You might also like

- Loss On Sale of An Asset 95780Document4 pagesLoss On Sale of An Asset 95780alok pratap singhNo ratings yet

- Financial Accounting & Analysis-CompressedDocument4 pagesFinancial Accounting & Analysis-Compressedvipin mohanNo ratings yet

- Fakruddin (Financial Accounting Analysis L)Document21 pagesFakruddin (Financial Accounting Analysis L)mohammad fakhruddinNo ratings yet

- Accounting BasicsDocument24 pagesAccounting BasicsRhey LuceroNo ratings yet

- TOPIC 2 Duality of TransactionsDocument4 pagesTOPIC 2 Duality of TransactionsMwai MuthoniNo ratings yet

- Financial Accounting & AnalysisDocument10 pagesFinancial Accounting & Analysisdeval mahajanNo ratings yet

- TO Accounting: PembahasanDocument17 pagesTO Accounting: PembahasanFitria Ramadhani AyuningtyasNo ratings yet

- Financial Accounting AnalysisDocument13 pagesFinancial Accounting AnalysisNikhil Agrawal88% (8)

- TASK-10: Submitted by Sincy Mathew Institute of Management and Technology, PunnapraDocument4 pagesTASK-10: Submitted by Sincy Mathew Institute of Management and Technology, PunnapraSincy MathewNo ratings yet

- Shs Abm Gr12 Fabm2 q1 m4-Statement-Of-cash-flow FinalDocument12 pagesShs Abm Gr12 Fabm2 q1 m4-Statement-Of-cash-flow FinalKye RauleNo ratings yet

- Accounting Tutorials Day 1Document8 pagesAccounting Tutorials Day 1Richboy Jude VillenaNo ratings yet

- Finance Assi FinalDocument8 pagesFinance Assi FinalVagdevi YadavNo ratings yet

- Cash Flow StatementsDocument30 pagesCash Flow Statementsp9198817011No ratings yet

- Suggested Solution To Tutorial On SOCFDocument5 pagesSuggested Solution To Tutorial On SOCFLiyendra FernandoNo ratings yet

- Financial Accounting and Analysis iUwmYf3ArOxyDocument6 pagesFinancial Accounting and Analysis iUwmYf3ArOxypayal guravNo ratings yet

- Final Account (Satyanath Mohapatra)Document38 pagesFinal Account (Satyanath Mohapatra)smrutiranjan swainNo ratings yet

- TOPIC 6 - Bookeeping ProceduresDocument31 pagesTOPIC 6 - Bookeeping Procedureseizah_osman3408100% (1)

- Financial Accounting & Analysis - N (1A)Document10 pagesFinancial Accounting & Analysis - N (1A)Tajinder MatharuNo ratings yet

- Cash Flow AssignmentDocument39 pagesCash Flow AssignmentMUHAMMAD HASSANNo ratings yet

- Financial Accounting and Analysis AssignmentDocument10 pagesFinancial Accounting and Analysis AssignmentRahul RJNo ratings yet

- Financial Accounting and Analysis AssignmentDocument13 pagesFinancial Accounting and Analysis Assignmentbhaskar paliwalNo ratings yet

- Class 11 Accountancy NCERT Textbook Part-II Chapter 10 Financial Statements-IIDocument70 pagesClass 11 Accountancy NCERT Textbook Part-II Chapter 10 Financial Statements-IIPathan KausarNo ratings yet

- Financial Accounting-1Document10 pagesFinancial Accounting-1Dharmik UpadhyayNo ratings yet

- Chapter 1-4Document20 pagesChapter 1-4BookDownNo ratings yet

- Chapter 4Document4 pagesChapter 4mayhipolito01No ratings yet

- Fundamentals of Accountancy, Business and Management 2Document58 pagesFundamentals of Accountancy, Business and Management 2Carmina Dongcayan100% (1)

- Chapter 1 FNM108Document13 pagesChapter 1 FNM108Aldrin John TungolNo ratings yet

- Accounting Volume 2 Canadian 9th Edition Horngren Solutions Manual 1Document76 pagesAccounting Volume 2 Canadian 9th Edition Horngren Solutions Manual 1edna100% (31)

- Financial Accounting and AnalysisDocument4 pagesFinancial Accounting and Analysisbhupendra mehraNo ratings yet

- Fabm2 Module 5Document4 pagesFabm2 Module 5Rea Mariz Jordan100% (1)

- Senior High School Department: LessonDocument10 pagesSenior High School Department: LessonJane Decenine CativoNo ratings yet

- (IV) Statement of Cash-FlowsDocument38 pages(IV) Statement of Cash-FlowsmusthaqhassanNo ratings yet

- Hock CMA P1 2019 (Sections A, B & C) AnswersDocument17 pagesHock CMA P1 2019 (Sections A, B & C) AnswersNathan DrakeNo ratings yet

