument1 pageCertificate of Employment and Compensationmoses_silva83% (18)

- External competitiveness policy options and recommendationsDocument1 pageExternal competitiveness policy options and recommendationsAkshatha Manjunath100% (1)

- Chapter-21 (Solved Past Papers of CA Mod CDocument67 pagesChapter-21 (Solved Past Papers of CA Mod CJer Rama100% (4)

- RevenueRegulations1 83Document4 pagesRevenueRegulations1 83Ansherina FranciscoNo ratings yet

- Producers Bank of The PhilDocument2 pagesProducers Bank of The PhilJoshua Mendoza100% (1)

- Sia Application Form NotesDocument40 pagesSia Application Form NotesRobin HardyNo ratings yet

- Incentive and CompensationDocument12 pagesIncentive and CompensationFarhaNo ratings yet

- 2-3mwi 2004 Dec ADocument13 pages2-3mwi 2004 Dec Aanga100% (1)

- 2-3mwi 2006 Jun ADocument12 pages2-3mwi 2006 Jun AangaNo ratings yet

- Maltex Capital AllowancesDocument11 pagesMaltex Capital AllowancesangaNo ratings yet

- Business Taxation: (Malawi)Document8 pagesBusiness Taxation: (Malawi)angaNo ratings yet

- F6mwi 2011 Jun ADocument9 pagesF6mwi 2011 Jun AangaNo ratings yet

- 2-3mwi 2006 Dec ADocument13 pages2-3mwi 2006 Dec AangaNo ratings yet

- Adb Fin Statement - Dec 2020 - Final 2Document2 pagesAdb Fin Statement - Dec 2020 - Final 2Fuaad DodooNo ratings yet

- F9 AnswersDocument10 pagesF9 AnswersHil ShahNo ratings yet

- Management and Cost Accounting 10th Edition Drury Solutions ManualDocument17 pagesManagement and Cost Accounting 10th Edition Drury Solutions Manualeliasvykh6in8100% (27)

- Management and Cost Accounting 10th Edition Drury Solutions Manual Full Chapter PDFDocument38 pagesManagement and Cost Accounting 10th Edition Drury Solutions Manual Full Chapter PDFirisdavid3n8lg100% (9)

- Malawi tax answers and marking schemeDocument7 pagesMalawi tax answers and marking schemeangaNo ratings yet

- Enterprise GroupDocument8 pagesEnterprise GroupFuaad DodooNo ratings yet

- Answer To Phase TestDocument5 pagesAnswer To Phase TestPohYeeLiewNo ratings yet

- CS Ratio Analysis - March 2020Document2 pagesCS Ratio Analysis - March 2020Onaderu Oluwagbenga EnochNo ratings yet

- Mirri TaxDocument10 pagesMirri TaxMandanda LovemoreNo ratings yet

- Enterprise Group PLC: Unaudited Financial Statements For The Year Ended 31 December 2021Document8 pagesEnterprise Group PLC: Unaudited Financial Statements For The Year Ended 31 December 2021Fuaad DodooNo ratings yet

- S20 TX MWI Sample AnswersDocument8 pagesS20 TX MWI Sample AnswersangaNo ratings yet

- AnswersDocument9 pagesAnswersEsha DasNo ratings yet

- Bishop Group (IAS-21 + Cashflow) : Cfap 1: A A F RDocument1 pageBishop Group (IAS-21 + Cashflow) : Cfap 1: A A F R.No ratings yet

- Suggested Answers Certified Finance and Accounting Professional Examination - Summer 2018Document7 pagesSuggested Answers Certified Finance and Accounting Professional Examination - Summer 2018Muhammad Usama SheikhNo ratings yet

- Depreciation calculation and gain on disposalDocument3 pagesDepreciation calculation and gain on disposaliamneonkingNo ratings yet

- Annual-Report-FML-30-June-2020-23 Vol 2Document1 pageAnnual-Report-FML-30-June-2020-23 Vol 2Bluish FlameNo ratings yet

