You might also like

- Please Pay by Total Due: Casimiro YulfoDocument2 pagesPlease Pay by Total Due: Casimiro YulfoJohn Bean100% (4)

- Alternate Demonstration Problem MerchandisingDocument5 pagesAlternate Demonstration Problem MerchandisingmoNo ratings yet

- SRCBAI ABM1 Q3M10 Merchandising Concern Part1Document14 pagesSRCBAI ABM1 Q3M10 Merchandising Concern Part1Jaye RuantoNo ratings yet

- Answer-Assignment DMBA104 MBA1 2 Set-1 and 2 Sep 2023Document13 pagesAnswer-Assignment DMBA104 MBA1 2 Set-1 and 2 Sep 2023Sabari Nathan100% (1)

- Chapter 5Document14 pagesChapter 5RB100% (3)

- Incoterms: EXW FCA CPT CIP DAT DAP DDP FAS FOB CFR CIFDocument1 pageIncoterms: EXW FCA CPT CIP DAT DAP DDP FAS FOB CFR CIFFerney Alejandro Diaz PaezNo ratings yet

- Merchadising LectureDocument12 pagesMerchadising Lecturejeonlei02No ratings yet

- In-Class Exercise Chapter 5Document6 pagesIn-Class Exercise Chapter 5Thomas TermoteNo ratings yet

- 1 InventoriesDocument4 pages1 InventoriesJamie MarizNo ratings yet

- Accounting For MerchandisingDocument15 pagesAccounting For MerchandisingAj de CastroNo ratings yet

- NIAT Review 3Document7 pagesNIAT Review 3April Joy InductaNo ratings yet

- Accounts ReceivableDocument54 pagesAccounts ReceivableFrancine Thea M. LantayaNo ratings yet

- Exercise Set-Intro For Merchandising BusinessDocument10 pagesExercise Set-Intro For Merchandising BusinessCha Eun WooNo ratings yet

- Acctng 2 MerchandiseDocument2 pagesAcctng 2 MerchandiseDonald BugtongNo ratings yet

- Chapter 7 09302019Document38 pagesChapter 7 09302019Arjay Molina100% (1)

- Merchandising BusinessDocument26 pagesMerchandising BusinessDan Gideon CariagaNo ratings yet

- Handout No. 03 - Purchase TransactionsDocument4 pagesHandout No. 03 - Purchase TransactionsApril SasamNo ratings yet

- Chapter 16 InventoriesDocument21 pagesChapter 16 InventoriesDidik DidiksterNo ratings yet

- 2018-0232 Beldia, Pitchie Mae G. ACT142: Auditing and Assurance: Concepts and Application 1Document8 pages2018-0232 Beldia, Pitchie Mae G. ACT142: Auditing and Assurance: Concepts and Application 1Melanie SamsonaNo ratings yet

- Basic Accounting - Q6Document3 pagesBasic Accounting - Q6wivadaNo ratings yet

- Accounts Receivable: Notwithstanding, Are Classified As Current AssetsDocument13 pagesAccounts Receivable: Notwithstanding, Are Classified As Current AssetsAdyangNo ratings yet

- 2018-1383 Samsona, Melanie S.Document8 pages2018-1383 Samsona, Melanie S.Melanie SamsonaNo ratings yet

- 9 Consignment SalesDocument11 pages9 Consignment SalesNil Justeen GarciaNo ratings yet

- Intacc NotesDocument11 pagesIntacc NotesKeith SalesNo ratings yet

- Acctg Exercise 2Document10 pagesAcctg Exercise 2Honeybunch beforeNo ratings yet

- Intermediate Accounting 1 Inventories AssignmentDocument3 pagesIntermediate Accounting 1 Inventories AssignmentGabriel Adrian Obungen0% (1)

- Merchandising Operations - CRDocument21 pagesMerchandising Operations - CRHabte AbeNo ratings yet

- Accounting for Merchandising OperationsDocument21 pagesAccounting for Merchandising OperationsNicole CagasNo ratings yet

- Special JournalsDocument5 pagesSpecial Journalsgnssgtld7No ratings yet

- Cash Discounts & Trade Discounts I. DrillDocument3 pagesCash Discounts & Trade Discounts I. DrillArny MaynigoNo ratings yet

- December 16 Complete Lecture With SolutionsDocument6 pagesDecember 16 Complete Lecture With SolutionsJa FranciscoNo ratings yet

- MerchandisingDocument17 pagesMerchandisingFelipe DologNo ratings yet

- MerchandisingDocument11 pagesMerchandisingShinjiNo ratings yet

- Practice Quiz - Quiz 2: Answer: Debit Accounts Receivable 26,250 Debit Freight Out 1,250 Credit Sales 27,500Document5 pagesPractice Quiz - Quiz 2: Answer: Debit Accounts Receivable 26,250 Debit Freight Out 1,250 Credit Sales 27,500Kieht catcherNo ratings yet

- Reading Material and ActivitiesDocument2 pagesReading Material and ActivitiesErlyn Joyce CerillaNo ratings yet

