You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Forest Products: Advanced Technologies and Economic AnalysesFrom EverandForest Products: Advanced Technologies and Economic AnalysesNo ratings yet

- CVP, AVC, BudgetingDocument8 pagesCVP, AVC, BudgetingLeoreyn Faye MedinaNo ratings yet

- 2021 Answer Chapter 5 PDFDocument19 pages2021 Answer Chapter 5 PDFRianne NavidadNo ratings yet

- Cost Accounting Chapter 5 AnswersDocument11 pagesCost Accounting Chapter 5 AnswersJolina MostalesNo ratings yet

- Cost Accounting Chapter 5 AnswersDocument11 pagesCost Accounting Chapter 5 AnswersMark Angelo AlvarezNo ratings yet

- Answer Key Midterm Exam Cost Acounting With Solutions PART IIDocument7 pagesAnswer Key Midterm Exam Cost Acounting With Solutions PART IINoel Carpio100% (1)

- 2023 Answer CHAPTER 7 PDFDocument19 pages2023 Answer CHAPTER 7 PDFRianne NavidadNo ratings yet

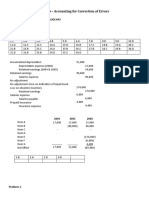

- Unit 4 - Accounting For Correction of Errors: Cabueñas, Brenton C. Bsa - 3 Audcap2 Problem 1 AnswersDocument14 pagesUnit 4 - Accounting For Correction of Errors: Cabueñas, Brenton C. Bsa - 3 Audcap2 Problem 1 AnswersSel BarrantesNo ratings yet

- Chapter 5 Job Order Costing 2019 Problem 2 Golden Shower CompanyDocument4 pagesChapter 5 Job Order Costing 2019 Problem 2 Golden Shower CompanyCertified Public AccountantNo ratings yet

- Chapter 01 - Answers - Job Order CostingDocument15 pagesChapter 01 - Answers - Job Order CostingEmmanuelle MazaNo ratings yet

- Solusi Kuis Jelang UTS-AkbiDocument7 pagesSolusi Kuis Jelang UTS-AkbiAnugerah BagusNo ratings yet

- Solutions To Sample Variable Absorption and Job Order CostingDocument7 pagesSolutions To Sample Variable Absorption and Job Order CostingWinter's ClandestineNo ratings yet

- Sol. Man. - Chapter 7 - Inventories - Ia Part 1aDocument19 pagesSol. Man. - Chapter 7 - Inventories - Ia Part 1aRezzan Joy Camara MejiaNo ratings yet

- Answer c20Document7 pagesAnswer c20Võ Huỳnh BăngNo ratings yet

- PRTC First Answer Key PDFDocument48 pagesPRTC First Answer Key PDFnanabaNo ratings yet

- PRTC 1stPB - 05.22 Sol FARDocument7 pagesPRTC 1stPB - 05.22 Sol FARCiatto SpotifyNo ratings yet

- Answer Chapter 4Document10 pagesAnswer Chapter 4Dela Cruz, Michelle Mae U.No ratings yet

- Sol. Man. - Chapter 7 - Inventories - Ia Part 1a - P 2,3,5,6 PDFDocument18 pagesSol. Man. - Chapter 7 - Inventories - Ia Part 1a - P 2,3,5,6 PDFLalaland Acads100% (2)

- 2023 Answer CHAPTER 6 PDFDocument8 pages2023 Answer CHAPTER 6 PDFRianne NavidadNo ratings yet

- Group 5Document16 pagesGroup 5Amelia AndrianiNo ratings yet

- Cost AccountingDocument24 pagesCost AccountingJalo NacionNo ratings yet

- C B FC 20% A: Debt RatioDocument4 pagesC B FC 20% A: Debt Ratiojohn condesNo ratings yet

- MAS-03 WorksheetDocument32 pagesMAS-03 WorksheetPaupauNo ratings yet

- Prelim ReviewerDocument19 pagesPrelim ReviewerMah2SetNo ratings yet

- PRTC 1stPB - 05.22 Sol APDocument4 pagesPRTC 1stPB - 05.22 Sol APCiatto SpotifyNo ratings yet

- Soultions - Chapter 3Document8 pagesSoultions - Chapter 3Naudia L. TurnbullNo ratings yet

- 2021 Answer Chapter 5Document15 pages2021 Answer Chapter 5prettyjessyNo ratings yet

