You might also like

- Capital Reduction 2Document6 pagesCapital Reduction 2SANJIB SHARMANo ratings yet

- Internal ReconstructionDocument26 pagesInternal ReconstructionRajesh NangaliaNo ratings yet

- Adv Acc - 3 CHDocument21 pagesAdv Acc - 3 CHhassan nassereddineNo ratings yet

- Accounting Redemption of Debentures 1642416359Document19 pagesAccounting Redemption of Debentures 1642416359Shashank SikarwarNo ratings yet

- Redemption of Preference Shares IllustrationsDocument6 pagesRedemption of Preference Shares IllustrationsManya GargNo ratings yet

- Consolidated Balance Sheet of Hold and SubDocument31 pagesConsolidated Balance Sheet of Hold and SubRahul NandurkarNo ratings yet

- DocumentDocument4 pagesDocumentTûshar ThakúrNo ratings yet

- Accounting For Holding Co. (Lecture 3) : Total 12,00,000 6,00,000Document6 pagesAccounting For Holding Co. (Lecture 3) : Total 12,00,000 6,00,000Michael JimNo ratings yet

- Class 12 Accountancy CBSE Cash Flow StatementDocument7 pagesClass 12 Accountancy CBSE Cash Flow StatementSarvesh SreedharNo ratings yet

- Financial Statements of a Company: Preparation of P&L and Balance SheetDocument40 pagesFinancial Statements of a Company: Preparation of P&L and Balance SheetyashbhardwajNo ratings yet

- CBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Document12 pagesCBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Sayantan DebnathNo ratings yet

- Practice Accounts Prime PDFDocument56 pagesPractice Accounts Prime PDFShraddha NepalNo ratings yet

- Particulars: © The Institute of Chartered Accountants of IndiaDocument17 pagesParticulars: © The Institute of Chartered Accountants of IndiaPraveen Reddy DevanapalleNo ratings yet

- Accountancy Assignment Grade 12Document4 pagesAccountancy Assignment Grade 12sharu SKNo ratings yet

- FAC114 Financial Accounting Redemption of Preference SharesDocument4 pagesFAC114 Financial Accounting Redemption of Preference SharesDhairya ShahNo ratings yet

- PART-B Analysis Test YtDocument8 pagesPART-B Analysis Test YtRiddhi GuptaNo ratings yet

- 232 FM AssignmentDocument17 pages232 FM Assignmentbhupesh joshiNo ratings yet

- Internal ReconstructionDocument8 pagesInternal Reconstructionsmit9993No ratings yet

- CHARTERED ACCOUNTANCY PROFESSIONAL CAP-II REVISION TEST PAPERDocument21 pagesCHARTERED ACCOUNTANCY PROFESSIONAL CAP-II REVISION TEST PAPERbinu100% (1)

- Jorpati, Kathmandu Pre-Board Examination-2077 Subject: Principles of Accounting II Grade: XII Time: 3 Hrs FM: 100 PM: 32Document3 pagesJorpati, Kathmandu Pre-Board Examination-2077 Subject: Principles of Accounting II Grade: XII Time: 3 Hrs FM: 100 PM: 32Abin DhakalNo ratings yet

- Accounting concepts and statutory auditDocument4 pagesAccounting concepts and statutory auditNamrata RamgadeNo ratings yet

- Accounts Important Questions by Rajat Jain SirDocument31 pagesAccounts Important Questions by Rajat Jain SirRajiv JhaNo ratings yet

- Corporate Accounting ProblemDocument6 pagesCorporate Accounting ProblemparameshwaraNo ratings yet

- Screenshot 2023-04-12 at 5.34.59 PMDocument24 pagesScreenshot 2023-04-12 at 5.34.59 PMManthan JainNo ratings yet

- RTP June 19 QnsDocument15 pagesRTP June 19 QnsbinuNo ratings yet

- June 2019Document182 pagesJune 2019shankar k.c.No ratings yet

- 1 Financial Statements of CompaniesDocument21 pages1 Financial Statements of CompaniesShivaram ShivaramNo ratings yet

- Financial Accounting & AuditingDocument13 pagesFinancial Accounting & Auditingkashish mehtaNo ratings yet

- Xii Acc Worksheetss-30-55Document26 pagesXii Acc Worksheetss-30-55Unknown patelNo ratings yet

- Additional Questions 5Document13 pagesAdditional Questions 5Sanjay SiddharthNo ratings yet

- 3526 - 25114 - Textbooksolution - PDF 3Document108 pages3526 - 25114 - Textbooksolution - PDF 3dhanuka jiNo ratings yet

- Adobe Scan Jan 30, 2023Document6 pagesAdobe Scan Jan 30, 2023Karan RajakNo ratings yet

- QP CODE: 22100973: Reg No: NameDocument6 pagesQP CODE: 22100973: Reg No: NameSajithaNo ratings yet

