You might also like

- Green Business - People - Planet - Profit - 2023/24: A Comprehensive Guide to Building & Managing A Sustainable Business.: Volume 1, #1From EverandGreen Business - People - Planet - Profit - 2023/24: A Comprehensive Guide to Building & Managing A Sustainable Business.: Volume 1, #1No ratings yet

- Responsible Business: How to Manage a CSR Strategy SuccessfullyFrom EverandResponsible Business: How to Manage a CSR Strategy SuccessfullyNo ratings yet

- ESG Framework in India Explained PointwiseDocument8 pagesESG Framework in India Explained PointwisevinayaikNo ratings yet

- Dissertation ProposalDocument10 pagesDissertation ProposalVanshika LambaNo ratings yet

- Evaluating The Contribution of CSR in Achieving UN's Sustainable Development GoalsDocument8 pagesEvaluating The Contribution of CSR in Achieving UN's Sustainable Development GoalsDrunk funNo ratings yet

- Raising The Bar: Rethinking The Role of Business in The Sustainable Development GoalsDocument32 pagesRaising The Bar: Rethinking The Role of Business in The Sustainable Development GoalsOxfamNo ratings yet

- Raising The Bar: Rethinking The Role of Business in The Sustainable Development GoalsDocument32 pagesRaising The Bar: Rethinking The Role of Business in The Sustainable Development GoalsOxfamNo ratings yet

- Raising The Bar: Rethinking The Role of Business in The Sustainable Development GoalsDocument32 pagesRaising The Bar: Rethinking The Role of Business in The Sustainable Development GoalsOxfamNo ratings yet

- Raising The Bar: Rethinking The Role of Business in The Sustainable Development GoalsDocument32 pagesRaising The Bar: Rethinking The Role of Business in The Sustainable Development GoalsOxfamNo ratings yet

- Ey Esg Megatrends and Opportunities Shaping Future Report - v2Document29 pagesEy Esg Megatrends and Opportunities Shaping Future Report - v2lewi251202No ratings yet

- Summary Article On SEBI Notification On BRSR - V1Document4 pagesSummary Article On SEBI Notification On BRSR - V1Disha MalkaniNo ratings yet

- SKY ManagementDocument8 pagesSKY ManagementΜαρία ΤιγκαράκηNo ratings yet

- The Business Case For SDGS: An Analysis of Inclusive Business Models in Emerging EconomiesDocument11 pagesThe Business Case For SDGS: An Analysis of Inclusive Business Models in Emerging Economieswell itsbusNo ratings yet

- Azlarbek 1Document7 pagesAzlarbek 1AzlarbekNo ratings yet

- Corporate Social Responsibility RevisedDocument9 pagesCorporate Social Responsibility RevisedKirtikkcNo ratings yet

- SDG Compass For BusinessDocument30 pagesSDG Compass For BusinessSIPIROK100% (1)

- Corporate Sustainability 1Document7 pagesCorporate Sustainability 1otieno vilmaNo ratings yet

- The Linkage of SDG and Corporate Actions With Reference To Companies Act, 2013Document5 pagesThe Linkage of SDG and Corporate Actions With Reference To Companies Act, 2013rohanNo ratings yet

- ESG-Environmental Social and GovernanceDocument5 pagesESG-Environmental Social and GovernancevinayaikNo ratings yet

- Deloitte CH - Risk Responsible Business in A Post-Covid WorldDocument4 pagesDeloitte CH - Risk Responsible Business in A Post-Covid WorldGeoBonNo ratings yet

- Diwakar Pandey GM18090 (BECG Mid Term)Document6 pagesDiwakar Pandey GM18090 (BECG Mid Term)Diwakar PandeyNo ratings yet

- Towards Stakeholder Capitalism: How We Can Get There: The GRI PerspectiveDocument4 pagesTowards Stakeholder Capitalism: How We Can Get There: The GRI PerspectiveYi-liang ChenNo ratings yet

- CSR in An MNC in BD, UnileverDocument23 pagesCSR in An MNC in BD, UnileverAbdullah Al Mahmud50% (2)

