You might also like

- Business Development Strategy for the Upstream Oil and Gas IndustryFrom EverandBusiness Development Strategy for the Upstream Oil and Gas IndustryRating: 5 out of 5 stars5/5 (1)

- Case Analysis - Worldwide Paper Company: Finance ManagementDocument8 pagesCase Analysis - Worldwide Paper Company: Finance ManagementVivek SinghNo ratings yet

- Wealth Opportunities in Commercial Real Estate: Management, Financing, and Marketing of Investment PropertiesFrom EverandWealth Opportunities in Commercial Real Estate: Management, Financing, and Marketing of Investment PropertiesNo ratings yet

- AFM Tution A! Class VersionDocument11 pagesAFM Tution A! Class VersionMalcom Tafara MazengeraNo ratings yet

- Lessons in Corporate Finance: A Case Studies Approach to Financial Tools, Financial Policies, and ValuationFrom EverandLessons in Corporate Finance: A Case Studies Approach to Financial Tools, Financial Policies, and ValuationNo ratings yet

- Final Exam f02Document13 pagesFinal Exam f02Omar Ahmed ElkhalilNo ratings yet

- Strategy, Value and Risk: A Guide to Advanced Financial ManagementFrom EverandStrategy, Value and Risk: A Guide to Advanced Financial ManagementNo ratings yet

- 1 Mock Adv, Test (Q-Only) - Acf (Sgpin) - March 17th Final v23Document16 pages1 Mock Adv, Test (Q-Only) - Acf (Sgpin) - March 17th Final v23LuisaNo ratings yet

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsFrom EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo ratings yet

- FINA 410 - Exercises (NOV)Document7 pagesFINA 410 - Exercises (NOV)said100% (1)

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Final Practice Questions and SolutionsDocument12 pagesFinal Practice Questions and Solutionsshaikhnazneen100No ratings yet

- Streetsmart Financial Basics for Nonprofit ManagersFrom EverandStreetsmart Financial Basics for Nonprofit ManagersRating: 1 out of 5 stars1/5 (1)

- Financial Management: Thursday 9 June 2011Document9 pagesFinancial Management: Thursday 9 June 2011catcat1122No ratings yet

- F9FM RQB Qs - D08ojnpDocument62 pagesF9FM RQB Qs - D08ojnpErclan25% (4)

- STRATEGIC FINANCIAL MANAGEMENT EXAMDocument19 pagesSTRATEGIC FINANCIAL MANAGEMENT EXAMCLIVENo ratings yet

- FTX2024S - 2022 Test 2 Question PaperDocument9 pagesFTX2024S - 2022 Test 2 Question PaperhannaNo ratings yet

- MBA436 Exam - 2020Document8 pagesMBA436 Exam - 2020Nivi KumarNo ratings yet

- F9FM RQB Qs - j09kj NDocument64 pagesF9FM RQB Qs - j09kj NErclan0% (1)

- Fsav 6e Test Bank Mod13 TF MC 101520Document9 pagesFsav 6e Test Bank Mod13 TF MC 101520pauline leNo ratings yet

- Exam2 Solutions 40610 2008Document8 pagesExam2 Solutions 40610 2008blackghostNo ratings yet

- AFM - Mock Exam Answers - Dec18Document21 pagesAFM - Mock Exam Answers - Dec18David LeeNo ratings yet

- DynatronicsDocument24 pagesDynatronicsFezi Afesina Haidir90% (10)

- FINS1613 Business Finance Final Exam ReviewDocument30 pagesFINS1613 Business Finance Final Exam Reviewriders29No ratings yet

- Chapter 11 Question Answer KeyDocument91 pagesChapter 11 Question Answer KeyBrian Schweinsteiger Fok100% (1)

- Coroporate Finance ExamDocument4 pagesCoroporate Finance ExammustafaNo ratings yet

- CH 4Document20 pagesCH 4Waheed Zafar100% (1)

- Problems and Questions - 3Document6 pagesProblems and Questions - 3mashta04No ratings yet

- Fundamental of Financial Management May 1, 2020: Tutorial: Capital Cash Flow ProjectionDocument14 pagesFundamental of Financial Management May 1, 2020: Tutorial: Capital Cash Flow ProjectionNgân Võ Trần TuyếtNo ratings yet

