You might also like

- Pom Mock ExamDocument3 pagesPom Mock ExamManzar HussainNo ratings yet

- Business Budget - Assignment ProblemsDocument3 pagesBusiness Budget - Assignment ProblemsSHARATH JNo ratings yet

- Business Budget Excercise ProblemsDocument5 pagesBusiness Budget Excercise ProblemsSHARATH JNo ratings yet

- Budgeting OnlineDocument4 pagesBudgeting OnlineSoumendra RoyNo ratings yet

- FinancialManagement October2019 B B A WithCredits RegularJune-2017PatternSecondYearB B A 386E9789Document3 pagesFinancialManagement October2019 B B A WithCredits RegularJune-2017PatternSecondYearB B A 386E9789Mubin Shaikh NooruNo ratings yet

- Afar QuizDocument6 pagesAfar QuizJazzyNo ratings yet

- Corp-Bgt#IUP-X#Sept21#Aldira Jasmine R A#12010119190284Document4 pagesCorp-Bgt#IUP-X#Sept21#Aldira Jasmine R A#12010119190284aldira jasmineNo ratings yet

- Scenario Roletter Company Budgets For The Five Months 2007 Particulars Jan Feb Mar Apr MayDocument11 pagesScenario Roletter Company Budgets For The Five Months 2007 Particulars Jan Feb Mar Apr MayajithsubramanianNo ratings yet

- Comprehensive Illustration of Consolidated Financial Statements - Intercompany Sale of Inventories PDFDocument9 pagesComprehensive Illustration of Consolidated Financial Statements - Intercompany Sale of Inventories PDFamie honnagNo ratings yet

- CMA SS August 2018Document12 pagesCMA SS August 2018Goremushandu MungarevaniNo ratings yet

- Budgetary Control AssignmentDocument4 pagesBudgetary Control AssignmentYash AggarwalNo ratings yet

- Financial Reporting & Financial Statement Analysis Paper - Dse 6.1A FM - 80 Group - A (5x3 15)Document5 pagesFinancial Reporting & Financial Statement Analysis Paper - Dse 6.1A FM - 80 Group - A (5x3 15)tanmoy sardarNo ratings yet

- Sattva Paints F-Plan FinalDocument44 pagesSattva Paints F-Plan FinalShrushti MehtaNo ratings yet

- Previous Year Question Paper (FSA)Document16 pagesPrevious Year Question Paper (FSA)Alisha ShawNo ratings yet

- Exercise Working CapitalDocument4 pagesExercise Working CapitalShafiul AzamNo ratings yet

- Financial Statement Analysis Live ProjectDocument6 pagesFinancial Statement Analysis Live ProjectAnand Shekhar MishraNo ratings yet

- 13 17227rtp Ipcc Nov09 Paper3aDocument24 pages13 17227rtp Ipcc Nov09 Paper3aemmanuel JohnyNo ratings yet

- ACFrOgAMXLJQ31ib6NhLGI0LJ g6GJ517KX03aMrtqxVEqeGBZVYeNyhJHHN9 NBC Vi fXXpyOSGJRyPbtkRLA5DID6 - WJh7xyy7T4 - lcWF9qvk7GWZbEblGKEapUTdWZQyBqXGaUpCDjeEy - FVDocument6 pagesACFrOgAMXLJQ31ib6NhLGI0LJ g6GJ517KX03aMrtqxVEqeGBZVYeNyhJHHN9 NBC Vi fXXpyOSGJRyPbtkRLA5DID6 - WJh7xyy7T4 - lcWF9qvk7GWZbEblGKEapUTdWZQyBqXGaUpCDjeEy - FVmy VinayNo ratings yet

- SolutionDocument6 pagesSolutionJhazzie Dolor100% (1)

- Apr 18 Management Acc 2Document4 pagesApr 18 Management Acc 2Harish KapoorNo ratings yet

- JayathDocument5 pagesJayathJayaprakash JayathNo ratings yet

- 5th Year Pre-Final ExamDocument3 pages5th Year Pre-Final ExamJoshua UmaliNo ratings yet

- ACCG 2000 Week 1 Homework Questions PDFDocument2 pagesACCG 2000 Week 1 Homework Questions PDF张嘉雯No ratings yet

- Jun Zen Ralph V. Yap 3 Year - BSA Let's CheckDocument4 pagesJun Zen Ralph V. Yap 3 Year - BSA Let's CheckJunzen Ralph YapNo ratings yet

- Management Accounitng - 104 (I)Document4 pagesManagement Accounitng - 104 (I)Rudraksh PareyNo ratings yet

- Operation TestDocument4 pagesOperation TestFariya HossainNo ratings yet

- BF U4 (WC) - 1 PDFDocument14 pagesBF U4 (WC) - 1 PDFjrkukrejatrw253No ratings yet