- Do Environmental, Social and Corporate Governance Practices Enhance Malaysian Public-Listed Companies Performance?Document28 pagesDo Environmental, Social and Corporate Governance Practices Enhance Malaysian Public-Listed Companies Performance?Li Chen LeeNo ratings yet

- ESG Indicator Metrics Used by Organisations To Assess The Degree of Sustainability in CompaniesDocument12 pagesESG Indicator Metrics Used by Organisations To Assess The Degree of Sustainability in CompaniesIJAERS JOURNALNo ratings yet

- Shaping The Future1Document38 pagesShaping The Future1indy_4xNo ratings yet

- C Min (2023) 13 Add1 Final - enDocument18 pagesC Min (2023) 13 Add1 Final - enComunicarSe-ArchivoNo ratings yet

- Global Compact Sust DevDocument3 pagesGlobal Compact Sust DevDaniela FrumusachiNo ratings yet

- Reference Material Module 2Document21 pagesReference Material Module 2sarat c padhihariNo ratings yet

- Unit 2Document35 pagesUnit 2Pallavi KapoorNo ratings yet

- B READY Methodology HandbookDocument770 pagesB READY Methodology HandbookAWARE GUEHIDANo ratings yet

- CSR and Regulatory IssuesDocument28 pagesCSR and Regulatory IssuesRishabh SoniNo ratings yet

- PWC Taking The Lead Achieving The Global GoalsDocument24 pagesPWC Taking The Lead Achieving The Global GoalsMilind Sangtiani100% (1)

- Aakash Vishwakarma (PG Thesis)Document75 pagesAakash Vishwakarma (PG Thesis)Akrity ParasharNo ratings yet

- Shaping The Future MckinseyDocument38 pagesShaping The Future MckinseyGareth CaponNo ratings yet

- SSA 02 - Sustainability Reporting Framework and ConceptsDocument5 pagesSSA 02 - Sustainability Reporting Framework and ConceptsRycia Tariga TamNo ratings yet

- Influence of Green Accounting Environmental PerforDocument16 pagesInfluence of Green Accounting Environmental Perforppg.rismafebriani02No ratings yet

- Hu 308 ProjectDocument17 pagesHu 308 ProjectLavish OberoiNo ratings yet

- Corporate Governance Assignment (AKSHAY ANAND - 181001501007)Document11 pagesCorporate Governance Assignment (AKSHAY ANAND - 181001501007)Akshay YaduvanshiNo ratings yet

- Empresas 2015 Nueva ArquitecturaDocument21 pagesEmpresas 2015 Nueva Arquitecturajuan31988No ratings yet

- Corporate Social Responsibility of Brac BankDocument8 pagesCorporate Social Responsibility of Brac BankRashedul HasanNo ratings yet

- Budgeting ESG Synergy, CFO News, ETCFODocument5 pagesBudgeting ESG Synergy, CFO News, ETCFORamisha JainNo ratings yet

- Corporate Social Responsibility in IndiaDocument22 pagesCorporate Social Responsibility in IndiaFaizKazi140% (1)

- Eng - Fadilla Primaria Dewi - Karya Akhir - Naskah Ringkas - FEB - 2018 PDFDocument22 pagesEng - Fadilla Primaria Dewi - Karya Akhir - Naskah Ringkas - FEB - 2018 PDFFadilla Primaria DewiNo ratings yet

- The Effect of Sustainability Practices Based On Sustainable Development Goals (SDGS) To Firm Performance and Moderation Effect of Independent AssuranceDocument22 pagesThe Effect of Sustainability Practices Based On Sustainable Development Goals (SDGS) To Firm Performance and Moderation Effect of Independent AssuranceFadilla Primaria DewiNo ratings yet

- Business As Usual Will Not Save The PlanetDocument8 pagesBusiness As Usual Will Not Save The PlanetElisa Pavez A.No ratings yet

- Sustainability 15 13506Document22 pagesSustainability 15 13506Rudana SausanNo ratings yet