- p7sgp 2011 Dec QDocument10 pagesp7sgp 2011 Dec QamNo ratings yet

- 06 JUNE AnswersDocument13 pages06 JUNE AnswerskhengmaiNo ratings yet

- Fm-Nov-Dec 2012Document14 pagesFm-Nov-Dec 2012banglauserNo ratings yet

- Rs. in 000: Ans.6 (A) Hadi Limited Statement of Comprehensive Income For The Year Ended 31 December 2016Document4 pagesRs. in 000: Ans.6 (A) Hadi Limited Statement of Comprehensive Income For The Year Ended 31 December 2016Sameen KhanNo ratings yet

- Chapter 5: Preparation of Financial Statements Practice ProblemsDocument27 pagesChapter 5: Preparation of Financial Statements Practice Problemsmayank shridharNo ratings yet

- Kuwait Privatization Projects Holding Co.: Financial Statement - 2006Document21 pagesKuwait Privatization Projects Holding Co.: Financial Statement - 2006phckuwaitNo ratings yet

- S20 TX BWA Sample AnswersDocument10 pagesS20 TX BWA Sample AnswersKAM JIA LINGNo ratings yet

- MFA Test 1 SolutionDocument4 pagesMFA Test 1 SolutionMuhammad ImranNo ratings yet

- Proforma Balance SheetDocument24 pagesProforma Balance SheetBarbara YoungNo ratings yet

- Lakh Datta Flour MillsDocument14 pagesLakh Datta Flour MillsjimmuNo ratings yet

- Rise School of Accountancy: Suggested Solution Test 08Document2 pagesRise School of Accountancy: Suggested Solution Test 08iamneonkingNo ratings yet

- 2015 Dec Ans-8Document1 page2015 Dec Ans-8何健珩No ratings yet

- CAF-6 Mock Solution by SkansDocument6 pagesCAF-6 Mock Solution by SkansMuhammad YahyaNo ratings yet

- 14-Combining Financial Statements-Sept. 30, 07-Fin Com-ADocument4 pages14-Combining Financial Statements-Sept. 30, 07-Fin Com-ACOASTNo ratings yet

- 2019 12 December-2019-Cpe-Audit-Question-PaperDocument10 pages2019 12 December-2019-Cpe-Audit-Question-Paperkellz accountingNo ratings yet

- IGB REIT-Interim Report-Dec19-200122Document18 pagesIGB REIT-Interim Report-Dec19-200122Gan Zhi HanNo ratings yet

- Change Analysis Balance Sheet AccountsDocument10 pagesChange Analysis Balance Sheet AccountsIndra HadiNo ratings yet

- B2 2022 May AnsDocument15 pagesB2 2022 May AnsRashid AbeidNo ratings yet

- CR - MA-2023 - Suggested - AnswersDocument15 pagesCR - MA-2023 - Suggested - AnswersfahadsarkerNo ratings yet

- 2015 Jun Ans-8Document1 page2015 Jun Ans-8何健珩No ratings yet

- Document Incorporated by Reference EBI F Cial Statements 2007 2009-08-17Document80 pagesDocument Incorporated by Reference EBI F Cial Statements 2007 2009-08-17Megan KosNo ratings yet

- AlMeezan AnnualReport2023 MIIF (1)Document9 pagesAlMeezan AnnualReport2023 MIIF (1)mrordinaryNo ratings yet

- F7irl 2008 Dec ADocument10 pagesF7irl 2008 Dec Awaseemhasan85No ratings yet

- T12 - ABFA1153 (Extra)Document2 pagesT12 - ABFA1153 (Extra)LOO YU HUANGNo ratings yet

- Income Statement: Year Ended 31 December 2005Document19 pagesIncome Statement: Year Ended 31 December 2005phckuwaitNo ratings yet

- Chapter 4 Governmental AccountingDocument5 pagesChapter 4 Governmental Accountingmohamad ali osmanNo ratings yet

- Tax 2005 ExamDocument26 pagesTax 2005 ExamleerenjyeNo ratings yet

- P6 Princiiples of Taxation QJ17Document12 pagesP6 Princiiples of Taxation QJ17angaNo ratings yet

- M/S Goladi Khola Multipurpose Agriculture Firm: Pokhara-33, KaskiDocument10 pagesM/S Goladi Khola Multipurpose Agriculture Firm: Pokhara-33, KaskiMadhav Prasad KadelNo ratings yet

- Assignment FSADocument15 pagesAssignment FSAJaveria KhanNo ratings yet

- Accounts Fy 22 23 BaluchistanDocument104 pagesAccounts Fy 22 23 BaluchistanFarooq MaqboolNo ratings yet