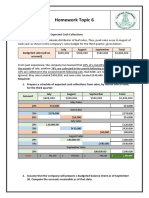

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- FM+ECO M.Test EM Question 26.02.2023Document6 pagesFM+ECO M.Test EM Question 26.02.2023harish jangidNo ratings yet

- Budgetary Control AssignmentDocument6 pagesBudgetary Control AssignmentBhavvyam BhatnagarNo ratings yet

- General Instructions: All The Questions Are CompulsoryDocument2 pagesGeneral Instructions: All The Questions Are CompulsoryJatin ChaudharyNo ratings yet

- Strategic Cost Management Assignment 3 Exercise 1 (Schedule of Expected Cash Collection)Document9 pagesStrategic Cost Management Assignment 3 Exercise 1 (Schedule of Expected Cash Collection)Rhea OraaNo ratings yet

- AFM-Session 25Document13 pagesAFM-Session 25abhijit.kundu23-25No ratings yet

- Simsr2 Mba B III FM Quep 1Document4 pagesSimsr2 Mba B III FM Quep 1Priyanka ReddyNo ratings yet

- Ratio Analysis ProblemsDocument4 pagesRatio Analysis ProblemsNavya SreeNo ratings yet

- BUDGETINGDocument7 pagesBUDGETINGuma selvarajNo ratings yet

- M/s XYZ Industries: Unsecured LoanDocument33 pagesM/s XYZ Industries: Unsecured LoanDaya SharmaNo ratings yet

- Business Accounting and Analysis (Semester I) q1xAKCGPn2Document3 pagesBusiness Accounting and Analysis (Semester I) q1xAKCGPn2PriyankaNo ratings yet

- II Internal Test - Accounting For Management - Important QuestionsDocument3 pagesII Internal Test - Accounting For Management - Important QuestionsSTARBOYNo ratings yet

- Test 1 & Test 2 - MADocument8 pagesTest 1 & Test 2 - MAChi Nguyễn Thị KimNo ratings yet

- Chap07 Rev. FI5 Ex PRDocument11 pagesChap07 Rev. FI5 Ex PRKhryzha Hanne Dela CruzNo ratings yet

- Fin Mang 2020Document3 pagesFin Mang 2020vinayakraj jamreNo ratings yet

- In Such A Way As To Assist The Management in The Creation of Policy and in The Day-To-Day Operations of An Undertaking." ElucidateDocument4 pagesIn Such A Way As To Assist The Management in The Creation of Policy and in The Day-To-Day Operations of An Undertaking." ElucidateKeran VarmaNo ratings yet

- Adobe Scan 02 Nov 2023Document2 pagesAdobe Scan 02 Nov 2023umangchh2306No ratings yet

- Dec 21Document26 pagesDec 21Prabhat Kumar GuptaNo ratings yet

- Required:: TH STDocument2 pagesRequired:: TH STChris - Ann Mae De LeonNo ratings yet

- F19 Chapter 18 Working CapitalDocument2 pagesF19 Chapter 18 Working CapitalAshwin MenghaniNo ratings yet

- Budgeting - ExamplesDocument2 pagesBudgeting - Examplessunil.ctNo ratings yet

- Test 1 - 2022 08 17Document3 pagesTest 1 - 2022 08 17MiclczeeNo ratings yet

- Project ReportDocument16 pagesProject ReportAshok PatelNo ratings yet

- DiscussionDocument2 pagesDiscussionHaniNo ratings yet

- Problem Based On Ratio Analysis - Part - 2Document1 pageProblem Based On Ratio Analysis - Part - 2Mohd shariqNo ratings yet

- Cable TV Installation Satellite TV Installation DSL Installation 0 $0Document30 pagesCable TV Installation Satellite TV Installation DSL Installation 0 $0Fatma MohomedNo ratings yet

- 202-Financial ManagementDocument5 pages202-Financial ManagementRAHUL GHOSALENo ratings yet

- Lecture 11Document26 pagesLecture 11Riaz Baloch Notezai100% (1)

- Paper - 8: Financial Management and Economics For Finance Section - A: Financial ManagementDocument23 pagesPaper - 8: Financial Management and Economics For Finance Section - A: Financial ManagementZrake 24No ratings yet

- Institutional Investment in Infrastructure in Emerging Markets and Developing EconomiesFrom EverandInstitutional Investment in Infrastructure in Emerging Markets and Developing EconomiesNo ratings yet

- Enabling the Business of Agriculture 2016: Comparing Regulatory Good PracticesFrom EverandEnabling the Business of Agriculture 2016: Comparing Regulatory Good PracticesNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- OLC Chap 20Document5 pagesOLC Chap 20NeelNo ratings yet

- Foreign Exchange Markets and Dealings: Solution RQ.33.3Document3 pagesForeign Exchange Markets and Dealings: Solution RQ.33.3NeelNo ratings yet

