You might also like

- Chapter 28 AnsDocument9 pagesChapter 28 AnsDave ManaloNo ratings yet

- Chapter 3 Corporate Liquidation and Reorganization-PROFE01Document3 pagesChapter 3 Corporate Liquidation and Reorganization-PROFE01Steffany RoqueNo ratings yet

- QuizDocument13 pagesQuizPearl Morni AlbanoNo ratings yet

- Chapter 6 - Joint ArrangementsDocument16 pagesChapter 6 - Joint ArrangementsMikael James VillanuevaNo ratings yet

- PFRS 14 15 16Document3 pagesPFRS 14 15 16kara mNo ratings yet

- Quiz 1 - Business CombiDocument6 pagesQuiz 1 - Business CombiKaguraNo ratings yet

- FM112 Student Chapter 1Document15 pagesFM112 Student Chapter 1Thricia Mae IgnacioNo ratings yet

- Chapter 16 Summary: Accounting for Non-Profit OrganizationsDocument27 pagesChapter 16 Summary: Accounting for Non-Profit OrganizationsEllen MNo ratings yet

- Allowable Deductions Part 1Document3 pagesAllowable Deductions Part 1John Rich GamasNo ratings yet

- Final 2 2Document3 pagesFinal 2 2RonieOlarteNo ratings yet

- SGV & Co. Philippines' Largest Professional Services FirmDocument6 pagesSGV & Co. Philippines' Largest Professional Services FirmjeanruedasNo ratings yet

- Answers To Assignement 1 Period 3Document16 pagesAnswers To Assignement 1 Period 3trishaNo ratings yet

- At Last Minute by HerculesDocument19 pagesAt Last Minute by HerculesFranklin ValdezNo ratings yet

- Audit of ReceivablesDocument20 pagesAudit of ReceivablesDethzaida AsebuqueNo ratings yet

- Calculation For Liquidation Value at Closure Date Is Somewhat Like The Book Value CalculationDocument3 pagesCalculation For Liquidation Value at Closure Date Is Somewhat Like The Book Value CalculationALYZA ANGELA ORNEDONo ratings yet

- Quiz 3 - Business Combination and Consolidated Financial StatementsDocument3 pagesQuiz 3 - Business Combination and Consolidated Financial StatementsMaria LopezNo ratings yet

- AISDocument11 pagesAISJezeil DimasNo ratings yet

- CPAR Financial StatementsDocument5 pagesCPAR Financial StatementsAnjo EllisNo ratings yet

- Intercompany DividendsDocument6 pagesIntercompany DividendsClauie BarsNo ratings yet

- Part 5 - ADocument1 pagePart 5 - AKuro YukiNo ratings yet

- Accounting for Debt InstrumentsDocument4 pagesAccounting for Debt InstrumentsKeahlyn Boticario CapinaNo ratings yet

- Chapter 3 Liquidation ValueDocument11 pagesChapter 3 Liquidation ValueJIL Masapang Victoria ChapterNo ratings yet

- Final Exam 10 PDF FreeDocument12 pagesFinal Exam 10 PDF FreeMariefel OrdanezNo ratings yet

- Chapter 19 Professional EthicsDocument26 pagesChapter 19 Professional EthicsSavya SachiNo ratings yet

- Auditing TheoDocument27 pagesAuditing TheoSherri BonquinNo ratings yet

- Accounting for Governmental Entities ExamDocument4 pagesAccounting for Governmental Entities ExamKarla OñasNo ratings yet

- Chapter 1: Introduction To Consumption TaxesDocument6 pagesChapter 1: Introduction To Consumption TaxesJoody CatacutanNo ratings yet

- Solution Chapter 6 Joint ArrangementsDocument17 pagesSolution Chapter 6 Joint ArrangementsMariz QuintoNo ratings yet

- RFBT - Chapter 8 - Ease of Doing BusinessDocument15 pagesRFBT - Chapter 8 - Ease of Doing Businesslaythejoylunas21No ratings yet

- PFRS 3 Business Combinations SummaryDocument4 pagesPFRS 3 Business Combinations SummaryKryzzel Anne JonNo ratings yet

