You might also like

- CAF 1 Autumn 2023Document7 pagesCAF 1 Autumn 2023Asim MahmoodNo ratings yet

- Batch - 19 - Aug - 2021-With CommentsDocument15 pagesBatch - 19 - Aug - 2021-With CommentsSomeshNo ratings yet

- Chapter 16: Tool Kit For Working Capital ManagementDocument23 pagesChapter 16: Tool Kit For Working Capital ManagementosamaNo ratings yet

- Bodie10ce SM CH18Document20 pagesBodie10ce SM CH18beadand1No ratings yet

- Tugas Akhir GGRMDocument34 pagesTugas Akhir GGRMFairly 288No ratings yet

- Corprate FinanceDocument14 pagesCorprate Financeramisha tasnuvaNo ratings yet

- Proyeksi INAF - Kelompok 3Document43 pagesProyeksi INAF - Kelompok 3Fairly 288No ratings yet

- Fixed Income Market Report - 31.01.2022Document1 pageFixed Income Market Report - 31.01.2022Fuaad DodooNo ratings yet

- Goil Company Limited: Group Unaudited Statement of Comprehensive Income For The Period Ended March 31,2022Document4 pagesGoil Company Limited: Group Unaudited Statement of Comprehensive Income For The Period Ended March 31,2022Fuaad DodooNo ratings yet

- Income Statement ForecastDocument1 pageIncome Statement ForecastMuhammad Irfan ZafarNo ratings yet

- Apex QE2012 Paper 1 Suggested Solution Question 2 CleanDocument2 pagesApex QE2012 Paper 1 Suggested Solution Question 2 CleanNicolasNo ratings yet

- CH 08 A Solution SET 1Document3 pagesCH 08 A Solution SET 1kolidishant692No ratings yet

- Valuation Final ExamDocument4 pagesValuation Final ExamJeane Mae Boo100% (1)

- M6 Promissory NotesDocument14 pagesM6 Promissory NotesAldous RenielNo ratings yet

- D.M Textile Mill: Calculations: 1. Current RatioDocument9 pagesD.M Textile Mill: Calculations: 1. Current RatioArslan GulrazNo ratings yet

- AY5122 Semester 2 2022 2023 StudentsDocument8 pagesAY5122 Semester 2 2022 2023 StudentsRahulNo ratings yet

- F9 Mock Exam June 2020 - Answers PDFDocument9 pagesF9 Mock Exam June 2020 - Answers PDFNguyễn Quốc TuấnNo ratings yet

- 9706 Accounting: MARK SCHEME For The October/November 2013 SeriesDocument5 pages9706 Accounting: MARK SCHEME For The October/November 2013 SeriestarunyadavfutureNo ratings yet

- Option StratergiesDocument8 pagesOption StratergiesPANU INGAVALENo ratings yet

- 3756 Skema Trial PERLIS 2022Document14 pages3756 Skema Trial PERLIS 2022parameswariNo ratings yet

- Hard Rock (Pty) LTD - SolutionDocument8 pagesHard Rock (Pty) LTD - SolutionNicolasNo ratings yet

- United Metal: Initial Outlay (IO) CalculationDocument3 pagesUnited Metal: Initial Outlay (IO) CalculationMarjina Binte Abbas BrishtiNo ratings yet

- New Changes in Company Balance SheetDocument12 pagesNew Changes in Company Balance SheetSBMG & AssociatesNo ratings yet

- Interest Bearing Note - Periodic Collection (Interest Only) PremiumDocument2 pagesInterest Bearing Note - Periodic Collection (Interest Only) PremiumShannonNo ratings yet

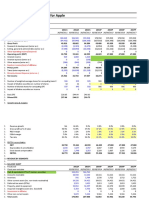

- Financial Statement Model For Apple: $ MM Except Per ShareDocument16 pagesFinancial Statement Model For Apple: $ MM Except Per ShareThinh TNTNo ratings yet