- Inventories (Problems)Document6 pagesInventories (Problems)IAN PADAYOGDOGNo ratings yet

- Midterm Quiz No 2Document2 pagesMidterm Quiz No 2mariejoyceaggabaoNo ratings yet

- Intermediate Accounting 1 Inventories - Assignment A. Supply The Missing AmountsDocument5 pagesIntermediate Accounting 1 Inventories - Assignment A. Supply The Missing AmountsGabriel Adrian ObungenNo ratings yet

- 05 Accounting For Merchandising OperationsDocument33 pages05 Accounting For Merchandising OperationsoriboiNo ratings yet

- Acctg 1 11 101 Final ExamDocument3 pagesAcctg 1 11 101 Final ExamMichael John DayondonNo ratings yet

- Lesson 6 - FA1Document56 pagesLesson 6 - FA1angelo eleazarNo ratings yet

- Mechandising - Part 1Document22 pagesMechandising - Part 1hello hayaNo ratings yet

- 4 Accounts ReceivableDocument10 pages4 Accounts ReceivableAYEZZA SAMSONNo ratings yet

- Merchandising BusinessDocument26 pagesMerchandising BusinessPatricia Mae CruzNo ratings yet

- Merchandising Operations JournalizingDocument45 pagesMerchandising Operations JournalizingNeri La LunaNo ratings yet

- Teresita Buenaflor ShoesDocument30 pagesTeresita Buenaflor ShoesHannah Pearl Flores Villar100% (1)

- Guide to Accounting for Merchandising BusinessesDocument12 pagesGuide to Accounting for Merchandising BusinessesLeica Jayme100% (1)

- Chapter 4, 5, 6 AssignmentDocument23 pagesChapter 4, 5, 6 AssignmentSamantha Charlize VizcondeNo ratings yet

- Accounting For A Merchandising Business Week 3Document35 pagesAccounting For A Merchandising Business Week 3kayeNo ratings yet

- Cash and Accrual BasisDocument24 pagesCash and Accrual BasisAlexa LeeNo ratings yet

- Accounting For Merchandising BusinessDocument21 pagesAccounting For Merchandising BusinessJunel PlanosNo ratings yet

- Integrated Accounting Learning Module Attachment (Do Not Copy)Document15 pagesIntegrated Accounting Learning Module Attachment (Do Not Copy)Jasper PelicanoNo ratings yet

- Accounts Receivables 1Document6 pagesAccounts Receivables 1Ralph Renan NapalaNo ratings yet

- Unit II A Accounts ReceivablesDocument12 pagesUnit II A Accounts ReceivablesJulie Ann TolinNo ratings yet

- Working Papers in InventoriesDocument17 pagesWorking Papers in InventoriesTrisha VillegasNo ratings yet

- Acccob2-Chapter5-Inventories - ExercisesDocument65 pagesAcccob2-Chapter5-Inventories - ExercisesMelyssa Dawn GullonNo ratings yet

- MerchandisingDocument37 pagesMerchandisingDaniel Togonon Capones Jr.No ratings yet

- ACC101 Chapter4new PDFDocument25 pagesACC101 Chapter4new PDFJonnafe Almendralejo IntanoNo ratings yet

- PAS 2: INVENTORIESDocument22 pagesPAS 2: INVENTORIESRey ViloriaNo ratings yet

- Accounting For Merchandising Operations: HOSP 1210 (Financial Acct) Learning CentreDocument4 pagesAccounting For Merchandising Operations: HOSP 1210 (Financial Acct) Learning CentreHuening KaiNo ratings yet

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- TLE Q2 W3 Online PresentationDocument19 pagesTLE Q2 W3 Online PresentationJean Paula SequiñoNo ratings yet

- TLE 6 ICT ENTREP Q1 Week 5Document10 pagesTLE 6 ICT ENTREP Q1 Week 5Jean Paula SequiñoNo ratings yet

- TLE Q2 W7 Online PresentationDocument12 pagesTLE Q2 W7 Online PresentationJean Paula SequiñoNo ratings yet

- TLE 6 ICT ENTREP Q1 Week 1Document10 pagesTLE 6 ICT ENTREP Q1 Week 1Jean Paula SequiñoNo ratings yet

- TLE 6 ICT ENTREP Q1 Week 8Document9 pagesTLE 6 ICT ENTREP Q1 Week 8Jean Paula SequiñoNo ratings yet

- Crim Old Curriculum Tri SemDocument3 pagesCrim Old Curriculum Tri SemJean Paula SequiñoNo ratings yet

- Online Class Etiquettes: Acknowledged YouDocument37 pagesOnline Class Etiquettes: Acknowledged YouJean Paula SequiñoNo ratings yet

- Weeks 10 Chapter 5. General Provisions (Republic Act No. 11232)Document6 pagesWeeks 10 Chapter 5. General Provisions (Republic Act No. 11232)Jean Paula SequiñoNo ratings yet

