You might also like

- Local Government Taxation Short Cases ExplainedDocument1 pageLocal Government Taxation Short Cases ExplainedRichard Rhamil Carganillo Garcia Jr.No ratings yet

- Chapter 13 Test Bank Romney AisDocument35 pagesChapter 13 Test Bank Romney AisEarl QuimsonNo ratings yet

- 1st Pre-Board TaxationDocument11 pages1st Pre-Board Taxationrandyblanza2014No ratings yet

- Oblicon Practice Sets To Premidterms ReviewerDocument21 pagesOblicon Practice Sets To Premidterms ReviewerCharles LaspiñasNo ratings yet

- Philippine Securities and Banking Regulations SummaryDocument11 pagesPhilippine Securities and Banking Regulations SummaryCovi LokuNo ratings yet

- CPA Dreams Test BankDocument6 pagesCPA Dreams Test BankMayla MasxcxlNo ratings yet

- RFBT Quiz 1Document8 pagesRFBT Quiz 1JessaNo ratings yet

- Pamantasan ng Cabuyao Partnership Law ExamDocument4 pagesPamantasan ng Cabuyao Partnership Law ExamDan RyanNo ratings yet

- Tax DrillsDocument21 pagesTax DrillsJewelle CantosNo ratings yet

- ACCTG 25 Negotiable Instruments Law: Lyceum-Northwestern UniversityDocument4 pagesACCTG 25 Negotiable Instruments Law: Lyceum-Northwestern UniversityAmie Jane MirandaNo ratings yet

- Bl2: The Law On Private Corporation Final Examination General InstructionsDocument4 pagesBl2: The Law On Private Corporation Final Examination General InstructionsShaika HaceenaNo ratings yet

- Conditions foreign CPAs practice accountancy PhilippinesDocument3 pagesConditions foreign CPAs practice accountancy PhilippinesANGELU RANE BAGARES INTOLNo ratings yet

- Value Added TaxDocument4 pagesValue Added TaxAllen KateNo ratings yet

- DocumentDocument2 pagesDocumentAisaka Taiga0% (1)

- Business Law and Regulations Quiz: Partnerships 2Document15 pagesBusiness Law and Regulations Quiz: Partnerships 2Gabriela Marie F. Palatulan100% (1)

- Second PB Acctg 203BDocument12 pagesSecond PB Acctg 203BBella AyabNo ratings yet

- 68125672575bdf96fc857f403531f1c9-copyDocument9 pages68125672575bdf96fc857f403531f1c9-copyyour unreal0% (1)

- MCQ Pre-Long Exam On Value Added Tax May 19, 2020Document6 pagesMCQ Pre-Long Exam On Value Added Tax May 19, 2020JDR JDRNo ratings yet

- Qualifying Exam Reviewer - ObliconDocument10 pagesQualifying Exam Reviewer - ObliconFeeNo ratings yet

- TILA Compliance in Loan AgreementsDocument3 pagesTILA Compliance in Loan AgreementsJessa MaeNo ratings yet

- Cost Concept, Terminologies and BehaviorDocument8 pagesCost Concept, Terminologies and BehaviorANDREA NICOLE DE LEONNo ratings yet

- Value Added TaxDocument8 pagesValue Added TaxErica VillaruelNo ratings yet

- Fria 2010Document128 pagesFria 2010Mary Joyce Cornejo100% (1)

- TBCH08Document8 pagesTBCH08Butternut23No ratings yet

- Tax 1 PDFDocument17 pagesTax 1 PDFLeah MoscareNo ratings yet

- 11 Deductions From Gross Income (Expenses in General, Interest Expense and Taxes)Document18 pages11 Deductions From Gross Income (Expenses in General, Interest Expense and Taxes)Clarisse PelayoNo ratings yet

- Calculating Donor's Tax for Various Property DonationsDocument12 pagesCalculating Donor's Tax for Various Property DonationsKathrine CruzNo ratings yet

- III. Law On Pledge Mortgage Recto Law Maceda Law PD 957 and Assignment of Credit PDFDocument17 pagesIII. Law On Pledge Mortgage Recto Law Maceda Law PD 957 and Assignment of Credit PDFseya dummyNo ratings yet

- Tax Term Quiz TheoriesDocument6 pagesTax Term Quiz TheoriesRena Jocelle NalzaroNo ratings yet