- Chapter 1Document7 pagesChapter 1Danrev dela CruzNo ratings yet

- Corporate SocialDocument15 pagesCorporate SocialdnadilNo ratings yet

- SS - CSR4Stakeholders of CSR and Their RolesDocument12 pagesSS - CSR4Stakeholders of CSR and Their Rolessenshourya66No ratings yet

- SDG Report - Team 4Document6 pagesSDG Report - Team 4salnasuNo ratings yet

- The Three Pillars of CSRDocument22 pagesThe Three Pillars of CSRDianne GloriaNo ratings yet

- 9-Reforming Business For The 21st Century - A Framework For The Future of The CorporationDocument33 pages9-Reforming Business For The 21st Century - A Framework For The Future of The CorporationsiddhantNo ratings yet

- Impact of Corporate Social Responsibility Activities Communicating About A BrandDocument11 pagesImpact of Corporate Social Responsibility Activities Communicating About A BrandIJRASETPublicationsNo ratings yet

- International Perspectives Individual AssignmentDocument14 pagesInternational Perspectives Individual AssignmentFrancesco CambriaNo ratings yet

- Piyali Mitra - Content Submission (The Connection Between CSR and Corporate Governance-Conceptually Analysing The Concepts)Document6 pagesPiyali Mitra - Content Submission (The Connection Between CSR and Corporate Governance-Conceptually Analysing The Concepts)Piyali MitraNo ratings yet

- Social Impact and CSR Leadership Get SeriousDocument2 pagesSocial Impact and CSR Leadership Get SeriousWSSocialImpactNo ratings yet

- Scoping The Evolution of CorpoDocument22 pagesScoping The Evolution of CorpoTABAH RIZKINo ratings yet

- Corporate Social Responsibility - A Case Study of Microsoft Corporation (India) Pvt. LTDDocument16 pagesCorporate Social Responsibility - A Case Study of Microsoft Corporation (India) Pvt. LTDGaurav ChauhanNo ratings yet

- Sustainability Standards and Instruments (Second Edition)From EverandSustainability Standards and Instruments (Second Edition)No ratings yet

- Institute of Law, Nirma University Law of Evidence 2021-22Document6 pagesInstitute of Law, Nirma University Law of Evidence 2021-22Colonial LegislationNo ratings yet

- In The High Court of Karnataka, at Bengaluru Regular First Appeal No. - /2020 BetweenDocument13 pagesIn The High Court of Karnataka, at Bengaluru Regular First Appeal No. - /2020 BetweenColonial Legislation100% (1)

- Discussions On Uniform Civil CodeDocument9 pagesDiscussions On Uniform Civil CodeColonial LegislationNo ratings yet

- RSADocument22 pagesRSAColonial Legislation100% (1)

- Research Proposal For Company LawDocument11 pagesResearch Proposal For Company LawColonial LegislationNo ratings yet

- Case Law AnalysisDocument10 pagesCase Law AnalysisColonial LegislationNo ratings yet

- Israel - Palestine ConflictDocument30 pagesIsrael - Palestine ConflictColonial LegislationNo ratings yet

- Analysis of of The Principles of JurisprudenceDocument5 pagesAnalysis of of The Principles of JurisprudenceColonial LegislationNo ratings yet

- HK Land Law ExamDocument8 pagesHK Land Law ExamSunita RokaNo ratings yet

- Indian Penal Code (IPC) Detailed Notes and Study Material - LexFortiDocument98 pagesIndian Penal Code (IPC) Detailed Notes and Study Material - LexFortiakash100% (1)

- 2022-TN-Forecast of AcquisitionslDocument65 pages2022-TN-Forecast of AcquisitionslDorris GardenerNo ratings yet

- Notification Pharmacist Allopathy VacancyDocument4 pagesNotification Pharmacist Allopathy VacancyHikaNo ratings yet

- VAT CLAIM FOR REFUND - Northern Mini Hydro Vs CIRDocument2 pagesVAT CLAIM FOR REFUND - Northern Mini Hydro Vs CIRChristine Gel MadrilejoNo ratings yet