- DiviđenDocument12 pagesDiviđenPhan GiápNo ratings yet

- FIT Adj. AR TestingDocument14 pagesFIT Adj. AR TestingAlvin Lozares CasajeNo ratings yet

- Bay Beak Co. - Activity StatementDocument2 pagesBay Beak Co. - Activity StatementJanine Leigh BacalsoNo ratings yet

- Fundamentals of Business Math Canadian 3rd Edition Jerome Solutions ManualDocument21 pagesFundamentals of Business Math Canadian 3rd Edition Jerome Solutions Manualnorianenclasphxnu100% (23)

- Case 3 Intro To Statistics (Data)Document8 pagesCase 3 Intro To Statistics (Data)Akoo Lagie MalesNo ratings yet

- Dwnload Full Corporate Financial Management 5th Edition Glen Arnold Solutions Manual PDFDocument35 pagesDwnload Full Corporate Financial Management 5th Edition Glen Arnold Solutions Manual PDFhofstadgypsyus100% (14)

- Txbwa 2022 Dec ADocument9 pagesTxbwa 2022 Dec AArundhati SinghNo ratings yet

- FY 2022 Earnings Call Deck 3 - 13 - 2023 For PostDocument27 pagesFY 2022 Earnings Call Deck 3 - 13 - 2023 For PostCesar AugustoNo ratings yet

- Antm FinalllllDocument3 pagesAntm FinalllllRenita KhofifahNo ratings yet

- Poa T - 13Document3 pagesPoa T - 13SHEVENA A/P VIJIANNo ratings yet

- UltraTech Cements and Jaiprakash AssociatesDocument8 pagesUltraTech Cements and Jaiprakash AssociatesanushaNo ratings yet

- PMPU - D4 AkuntansiDocument13 pagesPMPU - D4 AkuntansiNanadNo ratings yet

- Taxation: Gudani/Naranjo/Siapian First Pre-Board Examination August 6, 2022Document15 pagesTaxation: Gudani/Naranjo/Siapian First Pre-Board Examination August 6, 2022Harold Dan AcebedoNo ratings yet

- BINISH M MODELDocument8 pagesBINISH M MODELlyrastarfallauthorNo ratings yet

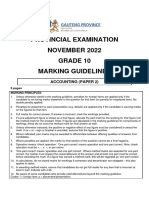

- GR 10 Accounting P2 (English) November 2022 Possible AnswersDocument9 pagesGR 10 Accounting P2 (English) November 2022 Possible AnswersRea SeremaNo ratings yet

- Review Guide W/ Tables For Depreciation & TaxesDocument29 pagesReview Guide W/ Tables For Depreciation & Taxesjer7313No ratings yet

- SBR II Group 2Document1,654 pagesSBR II Group 2Ankit JindalNo ratings yet

- Fins 1612Document51 pagesFins 1612Q VanichaNo ratings yet

- Research Needed For Question 5Document4 pagesResearch Needed For Question 5Ahmed MahmoudNo ratings yet

- NWC model + CF new versionDocument1 pageNWC model + CF new versionmichael odiemboNo ratings yet

- WBD 1Q23 Trending Schedule Final 05 04 23Document12 pagesWBD 1Q23 Trending Schedule Final 05 04 23Stephano Gomes GabrielNo ratings yet

- InvalidDocument6 pagesInvalidSUHAIL ALINo ratings yet

- Promissory NotesDocument10 pagesPromissory Notespretty lyreNo ratings yet

- Unaudited Financial Statements For The Period Ended 31 March, 2022Document2 pagesUnaudited Financial Statements For The Period Ended 31 March, 2022Fuaad DodooNo ratings yet

- RateSheet January 2024 ReviewedDocument1 pageRateSheet January 2024 Revieweddonovansaunders058No ratings yet

- 62976cbd028e75bc7a73ce84 - AltSignals VVIP 2022 04 April Forex Report - Wo - WPDocument3 pages62976cbd028e75bc7a73ce84 - AltSignals VVIP 2022 04 April Forex Report - Wo - WPGiovanni PalermoNo ratings yet