- Jhanvi Shah 2012 CF PresentationDocument12 pagesJhanvi Shah 2012 CF PresentationJhanvi ShahNo ratings yet

- AnswersDocument8 pagesAnswersNirmal ShresthaNo ratings yet

- 16.9.chapter 8+9 - Conso SoCI - Jun 11 - AnswerDocument3 pages16.9.chapter 8+9 - Conso SoCI - Jun 11 - AnswerPHUC TRAN TRIEU NGUYENNo ratings yet

- I Fitness Venture StandaloneDocument15 pagesI Fitness Venture StandaloneThe keyboard PlayerNo ratings yet

- Financial Statement SingerDocument13 pagesFinancial Statement SingerAnuja PasandulNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Txmwi 2018 Dec Q PDFDocument15 pagesTxmwi 2018 Dec Q PDFangaNo ratings yet

- FinalDocument104 pagesFinalEZEKIELNo ratings yet

- FinalDocument104 pagesFinalEZEKIELNo ratings yet

- HttpsDocument1 pageHttpsangaNo ratings yet

- 2018 Nov All FinalDocument105 pages2018 Nov All FinalangaNo ratings yet

- Malawi tax answers and marking schemeDocument7 pagesMalawi tax answers and marking schemeangaNo ratings yet

- Txmwi 2018 Jun ADocument6 pagesTxmwi 2018 Jun AangaNo ratings yet

- Atec 2Document55 pagesAtec 2angaNo ratings yet

- F6mwi 2009 June QDocument8 pagesF6mwi 2009 June QangaNo ratings yet

- F6mwi QPDocument15 pagesF6mwi QPangaNo ratings yet

- Advanced Engineering Mathematics 10th EditionDocument7 pagesAdvanced Engineering Mathematics 10th EditionsamuelNo ratings yet

- Taxation (Malawi) : Thursday 7 June 2018Document11 pagesTaxation (Malawi) : Thursday 7 June 2018angaNo ratings yet

- F6mwi 2007 Dec QDocument8 pagesF6mwi 2007 Dec Qanga100% (1)

- Taxation (Malawi) : Tuesday 3 June 2014Document11 pagesTaxation (Malawi) : Tuesday 3 June 2014angaNo ratings yet

- Taxation (Malawi) : Tuesday 2 December 2014Document12 pagesTaxation (Malawi) : Tuesday 2 December 2014angaNo ratings yet

- F6MWI 2014 Jun ADocument9 pagesF6MWI 2014 Jun AangaNo ratings yet

- F6MWI 2014 Dec ADocument9 pagesF6MWI 2014 Dec AangaNo ratings yet

- Malawi Taxation Paper F6Document10 pagesMalawi Taxation Paper F6angaNo ratings yet

- Taxation (Malawi) : Tuesday 2 June 2015Document13 pagesTaxation (Malawi) : Tuesday 2 June 2015angaNo ratings yet

- Taxation (Malawi) : Specimen Questions For June 2015Document10 pagesTaxation (Malawi) : Specimen Questions For June 2015angaNo ratings yet

- Malawi Taxation AnswersDocument7 pagesMalawi Taxation Answersanga100% (1)

- F6MWI 2015 Jun ADocument7 pagesF6MWI 2015 Jun AangaNo ratings yet

- TX (MWI) Sept 20 Sample CBE QuestionsDocument31 pagesTX (MWI) Sept 20 Sample CBE QuestionsangaNo ratings yet

- Txmwi 2019 Jun ADocument9 pagesTxmwi 2019 Jun AangaNo ratings yet

- S20 TX MWI Sample AnswersDocument8 pagesS20 TX MWI Sample AnswersangaNo ratings yet

- Taxation (Malawi) : Monday 2 June 2008Document9 pagesTaxation (Malawi) : Monday 2 June 2008angaNo ratings yet

- Taxation - Malawi (TX - Mwi) : Applied SkillsDocument15 pagesTaxation - Malawi (TX - Mwi) : Applied SkillsangaNo ratings yet

- Taxation Answers for MalawiDocument12 pagesTaxation Answers for MalawiangaNo ratings yet