- True or False Chapter 4 and 5 QuestionsDocument2 pagesTrue or False Chapter 4 and 5 Questionswaiting4y100% (1)

- Elimination RoundDocument11 pagesElimination RoundDeeNo ratings yet

- Donor's TaxDocument25 pagesDonor's TaxMark Erick Acojido RetonelNo ratings yet

- DLSL CPA Board Operation - Business LawDocument12 pagesDLSL CPA Board Operation - Business LawPrincessAngelaDeLeonNo ratings yet

- Quizzer 1 - OverallDocument25 pagesQuizzer 1 - OverallJan Elaine CalderonNo ratings yet

- Bouncing LawDocument3 pagesBouncing LawALYSSA MAE ABAAGNo ratings yet

- Multiple ChoiceDocument2 pagesMultiple ChoiceCarlo ParasNo ratings yet

- MAS Compilation of QuestionsDocument21 pagesMAS Compilation of QuestionsHazel Joy GaboNo ratings yet

- MAS First Preboard QuestionsDocument12 pagesMAS First Preboard QuestionsVillanueva, Mariella De VeraNo ratings yet

- AT-07 (FS Audit Process - Audit Planning)Document4 pagesAT-07 (FS Audit Process - Audit Planning)Bernadette PanicanNo ratings yet

- PRELIMS Law 3Document4 pagesPRELIMS Law 3ALMA MORENANo ratings yet

- At - Prelim Rev (875 MCQS) Red Sirug Page 1 of 85Document85 pagesAt - Prelim Rev (875 MCQS) Red Sirug Page 1 of 85Waleed MustafaNo ratings yet

- Tax Remedies and ProceduresDocument2 pagesTax Remedies and ProceduresEqui TinNo ratings yet

- Estate Tax Exam Multiple Choice QuestionsDocument8 pagesEstate Tax Exam Multiple Choice Questionsrey mark hamacNo ratings yet

- Actg 216 Reviwer Part 2 Without AnswerDocument5 pagesActg 216 Reviwer Part 2 Without Answercute meNo ratings yet

- Pledge and MortgageDocument5 pagesPledge and MortgageMhiletNo ratings yet

- TAX Final-PB FEUDocument9 pagesTAX Final-PB FEUkarim abitagoNo ratings yet

- Allowed Deductions From Gross IncomeDocument8 pagesAllowed Deductions From Gross Incomealliahbilities currentNo ratings yet

- Fischer - Pship LiquiDocument7 pagesFischer - Pship LiquiShawn Michael DoluntapNo ratings yet

- CPA review school Philippines tax questionsDocument9 pagesCPA review school Philippines tax questionsNah HamzaNo ratings yet

- Mastery in Management Advisory ServicesDocument12 pagesMastery in Management Advisory ServicesPrincess Claris Araucto0% (1)

- Topic 2 ExercisesDocument6 pagesTopic 2 ExercisesRaniel Pamatmat0% (1)

- Ia2 Quiz Notes and Bonds PayableDocument6 pagesIa2 Quiz Notes and Bonds PayableMicah ErguizaNo ratings yet

- Business Law Atty. Macmod, CPA 2018 Edition Obligations - 01 I. Identification (Basic Concept/Principles)Document9 pagesBusiness Law Atty. Macmod, CPA 2018 Edition Obligations - 01 I. Identification (Basic Concept/Principles)bobo kaNo ratings yet

- RFBT MidtermDocument27 pagesRFBT MidtermShane CabinganNo ratings yet

- Calculating Income Tax for COVID CompanyDocument2 pagesCalculating Income Tax for COVID CompanyRico, Jalaica B.No ratings yet

- General Provisions: The Law On PartnershipDocument38 pagesGeneral Provisions: The Law On PartnershipJoe P PokaranNo ratings yet

- Quiz 1 Tax Review 23 24Document5 pagesQuiz 1 Tax Review 23 24Aang GrandeNo ratings yet

- Basic Principles QuizzerDocument16 pagesBasic Principles Quizzerbobo kaNo ratings yet

- Evaluation ExamDocument4 pagesEvaluation ExamMj OrtizNo ratings yet

- Handout 01Document7 pagesHandout 01Josua PagcaliwaganNo ratings yet

- AU 9 Consideration of ICDocument11 pagesAU 9 Consideration of ICJb MejiaNo ratings yet

