You might also like

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- Icici Marketing Strategy of Icici BankDocument68 pagesIcici Marketing Strategy of Icici BankShilpi KumariNo ratings yet

- Summer Training Project ReportDocument118 pagesSummer Training Project Reporttariquewali11No ratings yet

- Cash Management - ICICI BankDocument64 pagesCash Management - ICICI BankRini Akshat Govil75% (4)

- General Management Project On "Analysis of Banking Industry"Document24 pagesGeneral Management Project On "Analysis of Banking Industry"Sharvil PanvekarNo ratings yet

- A Project Report ON Industrial Exposure: (Icici Bank)Document59 pagesA Project Report ON Industrial Exposure: (Icici Bank)Gaurav MandhanaNo ratings yet

- March 2023Document69 pagesMarch 2023Vaheed ManiharNo ratings yet

- AcknowledgementDocument90 pagesAcknowledgementMohammed Miqdaad RizviNo ratings yet

- "Icici": Industrial Exposur/E Project OnDocument57 pages"Icici": Industrial Exposur/E Project OnShubham KhuranaNo ratings yet

- ICICI Bank's Marketing StrategyDocument73 pagesICICI Bank's Marketing StrategyVaheed ManiharNo ratings yet

- March 2023Document69 pagesMarch 2023Vaheed ManiharNo ratings yet

- Financial Service Offered HDFCDocument103 pagesFinancial Service Offered HDFCdeepak GuptaNo ratings yet

- Project On Icic BankDocument69 pagesProject On Icic BankDavinder Singh BanssNo ratings yet

- Financial Service Offered HDFCDocument102 pagesFinancial Service Offered HDFCdeepak GuptaNo ratings yet

- Retail Banking and Operations at HDFC BankDocument38 pagesRetail Banking and Operations at HDFC Bankambikesh dwivediNo ratings yet

- Vaheedmanihar 1Document72 pagesVaheedmanihar 1Vaheed ManiharNo ratings yet

- 152 - Mandar Zagde - General MangementDocument55 pages152 - Mandar Zagde - General MangementMAHIMA RAONo ratings yet

- Tybms Sem V Project 2017-18Document54 pagesTybms Sem V Project 2017-18sagarNo ratings yet

- Project ReportDocument85 pagesProject ReportramankumarbadNo ratings yet

- Leveraging Digital Channels For Enhancing Customer Experience and Analysis of Micro MarketsDocument22 pagesLeveraging Digital Channels For Enhancing Customer Experience and Analysis of Micro MarketsTashioNo ratings yet

- ProjectDocument40 pagesProjectSanjay WadhwaNo ratings yet

- SIPREPORT Ajay Boricha DivADocument60 pagesSIPREPORT Ajay Boricha DivABoricha AjayNo ratings yet

- Cash Management ICICI BankDocument63 pagesCash Management ICICI Bankkrushna vaidyaNo ratings yet

- Bank of BarodaDocument72 pagesBank of Barodamukeshahuja87100% (3)

- SBI's Point of Sale (POS) ManagementDocument64 pagesSBI's Point of Sale (POS) Managementakshparmar25100% (1)

- Ajay YadavDocument146 pagesAjay Yadav9415697349No ratings yet

- Mutual Fund Icici BANKDocument87 pagesMutual Fund Icici BANKVipul TandonNo ratings yet

- Profitability Analysis of Icici BankDocument50 pagesProfitability Analysis of Icici Banksomraj.presidencyNo ratings yet

- Compare Govt and Private BankDocument68 pagesCompare Govt and Private BankRuman KhanNo ratings yet

- Axis Bank ReportDocument55 pagesAxis Bank ReportAjay RohillaNo ratings yet

- 7 P's of Private Sector BankDocument21 pages7 P's of Private Sector BankMinal DalviNo ratings yet

- Summer Training ReportDocument65 pagesSummer Training ReportAmanpreet KaurNo ratings yet

- Bank of BarodaDocument75 pagesBank of BarodaVicky SinghNo ratings yet

- Marketing Strategies of Financial ProductsDocument20 pagesMarketing Strategies of Financial ProductsMOHAMMED KHAYYUMNo ratings yet