- AFAR-07 (Home-Office & Branch Accounting)Document7 pagesAFAR-07 (Home-Office & Branch Accounting)mysweet surrenderNo ratings yet

- Ch15 Raiborn SMDocument26 pagesCh15 Raiborn SMMendelle Murry100% (1)

- Problems: Problem 4 - 1Document4 pagesProblems: Problem 4 - 1KioNo ratings yet

- Psa 600Document9 pagesPsa 600Bhebi Dela CruzNo ratings yet

- Sales Made Evenly (Warranty Liability)Document4 pagesSales Made Evenly (Warranty Liability)Jorufel Tomo PapasinNo ratings yet

- Fundamentals of Assurance Services - Docx'Document8 pagesFundamentals of Assurance Services - Docx'jhell dela cruzNo ratings yet

- Equity Test BanksDocument34 pagesEquity Test BanksHea Jennifer AyopNo ratings yet

- FAR Final Preboard SolutionsDocument6 pagesFAR Final Preboard SolutionsVillanueva, Mariella De VeraNo ratings yet

- Investing ActivitiesDocument7 pagesInvesting ActivitiesMs. ArianaNo ratings yet

- Computer-Based Accounting Systems: Automation and ReengineeringDocument5 pagesComputer-Based Accounting Systems: Automation and ReengineeringHendrikus AndriantoNo ratings yet

- CHAPTER 6 Auditing-Theory-MCQs-by-Salosagcol-with-answersDocument2 pagesCHAPTER 6 Auditing-Theory-MCQs-by-Salosagcol-with-answersMichNo ratings yet

- Differential Analysis:: The Key To Decision MakingDocument32 pagesDifferential Analysis:: The Key To Decision MakingkimmyNo ratings yet

- Cost of Property and Equipment for Aliaga Corporation and Bongabon Machine AcquisitionDocument4 pagesCost of Property and Equipment for Aliaga Corporation and Bongabon Machine AcquisitionAnna Mae NebresNo ratings yet

- Ap 06 REO Receivables - PDF 074431Document19 pagesAp 06 REO Receivables - PDF 074431ChristianNo ratings yet

- MOD2 Corporate LiquidationDocument4 pagesMOD2 Corporate LiquidationJasper Andrew AdjaraniNo ratings yet

- BSA 3202 Topic 2 - Joint ArrangementsDocument14 pagesBSA 3202 Topic 2 - Joint ArrangementsjenieNo ratings yet

- PFRS 3, Business CombinationsDocument39 pagesPFRS 3, Business Combinationsjulia4razoNo ratings yet

- PFRS 3 - Business Combination PDFDocument2 pagesPFRS 3 - Business Combination PDFMaria LopezNo ratings yet

- Estate Tax Guide for PhilippinesDocument50 pagesEstate Tax Guide for PhilippinesLea JoaquinNo ratings yet

- Chapter 1 - Overview of Government AccountingDocument4 pagesChapter 1 - Overview of Government AccountingChris tine Mae MendozaNo ratings yet

- Sales Chapter 13 Part II REPORTDocument50 pagesSales Chapter 13 Part II REPORTJeane Mae BooNo ratings yet

- Advanced Financial Accounting TopicsDocument16 pagesAdvanced Financial Accounting TopicsNhel AlvaroNo ratings yet

- Investments in Financial Instruments CompleteDocument34 pagesInvestments in Financial Instruments CompleteDenise CruzNo ratings yet

- Compute P/E ratios, dividend yields, and book-to-market ratiosDocument2 pagesCompute P/E ratios, dividend yields, and book-to-market ratiosJaneth NavalesNo ratings yet

- ACC117-CON09 Module 3 ExamDocument16 pagesACC117-CON09 Module 3 ExamMarlon LadesmaNo ratings yet

- PledgeDocument2 pagesPledgeKellNo ratings yet

- Investment in AssociateDocument11 pagesInvestment in AssociateElla MontefalcoNo ratings yet

- Philippine Deposit Insurance Corporation (PDIC) Law SummaryDocument11 pagesPhilippine Deposit Insurance Corporation (PDIC) Law SummaryElmer JuanNo ratings yet