- Taxation (Malawi) : Tuesday 3 December 2013Document10 pagesTaxation (Malawi) : Tuesday 3 December 2013angaNo ratings yet

- Taxation Answers for MalawiDocument11 pagesTaxation Answers for MalawiangaNo ratings yet

- FM GSIS OPS CPR 01 - Pensioners Request Form FillableDocument1 pageFM GSIS OPS CPR 01 - Pensioners Request Form FillableAttorney Rhy Jay100% (2)

- Chapter 16 - Payout PolicyDocument12 pagesChapter 16 - Payout PolicyTrinh VũNo ratings yet

- Non-Depository Financial Institutions Chapter SummaryDocument30 pagesNon-Depository Financial Institutions Chapter SummaryMarina KhanNo ratings yet

- File Form 540 2EZ CaliforniaDocument6 pagesFile Form 540 2EZ CaliforniaPhylicia MorrisNo ratings yet

- Test 5 Mutual Fund Nismtop500.in-1Document51 pagesTest 5 Mutual Fund Nismtop500.in-1अभिजीत आखाडेNo ratings yet

- Compensation and Final Withholding TaxesDocument7 pagesCompensation and Final Withholding TaxesbayombongumcNo ratings yet

- Case StudyDocument5 pagesCase StudyMD FAISALNo ratings yet

- September 15 Payslip PDFDocument1 pageSeptember 15 Payslip PDFjohn lerry loberioNo ratings yet

- Payroll Audit ProgramDocument21 pagesPayroll Audit ProgramAndrés Velasco PachecoNo ratings yet

- FAQ On ESOPDocument8 pagesFAQ On ESOPayushgmailNo ratings yet

- Tax Study Material PDFDocument151 pagesTax Study Material PDFROHITH R MENONNo ratings yet

- Financial Services Compensation Scheme Information SheetDocument2 pagesFinancial Services Compensation Scheme Information SheetRocketNo ratings yet

- Employee Salaries and Benefits and Their Disclosures in NGOsDocument22 pagesEmployee Salaries and Benefits and Their Disclosures in NGOspretty frauNo ratings yet

- Employee Benefits (Part 2) : Problem 1: True or FalseDocument21 pagesEmployee Benefits (Part 2) : Problem 1: True or FalseChi Chi100% (1)

- Income Tax by Sachin RevekarDocument5 pagesIncome Tax by Sachin RevekarSACHIN REVEKARNo ratings yet

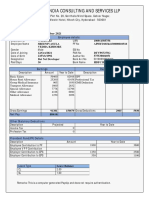

- Purview India Consulting and Services LLPDocument1 pagePurview India Consulting and Services LLPmamatha vemulaNo ratings yet

- Withholding Tax Rates MalawiDocument2 pagesWithholding Tax Rates Malawianraomca100% (1)

- Chapter 3: Insurance MarketDocument11 pagesChapter 3: Insurance MarketHarris YIGNo ratings yet

- Lagnajit Ayaskant Sahoo Gourab Biswas Suchismita Das Santanu Rath Ranjeet Kumar September, 2010Document23 pagesLagnajit Ayaskant Sahoo Gourab Biswas Suchismita Das Santanu Rath Ranjeet Kumar September, 2010Lagnajit Ayaskant SahooNo ratings yet

- Tax PlanningDocument26 pagesTax Planningpuneeta chughNo ratings yet

- PAYSLIP FOR THE MONTH OF September, 2023: Toyota Kirloskar Motor PVT LTDDocument2 pagesPAYSLIP FOR THE MONTH OF September, 2023: Toyota Kirloskar Motor PVT LTDevilghostevilghost666No ratings yet

- Savvy Social Security Planning:: What Baby Boomers Need To Know To Maximize Retirement IncomeDocument49 pagesSavvy Social Security Planning:: What Baby Boomers Need To Know To Maximize Retirement IncomeTammara BandyNo ratings yet

- Fabm 2: Quarter 4 - Module 5-6 Principles and Processes of Income and Business TaxationDocument12 pagesFabm 2: Quarter 4 - Module 5-6 Principles and Processes of Income and Business TaxationChelsea Mae AlingNo ratings yet

- Activity 2 Income TaxationDocument3 pagesActivity 2 Income TaxationKim Cyrah Amor GerianNo ratings yet