- Standard Costing and Manufacturing Methods Answer To End of Chapter ExercisesDocument5 pagesStandard Costing and Manufacturing Methods Answer To End of Chapter ExercisesJay BrockNo ratings yet

- Working CapitalDocument2 pagesWorking CapitalPayal bhatiaNo ratings yet

- Factory Overhead 1,000,000 800,000: Problem 1 - The Denmark Company 1. Material CostDocument11 pagesFactory Overhead 1,000,000 800,000: Problem 1 - The Denmark Company 1. Material CostMico NechaldasNo ratings yet

- MS Practice SetsDocument2 pagesMS Practice SetsKindred WolfeNo ratings yet

- Chapter 10Document22 pagesChapter 10Dan ChuaNo ratings yet

- Team PRTC 1stPB May 2023 - Key AnswersDocument51 pagesTeam PRTC 1stPB May 2023 - Key Answerskathryn b. fordNo ratings yet

- Answer Key: Activity-Based Costing and Service Cost AllocationsDocument5 pagesAnswer Key: Activity-Based Costing and Service Cost AllocationsNoreenNo ratings yet

- Additional Answers Exercises COGM-COGS-JEs PDFDocument2 pagesAdditional Answers Exercises COGM-COGS-JEs PDFNicola Erika EnriquezNo ratings yet

- Cost AcctgDocument5 pagesCost AcctgJerome MonserratNo ratings yet

- ABC - Practice Set Answer and SolutionDocument4 pagesABC - Practice Set Answer and SolutionYvone Ehnnery BumosaoNo ratings yet

- Strategic Cost Management Exercises 12369Document2 pagesStrategic Cost Management Exercises 12369Arlene Diane OrozcoNo ratings yet

- Practice Problem 1 1. Journal EntriesDocument6 pagesPractice Problem 1 1. Journal Entriesjohn carlo tolentinoNo ratings yet

- Computations: Material X 20,000 X P 5.20 P 104,000 Material Y 24,000 X P 3.75 90,000 Indirect Materials 35,040 P 229,040Document5 pagesComputations: Material X 20,000 X P 5.20 P 104,000 Material Y 24,000 X P 3.75 90,000 Indirect Materials 35,040 P 229,040DaisyNo ratings yet

- Quiz Learning Task Group Work PDFDocument5 pagesQuiz Learning Task Group Work PDFEric Kevin LecarosNo ratings yet

- Final Exam MA2Document5 pagesFinal Exam MA2Aramina Cabigting BocNo ratings yet

- Chater 5Document9 pagesChater 5Shania LiwanagNo ratings yet

- Chapter 12Document7 pagesChapter 12Ednel GubacNo ratings yet

- Answer Key - Midterm ExamDocument5 pagesAnswer Key - Midterm ExamSilvermist AriaNo ratings yet

- 93 - Final Preaboard AFAR SolutionsDocument11 pages93 - Final Preaboard AFAR SolutionsLeiNo ratings yet

- Chap1-3 Illustration ProblemsDocument8 pagesChap1-3 Illustration ProblemscykablyatNo ratings yet

- MA1 - De thi giua ky - HK2 - 21-22 - send-đã chuyển đổiDocument4 pagesMA1 - De thi giua ky - HK2 - 21-22 - send-đã chuyển đổiThu ThanhNo ratings yet

- Traditional Approaches To Full Costing Answers To End of Chapter ExercisesDocument4 pagesTraditional Approaches To Full Costing Answers To End of Chapter ExercisesJay BrockNo ratings yet

- ACCOUNTING FOR LABOR AND OH LectureDocument13 pagesACCOUNTING FOR LABOR AND OH LectureNah HamzaNo ratings yet

- Cost&Mgmt SM Ch12Document5 pagesCost&Mgmt SM Ch12DivashiniNo ratings yet

- Mock Test 3 Online AnswerDocument4 pagesMock Test 3 Online AnswerLucia XIIINo ratings yet

- Topic 11 Homework AnswersDocument4 pagesTopic 11 Homework Answersiwhy_No ratings yet

- ch2 ExercisesDocument8 pagesch2 ExercisesDanicaEsponillaNo ratings yet

- Mas 1st PB October 2022 Suggested SolutionDocument8 pagesMas 1st PB October 2022 Suggested SolutionAsnifah AlinorNo ratings yet

- Chapter 6: Job Order Costing Exercise 6-1Document25 pagesChapter 6: Job Order Costing Exercise 6-1Iyah AmranNo ratings yet

- Modular Forms and Special Cycles on Shimura Curves. (AM-161)From EverandModular Forms and Special Cycles on Shimura Curves. (AM-161)No ratings yet

