You might also like

- Financial Statements and Ratio Anlysis UpdatedDocument5 pagesFinancial Statements and Ratio Anlysis Updatedarbazhabibkk4No ratings yet

- Partnership LiquidationDocument20 pagesPartnership LiquidationIvhy Cruz Estrella0% (1)

- Financial Analysis and Reporting Midterm Quiz 1Document8 pagesFinancial Analysis and Reporting Midterm Quiz 1Santi SeguinNo ratings yet

- 60 BIWS Bank Projections Reference PDFDocument5 pages60 BIWS Bank Projections Reference PDFAnish ShahNo ratings yet

- REG-04 108d871Document54 pagesREG-04 108d871Vidyadhar TRNo ratings yet

- Strides Arcolab Limited - PCBDocument15 pagesStrides Arcolab Limited - PCBNAMI100% (1)

- Interactive CH 23 Measuring A Nation - S Income 9eDocument40 pagesInteractive CH 23 Measuring A Nation - S Income 9eNguyen Vu Thuc Uyen (K17 QN)No ratings yet

- Developing Your Financial Statements and PlansDocument40 pagesDeveloping Your Financial Statements and PlansEdmund AngNo ratings yet

- Accounts Debit Credit: Normal Balance Normal BalanceDocument4 pagesAccounts Debit Credit: Normal Balance Normal BalanceVG R1NG3RNo ratings yet

- WorkbookDocument72 pagesWorkbookMbalenhle NdlovuNo ratings yet

- Debit and Credit RulesDocument1 pageDebit and Credit RulesYonas D. EbrenNo ratings yet

- Corporate Restructuring: Unit 3Document43 pagesCorporate Restructuring: Unit 3Maithreye HoleyachiNo ratings yet

- 2023 Accounting Learners Notes Session 1-8Document215 pages2023 Accounting Learners Notes Session 1-8Nomfundo ShabalalaNo ratings yet

- CH 12Document58 pagesCH 12maschip313No ratings yet

- Chapter 16 - Working Capital Management 1Document36 pagesChapter 16 - Working Capital Management 1Phán Tiêu TiềnNo ratings yet

- Pertemuan 2 - Financial Reporting MechanicDocument32 pagesPertemuan 2 - Financial Reporting MechanicJhoni LimNo ratings yet

- Section 3 Modified - Ch5+Ch6Document8 pagesSection 3 Modified - Ch5+Ch6Dina AlfawalNo ratings yet

- Lecture - CH 15Document45 pagesLecture - CH 15burucsgNo ratings yet

- Williams FinMan 19e Chap005 PPTDocument64 pagesWilliams FinMan 19e Chap005 PPTPedro ValdiviaNo ratings yet

- The Accounting Cycle: Reporting Financial ResultsDocument64 pagesThe Accounting Cycle: Reporting Financial ResultsLama KaedbeyNo ratings yet

- Finance Ratio AnalysisDocument3 pagesFinance Ratio AnalysisPRIYA SINGHNo ratings yet

- Lesson 9Document4 pagesLesson 9malik123ggNo ratings yet

- 01-Evaluating Bank PerformanceDocument66 pages01-Evaluating Bank PerformanceAhmed NaguibNo ratings yet

- BUSI3111 Ch2Document51 pagesBUSI3111 Ch2Hakkı Anıl AksoyNo ratings yet

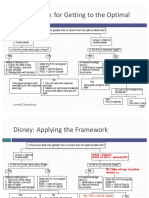

- A Framework For Getting To The Optimal: Aswath DamodaranDocument19 pagesA Framework For Getting To The Optimal: Aswath DamodaransheinaNo ratings yet

- Vadeo Inc Exercise: Strictly Confidential AssetsDocument3 pagesVadeo Inc Exercise: Strictly Confidential AssetsNeha SathayeNo ratings yet

- Dokumen - Tips Ch03test Bank Jeter Chapter 3Document18 pagesDokumen - Tips Ch03test Bank Jeter Chapter 3Evelyn Purnama SariNo ratings yet

- SMB18 e CH 22Document40 pagesSMB18 e CH 22Bantilan ElejunNo ratings yet

- TRANSACTIONSDocument7 pagesTRANSACTIONSAlison HankinsNo ratings yet

- The Statement of Cash FlowsDocument45 pagesThe Statement of Cash FlowsJavix ThomasNo ratings yet

- RWJ Corp 12e PPT Ch02Document38 pagesRWJ Corp 12e PPT Ch02Shashank SauravNo ratings yet