- GDV: TDC:: Per PeriodDocument9 pagesGDV: TDC:: Per PeriodM. HfizzNo ratings yet

- Horana Plantation Ratio Analysis - Accounting AssignmentDocument7 pagesHorana Plantation Ratio Analysis - Accounting AssignmentNuwani ManasingheNo ratings yet

- PRTC 1stpb - 05.22 Sol TaxDocument21 pagesPRTC 1stpb - 05.22 Sol TaxCiatto SpotifyNo ratings yet

- Full Download Corporate Financial Management 5th Edition Glen Arnold Solutions ManualDocument35 pagesFull Download Corporate Financial Management 5th Edition Glen Arnold Solutions Manualmasonh7dswebb100% (39)

- Answer Q3 Minicase Chapt 26Document7 pagesAnswer Q3 Minicase Chapt 26damtuan11012000No ratings yet

- 1 - Carriage InwardsDocument2 pages1 - Carriage Inwardswaleedsikander997No ratings yet

- HBMN330-1 Submit Sa1Document6 pagesHBMN330-1 Submit Sa1Yolanda MazibukoNo ratings yet

- Fixed Income Market Report - 04.07.2022Document1 pageFixed Income Market Report - 04.07.2022Fuaad DodooNo ratings yet

- Sponsorship Resume TemplateDocument12 pagesSponsorship Resume TemplatetakundaNo ratings yet

- Actuary Linkk at KentDocument2 pagesActuary Linkk at KenttakundaNo ratings yet

- College InformationDocument29 pagesCollege InformationtakundaNo ratings yet

- Foundations of Deep LearningDocument48 pagesFoundations of Deep LearningtakundaNo ratings yet

- HPRM440 1 July Dec2022 FA2 LN V3 17062022Document11 pagesHPRM440 1 July Dec2022 FA2 LN V3 17062022takundaNo ratings yet

- Telecom Analytics SolutionsDocument12 pagesTelecom Analytics Solutionsdivya2882No ratings yet

- Foundations of Machine Learning - 3Document38 pagesFoundations of Machine Learning - 3takundaNo ratings yet

- ECS4863 2022 Assignment 03 - Corrected VersionDocument3 pagesECS4863 2022 Assignment 03 - Corrected VersiontakundaNo ratings yet

- Introduction to Data Warehousing and Business IntelligenceDocument72 pagesIntroduction to Data Warehousing and Business IntelligenceJhansi NayakNo ratings yet

- Foundations of Machine Learning - 3Document38 pagesFoundations of Machine Learning - 3takundaNo ratings yet

- CHP 19Document63 pagesCHP 19mona yadvNo ratings yet

- Top Big Data Analytics Use CasesDocument18 pagesTop Big Data Analytics Use CasestakundaNo ratings yet

- Big Data BasicsDocument70 pagesBig Data BasicsAlexandru PuiuNo ratings yet

- Use Cases and Challenges in Telecom Big Data AnalyDocument7 pagesUse Cases and Challenges in Telecom Big Data AnalybasseyNo ratings yet

- Churn Analysis in Telecommunication Using Logistic RegressionDocument6 pagesChurn Analysis in Telecommunication Using Logistic RegressiontakundaNo ratings yet

- Ratios: Interpreting Financial StatementsDocument3 pagesRatios: Interpreting Financial StatementsMr RizviNo ratings yet

- Assymetric Information - Adverse Selection and Moral HazardDocument6 pagesAssymetric Information - Adverse Selection and Moral HazardRayniel ZabalaNo ratings yet

- UT Dallas Syllabus For Ba4349.501 05f Taught by Mark Frost (Mfrost)Document3 pagesUT Dallas Syllabus For Ba4349.501 05f Taught by Mark Frost (Mfrost)UT Dallas Provost's Technology GroupNo ratings yet

- ML PointsDocument196 pagesML Pointsapi-3744156100% (8)