- Financial Accounting & AnalysisDocument2 pagesFinancial Accounting & AnalysisTangerine Ila TomarNo ratings yet

- Financial Accounting and AnalysisDocument8 pagesFinancial Accounting and AnalysismeghaNo ratings yet

- Jenjen 2Document11 pagesJenjen 2Kim FloresNo ratings yet

- Self-Learning Kit: Region I Schools Division of Ilocos Sur Bantay, Ilocos SurDocument13 pagesSelf-Learning Kit: Region I Schools Division of Ilocos Sur Bantay, Ilocos SurLiam Aleccis Obrero CabanitNo ratings yet

- Financial Statements - II: 360 AccountancyDocument65 pagesFinancial Statements - II: 360 AccountancyshantX100% (1)

- Wlof Hsac Gnitarepo Gncinfina: Jumble LettersDocument23 pagesWlof Hsac Gnitarepo Gncinfina: Jumble LettersAce Soleil RiegoNo ratings yet

- Statement of Cash Flows and BudgetsDocument66 pagesStatement of Cash Flows and BudgetsJack100% (1)

- Fundamentals of Accountancy, Business and Management 1Document25 pagesFundamentals of Accountancy, Business and Management 1Worship Songs / Choreo / LyricsNo ratings yet

- FRAV Individual Assignment - Pranjali Silimkar - 2016PGP278Document12 pagesFRAV Individual Assignment - Pranjali Silimkar - 2016PGP278pranjaligNo ratings yet

- Financial Accounting and AnalysisDocument6 pagesFinancial Accounting and AnalysistanmayNo ratings yet

- Chapter 13 - Statement of Cash Flows SummaryDocument13 pagesChapter 13 - Statement of Cash Flows SummaryPRITHWISH MITRANo ratings yet

- Module I: Basics of Credit and Credit Process: Chapter 4: Cash Flow Statement AnalysisDocument26 pagesModule I: Basics of Credit and Credit Process: Chapter 4: Cash Flow Statement Analysissagar7No ratings yet

- Week 12 EntrepreneurshipDocument7 pagesWeek 12 EntrepreneurshipMarcel Baring ImperialNo ratings yet

- Accounting PrincipleDocument24 pagesAccounting PrincipleMonirHRNo ratings yet

- Module 4 Statement of Cash Flows 1Document9 pagesModule 4 Statement of Cash Flows 1Kimberly BalontongNo ratings yet

- Chapter 4Document18 pagesChapter 4Amjad J AliNo ratings yet

- LCCI Level 2 Text Book (Word)Document126 pagesLCCI Level 2 Text Book (Word)Phyu Nu NgeNo ratings yet

- Classification of Cash Flow Statement: ExampleDocument6 pagesClassification of Cash Flow Statement: ExampleRISHABH GOYALNo ratings yet

- Chapter 3 NotesDocument30 pagesChapter 3 NotesnoxoloNo ratings yet

- Double Entry System & Accounting Equation: by - Mrs. Dilshad D. JalnawallaDocument34 pagesDouble Entry System & Accounting Equation: by - Mrs. Dilshad D. JalnawallaTufail GanaieNo ratings yet

- Class 11 Accountancy Chapter-10 Revision NotesDocument7 pagesClass 11 Accountancy Chapter-10 Revision NotesBadal singh ThakurNo ratings yet

- Financial Accounting & AnalysisDocument7 pagesFinancial Accounting & AnalysisMitaliNo ratings yet

- Assessment - 1: Student Name: Arth Patel Student Id: UEDT505Document12 pagesAssessment - 1: Student Name: Arth Patel Student Id: UEDT505Fayyaz HussainNo ratings yet

- Introduction To Accounting (Sheet.1)Document9 pagesIntroduction To Accounting (Sheet.1)Rithvik SangilirajNo ratings yet

- ABM 1 (Reviewer)Document15 pagesABM 1 (Reviewer)Lynne YsaNo ratings yet

- Chapter Zakat Acc For Ibis-1 - 42051Document20 pagesChapter Zakat Acc For Ibis-1 - 42051Aisyah AnuarNo ratings yet

- Business Economics AssigmentDocument4 pagesBusiness Economics AssigmentDhanshree Thorat AmbavleNo ratings yet

- Information Systems For Managers AssignmentDocument2 pagesInformation Systems For Managers AssignmentDhanshree Thorat AmbavleNo ratings yet

- Management Theory and Practice AssignmentDocument4 pagesManagement Theory and Practice AssignmentDhanshree Thorat AmbavleNo ratings yet

- Marketing Management AssignmentDocument2 pagesMarketing Management AssignmentDhanshree Thorat AmbavleNo ratings yet

- Comparative Study of Constitutions TopicDocument68 pagesComparative Study of Constitutions TopicDhanshree Thorat AmbavleNo ratings yet

