You might also like

- The Mutual Funds Book: How to Invest in Mutual Funds & Earn High Rates of Returns SafelyFrom EverandThe Mutual Funds Book: How to Invest in Mutual Funds & Earn High Rates of Returns SafelyRating: 5 out of 5 stars5/5 (1)

- Understanding Islamic Bonds (SukukDocument29 pagesUnderstanding Islamic Bonds (Sukukwokyoh91No ratings yet

- Sukuk PresentationDocument79 pagesSukuk PresentationJameel AhmadNo ratings yet

- Islamic Sukuk Concepts & ApplicationsDocument79 pagesIslamic Sukuk Concepts & ApplicationsAsad UllahNo ratings yet

- ReportDocument4 pagesReportTonmoy DelwarNo ratings yet

- SukukDocument9 pagesSukukanamejenicoleNo ratings yet

- Chapter 2 SukukDocument8 pagesChapter 2 SukukFahmi IzzuddinNo ratings yet

- SUKUK Not FinishedDocument14 pagesSUKUK Not FinishedAbdiKarem JamalNo ratings yet

- The Effectiveness of Sukuk in Islamic Finance MarketDocument7 pagesThe Effectiveness of Sukuk in Islamic Finance MarketKhairul AnnuwarNo ratings yet

- Islamic Banking and Finance Unit 10: SukukDocument8 pagesIslamic Banking and Finance Unit 10: SukukAmir Abdalla IbrahimNo ratings yet

- Arabic Arabic Certificates Islamic Bonds Islam Islamic Law: Sukuk (Document4 pagesArabic Arabic Certificates Islamic Bonds Islam Islamic Law: Sukuk (Zaid AlaviNo ratings yet

- Islamic Capital Markets: The Role of Sukuk: Executive SummaryDocument4 pagesIslamic Capital Markets: The Role of Sukuk: Executive SummaryiisjafferNo ratings yet

- Sana Islamic LawDocument7 pagesSana Islamic LawArslan MalikNo ratings yet

- Laila 1Document22 pagesLaila 1Arbab Usman KhanNo ratings yet

- Islamic Bonds: Learning ObjectivesDocument20 pagesIslamic Bonds: Learning ObjectivesAbdelnasir HaiderNo ratings yet

- Chapter No. 9 Investment in Sukuk: Mashad Raza Muhammad Nauman H.M Mazhar ZeeshanDocument32 pagesChapter No. 9 Investment in Sukuk: Mashad Raza Muhammad Nauman H.M Mazhar ZeeshanMunawar AbbasNo ratings yet

- Islamic FinanceDocument9 pagesIslamic FinanceMohsin AijazNo ratings yet

- Sukuk Structures Profiles and RisksDocument18 pagesSukuk Structures Profiles and Risksardelektrik 2021No ratings yet

- Overview of Islamic Banking Services and PrinciplesDocument9 pagesOverview of Islamic Banking Services and PrinciplesNabeela ShahNo ratings yet

- Essay Week 5 On SukukDocument2 pagesEssay Week 5 On SukukRuddy Von OhlenNo ratings yet

- TO Islamic Banking: Naina Jagesha Roll No - 22 Prof-In-Charge-Rashmi MamDocument12 pagesTO Islamic Banking: Naina Jagesha Roll No - 22 Prof-In-Charge-Rashmi Mamnaina_jageshaNo ratings yet

- Securitization in Islamic BankingDocument6 pagesSecuritization in Islamic BankingFaisal RehmanNo ratings yet

- Sukuk Islamic Banking 2025Document9 pagesSukuk Islamic Banking 2025Juzer JiruNo ratings yet

- Chapter - 8Document17 pagesChapter - 8Maruf AhmedNo ratings yet

- SUKUKDocument18 pagesSUKUKNur ShahiraNo ratings yet

- Pursuit of Islamic FinanceDocument3 pagesPursuit of Islamic FinanceShamim IqbalNo ratings yet

- CORPORATE BANKING ACTIVITIES CHAPTER THREEDocument26 pagesCORPORATE BANKING ACTIVITIES CHAPTER THREENini MohamedNo ratings yet

- Forms of Islamic BankingDocument55 pagesForms of Islamic BankingMuhammad Talha KhanNo ratings yet

- Sources of Finance - Islamic Finance: (A) MurabahaDocument2 pagesSources of Finance - Islamic Finance: (A) MurabahaMilanNo ratings yet

- Islamic Private Debt SecuritiesDocument6 pagesIslamic Private Debt SecuritiesMuhammad Shahrul NazwinNo ratings yet

- SukukDocument15 pagesSukuk2345008100% (1)