- Project Red: Problem 9-3: Daisy CompanyDocument2 pagesProject Red: Problem 9-3: Daisy CompanyJPNo ratings yet

- Brac Bank PresentationDocument24 pagesBrac Bank PresentationSumi Islam100% (2)

- APSFC Application Fee Challan FormDocument1 pageAPSFC Application Fee Challan Formapr12_86No ratings yet

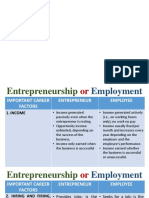

- Choosing Between Entrepreneurship and EmploymentDocument9 pagesChoosing Between Entrepreneurship and EmploymentMa Melissa Nacario SanPedroNo ratings yet

- Soal-Soal Chap 017 Understasnding Accounting and Information SystemDocument52 pagesSoal-Soal Chap 017 Understasnding Accounting and Information SystemNurhayati SitorusNo ratings yet

- 6.1 and 6.2 - Balance of Payments Accounts & Exchange RatesDocument5 pages6.1 and 6.2 - Balance of Payments Accounts & Exchange RatesReed-Animated ProductionsNo ratings yet

- Beechy 7e Tif Ch09Document20 pagesBeechy 7e Tif Ch09mashta04No ratings yet

- Role of Tech in Promoting Financial InclusionDocument66 pagesRole of Tech in Promoting Financial InclusionKheang VesalNo ratings yet

- Income Tax: General Principles: Module No. 4Document4 pagesIncome Tax: General Principles: Module No. 4Jay Lord Floresca100% (1)

- JPM - Economic Data AnalysisDocument11 pagesJPM - Economic Data AnalysisAvid HikerNo ratings yet

- SBI Project ReportDocument14 pagesSBI Project ReportNick IvanNo ratings yet

- Arsenal FC Financial AnalysisDocument14 pagesArsenal FC Financial AnalysisDidiDieva0% (1)

- Finance and Economics - 22 CasesDocument35 pagesFinance and Economics - 22 CasesSeong-uk KimNo ratings yet

- Working Capital ManagementDocument82 pagesWorking Capital ManagementAnacristina PincaNo ratings yet

- ACCA REVISION MOCK EXAMDocument14 pagesACCA REVISION MOCK EXAMGyanu Khatri100% (3)

- Mod 3Document3 pagesMod 3Margarette ManaigNo ratings yet

- Pag Ibig Foreclosed Properties MAY 17Document9 pagesPag Ibig Foreclosed Properties MAY 17ramszlaiNo ratings yet

- Option Mine CalculatorDocument88 pagesOption Mine CalculatorVarinder AnandNo ratings yet

- Lecturer-Led Tutorial Chapter 5 (2023)Document9 pagesLecturer-Led Tutorial Chapter 5 (2023)Ncebakazi DawedeNo ratings yet

- Preparation of Project, Project Identification and Formulation, Project Appraisal & Sources of FinanceDocument19 pagesPreparation of Project, Project Identification and Formulation, Project Appraisal & Sources of FinanceDrRashmiranjan PanigrahiNo ratings yet

- Case Study - Financial AppDocument9 pagesCase Study - Financial AppprawinjhaNo ratings yet

- 55966bos45368may20 p5 cp3 PDFDocument26 pages55966bos45368may20 p5 cp3 PDFankush sharmaNo ratings yet

- Notes On Final Accounts & Journal& Ledger ProblemDocument17 pagesNotes On Final Accounts & Journal& Ledger ProblemSaiVenkatNo ratings yet

- B.Com Money and Banking Reading MaterialDocument110 pagesB.Com Money and Banking Reading MaterialBabita DeviNo ratings yet

- Money MattersDocument2 pagesMoney MattersAndrew ChambersNo ratings yet

- Vendor-Form Sakchham KarkiDocument4 pagesVendor-Form Sakchham KarkiMijuna RukihaNo ratings yet

- Adjusted Adjusted Trial Balance Income Statement BalanceDocument1 pageAdjusted Adjusted Trial Balance Income Statement BalancedreaNo ratings yet