You might also like

- Accenture Emerging Market EntryDocument16 pagesAccenture Emerging Market EntryPrateek JainNo ratings yet

- Chapter 11Document9 pagesChapter 11oranghebat0% (1)

- CHP 8 AnsDocument9 pagesCHP 8 Ans6vnh5z7fnjNo ratings yet

- Supply Chain Management and The Catalytic Role of The Management AccountantDocument7 pagesSupply Chain Management and The Catalytic Role of The Management Accountantvb_krishnaNo ratings yet

- Maneesh KR TarunDocument9 pagesManeesh KR Tarungoel_anshipu87No ratings yet

- Us Cons Thriving in Uncertainty MarginDocument6 pagesUs Cons Thriving in Uncertainty MarginKikiNo ratings yet

- User GuideDocument28 pagesUser GuidePuneet SinghNo ratings yet

- Module 8 AssignmentDocument5 pagesModule 8 AssignmentMuafa BasheerNo ratings yet

- Global Marketing: How Do Standardise and Customise The Products Globally?Document7 pagesGlobal Marketing: How Do Standardise and Customise The Products Globally?RajaRajeswari.LNo ratings yet

- Article 10 - Headquarters or Regions Who Leads Growth in EMDocument4 pagesArticle 10 - Headquarters or Regions Who Leads Growth in EMRNo ratings yet

- MKT 571 Final Exam Latest Question AnswersDocument9 pagesMKT 571 Final Exam Latest Question AnswersLiza DanialNo ratings yet

- Measuring The Fashion World Full ReportDocument32 pagesMeasuring The Fashion World Full ReportAmit JainNo ratings yet

- Positioning Sustainable Brands in The International Market Through E-CommerceDocument20 pagesPositioning Sustainable Brands in The International Market Through E-CommerceTrường NguyễnNo ratings yet

- Business Analysis and Valuation - Strategic AnalysisDocument40 pagesBusiness Analysis and Valuation - Strategic AnalysiscapassoaNo ratings yet

- Discussion QuestionsDocument5 pagesDiscussion Questionsbokikg87No ratings yet

- NikonDocument58 pagesNikonPriyanka SinghNo ratings yet

- Manager's Guide To Competitive Marketing Strategies .13Document15 pagesManager's Guide To Competitive Marketing Strategies .13Ameya KambleNo ratings yet

- MKT 571 Final Exam Latest UOP Final Exam Questions With AnswersDocument9 pagesMKT 571 Final Exam Latest UOP Final Exam Questions With AnswersLiza DanialNo ratings yet

- Future of B2B Sales The Big ReframeDocument37 pagesFuture of B2B Sales The Big ReframeDental Wiz50% (2)

- 7 Steps To Transforming A Marketing PlanDocument12 pages7 Steps To Transforming A Marketing Planart2sinNo ratings yet

- Clariant Corporation Case: Submitted By: Nisha ThakkarDocument16 pagesClariant Corporation Case: Submitted By: Nisha ThakkarAshwin GanatraNo ratings yet

- Capsim Global User GuideDocument28 pagesCapsim Global User GuideKevin DebrownNo ratings yet

- International Expansion: A Roadmap To Successful Growth For EntrepreneursDocument10 pagesInternational Expansion: A Roadmap To Successful Growth For EntrepreneursVaishali KakadeNo ratings yet

- Marketing Management ReportDocument6 pagesMarketing Management ReportCriselda TeanoNo ratings yet

- Global Marketing StrategyDocument3 pagesGlobal Marketing StrategyDonna LouisaNo ratings yet

- International Business Environment Assignment 1Document5 pagesInternational Business Environment Assignment 1mechidream0% (2)

- SapientNitro Global Marketing Series: Part Three - Five Ways Agencies Are Grappling With Global MarketingDocument10 pagesSapientNitro Global Marketing Series: Part Three - Five Ways Agencies Are Grappling With Global MarketingSapientNitroNo ratings yet

- Kumar Et Al. (2019)Document17 pagesKumar Et Al. (2019)Lance HuendersNo ratings yet

- Industrial Marketing Final SemDocument21 pagesIndustrial Marketing Final SemRaj KumarNo ratings yet

- The Mars Agency - Retail Media Report Card EUROPE - March 2024Document40 pagesThe Mars Agency - Retail Media Report Card EUROPE - March 2024ameliaNo ratings yet

- 5SMM MarketanalysisDocument23 pages5SMM MarketanalysisSaron GebreNo ratings yet

- McKinsey NOW NEW NEXT How Growth Champions Create New ValueDocument12 pagesMcKinsey NOW NEW NEXT How Growth Champions Create New ValueHansNo ratings yet

- Accelerating AI-driven Marketing MaturityDocument13 pagesAccelerating AI-driven Marketing MaturityJimmy ChoiNo ratings yet