- Icici Bank and RajasthanDocument19 pagesIcici Bank and Rajasthanadarsh walavalkarNo ratings yet

- ProjectDocument61 pagesProjectbalaNo ratings yet

- Banking & Financial Stement at HDFC Bank LTDDocument102 pagesBanking & Financial Stement at HDFC Bank LTDdeepak GuptaNo ratings yet

- Analysis of Financial Statements of ICICI BankDocument77 pagesAnalysis of Financial Statements of ICICI BankMohit RohillaNo ratings yet

- Sip Project ReportDocument29 pagesSip Project ReportAAKIB HAMDANINo ratings yet

- PROJECT REPORT Central BankDocument13 pagesPROJECT REPORT Central BankShivangi SharmaNo ratings yet

- Shweta TybbiDocument72 pagesShweta Tybbishwetalad887% (30)

- Bank of IndiaDocument22 pagesBank of IndiaLeeladhar Nagar100% (1)

- MT 2 NPADocument30 pagesMT 2 NPAPri AgarwalNo ratings yet

- Summer Internship ReportDocument21 pagesSummer Internship ReportYashika GuptaNo ratings yet

- Industry NameDocument32 pagesIndustry NameBavadharani MNo ratings yet

- Roll No. 21Document76 pagesRoll No. 21gulatisrishti15No ratings yet

- Customer Satisfaction in The Indian Banking Industry: Submitted By:-Ameerah Fatima Syed BBA (2009 - 2012) A7006409058Document90 pagesCustomer Satisfaction in The Indian Banking Industry: Submitted By:-Ameerah Fatima Syed BBA (2009 - 2012) A7006409058Abdul Muneeb Khan50% (2)

- College Project Report ABHISHEKDocument121 pagesCollege Project Report ABHISHEKHarsh JhaNo ratings yet

- Digitalization Improves Banking ServicesDocument76 pagesDigitalization Improves Banking ServicesNikhil KapoorNo ratings yet

- Corporate CreditDocument69 pagesCorporate CreditAshish chanchlani100% (1)

- Customer Relationship Management On Retail Banking. On ING BANKDocument63 pagesCustomer Relationship Management On Retail Banking. On ING BANKNilesh SahuNo ratings yet

- Designation: Faculty Department: Bachelors of Management Studies K.H.M.W. College Submitted in Partial Fulfillment ofDocument53 pagesDesignation: Faculty Department: Bachelors of Management Studies K.H.M.W. College Submitted in Partial Fulfillment ofPooja SahaniNo ratings yet

- Finance Major ProjectDocument16 pagesFinance Major ProjectVarshini KrishnaNo ratings yet

- Amity Business School Amity University, Uttar PradeshDocument79 pagesAmity Business School Amity University, Uttar PradeshBohra RavishNo ratings yet

- Project Vijaya Bank FinalDocument62 pagesProject Vijaya Bank FinalNalina Gs G100% (1)

- ROHITH company profileDocument10 pagesROHITH company profileMechWindNaniNo ratings yet

- Summer Training Project: (Seth Jai Parkash Mukand Lal Institute of Engineering and Technology, Radaur)Document86 pagesSummer Training Project: (Seth Jai Parkash Mukand Lal Institute of Engineering and Technology, Radaur)Anonymous 7q2hVLAB2pNo ratings yet

- ICICI Bank Customers' Perceptions of Market InvestmentsDocument80 pagesICICI Bank Customers' Perceptions of Market InvestmentsDivyansh DhamijaNo ratings yet

- A Practical Approach to the Study of Indian Capital MarketsFrom EverandA Practical Approach to the Study of Indian Capital MarketsNo ratings yet

- SOFTWARE ARCHITECTURE - PDF RAJNEESH KORIDocument10 pagesSOFTWARE ARCHITECTURE - PDF RAJNEESH KORIvidhya associateNo ratings yet

- MitsDocument4 pagesMitsvidhya associateNo ratings yet

- Sample Report For Movie Recommender SystemDocument30 pagesSample Report For Movie Recommender Systemsanskritiiiii.2002No ratings yet