- CONSOLIDATED STATEMENTDocument8 pagesCONSOLIDATED STATEMENTPrageeth Roshan WeerathungaNo ratings yet

- Paper - 5: Advanced Accounting Questions Answer The Following (Give Adequate Working Notes in Support of Your Answer)Document56 pagesPaper - 5: Advanced Accounting Questions Answer The Following (Give Adequate Working Notes in Support of Your Answer)Basant OjhaNo ratings yet

- Inp 2205 - Advance Accounting - Question PaperDocument10 pagesInp 2205 - Advance Accounting - Question PaperAnshit BahediaNo ratings yet

- Alpha Arts College Corporate Accounting ExamDocument3 pagesAlpha Arts College Corporate Accounting Exammahabalu123456789No ratings yet

- Admission of A Partner PDFDocument8 pagesAdmission of A Partner PDFSpandan DasNo ratings yet

- Cash Flow Statement for John & Joe LtdDocument4 pagesCash Flow Statement for John & Joe LtdSanjayNo ratings yet

- Internal ReconsrtuctionDocument33 pagesInternal ReconsrtuctionRenuNo ratings yet

- Corrporate ModelDocument10 pagesCorrporate Modelnithinjoseph562005No ratings yet

- AFM Assignment 2021Document7 pagesAFM Assignment 2021NARENDRA PATTELANo ratings yet

- June 2019 All Paper SuggestedDocument120 pagesJune 2019 All Paper SuggestedEdtech NepalNo ratings yet

- Additional Illustrations-5Document19 pagesAdditional Illustrations-5goyalmanasvi06No ratings yet

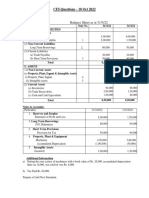

- CFS Questions - 18 - OCT - 2022Document5 pagesCFS Questions - 18 - OCT - 2022Kartik SujanNo ratings yet

- Valuation of GoodwillDocument15 pagesValuation of Goodwillbtsa1262013No ratings yet

- Adv Acc Q.P 2Document7 pagesAdv Acc Q.P 2Swetha ReddyNo ratings yet

- IPS Academy, IBMR Session Jan-June 2020 BBA II Semester: Assignment Of: Financial ManagementDocument6 pagesIPS Academy, IBMR Session Jan-June 2020 BBA II Semester: Assignment Of: Financial ManagementDrShailesh Singh ThakurNo ratings yet

- Corporate Accounting - I Semester ExaminationDocument7 pagesCorporate Accounting - I Semester ExaminationVijay KumarNo ratings yet

- Cash Flow Statement - 2Document9 pagesCash Flow Statement - 2Midhun PerozhiNo ratings yet

- Accounts Mock Test May 2019Document18 pagesAccounts Mock Test May 2019poojitha reddyNo ratings yet

- Revision Questions XiiDocument11 pagesRevision Questions XiiSahej Kaur AroraNo ratings yet

- 19013comp Sugans Pe2 Accounting Cp8 5Document12 pages19013comp Sugans Pe2 Accounting Cp8 5Ubaidulla MachingalNo ratings yet

- Series 1 PDFDocument8 pagesSeries 1 PDFBKLMMDFKLFBNo ratings yet

- Management Accouting Assignment4 Manish Chauhan (09-1128) .Document17 pagesManagement Accouting Assignment4 Manish Chauhan (09-1128) .manishNo ratings yet

- FR (New) A MTP Final Mar 2021Document17 pagesFR (New) A MTP Final Mar 2021ritz meshNo ratings yet

- 3054 Faca-V L 8Document8 pages3054 Faca-V L 8ab6154951No ratings yet

- Adobe Scan 05 Mar 2022Document5 pagesAdobe Scan 05 Mar 2022Titiksha Joshi100% (1)

- Corporate Accounting Exam Questions PaperDocument7 pagesCorporate Accounting Exam Questions PaperAmmar Bin NasirNo ratings yet

- As Technology Gets Better, Will Society Get Worse The New YorkerDocument6 pagesAs Technology Gets Better, Will Society Get Worse The New YorkerNaomi SaldanhaNo ratings yet

- Business cycles LESSON - 4Document24 pagesBusiness cycles LESSON - 4Naomi SaldanhaNo ratings yet

- Lecture 2 Academic ScriptDocument6 pagesLecture 2 Academic ScriptNaomi SaldanhaNo ratings yet

- L3 - Academic ScriptDocument10 pagesL3 - Academic ScriptNaomi SaldanhaNo ratings yet

- L1 - Academic ScriptDocument9 pagesL1 - Academic ScriptNaomi SaldanhaNo ratings yet

- St. Joseph's College Internal ReconstructionDocument3 pagesSt. Joseph's College Internal ReconstructionNaomi SaldanhaNo ratings yet

- Problems On Mod 1Document11 pagesProblems On Mod 1Naomi SaldanhaNo ratings yet

- Mod 1 Final Accounts NotesDocument8 pagesMod 1 Final Accounts NotesNaomi SaldanhaNo ratings yet