- SWOT InfographicsDocument20 pagesSWOT InfographicsArun Raj MNo ratings yet

- (Product) Construction EquipmentDocument17 pages(Product) Construction EquipmentmustangpipelinesNo ratings yet

- Legal Appointments ListDocument19 pagesLegal Appointments ListHeleen86% (7)

- Joint Ventures Act (Chapter 22-22)Document13 pagesJoint Ventures Act (Chapter 22-22)kailong wangNo ratings yet

- Amazon Seller BookkeepingDocument115 pagesAmazon Seller BookkeepingsezoNo ratings yet

- Method Statement For Application of Tiles WorksDocument19 pagesMethod Statement For Application of Tiles WorksHafiz M WaqasNo ratings yet

- Homework Practice CH 6 25th EdDocument4 pagesHomework Practice CH 6 25th EdThomas TermoteNo ratings yet

- Modern Business AnalysisDocument7 pagesModern Business AnalysisTANNU BBA LLBNo ratings yet

- CFZ Locators DirectoryDocument96 pagesCFZ Locators DirectoryMhel BundalianNo ratings yet

- Shahzad Farrukh - 00704963 - 1535-Qanmos College - IG-1Document11 pagesShahzad Farrukh - 00704963 - 1535-Qanmos College - IG-1Rashid Jamil100% (3)

- Samriddhi Quiz 2022 - FinalsDocument52 pagesSamriddhi Quiz 2022 - FinalsAnand Kumar100% (1)

- Summary Chapter 7 "Digital Marketing"Document2 pagesSummary Chapter 7 "Digital Marketing"Aziz Putra AkbarNo ratings yet

- A Leading Independent Investment Bank Based in Southern Europe, Latam and ChinaDocument32 pagesA Leading Independent Investment Bank Based in Southern Europe, Latam and ChinaDaniel GalvánNo ratings yet

- MNGT412 Mid Term Exam Assignment - 14128Document3 pagesMNGT412 Mid Term Exam Assignment - 14128Saad MajeedNo ratings yet

- Supply Chain Management SCM: Course: Management Information System MIS 201Document10 pagesSupply Chain Management SCM: Course: Management Information System MIS 201Abdelrahman MohamedNo ratings yet

- G12 LAS Applied Economics 1stQ&2ndQ Week 3to12Document29 pagesG12 LAS Applied Economics 1stQ&2ndQ Week 3to12Boss NenengNo ratings yet

- LULU ReportDocument4 pagesLULU Reportyovokew738No ratings yet

- Risk Assessment and Opportunity Assessment Matrix TableDocument1 pageRisk Assessment and Opportunity Assessment Matrix TableWin AsharNo ratings yet

- Chapter 3 - Engineering ManagementDocument6 pagesChapter 3 - Engineering ManagementJohn Philip Molina NuñezNo ratings yet

- Case Descriptive Solve 2Document8 pagesCase Descriptive Solve 2rocken samiunNo ratings yet

- Amusement Park ProjectDocument20 pagesAmusement Park ProjectdrkksarmaNo ratings yet

- Sama Sama LipDocument4 pagesSama Sama LipAnesa SimamoraNo ratings yet

- CMMI Adoption Transition Guidance PDFDocument53 pagesCMMI Adoption Transition Guidance PDFYadira VargasNo ratings yet

- CH 10 NotesDocument13 pagesCH 10 NotesmohamedNo ratings yet

- Financial Tools Week 5 Block BDocument9 pagesFinancial Tools Week 5 Block BBelen González BouzaNo ratings yet

- Campus Hiring - Final PlacementsDocument3 pagesCampus Hiring - Final Placementsumesh kumarNo ratings yet

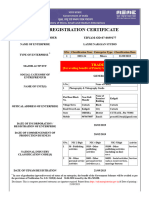

- Print - Udyam Registration CertificateDocument2 pagesPrint - Udyam Registration Certificatepranab123majiNo ratings yet

- 4882-Article Text-21748-1-10-20220329Document13 pages4882-Article Text-21748-1-10-20220329Aldela AlipNo ratings yet

- Management: Paper: 09, Entrepreneurship Development & Project ManagementDocument11 pagesManagement: Paper: 09, Entrepreneurship Development & Project ManagementDeepak Kumar PanigrahiNo ratings yet

- TD FHR1-50 R7 EngDocument24 pagesTD FHR1-50 R7 EngtiagoNo ratings yet