- Emerging MarketsDocument44 pagesEmerging MarketsKrishnendu GhoshNo ratings yet

- Global Cross Channel Retailing Report: The (Un) Connected StoreDocument38 pagesGlobal Cross Channel Retailing Report: The (Un) Connected StoreTan LeNo ratings yet

- Planning and Research in International MarketsDocument7 pagesPlanning and Research in International MarketsKhalil RushdiNo ratings yet

- MGT3054 Strategic ManagementDocument14 pagesMGT3054 Strategic ManagementTharvind KumarNo ratings yet

- MAN 010 Module 5Document5 pagesMAN 010 Module 5Maxine ConstantinoNo ratings yet

- Is Apparel Manufacturing Coming Home VFDocument32 pagesIs Apparel Manufacturing Coming Home VFAnkit Shreyash BhardwajNo ratings yet

- CNBC Catalyst The Road AheadDocument28 pagesCNBC Catalyst The Road AheadromanNo ratings yet

- Strategic ManagementLecture8Fall9Document20 pagesStrategic ManagementLecture8Fall9Md Fahimul Haque 1721143No ratings yet

- Go-to-Market Revolution May 2014 tcm9-84009Document80 pagesGo-to-Market Revolution May 2014 tcm9-84009typemonoNo ratings yet

- PoRCG 4 Full Issue 082415Document64 pagesPoRCG 4 Full Issue 082415ChahinezHejjamyNo ratings yet

- MKTC001 - Marketing Managment - Both AssignmentDocument330 pagesMKTC001 - Marketing Managment - Both Assignmentanish13121991No ratings yet

- Bimtech Mmi Vi Market AnalysisDocument51 pagesBimtech Mmi Vi Market AnalysisHitesh SharmaNo ratings yet

- C2B2B2C Business Model: Marketing Strategy For Digital EraDocument6 pagesC2B2B2C Business Model: Marketing Strategy For Digital EraInternational Journal of Business Marketing and ManagementNo ratings yet

- Operations As A Competitive Advantage in A Disruptiv PDFDocument172 pagesOperations As A Competitive Advantage in A Disruptiv PDFDIGITALIEUNo ratings yet

- International Business ManagementDocument33 pagesInternational Business Managementpragya jainNo ratings yet

- Bsiness Level Strategy (11 To 16)Document61 pagesBsiness Level Strategy (11 To 16)saumya shrivastavNo ratings yet

- Costco Wholesale Corporation: "Quality Goods and Services and The Lowest Price."Document23 pagesCostco Wholesale Corporation: "Quality Goods and Services and The Lowest Price."RBNo ratings yet

- Strategic Challenges Faced by FMCG and RetailDocument53 pagesStrategic Challenges Faced by FMCG and RetailRajNo ratings yet

- Customer Relationship Management: Concepts and TechnologiesDocument32 pagesCustomer Relationship Management: Concepts and TechnologiesLaiba Khan100% (1)

- Interface Between Place and Promotion: Selling StrategyDocument42 pagesInterface Between Place and Promotion: Selling StrategyPuja Jaiswal100% (1)

- BCG Emerging Market Companies Up Their Game Oct 2018 Tcm9 204262Document26 pagesBCG Emerging Market Companies Up Their Game Oct 2018 Tcm9 204262kshitijsaxenaNo ratings yet

- Strategic Management Part 8Document5 pagesStrategic Management Part 8aansh rajNo ratings yet

- Deloitte General Trends 2023Document48 pagesDeloitte General Trends 2023Kanika.SinghNo ratings yet

- MMI Outline PGDM (2010-12)Document6 pagesMMI Outline PGDM (2010-12)Siddharth SinghNo ratings yet

- Operation Strategy: By: Ot Chan Dy, Be & Msc. Management Institute of CambodiaDocument55 pagesOperation Strategy: By: Ot Chan Dy, Be & Msc. Management Institute of Cambodiatopnotcher2011No ratings yet

- KNOW Your Consumer: What You See Is What You Get!Document56 pagesKNOW Your Consumer: What You See Is What You Get!Yash NyatiNo ratings yet

- Big Decision of CCD Related To Marketing DecisionDocument4 pagesBig Decision of CCD Related To Marketing DecisionKeshav talwarNo ratings yet

- How Market Research Supports The New Product Development DecisionDocument5 pagesHow Market Research Supports The New Product Development DecisionKeshav talwarNo ratings yet

- Big Decision of CCD Related To Marketing DecisionDocument4 pagesBig Decision of CCD Related To Marketing DecisionKeshav talwarNo ratings yet

- BakeysDocument7 pagesBakeysKeshav talwarNo ratings yet

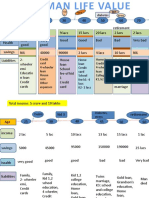

- Human Life ValueDocument2 pagesHuman Life ValueKeshav talwarNo ratings yet

- Brochure Shriram Assured Income Plan OfflineDocument12 pagesBrochure Shriram Assured Income Plan OfflineBellapu Durga vara prasadNo ratings yet