- E7 Introduction To Islamic FinanceDocument5 pagesE7 Introduction To Islamic FinanceTENGKU ANIS TENGKU YUSMANo ratings yet

- An Introduction To Islamic Finance and The Malaysian ExperienceDocument10 pagesAn Introduction To Islamic Finance and The Malaysian Experiencecharlie simoNo ratings yet

- An Introduction To Islamic FinanceDocument14 pagesAn Introduction To Islamic FinanceThargistNo ratings yet

- Islamic Capital Market Development and InstrumentsDocument32 pagesIslamic Capital Market Development and InstrumentsSharmila DeviNo ratings yet

- IBF BY DaniDocument14 pagesIBF BY DaniDaniyal AwanNo ratings yet

- Special Focus May2012 PDFDocument6 pagesSpecial Focus May2012 PDFMAKK Business SolutionsNo ratings yet

- Securitisation An Overview: H HE EM ME EDocument8 pagesSecuritisation An Overview: H HE EM ME Ejlo42No ratings yet

- The Potential and Risks of Sukuk According to Shariah LawDocument30 pagesThe Potential and Risks of Sukuk According to Shariah Lawbadrul_ibrahim100% (1)

- Islamic Finance NotesDocument6 pagesIslamic Finance NotesHosea KanyangaNo ratings yet

- FuzzyDocument16 pagesFuzzyAhmad FadzwanNo ratings yet

- Basic Concepts of Islamic FinanceDocument5 pagesBasic Concepts of Islamic FinanceSaifullahMakenNo ratings yet

- Types of SukukDocument6 pagesTypes of Sukuknawel mezighecheNo ratings yet

- Working With Islamic FinanceDocument3 pagesWorking With Islamic FinanceNaffay HussainNo ratings yet

- Islamic Bonds Issues: The Malaysian Experience: Kolej Universiti Islam MalaysiaDocument9 pagesIslamic Bonds Issues: The Malaysian Experience: Kolej Universiti Islam MalaysiaaqeelzaidiNo ratings yet

- Islamic SukukDocument85 pagesIslamic SukukwaqarkhaliqNo ratings yet

- What is Islamic bankingDocument8 pagesWhat is Islamic bankingFahad Bhuiyan100% (1)

- My Lec Securitization 2Document31 pagesMy Lec Securitization 2nouman nawazNo ratings yet

- Assignment On Islamic BankingDocument8 pagesAssignment On Islamic BankingRimsha LatifNo ratings yet

- The Structure and Application of Asset Based and Asset Backed SukukDocument8 pagesThe Structure and Application of Asset Based and Asset Backed SukukSyazwan IqbalNo ratings yet

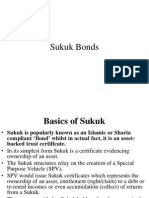

- Basics of Sukuk BondsDocument11 pagesBasics of Sukuk BondsFawad Ahmed ArainNo ratings yet

- Sukuk Features, TypesCharacteristisDocument2 pagesSukuk Features, TypesCharacteristisMohammed SaifulNo ratings yet

- Ijarah Sukuk: Ahmed Shahir Usmani Muhammad Rizwan Abdul Rahim Ali Iftekhar Muhammad Junaid KhanDocument8 pagesIjarah Sukuk: Ahmed Shahir Usmani Muhammad Rizwan Abdul Rahim Ali Iftekhar Muhammad Junaid KhanAhmed Shahir UsmaniNo ratings yet

- Islamic FinanceDocument5 pagesIslamic FinanceAbdul Wahid KhanNo ratings yet

- Islamic Banking System - EditedDocument5 pagesIslamic Banking System - EditedLubaba RazaNo ratings yet

- Shariah-Compliant Investment OpportunitiesDocument12 pagesShariah-Compliant Investment OpportunitiesIbn Bashir Ar-RaisiNo ratings yet

- Islamic Banking Myths and FactsDocument12 pagesIslamic Banking Myths and Factsthexplorer008No ratings yet

- Mutual Funds - The Mutual Fund Retirement Plan For Long - Term Wealth BuildingFrom EverandMutual Funds - The Mutual Fund Retirement Plan For Long - Term Wealth BuildingNo ratings yet

- Dawam Ul AishDocument110 pagesDawam Ul AishAbbasi WritesNo ratings yet

- Doctor Zeshan SBDocument7 pagesDoctor Zeshan SBAbbasi WritesNo ratings yet

- Fourth Lecture On Orientalism Final 07042022 033206pmDocument34 pagesFourth Lecture On Orientalism Final 07042022 033206pmAbbasi WritesNo ratings yet

- In The Name of AllahDocument9 pagesIn The Name of AllahAbbasi WritesNo ratings yet