- Here are the steps to solve this problem:1) 10, 15The difference between terms is 5. The rule is: Add 5.Next three terms: 20, 25, 30Rule for nth term: n + 52) 2, 6, 12, 20Document9 pagesHere are the steps to solve this problem:1) 10, 15The difference between terms is 5. The rule is: Add 5.Next three terms: 20, 25, 30Rule for nth term: n + 52) 2, 6, 12, 20Jean Paula Sequiño100% (1)

- q1 Entrepreneurship Module 1 PDF FreeDocument21 pagesq1 Entrepreneurship Module 1 PDF FreeJean Paula SequiñoNo ratings yet

- Quarter 2 Week 8: Animal Raising and Fish FarmingDocument14 pagesQuarter 2 Week 8: Animal Raising and Fish FarmingJean Paula SequiñoNo ratings yet

- TLE Q3 W3 Online PresentationDocument11 pagesTLE Q3 W3 Online PresentationJean Paula SequiñoNo ratings yet

- IGCSE Economics Discuss Question NotesDocument12 pagesIGCSE Economics Discuss Question NotesAliya KNo ratings yet

- Commercial Invoice: Reset FormDocument3 pagesCommercial Invoice: Reset FormBen AliNo ratings yet

- Ch31 Open Economy MacroeconomicesDocument42 pagesCh31 Open Economy MacroeconomicesHannah ZhangNo ratings yet

- Indian ExportDocument17 pagesIndian ExportrajjogiNo ratings yet

- Qu NH Cute Phô Mai QueDocument5 pagesQu NH Cute Phô Mai QueNguyễn QuỳnhNo ratings yet

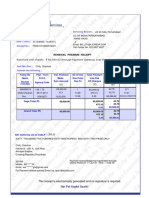

- Received With Thanks ' 60,569.62 Through Payment Gateway Over The Internet FromDocument1 pageReceived With Thanks ' 60,569.62 Through Payment Gateway Over The Internet FromCSK100% (1)

- Invoice for eSignature Standard Edition SubscriptionDocument1 pageInvoice for eSignature Standard Edition SubscriptionjhilikNo ratings yet

- Money, Banking and International TradeDocument228 pagesMoney, Banking and International TradeRashmiNo ratings yet

- Pertemuan 10 SCMDocument31 pagesPertemuan 10 SCMaburizarahmanNo ratings yet

- Impacts and Main Issues of Korea-China FTADocument6 pagesImpacts and Main Issues of Korea-China FTAKorea Economic Institute of America (KEI)No ratings yet

- The Basics of Tariff & Customs Laws in The PhilippinesDocument8 pagesThe Basics of Tariff & Customs Laws in The PhilippinesRaymond AndesNo ratings yet

- On Currency WarDocument22 pagesOn Currency WarrajutheoneNo ratings yet

- 2GO Together - Tools - Day 1 (E-Trace)Document1 page2GO Together - Tools - Day 1 (E-Trace)Maicha LucaylucayNo ratings yet

- Petty Cash Bank Reconciliation Bill Jovi Is Reviewing The Cash PDFDocument1 pagePetty Cash Bank Reconciliation Bill Jovi Is Reviewing The Cash PDFAnbu jaromiaNo ratings yet

- Electronic Trading SystemDocument31 pagesElectronic Trading SystemMd.abdul AzizNo ratings yet

- Heckscher-Ohlin TheoryDocument19 pagesHeckscher-Ohlin TheoryRahul GoyalNo ratings yet

- Effects of Inflation AlchianDocument18 pagesEffects of Inflation AlchianCoco 12No ratings yet

- Puducherry Sunday Market: A Paradise for Book LoversDocument4 pagesPuducherry Sunday Market: A Paradise for Book LoversSuriya ArNo ratings yet

- Comparing Macroeconomics of India and France EconomiesDocument26 pagesComparing Macroeconomics of India and France EconomiesDiksha LathNo ratings yet

- Macroeconomics Focus: Growth, Inflation, Balance of PaymentsDocument3 pagesMacroeconomics Focus: Growth, Inflation, Balance of PaymentsAnh LeNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument39 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceVishal BhosaleNo ratings yet

- Cash Book NotesDocument4 pagesCash Book NotesJoRaccoonaNo ratings yet

- Clarity Inquiry #jqn39d08gqDocument15 pagesClarity Inquiry #jqn39d08gqChristopher IknerNo ratings yet

- Compare trading fees and calculate profits for top crypto exchangesDocument8 pagesCompare trading fees and calculate profits for top crypto exchangesLester Bug-osNo ratings yet

- Pearson trade theory quizDocument31 pagesPearson trade theory quizHemant Deshmukh100% (2)

- Chapter 04Document38 pagesChapter 04dimren20No ratings yet

- CFAS Reviewer - Module 6Document14 pagesCFAS Reviewer - Module 6Lizette Janiya SumantingNo ratings yet

- International Business: by Charles W.L. HillDocument29 pagesInternational Business: by Charles W.L. HillRadha PalachollaNo ratings yet