- Module 3 - Overview of NPODocument19 pagesModule 3 - Overview of NPOJebong CaguitlaNo ratings yet

- Activity in E3 - LiabilitiesDocument9 pagesActivity in E3 - LiabilitiesPaupau100% (1)

- Actvity 4 in Auditing 4 - Biological AssetsDocument3 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Implement Strategy StructureDocument21 pagesImplement Strategy StructurePaupau100% (1)

- Activity - Derivatives and Hedging Accounting (PFRS 9)Document8 pagesActivity - Derivatives and Hedging Accounting (PFRS 9)PaupauNo ratings yet

- Activity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)Document1 pageActivity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)PaupauNo ratings yet

- Accounting for Cash, Receivables and InventoriesDocument12 pagesAccounting for Cash, Receivables and InventoriesPaupau100% (1)

- Assessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerDocument12 pagesAssessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerPaupauNo ratings yet

- Audit 4 - Audit in Specialized IndustryDocument7 pagesAudit 4 - Audit in Specialized IndustryPaupauNo ratings yet

- Assignment On PCF and Bank ReconDocument2 pagesAssignment On PCF and Bank ReconPaupauNo ratings yet

- Activity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0Document6 pagesActivity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0PaupauNo ratings yet

- AFAR ReviewDocument11 pagesAFAR ReviewPaupauNo ratings yet

- Activity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Document12 pagesActivity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Paupau0% (1)

- Activity On Application ControlDocument5 pagesActivity On Application ControlPaupauNo ratings yet

- Activity 2 Audit On CISDocument4 pagesActivity 2 Audit On CISPaupauNo ratings yet

- Special Purpose Audit Procedures and ReportsDocument6 pagesSpecial Purpose Audit Procedures and ReportsPaupauNo ratings yet

- Answer in Prelim Exam E4.Document12 pagesAnswer in Prelim Exam E4.PaupauNo ratings yet

- Activity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Document11 pagesActivity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Paupau100% (1)

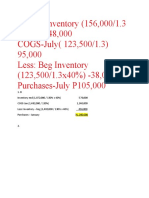

- Ending Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000Document1 pageEnding Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000PaupauNo ratings yet

- Activity 3 - CAATsDocument4 pagesActivity 3 - CAATsPaupauNo ratings yet

- Estimated transaction price methods and entries for consignment salesDocument7 pagesEstimated transaction price methods and entries for consignment salesPaupauNo ratings yet

- Answers - Partnership AccountingDocument14 pagesAnswers - Partnership AccountingPaupauNo ratings yet

- Actvity 4 in Auditing 4 - Biological AssetsDocument2 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Home Office, Agency and Branch AccountingDocument17 pagesHome Office, Agency and Branch AccountingPaupauNo ratings yet

- Answer in Act. 2 For Cash-receivables-InventoriesDocument10 pagesAnswer in Act. 2 For Cash-receivables-InventoriesPaupauNo ratings yet

- MAS-04 Relevant CostingDocument10 pagesMAS-04 Relevant CostingPaupauNo ratings yet

- Management Accounting Techniques CompilationDocument40 pagesManagement Accounting Techniques CompilationGracelle Mae Oraller100% (1)

- 6 Business StrategyDocument27 pages6 Business StrategyPaupauNo ratings yet

- PAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesDocument9 pagesPAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesPaupauNo ratings yet

- Activity - Consolidated Financial Statement Part 1Document10 pagesActivity - Consolidated Financial Statement Part 1PaupauNo ratings yet

- Assessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerDocument12 pagesAssessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerPaupauNo ratings yet

- 161 Quiz CH 6 Debt Sevice KEYDocument2 pages161 Quiz CH 6 Debt Sevice KEYChao Thao100% (1)

- Week 5 Special Revenue and Measurement Focus and Basis of Accounting - ACTG343Document10 pagesWeek 5 Special Revenue and Measurement Focus and Basis of Accounting - ACTG343Marilou Arcillas PanisalesNo ratings yet

- T10 Government Accounting PDFDocument9 pagesT10 Government Accounting PDFnicahNo ratings yet