- OLC Chap 17Document3 pagesOLC Chap 17NeelNo ratings yet

- Chapter 22Document1 pageChapter 22NeelNo ratings yet

- 2 Sampling Methods Part2Document21 pages2 Sampling Methods Part2NeelNo ratings yet

- Anti-Ragging UndertakingsDocument1 pageAnti-Ragging UndertakingsNeelNo ratings yet

- Names of PartnerDocument7 pagesNames of PartnerDana-Zaza BajicNo ratings yet

- To The Lighthouse To The SelfDocument36 pagesTo The Lighthouse To The SelfSubham GuptaNo ratings yet

- (Oxford Readers) Michael Rosen - Catriona McKinnon - Jonathan Wolff - Political Thought-Oxford University Press (1999) - 15-18Document4 pages(Oxford Readers) Michael Rosen - Catriona McKinnon - Jonathan Wolff - Political Thought-Oxford University Press (1999) - 15-18jyahmedNo ratings yet

- IGNOU Vs MCI High Court JudgementDocument46 pagesIGNOU Vs MCI High Court Judgementom vermaNo ratings yet

- Assets Misappropriation in The Malaysian Public AnDocument5 pagesAssets Misappropriation in The Malaysian Public AnRamadona SimbolonNo ratings yet

- SWOT Analysis and Competion of Mangola Soft DrinkDocument2 pagesSWOT Analysis and Competion of Mangola Soft DrinkMd. Saiful HoqueNo ratings yet

- Unit 1 PDFDocument5 pagesUnit 1 PDFaadhithiyan nsNo ratings yet

- TallyDocument70 pagesTallyShree GuruNo ratings yet

- Keys For Change - Myles Munroe PDFDocument46 pagesKeys For Change - Myles Munroe PDFAndressi Label100% (2)

- Anaphy Finals ReviewerDocument193 pagesAnaphy Finals Reviewerxuxi dulNo ratings yet

- FINAL-Ordinance B.tech - 1Document12 pagesFINAL-Ordinance B.tech - 1Utkarsh PathakNo ratings yet

- Gender View in Transitional Justice IraqDocument21 pagesGender View in Transitional Justice IraqMohamed SamiNo ratings yet

- Torts ProjectDocument20 pagesTorts ProjectpriyaNo ratings yet

- Concept Note TemplateDocument2 pagesConcept Note TemplateDHYANA_1376% (17)

- Psychology Essay IntroductionDocument3 pagesPsychology Essay Introductionfesegizipej2100% (2)

- SOL 051 Requirements For Pilot Transfer Arrangements - Rev.1 PDFDocument23 pagesSOL 051 Requirements For Pilot Transfer Arrangements - Rev.1 PDFVembu RajNo ratings yet

- Periodical Test - English 5 - Q1Document7 pagesPeriodical Test - English 5 - Q1Raymond O. BergadoNo ratings yet

- Listening Practice9 GGBFDocument10 pagesListening Practice9 GGBFDtn NgaNo ratings yet

- Agara Lake BookDocument20 pagesAgara Lake Bookrisheek saiNo ratings yet

- Ia Prompt 12 Theme: Knowledge and Knower "Is Bias Inevitable in The Production of Knowledge?"Document2 pagesIa Prompt 12 Theme: Knowledge and Knower "Is Bias Inevitable in The Production of Knowledge?"Arham ShahNo ratings yet

- Sculi EMT enDocument1 pageSculi EMT enAndrei Bleoju100% (1)

- Teaching Resume-Anna BedillionDocument3 pagesTeaching Resume-Anna BedillionAnna Adams ProctorNo ratings yet

- Wendy in Kubricks The ShiningDocument5 pagesWendy in Kubricks The Shiningapi-270111486No ratings yet

- The Realistic NovelDocument25 pagesThe Realistic NovelNinna NannaNo ratings yet

- Executive Summary: Source of Commission: PMA Date of Commission: 16 March 2009 Date of Rank: 16 March 2016Document3 pagesExecutive Summary: Source of Commission: PMA Date of Commission: 16 March 2009 Date of Rank: 16 March 2016Yanna PerezNo ratings yet

- Cagayan Capitol Valley Vs NLRCDocument7 pagesCagayan Capitol Valley Vs NLRCvanessa_3No ratings yet

- The Difference Between The Bible and The Qur'an - Gary MillerDocument6 pagesThe Difference Between The Bible and The Qur'an - Gary Millersearch_truth100% (1)

- Anderson v. Eighth Judicial District Court - OpinionDocument8 pagesAnderson v. Eighth Judicial District Court - OpinioniX i0No ratings yet

- First Online Counselling CutoffDocument2 pagesFirst Online Counselling CutoffJaskaranNo ratings yet

- Returns To Scale in Beer and Wine: A P P L I C A T I O N 6 - 4Document1 pageReturns To Scale in Beer and Wine: A P P L I C A T I O N 6 - 4PaulaNo ratings yet