- AU 6 NO AnswersDocument75 pagesAU 6 NO AnswersAnonymous YtNo ratings yet

- RFBT - 01 - Obligations & ContractsDocument18 pagesRFBT - 01 - Obligations & ContractsJb MejiaNo ratings yet

- AU 7 Client AcceptanceDocument5 pagesAU 7 Client AcceptanceAnonymous YtNo ratings yet

- Advanced Financial Accounting & Reporting Business CombinationDocument8 pagesAdvanced Financial Accounting & Reporting Business CombinationAnonymous YtNo ratings yet

- (Regulatory Framework For Business Transactions) : PartnershipDocument10 pages(Regulatory Framework For Business Transactions) : PartnershipAnonymous YtNo ratings yet

- Resume, John Bernard MejiaDocument3 pagesResume, John Bernard MejiaAnonymous YtNo ratings yet

- Marketing Audit Findings and RecommendationsDocument3 pagesMarketing Audit Findings and RecommendationsAnonymous YtNo ratings yet

- John Bernard Mejia. Assignment in Expenditure CyclesDocument4 pagesJohn Bernard Mejia. Assignment in Expenditure CyclesAnonymous YtNo ratings yet

- Mejia, John Bernard C. Bsa - 3ADocument1 pageMejia, John Bernard C. Bsa - 3AAnonymous YtNo ratings yet

- Mejia, John Bernard C. ECO 302Document2 pagesMejia, John Bernard C. ECO 302Anonymous YtNo ratings yet

- Kpop Reflection PaperDocument2 pagesKpop Reflection PaperAnonymous YtNo ratings yet

- Headquarters 105Th (Pgn-East) Community Defense Center, 1Rcdg, Arescom CAMP LT Tito B Abat, Manaoag, PangasinanDocument1 pageHeadquarters 105Th (Pgn-East) Community Defense Center, 1Rcdg, Arescom CAMP LT Tito B Abat, Manaoag, PangasinanAnonymous YtNo ratings yet

- PFRS 11 vs PFRS for SEs and SMEs on Joint ArrangementsDocument3 pagesPFRS 11 vs PFRS for SEs and SMEs on Joint ArrangementsAnonymous YtNo ratings yet

- JBCM MGTDocument2 pagesJBCM MGTJb MejiaNo ratings yet

- Mejia, John Bernard C. Bsa - 3ADocument1 pageMejia, John Bernard C. Bsa - 3AAnonymous YtNo ratings yet

- John Bernard Mejia. Assignment in Expenditure CyclesDocument4 pagesJohn Bernard Mejia. Assignment in Expenditure CyclesAnonymous YtNo ratings yet

- College of Accountancy: University of Luzon Dagupan City Syllabus inDocument7 pagesCollege of Accountancy: University of Luzon Dagupan City Syllabus inAnonymous YtNo ratings yet

- University of Luzon IT21 Course PlanDocument5 pagesUniversity of Luzon IT21 Course PlanAnonymous YtNo ratings yet

- Final Examination in IT22: S B A I A CDocument8 pagesFinal Examination in IT22: S B A I A CJb MejiaNo ratings yet

- Toyota Production SystemDocument27 pagesToyota Production Systemmentee111100% (3)

- SG 2Document43 pagesSG 2SWETCHCHA MISKANo ratings yet

- Chapter V. Unit1Document9 pagesChapter V. Unit1Rosewhayne Tiffany TejadaNo ratings yet

- Bule Hora University Faculty of Engineering and Technology Departement of Architecture Building Materials and Construction I Chapter-2Document34 pagesBule Hora University Faculty of Engineering and Technology Departement of Architecture Building Materials and Construction I Chapter-2yisihak mathewosNo ratings yet

- Eddy Mata: San Diego CA 626 922 8310Document1 pageEddy Mata: San Diego CA 626 922 8310Eddy MataNo ratings yet

- FP Lean Warehouse OperationsDocument8 pagesFP Lean Warehouse OperationsIbrahim SkakriNo ratings yet

- W3. Present Worth AnalysisDocument26 pagesW3. Present Worth AnalysisChrisThunder555No ratings yet

- 2018 Coleman Tax Return PDFDocument46 pages2018 Coleman Tax Return PDFJonathan Brinton100% (1)

- ACAAP2 - Week 8 MODULE - Audit of Prepaid Expenses, Deferred Charges and Other Current LiabilitiesDocument8 pagesACAAP2 - Week 8 MODULE - Audit of Prepaid Expenses, Deferred Charges and Other Current LiabilitiesDee100% (1)