- Full Download Corporate Finance Canadian 3rd Edition Berk Solutions ManualDocument36 pagesFull Download Corporate Finance Canadian 3rd Edition Berk Solutions Manualkisslingcicelypro100% (33)

- Dwnload Full Corporate Finance Canadian 3rd Edition Berk Solutions Manual PDFDocument36 pagesDwnload Full Corporate Finance Canadian 3rd Edition Berk Solutions Manual PDFgoblinerentageb0rls7100% (13)

- Case2 04 2Document9 pagesCase2 04 2writer topNo ratings yet

- FINA 6092 Case QuestionsDocument7 pagesFINA 6092 Case QuestionsKenny HoNo ratings yet

- Solutions Manual To Accompany Corporate Finance The Core 2nd Edition 9780132153683Document38 pagesSolutions Manual To Accompany Corporate Finance The Core 2nd Edition 9780132153683verawarnerq5cl100% (13)

- Coporate Finance AssignmentsDocument36 pagesCoporate Finance AssignmentsZahra HussainNo ratings yet

- Solutions Manual To Accompany Corporate Finance The Core 2nd Edition 9780132153683Document38 pagesSolutions Manual To Accompany Corporate Finance The Core 2nd Edition 9780132153683auntyprosperim1ru100% (15)

- Q and As-Corporate Financial Management - June 2010 Dec 2010 and June 2011Document71 pagesQ and As-Corporate Financial Management - June 2010 Dec 2010 and June 2011chisomo_phiri72290% (2)

- Questions For Group 1: S.B.Khatri-FM-AIMDocument6 pagesQuestions For Group 1: S.B.Khatri-FM-AIMAbhishek singhNo ratings yet

- Questions For Group 1: S.B.Khatri-FM-AIMDocument6 pagesQuestions For Group 1: S.B.Khatri-FM-AIMAbhishek singhNo ratings yet

- HW8 AnswersDocument6 pagesHW8 AnswersPushkar Singh100% (1)

- Chapter 5Document19 pagesChapter 5ragi malikNo ratings yet

- Canadian Tax Principles 2014 2015 Edition Volume I and Volume II 1st Edition Byrd Test BankDocument7 pagesCanadian Tax Principles 2014 2015 Edition Volume I and Volume II 1st Edition Byrd Test Bankdrkevinlee03071984jki100% (22)

- Assignment 4 Capital Budgeting and COCDocument3 pagesAssignment 4 Capital Budgeting and COCQurat Saboor100% (1)

- Chapter 3. Advanced Discounted Cash Flow TechniquesDocument16 pagesChapter 3. Advanced Discounted Cash Flow TechniquesHastings KapalaNo ratings yet

- ftyfyftyftymfmfhe surge in foreign direct investment spending is easing back from its 1994 highs as the authorities seek to channel funds into so-called priority areas—away from real estate and towards high-tech manufacturing production, infrastructure expenditure, energy and communications and, on a geographical basis, increasingly into the 18 inland provinces. Recent guidelines, however, continue to fail to offer sufficient incentives for expanded participation in the infrastructure sector as far as foreign investors are concerned. Plans to attract US$20 billion into China’s power sector by the year 2000, for example, are hampered by the ceiling of 15% put on investment rates of return. “Struggling With Reform,”he surge in foreign direct investment spending is easing back from its 1994 highs as the authorities seek to channel funds into so-called priority areas—away from real estate and towards high-tech manufacturing production, infrastructure expenditure, energy and communiDocument9 pagesftyfyftyftymfmfhe surge in foreign direct investment spending is easing back from its 1994 highs as the authorities seek to channel funds into so-called priority areas—away from real estate and towards high-tech manufacturing production, infrastructure expenditure, energy and communications and, on a geographical basis, increasingly into the 18 inland provinces. Recent guidelines, however, continue to fail to offer sufficient incentives for expanded participation in the infrastructure sector as far as foreign investors are concerned. Plans to attract US$20 billion into China’s power sector by the year 2000, for example, are hampered by the ceiling of 15% put on investment rates of return. “Struggling With Reform,”he surge in foreign direct investment spending is easing back from its 1994 highs as the authorities seek to channel funds into so-called priority areas—away from real estate and towards high-tech manufacturing production, infrastructure expenditure, energy and communiChineseaapNo ratings yet