- Complete Worksheet of Mod 1-Final Accounts of CompaniesDocument10 pagesComplete Worksheet of Mod 1-Final Accounts of CompaniesNaomi SaldanhaNo ratings yet

- Practice Question Paper - Financial AccountingDocument6 pagesPractice Question Paper - Financial AccountingNaomi SaldanhaNo ratings yet

- MOD - 3 FINAL ACCOUNTS - QuestionsDocument6 pagesMOD - 3 FINAL ACCOUNTS - QuestionsNaomi SaldanhaNo ratings yet

- Brief Introduction To Kannada Language: Geographic DistributionDocument16 pagesBrief Introduction To Kannada Language: Geographic DistributionNaomi SaldanhaNo ratings yet

- Book Value Per ShareDocument29 pagesBook Value Per ShareKaren MagsayoNo ratings yet

- IFM Chapter 11 AnswersDocument6 pagesIFM Chapter 11 AnswersPatty CherotschiltschNo ratings yet

- Cashflow Ex Cers IceDocument1 pageCashflow Ex Cers IceNuman RoxNo ratings yet

- Investment advice for client seeking retirement planningDocument16 pagesInvestment advice for client seeking retirement planningJaihindNo ratings yet

- Guide To Self Directed Investing - Equity Trust CompanyDocument24 pagesGuide To Self Directed Investing - Equity Trust CompanyEquityTrustNo ratings yet

- 5 SEM BCOM - Entrepreneurship DevelopmentDocument64 pages5 SEM BCOM - Entrepreneurship DevelopmentSparsh Jain75% (16)

- BHM EntrepreneurshipDocument106 pagesBHM EntrepreneurshipSabinaNo ratings yet

- Colgate Financial Model SolvedDocument33 pagesColgate Financial Model SolvedVvb SatyanarayanaNo ratings yet

- Financial Accounting GlossaryDocument5 pagesFinancial Accounting GlossaryDheeraj SunthaNo ratings yet

- Stocks and Bonds PDFDocument2 pagesStocks and Bonds PDF霏霏No ratings yet

- Chapter 36Document20 pagesChapter 36Flores Renato Jr. S.No ratings yet

- TBChap 005Document39 pagesTBChap 005QUANG DUONG HIENNo ratings yet

- Naik Divides L&T To Rule The Future: Companies EngineeringDocument5 pagesNaik Divides L&T To Rule The Future: Companies EngineeringAnupamaa SinghNo ratings yet

- Strategic Evaluation of TITAN Industries LimitedDocument27 pagesStrategic Evaluation of TITAN Industries LimitedDev SharmaNo ratings yet

- Recent DevelopmentDocument3 pagesRecent DevelopmentPooja SinghNo ratings yet

- Notes Lecture IIDocument2 pagesNotes Lecture IICigdemSahinNo ratings yet

- David Einhorn Grant's ConferenceDocument89 pagesDavid Einhorn Grant's ConferenceCanadianValueNo ratings yet

- 9.2 IAS36 - Impairment of Assets 1Document41 pages9.2 IAS36 - Impairment of Assets 1Given RefilweNo ratings yet

- Unit 1 Role of Financial Institutions and MarketsDocument11 pagesUnit 1 Role of Financial Institutions and MarketsGalijang ShampangNo ratings yet

- CG European Capital Growth Fund: StrategyDocument2 pagesCG European Capital Growth Fund: Strategyapi-25889552No ratings yet

- PT VOKSEL ELECTRIC TBKDocument14 pagesPT VOKSEL ELECTRIC TBKIra MakingNo ratings yet

- Supercomnet Technologies - Shaping Noteworthy ProspectsDocument6 pagesSupercomnet Technologies - Shaping Noteworthy ProspectsFong Kah YanNo ratings yet

- The 10 Minute Stock Trader S Guide To Triple Stock Profits 1Document11 pagesThe 10 Minute Stock Trader S Guide To Triple Stock Profits 1sachin jainNo ratings yet

- Chapter 7 - Problem SOlvingDocument26 pagesChapter 7 - Problem SOlvingDesirre Transona100% (1)

- Airline Finance PDFDocument137 pagesAirline Finance PDFMini Thomas100% (3)

- Liquidity and Stock MarketDocument4 pagesLiquidity and Stock MarketIMaths PowaiNo ratings yet

- Dividend-Protected Convertible Bonds and the Disappearance of Call DelayDocument54 pagesDividend-Protected Convertible Bonds and the Disappearance of Call DelayGursharanSinghBhueNo ratings yet

- 2023 Outlook InsuranceDocument43 pages2023 Outlook InsuranceTerryNo ratings yet

- Bse Nse222Document81 pagesBse Nse222Ravi SutharNo ratings yet

- CHP 13 Testbank 2Document15 pagesCHP 13 Testbank 2judyNo ratings yet