- Personal Bond of IndemnityDocument4 pagesPersonal Bond of IndemnityAmit Kumar100% (1)

- Dawn RaidDocument3 pagesDawn RaidNithi100% (1)

- Education Sciences: Inclusion and Special EducationDocument17 pagesEducation Sciences: Inclusion and Special Educationzed cozNo ratings yet

- CASE - Separate Legal Personality Salomon V A Salomon and Co LTD (1897) AC 22 Case SummaryDocument2 pagesCASE - Separate Legal Personality Salomon V A Salomon and Co LTD (1897) AC 22 Case SummarychavoNo ratings yet

- Conwi vs. Court of Tax Appeals, 213 SCRA 83, August 31, 1992Document14 pagesConwi vs. Court of Tax Appeals, 213 SCRA 83, August 31, 1992Jane BandojaNo ratings yet

- Auditing Standards, Statements and Guidance Notes - An OverviewDocument64 pagesAuditing Standards, Statements and Guidance Notes - An OverviewPraneethNo ratings yet

- Property Case Digest - Sept 10Document10 pagesProperty Case Digest - Sept 10Ayana LockeNo ratings yet

- Home Loan/Lap: Individual Co-Applicant/Guarantor SheetDocument4 pagesHome Loan/Lap: Individual Co-Applicant/Guarantor Sheetmadhukar sahayNo ratings yet

- Civil Liberties and The Mass Media Under Martial Law in The PhilippinesDocument14 pagesCivil Liberties and The Mass Media Under Martial Law in The PhilippinesMightyFilerNo ratings yet

- Republic Act For Penology ExamDocument5 pagesRepublic Act For Penology ExamHaysheryl Vallejo SalamancaNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument9 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledMara ClaraNo ratings yet

- So F Directed On 5:00 PM Wi:: The RevenueDocument4 pagesSo F Directed On 5:00 PM Wi:: The RevenueCarlo John C. RuelanNo ratings yet

- Din en 1253 - 2Document3 pagesDin en 1253 - 2Renzo Marquina AstoNo ratings yet

- Resolution Granting Automatic Pemanent TotalDocument3 pagesResolution Granting Automatic Pemanent TotalAshNo ratings yet

- Bsl605:Legal Aspects of Business: Dr. Arpit SidhuDocument22 pagesBsl605:Legal Aspects of Business: Dr. Arpit SidhuShivati Singh KahlonNo ratings yet

- PMT Online Schedule-2023Document3 pagesPMT Online Schedule-2023NeoNo ratings yet

- MR V P Mittal Vs Punjab National Bank On 13 December 2011Document3 pagesMR V P Mittal Vs Punjab National Bank On 13 December 2011Sukhbir Singh SandhuNo ratings yet

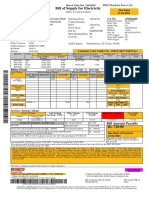

- Bill of Supply For Electricity: Due Date: 13-04-2021Document1 pageBill of Supply For Electricity: Due Date: 13-04-2021Aditya RajNo ratings yet

- District 2B Public DocumentsDocument123 pagesDistrict 2B Public DocumentsLocal 5 News (WOI-TV)No ratings yet

- Lamar Murry Hearing TranscriptDocument19 pagesLamar Murry Hearing TranscriptJoe EskenaziNo ratings yet

- David J StiansenDocument2 pagesDavid J StiansengaryNo ratings yet

- Crim Pro Subject Outline 2022.j.villenaDocument4 pagesCrim Pro Subject Outline 2022.j.villenaAnastacio, Micah Ann, G.No ratings yet

- S75 of The Contracts ActDocument37 pagesS75 of The Contracts ActJacky AngNo ratings yet

- 3pREMEDIAL LAWDocument10 pages3pREMEDIAL LAWmerk22paulNo ratings yet

- 2.3 Cabauatan v. VenidaDocument1 page2.3 Cabauatan v. VenidaRain HofileñaNo ratings yet