- Management of OrganizationDocument7 pagesManagement of OrganizationKeshav talwarNo ratings yet

- Human Life Value.Document2 pagesHuman Life Value.Keshav talwarNo ratings yet

- BS en 13369-2018 - TC - (2020-11-30 - 09-45-34 Am)Document164 pagesBS en 13369-2018 - TC - (2020-11-30 - 09-45-34 Am)Mustafa Uzyardoğan100% (1)

- Cassius Resume CVLatestDocument3 pagesCassius Resume CVLatestCaszNo ratings yet

- Tender Document For EOI of NIFT BhopalDocument19 pagesTender Document For EOI of NIFT Bhopalkethhes waranNo ratings yet

- Suricata User Guide: Release 4.1.0-DevDocument272 pagesSuricata User Guide: Release 4.1.0-DevDavid Simon Hoyos GonzalezNo ratings yet

- Course Code: CT-123 Course Title: Basic Networking Course DescriptionDocument3 pagesCourse Code: CT-123 Course Title: Basic Networking Course Descriptiondmcjr_stiNo ratings yet

- 1b.exadata X9M 2Document29 pages1b.exadata X9M 2Edu KiaiNo ratings yet

- Cebex 305: Constructive SolutionsDocument4 pagesCebex 305: Constructive SolutionsBalasubramanian AnanthNo ratings yet

- Uber+PM+Prioritisation+Assignment+Submission+File-Shashank KaranthDocument6 pagesUber+PM+Prioritisation+Assignment+Submission+File-Shashank KaranthShashank KaranthNo ratings yet

- Pertemuan Ke 12 - The Passive VoiceDocument5 pagesPertemuan Ke 12 - The Passive VoiceZarNo ratings yet

- But Flee Youthful Lusts - pdf2Document2 pagesBut Flee Youthful Lusts - pdf2emmaboakye2fNo ratings yet

- A Narrative Comprehensive Report of Student Teaching ExperiencesDocument82 pagesA Narrative Comprehensive Report of Student Teaching ExperiencesEpal Carlo74% (23)

- Boot Time Memory ManagementDocument22 pagesBoot Time Memory Managementblack jamNo ratings yet

- Zero Voltage Switching Active Clamp Buck-BoostDocument10 pagesZero Voltage Switching Active Clamp Buck-Boostranjitheee1292No ratings yet

- John Deere CaseDocument2 pagesJohn Deere CaseAldo ReynaNo ratings yet

- 2.HVT Terminacion InstrDocument18 pages2.HVT Terminacion Instrelectrica3No ratings yet

- Answerkey Precise ListeningDocument26 pagesAnswerkey Precise ListeningAn LeNo ratings yet

- Guru Stotram-1Document5 pagesGuru Stotram-1Green WattNo ratings yet

- A Priori and A Posteriori Knowledge: A Priori Knowledge Is Knowledge That Is Known Independently of Experience (That IsDocument7 pagesA Priori and A Posteriori Knowledge: A Priori Knowledge Is Knowledge That Is Known Independently of Experience (That Ispiyush_maheshwari22No ratings yet

- Sociology Internal AssessmentDocument21 pagesSociology Internal AssessmentjavoughnNo ratings yet

- Segment Reporting Decentralized Operations and Responsibility Accounting SystemDocument34 pagesSegment Reporting Decentralized Operations and Responsibility Accounting SystemalliahnahNo ratings yet

- Deaths in New York City Are More Than Double The Usual TotalDocument3 pagesDeaths in New York City Are More Than Double The Usual TotalRamón RuizNo ratings yet

- Prakhar Gupta Epics and Empires-Game of Thrones Make Up EssayDocument5 pagesPrakhar Gupta Epics and Empires-Game of Thrones Make Up EssayGat DanNo ratings yet

- Step Buying Process in LazadaDocument4 pagesStep Buying Process in LazadaAfifah FatihahNo ratings yet

- 3286306Document5 pages3286306Sanjit OracleTrainingNo ratings yet

- Reflective EssayDocument4 pagesReflective Essayapi-385380366No ratings yet

- DiseasesDocument11 pagesDiseasesapi-307430346No ratings yet

- FreeBSD HandbookDocument26 pagesFreeBSD Handbookhembeck119No ratings yet

- Tahmina Ferdousy Jhumu: HND Btec Unit 15 Psychology For Health and Social CareDocument29 pagesTahmina Ferdousy Jhumu: HND Btec Unit 15 Psychology For Health and Social CareNabi BoxNo ratings yet

- Understanding EarsDocument1 pageUnderstanding EarsmerkyworksNo ratings yet

- Can We Define Ecosystems - On The Confusion Between Definition and Description of Ecological ConceptsDocument15 pagesCan We Define Ecosystems - On The Confusion Between Definition and Description of Ecological ConceptsKionara SarabellaNo ratings yet