- Fina1003abc - Hw#4Document4 pagesFina1003abc - Hw#4Peter JacksonNo ratings yet

- PART-A (Closed Book) (75 Mins)Document4 pagesPART-A (Closed Book) (75 Mins)DEVANSH CHANDRAWATNo ratings yet

- QUIZDocument5 pagesQUIZNastya MedlyarskayaNo ratings yet

- Year CF To Equity Int (1-t) CF To Firm: Variant 1 A-MDocument5 pagesYear CF To Equity Int (1-t) CF To Firm: Variant 1 A-MNastya MedlyarskayaNo ratings yet

- CFA Level 1 Study Guide: Corporate FinanceDocument343 pagesCFA Level 1 Study Guide: Corporate Financed-fbuser-32825803100% (12)

- 562 Spring2003Document5 pages562 Spring2003Emmy W. RosyidiNo ratings yet

- Fsav 6e Test Bank Mod14 TF MC 101520Document10 pagesFsav 6e Test Bank Mod14 TF MC 101520pauline leNo ratings yet

- Translation and Consolidation of Foreign Operations: Solutions Manual, Chapter 11Document87 pagesTranslation and Consolidation of Foreign Operations: Solutions Manual, Chapter 11Gillian Snelling100% (3)

- Capital Budgeting Decisions Made EasyDocument9 pagesCapital Budgeting Decisions Made EasyiteddyzNo ratings yet

- Financial MarketDocument81 pagesFinancial MarketBijay AgrawalNo ratings yet

- ACF 103 Exam Revision Qns 20151Document5 pagesACF 103 Exam Revision Qns 20151Riri FahraniNo ratings yet

- 7 Long Lived AssetsDocument2 pages7 Long Lived AssetsPratheep GsNo ratings yet

- Annuity Tables p6Document17 pagesAnnuity Tables p6williammasvinuNo ratings yet

- Financial Managemnet 3B LAO 2020 FinalDocument11 pagesFinancial Managemnet 3B LAO 2020 Finalsabelo.j.nkosi.5No ratings yet

- T Industries Financial StrategyDocument18 pagesT Industries Financial Strategymagnetbox8No ratings yet

- Lesson Plan Biological SciencesDocument73 pagesLesson Plan Biological SciencesSwati AmritNo ratings yet

- Rocky Mountain Mutual CaseDocument2 pagesRocky Mountain Mutual CaseSwati AmritNo ratings yet

- NRTI 2021 - MBA Trimester 1 Online SessionDocument2 pagesNRTI 2021 - MBA Trimester 1 Online SessionSwati AmritNo ratings yet

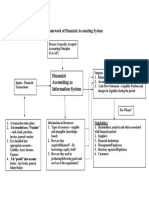

- Framework of Financial Accounting SystemDocument1 pageFramework of Financial Accounting SystemSwati AmritNo ratings yet

- The Next Manufacturing Revolution Is Here GRP 13Document11 pagesThe Next Manufacturing Revolution Is Here GRP 13Swati AmritNo ratings yet

- Text Book: Accounting: Text & Cases by Anthony, Hawkins & Merchant, 13 Edition (AHM)Document3 pagesText Book: Accounting: Text & Cases by Anthony, Hawkins & Merchant, 13 Edition (AHM)Swati AmritNo ratings yet

- NRTI - Lone Pine CafeDocument2 pagesNRTI - Lone Pine CafeSwati AmritNo ratings yet

- RivigoDocument8 pagesRivigoSwati AmritNo ratings yet

- Vegetable Market in IndiaDocument24 pagesVegetable Market in IndiaSwati AmritNo ratings yet

- Policy Making SlideDocument1 pagePolicy Making SlideSwati AmritNo ratings yet

- NRTI 2022 Financial Management Classroom Workings-13Document145 pagesNRTI 2022 Financial Management Classroom Workings-13Swati AmritNo ratings yet

- NRTI 2022 Financial Management Classroom Workings-11Document126 pagesNRTI 2022 Financial Management Classroom Workings-11Swati AmritNo ratings yet

- Chinese HiSpeed SystemDocument24 pagesChinese HiSpeed SystemSwati AmritNo ratings yet

- Hurricanes Katrina and Rita BibliographyDocument20 pagesHurricanes Katrina and Rita Bibliographyamericana100% (2)