- Cornett Finance 5e Chapter 02Document38 pagesCornett Finance 5e Chapter 02Lu LiNo ratings yet

- 86d77631 5003 Fs - Balance Sheet PDFDocument7 pages86d77631 5003 Fs - Balance Sheet PDFHeetNo ratings yet

- Ross 12e PPT Ch02Document6 pagesRoss 12e PPT Ch02Giang HoàngNo ratings yet

- Titman PPT CH10Document57 pagesTitman PPT CH10Sarah MoonNo ratings yet

- Debit and Credit: Fundamentals of Accountancy, Business and Management 1Document10 pagesDebit and Credit: Fundamentals of Accountancy, Business and Management 1triicciaa faith100% (1)

- Intercompany Profit Transactions - BondsDocument50 pagesIntercompany Profit Transactions - BondsJeremy JansenNo ratings yet

- Color-Coding:: Step 1 - Enter Info About Your Company in Yellow Shaded Boxes BelowDocument25 pagesColor-Coding:: Step 1 - Enter Info About Your Company in Yellow Shaded Boxes BelowShantanu UgaleNo ratings yet

- Success Center Accounting Tips and Practice Sheet Building Blocks To A General Journal Entry and T-AccountDocument2 pagesSuccess Center Accounting Tips and Practice Sheet Building Blocks To A General Journal Entry and T-AccountThe PsychoNo ratings yet

- Building Blocks To A General Journal Entry and T AccountDocument2 pagesBuilding Blocks To A General Journal Entry and T AccountChris AdoraNo ratings yet

- RWJ Corp 12e PPT Ch02Document38 pagesRWJ Corp 12e PPT Ch02tuongvi nguyenNo ratings yet

- Chapter 5 (3) - Bad Debts, Allowance For Doubtful Debts and Discount AllowableDocument43 pagesChapter 5 (3) - Bad Debts, Allowance For Doubtful Debts and Discount AllowableIrsamNo ratings yet

- Mergers Acquisitions Fact Sheet (Digital)Document2 pagesMergers Acquisitions Fact Sheet (Digital)Emperor OverwatchNo ratings yet

- FM02 Ch15 ShowDocument102 pagesFM02 Ch15 Showc108161109No ratings yet

- Chapter 2-1: Using T Accounts / Analyzing The Accounting EquationDocument23 pagesChapter 2-1: Using T Accounts / Analyzing The Accounting EquationGarrett JohnsonNo ratings yet

- AC530 Accounting Theory Module 6 AssignmentDocument3 pagesAC530 Accounting Theory Module 6 AssignmentMCNo ratings yet

- Session 2Document59 pagesSession 2Bảo Trí Nguyễn PhướcNo ratings yet

- Ratio Analysis: The Balance Sheet For FinancialDocument10 pagesRatio Analysis: The Balance Sheet For FinancialWahidul Islam 222-14-522No ratings yet

- Ross 12e PPT Ch02Document25 pagesRoss 12e PPT Ch02Trúc Quỳnh NguyễnNo ratings yet

- Comparative Study of Financial Statement Ratios Between Dell and EpsonDocument7 pagesComparative Study of Financial Statement Ratios Between Dell and EpsonMacharia NgunjiriNo ratings yet

- Application Test: Estimating A Bottom-Up Beta: Aswath DamodaranDocument24 pagesApplication Test: Estimating A Bottom-Up Beta: Aswath DamodaranIvan GomezNo ratings yet

- Cap StrucDocument58 pagesCap StrucTanyaNo ratings yet

- Chapter 2Document49 pagesChapter 2haiderasim1212No ratings yet

- Capital Structure TheoriesDocument38 pagesCapital Structure TheoriesShweta GoelNo ratings yet

- FANAS 7e PPT Chap16Document30 pagesFANAS 7e PPT Chap16hippop kNo ratings yet

- Finacc CH 4Document61 pagesFinacc CH 4Michael TorresNo ratings yet

- Cash Flows: Statement ofDocument75 pagesCash Flows: Statement ofNurai ChutbasovaNo ratings yet

- P1Document1 pageP1MahirAhmedNo ratings yet

- Price 16e CH002 PPTDocument42 pagesPrice 16e CH002 PPTSamuelle Michah CaychingcoNo ratings yet

- Lecture 3 - StocksDocument33 pagesLecture 3 - StocksFredrik BjørniNo ratings yet

- International Management SlidesDocument195 pagesInternational Management SlidesTarek AliNo ratings yet

- Bba Gee S8Document20 pagesBba Gee S8Tarek AliNo ratings yet

- Global Economic Environment: IE UniversityDocument9 pagesGlobal Economic Environment: IE UniversityTarek AliNo ratings yet