- Geographical Indication AssignmentDocument29 pagesGeographical Indication AssignmentDhanshree Thorat AmbavleNo ratings yet

- Copyright Law AssignmentDocument31 pagesCopyright Law AssignmentDhanshree Thorat Ambavle100% (1)

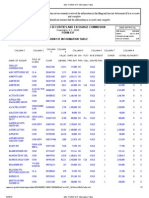

- SEC FORM 13-F Information TableDocument7 pagesSEC FORM 13-F Information TableBecket AdamsNo ratings yet

- Chapter 6Document17 pagesChapter 6Yusuf Raharja100% (1)

- Reserves & ProvisionsDocument20 pagesReserves & ProvisionsAhmad Tariq BhattiNo ratings yet

- TutorialsDocument16 pagesTutorialsBee ChunweiNo ratings yet

- Gray Company S Financial Statements Showed Income Before Income Taxes ofDocument1 pageGray Company S Financial Statements Showed Income Before Income Taxes ofFreelance WorkerNo ratings yet

- Tegar Dwi Laksono AKDocument4 pagesTegar Dwi Laksono AKTegarNo ratings yet

- Hindenburgresearch Com AdaniDocument20 pagesHindenburgresearch Com AdaniOmkar KambleNo ratings yet

- Week 4 Balance OffDocument16 pagesWeek 4 Balance OffNor LailyNo ratings yet

- Statement 1H0TFNJ Nov-2022Document3 pagesStatement 1H0TFNJ Nov-2022Mary MacLellanNo ratings yet

- Case 26 - Analysis GuidanceDocument2 pagesCase 26 - Analysis GuidanceVoramon PolkertNo ratings yet

- Chapter 3Document17 pagesChapter 3seneshaw tibebuNo ratings yet

- Nifty Weightage Understanding Its Significance in The Indian Stock MarketDocument23 pagesNifty Weightage Understanding Its Significance in The Indian Stock Marketmahedihasan141997No ratings yet

- Donina Halley vs. Printwell Inc.Document2 pagesDonina Halley vs. Printwell Inc.JermaeDelosSantosNo ratings yet

- Multiple Choice QuestionsDocument17 pagesMultiple Choice QuestionsNguyen Thanh Thao (K16 HCM)No ratings yet

- Slide of Chapter 1Document29 pagesSlide of Chapter 1Uyen ThuNo ratings yet

- Specimen Copy of Notice Sent To Members About Forfeiture of Shares Who Failed To Pay Call Money - 13 06 2022Document2 pagesSpecimen Copy of Notice Sent To Members About Forfeiture of Shares Who Failed To Pay Call Money - 13 06 2022i.pmanaseNo ratings yet

- Chapter 4 - Audit of InvestmentsDocument45 pagesChapter 4 - Audit of InvestmentsClene DoconteNo ratings yet

- Business Finance Week 2-3Document7 pagesBusiness Finance Week 2-3Luisa RadaNo ratings yet

- Jonaryl S. MacatuggalDocument2 pagesJonaryl S. MacatuggalJohn Paul TomasNo ratings yet

- On January 1 2012 Norma Smith and Grant Wood Formed PDFDocument1 pageOn January 1 2012 Norma Smith and Grant Wood Formed PDFAnbu jaromiaNo ratings yet

- Chapter 13C Optional Standard DeductionsDocument3 pagesChapter 13C Optional Standard DeductionsJason Mables100% (1)

- Lecture 4 DCF Valuation The Discounted Dividend ModelDocument6 pagesLecture 4 DCF Valuation The Discounted Dividend ModelBryan NgoNo ratings yet

- This Study Resource Was: Accounting 225 - Quiz #2 - Version A - April 13, 2016Document8 pagesThis Study Resource Was: Accounting 225 - Quiz #2 - Version A - April 13, 2016chiji chzzzmeowNo ratings yet

- Excel File of Financial Projection and FundingDocument21 pagesExcel File of Financial Projection and FundingDave John LavariasNo ratings yet

- Unit 6Document42 pagesUnit 6yebegashetNo ratings yet

- Questions 2Document12 pagesQuestions 2venice cambryNo ratings yet

- Group 2 Case 1 Assignment Bubble Bee Organic The Need For Pro Forma Financial Modeling SupplDocument13 pagesGroup 2 Case 1 Assignment Bubble Bee Organic The Need For Pro Forma Financial Modeling SupplSarah WuNo ratings yet

- Acctg 402Document9 pagesAcctg 402Marriah Izzabelle Suarez RamadaNo ratings yet

- Chapter 1 Audit of Cash and Cash Equivalents PDFDocument129 pagesChapter 1 Audit of Cash and Cash Equivalents PDFCasey Mae NeriNo ratings yet

- FM NCPDocument33 pagesFM NCPSmrithi BakkaNo ratings yet