- Trade UnionDocument14 pagesTrade UnionSaurabh KhandaskarNo ratings yet

- Export Procedure and DocumentationDocument30 pagesExport Procedure and DocumentationSiddhartha NeogNo ratings yet

- HistoryDocument4 pagesHistorynathaniel borlazaNo ratings yet

- DFCDocument1 pageDFCJolina BanzonNo ratings yet

- KapilDocument109 pagesKapilShivmohan JaiswalNo ratings yet

- Shariah Princiles in Islamic Securities Bba, Murabahah, Istisna & SalamDocument47 pagesShariah Princiles in Islamic Securities Bba, Murabahah, Istisna & Salamilyan_izaniNo ratings yet

- SE ContractDocument21 pagesSE Contractaugusta.mironNo ratings yet

- Case of Electric ToothbrushDocument5 pagesCase of Electric ToothbrushЮрий КориневскийNo ratings yet

- Pricing Strategy and Growth of Dmart - Project (1) UpdatedDocument17 pagesPricing Strategy and Growth of Dmart - Project (1) Updatednilesh.das22hNo ratings yet

- Pillar Stone Case StudyDocument3 pagesPillar Stone Case StudyAlexandra IthalNo ratings yet

- Project CapsicumDocument120 pagesProject CapsicumAdrian Edmund Shuu67% (3)

- Vidhey Patel ResumeDocument2 pagesVidhey Patel ResumeadelaideglxNo ratings yet

- AUG 10 Danske EMEADailyDocument3 pagesAUG 10 Danske EMEADailyMiir ViirNo ratings yet

- Rural Marketing 260214 PDFDocument282 pagesRural Marketing 260214 PDFarulsureshNo ratings yet

- China's Economic Growth and Foreign Business Environment in 40 CharactersDocument23 pagesChina's Economic Growth and Foreign Business Environment in 40 CharactersAsad BilalNo ratings yet

- Audit Cum Risk Compliance Officer, Provisional ResultDocument15 pagesAudit Cum Risk Compliance Officer, Provisional ResultWAQAS AHMEDNo ratings yet

- Swot Analysis OF A CompanyDocument34 pagesSwot Analysis OF A CompanyJacob PruittNo ratings yet

- Future of Finance:: 10 Trends To Watch NowDocument23 pagesFuture of Finance:: 10 Trends To Watch NowisudhNo ratings yet

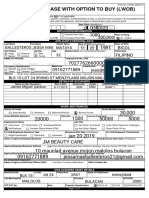

- Lwob - Application-Form Edited Edited EditedDocument2 pagesLwob - Application-Form Edited Edited Editedjessamaeballesteros21100% (1)

- The GoalDocument4 pagesThe GoalJenny LorNo ratings yet

- Inventory management key processes and termsDocument17 pagesInventory management key processes and termsVishnu Kumar SNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Invested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)From EverandInvested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)Rating: 4.5 out of 5 stars4.5/5 (43)

- What Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemFrom EverandWhat Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- Owner Operator Trucking Business Startup: How to Start Your Own Commercial Freight Carrier Trucking Business With Little Money. Bonus: Licenses and Permits ChecklistFrom EverandOwner Operator Trucking Business Startup: How to Start Your Own Commercial Freight Carrier Trucking Business With Little Money. Bonus: Licenses and Permits ChecklistRating: 5 out of 5 stars5/5 (6)

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- The Payroll Book: A Guide for Small Businesses and StartupsFrom EverandThe Payroll Book: A Guide for Small Businesses and StartupsRating: 5 out of 5 stars5/5 (1)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipFrom EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipNo ratings yet

- Tax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsFrom EverandTax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsRating: 4 out of 5 stars4/5 (1)

- Lower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderRating: 5 out of 5 stars5/5 (4)

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- The Hidden Wealth Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth Nations: The Scourge of Tax HavensRating: 4.5 out of 5 stars4.5/5 (40)

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Freight Broker Business Startup: Step-by-Step Guide to Start, Grow and Run Your Own Freight Brokerage Company In in Less Than 4 Weeks. Includes Business Plan TemplatesFrom EverandFreight Broker Business Startup: Step-by-Step Guide to Start, Grow and Run Your Own Freight Brokerage Company In in Less Than 4 Weeks. Includes Business Plan TemplatesRating: 5 out of 5 stars5/5 (1)