- Concept of Society & Islamic PerspectiveDocument14 pagesConcept of Society & Islamic PerspectiveAbbasi WritesNo ratings yet

- A Orientalist A J ArberryDocument8 pagesA Orientalist A J ArberryAbbasi WritesNo ratings yet

- Madaris e DinyaDocument89 pagesMadaris e DinyaAbbasi WritesNo ratings yet

- Final Marketing MattelDocument21 pagesFinal Marketing MattelMd Atiullah Khan100% (1)

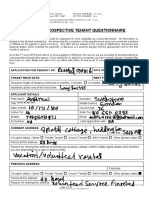

- PROSPECTIVE TENANT QUESTIONNAIRE (Updated 31.05.19 BHJ and MJBS) - 1Document10 pagesPROSPECTIVE TENANT QUESTIONNAIRE (Updated 31.05.19 BHJ and MJBS) - 1Duke Jno100% (1)

- ApplyTerms PDFDocument10 pagesApplyTerms PDFKaren FlanaganNo ratings yet

- PortCalls March 30 2020Document12 pagesPortCalls March 30 2020PortCallsNo ratings yet

- 14th WIEF Sponsorship BenefitsDocument2 pages14th WIEF Sponsorship BenefitsLatifiNo ratings yet

- SAP FICO Training Videos - Materials Folder Screenshots PDFDocument8 pagesSAP FICO Training Videos - Materials Folder Screenshots PDFSajanAndyNo ratings yet

- System Design SpecificationDocument8 pagesSystem Design Specificationapi-278499472No ratings yet

- Globalization of Markets SummaryDocument3 pagesGlobalization of Markets SummaryShriyashi Khatri100% (1)

- Union Bank Statement FreshDocument7 pagesUnion Bank Statement Freshbindu mathaiNo ratings yet

- Krishna Constructions: Work Order ToDocument2 pagesKrishna Constructions: Work Order ToNasim AktarNo ratings yet

- Sensor Tower Q2 2021 Data DigestDocument71 pagesSensor Tower Q2 2021 Data Digestchoong Poh100% (1)

- Statement Period: Primary Savings (ID 00)Document5 pagesStatement Period: Primary Savings (ID 00)Mark Williams100% (1)

- Promoting Malaysia's MICE IndustryDocument8 pagesPromoting Malaysia's MICE IndustrySuboh BeladingNo ratings yet

- Grade 11 Module 3Document122 pagesGrade 11 Module 3mhaiibreakerNo ratings yet

- Research Rma Format Guide 1Document110 pagesResearch Rma Format Guide 1Nicole Anne PacoNo ratings yet

- MBA 231 Marketing Management PDFDocument16 pagesMBA 231 Marketing Management PDFSNEHA SIVAKUMAR 1730152No ratings yet

- JESUS TABURA ResumeDocument5 pagesJESUS TABURA Resumekiran2710No ratings yet

- Java SuccessDocument3 pagesJava SuccessAnil Kumar BattulaNo ratings yet

- Tapa FSR 2020-1Document30 pagesTapa FSR 2020-1Ale Wenger100% (1)

- Mindanao Mission Academy Midterm ExaminationDocument2 pagesMindanao Mission Academy Midterm ExaminationHLeigh Nietes-GabutanNo ratings yet

- CT SS For Student Apr2019Document5 pagesCT SS For Student Apr2019Nabila RosmizaNo ratings yet

- Advance Chapter 1Document16 pagesAdvance Chapter 1abel habtamuNo ratings yet

- Prototype Courier ChargesDocument16 pagesPrototype Courier ChargesDeepak BhanjiNo ratings yet

- Successful Career DevelopmentDocument7 pagesSuccessful Career DevelopmentAynurNo ratings yet

- Identity Theft Letter For COVID-19Document2 pagesIdentity Theft Letter For COVID-19Wgme ProducersNo ratings yet

- Varalakshmi Agencies tax invoice for LPG cylinder refill orderDocument1 pageVaralakshmi Agencies tax invoice for LPG cylinder refill orderkhaderullaNo ratings yet

- Performance For Today and Tomorrow!: - Innovative Casthouse Solutions That PerformDocument2 pagesPerformance For Today and Tomorrow!: - Innovative Casthouse Solutions That PerformDaniel StuparekNo ratings yet

- Tangazo La Kazi CPBDocument13 pagesTangazo La Kazi CPBSaid AbdulkhNo ratings yet

- 45-Article Text-345-1-10-20211221Document7 pages45-Article Text-345-1-10-20211221buset lamakNo ratings yet

- Technological Advancement of Automotive IndustryDocument6 pagesTechnological Advancement of Automotive IndustryaspectNo ratings yet