- FULL Download Ebook PDF Government and Not For Profit Accounting Concepts and Practices 8th Edition PDF EbookDocument42 pagesFULL Download Ebook PDF Government and Not For Profit Accounting Concepts and Practices 8th Edition PDF Ebookmichael.porter654100% (31)

- Fund Acc - Ringkasan Chapter 1Document3 pagesFund Acc - Ringkasan Chapter 1Andini OleyNo ratings yet

- General ProvisionDocument22 pagesGeneral ProvisionAnna LynNo ratings yet

- 2021-22 Proposed BudgetDocument119 pages2021-22 Proposed BudgetinforumdocsNo ratings yet

- ACCTG 18 Accounting For Governmental Not-For-Profit Entities & Specialized Industries - 1Document19 pagesACCTG 18 Accounting For Governmental Not-For-Profit Entities & Specialized Industries - 1syrel s. olermoNo ratings yet

- Annual Financial Report For The Local Government Volume IDocument215 pagesAnnual Financial Report For The Local Government Volume IRhuejane Gay MaquilingNo ratings yet

- SUMMER HOLILDAYS HomeworkDocument33 pagesSUMMER HOLILDAYS HomeworkLorem LoremNo ratings yet

- Auditing-Non Profit Entities and HospitalsDocument12 pagesAuditing-Non Profit Entities and HospitalsVirgie MartinezNo ratings yet

- Budget Workshop 3 FY 2022Document41 pagesBudget Workshop 3 FY 2022Dan LehrNo ratings yet

- Advacc 1001-1014Document15 pagesAdvacc 1001-1014Camille SantosNo ratings yet

- Colorado Senate Bill 20B-001Document24 pagesColorado Senate Bill 20B-001Michael_Roberts2019No ratings yet

- Government AuditingDocument19 pagesGovernment AuditingGherine Joy Serrano Tayag100% (2)

- Not For Profit OrganizationDocument69 pagesNot For Profit OrganizationDristi SaudNo ratings yet

- 2C. NPO Hospitals - PPTDocument18 pages2C. NPO Hospitals - PPTJSNo ratings yet

- Accounting for religious organization orginalDocument20 pagesAccounting for religious organization orginaltsedekselashi90No ratings yet

- AOM - Cash in Bank-LCCA Without Legal BasisDocument5 pagesAOM - Cash in Bank-LCCA Without Legal Basisrussel1435No ratings yet

- Putney FD Operations AnalysisDocument174 pagesPutney FD Operations AnalysisSarah100% (1)

- NCERT Solutions For Class 12 Accountancy Chapter 1 - Accounting For Not For Profit Organisation - 67pDocument67 pagesNCERT Solutions For Class 12 Accountancy Chapter 1 - Accounting For Not For Profit Organisation - 67pshanmugam PalaniappanNo ratings yet

- Executive Summary - Honolulu Rail Transit Financial Plan AssessmentDocument21 pagesExecutive Summary - Honolulu Rail Transit Financial Plan AssessmentCraig GimaNo ratings yet

- Income and Expenditure Account AssignmentDocument38 pagesIncome and Expenditure Account AssignmentMUHAMMAD HASSANNo ratings yet

- Quiz 1 Chapter 1 Government AccountingDocument46 pagesQuiz 1 Chapter 1 Government Accountingswutea100% (1)

- Acctg For Revenue and Other ReceiptsDocument6 pagesAcctg For Revenue and Other ReceiptsLeonard CanamoNo ratings yet

- Oyster Bay 2014 Audited FinancialsDocument157 pagesOyster Bay 2014 Audited FinancialsNewsdayNo ratings yet

- 2020 21ASPBudgetOnline PDFDocument178 pages2020 21ASPBudgetOnline PDFJoyanta sorkarNo ratings yet

- ACC117-CON09 Module 3 ExamDocument16 pagesACC117-CON09 Module 3 ExamMarlon LadesmaNo ratings yet

- Test I - TRUE or FALSE (15 Points) : College of Business Management and AccountancyDocument2 pagesTest I - TRUE or FALSE (15 Points) : College of Business Management and AccountancyJamie Rose AragonesNo ratings yet

- Government Fundamentals QuizDocument9 pagesGovernment Fundamentals QuizAl Cariaga VelascoNo ratings yet