- Mits NIRDOSHDocument4 pagesMits NIRDOSHvidhya associateNo ratings yet

- Project 3Document16 pagesProject 3vidhya associateNo ratings yet

- Big Data RAJNEESH CCCDocument11 pagesBig Data RAJNEESH CCCvidhya associateNo ratings yet

- Digital Signature Cryptography (My2) Saurabh Kumar CCDocument12 pagesDigital Signature Cryptography (My2) Saurabh Kumar CCvidhya associateNo ratings yet

- Sample Report For Movie Recommender SystemDocument30 pagesSample Report For Movie Recommender Systemsanskritiiiii.2002No ratings yet

- SOFTWARE ARCHITECTURE - PDF RAJNEESH KORIDocument10 pagesSOFTWARE ARCHITECTURE - PDF RAJNEESH KORIvidhya associateNo ratings yet

- Extract File 20221130 193426Document1 pageExtract File 20221130 193426vidhya associateNo ratings yet

- Big Data RAJNEESH CCCDocument11 pagesBig Data RAJNEESH CCCvidhya associateNo ratings yet

- Digital Signature Cryptography (My2) Abhishek Praja CDocument12 pagesDigital Signature Cryptography (My2) Abhishek Praja Cvidhya associateNo ratings yet

- Digital Signature Cryptography (My2) Abhishek Praja CDocument12 pagesDigital Signature Cryptography (My2) Abhishek Praja Cvidhya associateNo ratings yet

- Dikshant Major Project2023Document1 pageDikshant Major Project2023vidhya associateNo ratings yet

- Project ReportDocument25 pagesProject Reportvidhya associateNo ratings yet

- 1st Abstract RA Bill Slab RateDocument1 page1st Abstract RA Bill Slab Ratevidhya associateNo ratings yet

- MD NausadDocument5 pagesMD Nausadvidhya associateNo ratings yet

- MD Gule RezaDocument5 pagesMD Gule Rezavidhya associateNo ratings yet

- Mobile Computing Guide: Parts, Issues & AdvantagesTITLEDocument231 pagesMobile Computing Guide: Parts, Issues & AdvantagesTITLEvidhya associateNo ratings yet

- RahulDocument8 pagesRahulvidhya associateNo ratings yet

- MD Kalam FinalDocument5 pagesMD Kalam Finalvidhya associateNo ratings yet

- Thyristor Controlled Power For Induction Motor 1 FrontDocument8 pagesThyristor Controlled Power For Induction Motor 1 Frontvidhya associateNo ratings yet

- Extract File 20221130 193426Document1 pageExtract File 20221130 193426vidhya associateNo ratings yet

- Babu HassanDocument5 pagesBabu Hassanvidhya associateNo ratings yet

- Skin Cancer Disease: A 40-CharacterDocument5 pagesSkin Cancer Disease: A 40-Charactervidhya associateNo ratings yet

- Madhyanchal: Bachelor of PharmacyDocument5 pagesMadhyanchal: Bachelor of Pharmacyvidhya associateNo ratings yet

- 3 ExpDocument4 pages3 Expvidhya associateNo ratings yet

- MD Kalam FinalDocument5 pagesMD Kalam Finalvidhya associateNo ratings yet

- 3 ExpDocument4 pages3 Expvidhya associateNo ratings yet

- 8 THDocument5 pages8 THvidhya associateNo ratings yet

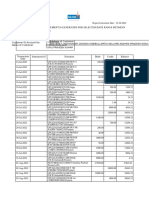

- The Mpassbook Statement Is Generated For Selected Date Range Between 14-07-2022 TO 12-10-2022. Customer DetailsDocument5 pagesThe Mpassbook Statement Is Generated For Selected Date Range Between 14-07-2022 TO 12-10-2022. Customer DetailsPraveen kumarNo ratings yet

- Object Oriented Analysis and Design of an ATM System Using UMLDocument5 pagesObject Oriented Analysis and Design of an ATM System Using UMLHarikrishna NethaNo ratings yet

- SOYDDocument3 pagesSOYDNathan Dungog100% (2)