- LESSON #7 - Managerial Economics: Wrap Up: Unit: LanguageDocument2 pagesLESSON #7 - Managerial Economics: Wrap Up: Unit: LanguageTarek AliNo ratings yet

- Exam MacroDocument7 pagesExam MacroTarek AliNo ratings yet

- LankaBangla Finance Limited: A Study On Leasing (NBFI) SectorDocument23 pagesLankaBangla Finance Limited: A Study On Leasing (NBFI) SectorRajesh PaulNo ratings yet

- p8-1 Tugas GSLCDocument3 pagesp8-1 Tugas GSLCelaine aureliaNo ratings yet

- SER Plagiarism ReportDocument6 pagesSER Plagiarism ReportmayankNo ratings yet

- 6941 Ais - Database.model - file.LampiranLain TUGAS PERTEMUAN 12Document4 pages6941 Ais - Database.model - file.LampiranLain TUGAS PERTEMUAN 12Amirah rasyidahNo ratings yet

- Apple Inc. (AAPL) Final PresentationDocument16 pagesApple Inc. (AAPL) Final PresentationShukran AlakbarovNo ratings yet

- True - False QuestionsDocument3 pagesTrue - False QuestionsNguyen Thanh Thao (K16 HCM)No ratings yet

- FIN 302 Notes 1Document55 pagesFIN 302 Notes 1Tekego TlakaleNo ratings yet

- Midterm Answer KeyDocument10 pagesMidterm Answer KeyRebecca ParisiNo ratings yet

- 1st Periodical Exam in Fundamentals of Accountancy and Business Management 1 ReviewerDocument9 pages1st Periodical Exam in Fundamentals of Accountancy and Business Management 1 ReviewerJaderick BalboaNo ratings yet

- PPT For CH 1 2 3Document135 pagesPPT For CH 1 2 3Kalkidan G/wahidNo ratings yet

- 204-Article Text-1386-1-10-20191025Document10 pages204-Article Text-1386-1-10-20191025IsnaynisabilaNo ratings yet

- Sources and Application of Funding OverallDocument4 pagesSources and Application of Funding OverallApril CaringalNo ratings yet

- Financial Analysis - Maruti Udyog LimitedDocument32 pagesFinancial Analysis - Maruti Udyog LimitedbhagypowaleNo ratings yet

- ASSET LIABILITIES Mnagament in BanksDocument25 pagesASSET LIABILITIES Mnagament in Bankspriyank shah100% (6)

- Albanese Company, Spa Worksheet (Partial) For The Month Ended April 30, 2017Document17 pagesAlbanese Company, Spa Worksheet (Partial) For The Month Ended April 30, 2017Mayang RijanieNo ratings yet

- Financial Risk and Relationship Between Cost of CapitalDocument41 pagesFinancial Risk and Relationship Between Cost of Capitalgameplay84No ratings yet

- Azim GroupDocument48 pagesAzim GroupABC Computer R.SNo ratings yet

- 142 0105Document27 pages142 0105api-27548664No ratings yet

- Advanced Financial ReportingDocument6 pagesAdvanced Financial ReportingRobin G'koolNo ratings yet

- The EVCA Yearbook 2011Document7 pagesThe EVCA Yearbook 2011Justyna GudaszewskaNo ratings yet

- Exam Chap 13Document60 pagesExam Chap 13asimNo ratings yet

- Group 1: Topic 1 Financial PlanningDocument55 pagesGroup 1: Topic 1 Financial PlanningjsemlpzNo ratings yet

- Module 1 - Intro and Conceptual Framework S2 2023Document42 pagesModule 1 - Intro and Conceptual Framework S2 2023Mark S.PNo ratings yet

- FMR - Mar 2010Document8 pagesFMR - Mar 2010Salman ArshadNo ratings yet

- GIM - Revised Mid Term Paper - Solution and Marking PatternDocument4 pagesGIM - Revised Mid Term Paper - Solution and Marking PatternNamitha ShajanNo ratings yet

- 5 AmalgamationDocument52 pages5 AmalgamationsmartshivenduNo ratings yet

- Sibugay Technical Institute: College of Education Module-1, Week 1-8Document51 pagesSibugay Technical Institute: College of Education Module-1, Week 1-8Mark Gary Fuentes OrdialezNo ratings yet

- Case 6 1 Browning Manufacturing Company 2 PDF FreeDocument7 pagesCase 6 1 Browning Manufacturing Company 2 PDF FreeLia AmeliaNo ratings yet