- Social Challenges and Threats to Filipino FamiliesDocument24 pagesSocial Challenges and Threats to Filipino FamiliesKarlo Jayson AbilaNo ratings yet

- HolaDocument5 pagesHolaioritzNo ratings yet

- MINOR PPT 5th SEM-4Document22 pagesMINOR PPT 5th SEM-4parthasharma861No ratings yet

- d59687gc10 Toc GLMFDocument14 pagesd59687gc10 Toc GLMFmahmoud_elassaNo ratings yet

- SPI Firefight Rules (1976)Document20 pagesSPI Firefight Rules (1976)Anonymous OUtcQZleTQNo ratings yet

- Response To Non Motion DocumentDocument5 pagesResponse To Non Motion DocumentLaw&CrimeNo ratings yet

- Encuesta Sesión 6 - Inglés 3 - Septiembre 29 - Prof. Oscar NiquénDocument3 pagesEncuesta Sesión 6 - Inglés 3 - Septiembre 29 - Prof. Oscar NiquénRobacorazones TkmNo ratings yet

- EEDI and SEEMP Guide for Yachts and OSVsDocument3 pagesEEDI and SEEMP Guide for Yachts and OSVskuruvillaj2217No ratings yet

- WJ 2016 07Document158 pagesWJ 2016 07JastenJesusNo ratings yet

- Choosing the Right Career and Job RequirementsDocument2 pagesChoosing the Right Career and Job RequirementsdinnahNo ratings yet

- National Occupation Map in the Framework of Telecommunications Qualification FieldsDocument647 pagesNational Occupation Map in the Framework of Telecommunications Qualification FieldsIndra KurniawanNo ratings yet

- Review Quality Assurance PDFDocument339 pagesReview Quality Assurance PDFBelayneh TadesseNo ratings yet

- Employee Stock Option SchemeDocument6 pagesEmployee Stock Option Schemezenith chhablaniNo ratings yet

- Training Courses 2022-TUV NORD MalaysiaDocument12 pagesTraining Courses 2022-TUV NORD MalaysiaInstitute of Marketing & Training ALGERIANo ratings yet

- Application For Admission To Master of Computer Applications (MCA) COURSES, KERALA: 2010-2011Document5 pagesApplication For Admission To Master of Computer Applications (MCA) COURSES, KERALA: 2010-2011anishbaiNo ratings yet

- Gift TaxDocument3 pagesGift TaxBiswas LitonNo ratings yet

- The Analysis of Code Mixing in Short StoryDocument13 pagesThe Analysis of Code Mixing in Short StoryDharWin d'Wing-Wing d'AriestBoyz100% (1)

- RPH ActivitiesDocument10 pagesRPH ActivitiesFrance Dorothy SamortinNo ratings yet

- 61 Ways To Get More Exposure For Your MusicDocument17 pages61 Ways To Get More Exposure For Your MusicjanezslovenacNo ratings yet

- Q&A Accounting Sales and Purchase JournalsDocument16 pagesQ&A Accounting Sales and Purchase JournalsQand A BookkeepingNo ratings yet

- AMA - Australias Forest Industries at A GlanceDocument2 pagesAMA - Australias Forest Industries at A GlanceCarlos D. GuiradosNo ratings yet

- RVUN's Role in Power Generation in RajasthanDocument126 pagesRVUN's Role in Power Generation in Rajasthanvenka07No ratings yet

- Birla Sun Life Insurance Co. LTDDocument92 pagesBirla Sun Life Insurance Co. LTDdknigamNo ratings yet

- Ias 19 NotesDocument41 pagesIas 19 NotesTanyahl MatumbikeNo ratings yet

- Hometown Brochure DesignDocument2 pagesHometown Brochure DesignTiffanymcliu100% (1)

- Ebook - Asphalt Pavement Inspector's ManualDocument156 pagesEbook - Asphalt Pavement Inspector's Manualuputsvo52No ratings yet

- Analysis of The Documentary Sarhad: Submitted By: Muhammad Anees Sabir CheemaDocument5 pagesAnalysis of The Documentary Sarhad: Submitted By: Muhammad Anees Sabir CheemaAbdullah Sabir CheemaNo ratings yet

- EthicalDocument2 pagesEthicalJohn Christopher GozunNo ratings yet

- Hexaware DelistingDocument48 pagesHexaware DelistingNihal YnNo ratings yet