- IFIC Bank Stress TestingDocument37 pagesIFIC Bank Stress TestingTanvir HasanNo ratings yet

- Financial Accounting International Student 7th Edition Kimmel Solutions ManualDocument25 pagesFinancial Accounting International Student 7th Edition Kimmel Solutions ManualDannyJohnsonobtk100% (58)

- 010-Reducing Agent SwitchingDocument91 pages010-Reducing Agent Switchingasri nurulNo ratings yet

- FIN104 Tutorial Questions - Week 2 Cost of Capital and Opportunity CostDocument4 pagesFIN104 Tutorial Questions - Week 2 Cost of Capital and Opportunity CostZijingNo ratings yet

- 1 SPL 19-20Document86 pages1 SPL 19-20westway NOIDANo ratings yet

- Great Cash Gain Ps en FW JoDocument53 pagesGreat Cash Gain Ps en FW JoGobinath SubramaniamNo ratings yet

- United Commercial Bank's Agent Banking ModelDocument21 pagesUnited Commercial Bank's Agent Banking Modelকাজী জিয়া উদ্দিনNo ratings yet

- Investment Appraisal Report (Individual Report)Document10 pagesInvestment Appraisal Report (Individual Report)Eric AwinoNo ratings yet

- Credit Creation: Primary Deposits: Primary Deposits Arise or Formed When Cash or Cheque Is Deposited byDocument7 pagesCredit Creation: Primary Deposits: Primary Deposits Arise or Formed When Cash or Cheque Is Deposited byMaisha AnzumNo ratings yet

- Prepration of Financial StatementsDocument35 pagesPrepration of Financial StatementsMercy GamingNo ratings yet

- Sample PfrsDocument7 pagesSample PfrsClint AbenojaNo ratings yet

- Managerial Finance 8e 2017-1Document711 pagesManagerial Finance 8e 2017-1MunyNo ratings yet

- AXIS BANK Project Word FileDocument28 pagesAXIS BANK Project Word Fileअक्षय गोयलNo ratings yet

- Performance Appraisal in BanksDocument54 pagesPerformance Appraisal in BanksParag More100% (1)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument28 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDhanraj KhatriNo ratings yet

- Focus On Personal Finance 5Th Edition Kapoor Solutions Manual Full Chapter PDFDocument45 pagesFocus On Personal Finance 5Th Edition Kapoor Solutions Manual Full Chapter PDFmiguelstone5tt0f100% (11)

- Mutual Fund Investment From An Individual's PerspectiveDocument89 pagesMutual Fund Investment From An Individual's PerspectiveSAJIDA SHAIKHNo ratings yet

- India's Top 10 Financial ScamDocument17 pagesIndia's Top 10 Financial Scamjaatmahi100% (1)

- John Doe UCC 1Document10 pagesJohn Doe UCC 1Bunny Fontaine100% (2)

- Introduction to Cyprus Investment Funds and Asset ManagementDocument31 pagesIntroduction to Cyprus Investment Funds and Asset ManagementRusMartinNo ratings yet

- TS IT FY 19-20 Full Version1.1 Gives You How To Calculate TaxDocument20 pagesTS IT FY 19-20 Full Version1.1 Gives You How To Calculate TaxHappy HourNo ratings yet

- Suvigya: Details Furnished by You WereDocument1 pageSuvigya: Details Furnished by You WereMKMK JilaniNo ratings yet

- Manage your LANDBANK accounts online with iAccessDocument2 pagesManage your LANDBANK accounts online with iAccessMay Elaine BelgadoNo ratings yet

- Which Companies Are Required To Issue Prospectus?: - Requirements of A ProspectusDocument9 pagesWhich Companies Are Required To Issue Prospectus?: - Requirements of A ProspectusDr.Shaifali GargNo ratings yet

- Banking ProjectDocument22 pagesBanking ProjectAkhileshwar RaiNo ratings yet

- Bankera WhitepaperDocument29 pagesBankera Whitepaperkenfouet ouamba gabinNo ratings yet

- Novena Shirts LimitedDocument1 pageNovena Shirts LimitedAndrea SalazarNo ratings yet