You might also like

- Atria Convergence Technologies Limited, Due Date: 10 // /202 1Document3 pagesAtria Convergence Technologies Limited, Due Date: 10 // /202 1Siva Sagar JaggaNo ratings yet

- P.Y Question Paper Income Tax Delhi UniversityDocument5 pagesP.Y Question Paper Income Tax Delhi UniversityHarsh chetiwal50% (2)

- Tax 5th Semeter Selected Questions PDFDocument40 pagesTax 5th Semeter Selected Questions PDFAvBNo ratings yet

- Chapter 25 Test BankDocument69 pagesChapter 25 Test BankBrandon Lee100% (1)

- Total Income Questions Set A Assessment Year 2021-22-18th EditionDocument30 pagesTotal Income Questions Set A Assessment Year 2021-22-18th EditionKaran Singh RanaNo ratings yet

- TaxationsDocument12 pagesTaxationsKansal AbhishekNo ratings yet

- 18515pcc Sugg Paper Nov09 5 PDFDocument16 pages18515pcc Sugg Paper Nov09 5 PDFGaurang AgarwalNo ratings yet

- Total IncomeDocument4 pagesTotal IncomeSiddharth VaswaniNo ratings yet

- PGBP QuestionsDocument6 pagesPGBP QuestionsHdkakaksjsb100% (2)

- New Course Solutions May 2019Document18 pagesNew Course Solutions May 2019Kali KhannaNo ratings yet

- For Revision of Income TaxDocument5 pagesFor Revision of Income TaxMA AttariNo ratings yet

- Division B - Descriptive Questions Question No. 1 Is CompulsoryDocument5 pagesDivision B - Descriptive Questions Question No. 1 Is CompulsoryUrvashi RNo ratings yet

- BB SIR QUESTION BANK DT May 22Document216 pagesBB SIR QUESTION BANK DT May 22Srushti AgarwalNo ratings yet

- 17267pcc Sugg Paper June09 5Document18 pages17267pcc Sugg Paper June09 5nbaghrechaNo ratings yet

- It QuestionsDocument21 pagesIt QuestionssanatnaharNo ratings yet

- Test 3 Tax SolutionsDocument17 pagesTest 3 Tax SolutionsManjulaNo ratings yet

- Advanced Taxation 2011-2019 DecDocument259 pagesAdvanced Taxation 2011-2019 Decrajeshkandel345No ratings yet

- Income Tax May23 Free ResourcesDocument29 pagesIncome Tax May23 Free ResourcesPurna PatelNo ratings yet

- Taxation Review Dec2016Document6 pagesTaxation Review Dec2016Shaiful Alam FCANo ratings yet

- Question CAP III AND CA MEMBERHSIP New OneDocument17 pagesQuestion CAP III AND CA MEMBERHSIP New OneSuraj ThapaNo ratings yet

- Problems On Individual Taxation AY 2020-21 StudentsDocument9 pagesProblems On Individual Taxation AY 2020-21 StudentsAminul Islam RubelNo ratings yet

- Computation of Total Income & Tax LiabilityDocument24 pagesComputation of Total Income & Tax LiabilityKartikNo ratings yet

- Tax SuggestedDocument28 pagesTax SuggestedHemaNo ratings yet

- Computation of Income Under The Head "Profits and Gains of Business or Profession"Document14 pagesComputation of Income Under The Head "Profits and Gains of Business or Profession"Shubham KumarNo ratings yet

- IPCC Gr.I Paper 4 TaxationDocument10 pagesIPCC Gr.I Paper 4 TaxationAyushi RajputNo ratings yet

- Taxation Attempt All Questions (10 10 100)Document6 pagesTaxation Attempt All Questions (10 10 100)Mff DeadsparkNo ratings yet

- Finals Quiz No. 1 W AnswerDocument4 pagesFinals Quiz No. 1 W AnswerLouris DanielNo ratings yet

- Total Income DTDocument54 pagesTotal Income DTJay jainNo ratings yet

- Paper - 4: Taxation Section A: Income Tax Law Part - II: Receipts PaymentsDocument29 pagesPaper - 4: Taxation Section A: Income Tax Law Part - II: Receipts PaymentsVaishnavi ShindeNo ratings yet

- E-Filling of Returns (Shivdas 10 Years)Document122 pagesE-Filling of Returns (Shivdas 10 Years)Unicorn SpiderNo ratings yet

- Fifth PartDocument17 pagesFifth PartMahsinur RahmanNo ratings yet

- CA Inter Taxation Mock Test - 02.08.2018 - Only QuestionDocument7 pagesCA Inter Taxation Mock Test - 02.08.2018 - Only QuestionKaustubhNo ratings yet

- Question Income From Salary Solved in ClassDocument4 pagesQuestion Income From Salary Solved in ClassFozle Rabby 182-11-5893No ratings yet

- Paper 4 Studycafe - inDocument28 pagesPaper 4 Studycafe - inApeksha ChilwalNo ratings yet

- Tax AssignmentDocument11 pagesTax AssignmentAM NerdyNo ratings yet

- Taxation Review June2017Document9 pagesTaxation Review June2017Shaiful Alam FCANo ratings yet

- CA IPCC Inter Income Tax Revision - Kalpesh Classes PDFDocument61 pagesCA IPCC Inter Income Tax Revision - Kalpesh Classes PDFnagababuNo ratings yet

- CA IPCC Inter Income Tax Revision - Kalpesh Classes PDFDocument61 pagesCA IPCC Inter Income Tax Revision - Kalpesh Classes PDFSandra MaloosNo ratings yet

- TAX Quiz 2Document10 pagesTAX Quiz 2Ednalyn CruzNo ratings yet

- Model Question BBS 3rd Taxation in NepalDocument6 pagesModel Question BBS 3rd Taxation in NepalAsmita BhujelNo ratings yet

- CA Inter Taxation Mock Test - 02.08.2018 - Detailed SolutionfDocument14 pagesCA Inter Taxation Mock Test - 02.08.2018 - Detailed SolutionfKaustubhNo ratings yet

- Question Bank: Errorless Taxation by Ca Pranav Chandak at Pranav Chandak Academy, PuneDocument5 pagesQuestion Bank: Errorless Taxation by Ca Pranav Chandak at Pranav Chandak Academy, PuneSimran MeherNo ratings yet

- Inter Taxation 50 Important Questions 1676977237180910Document79 pagesInter Taxation 50 Important Questions 1676977237180910Tushar MittalNo ratings yet

- ACCT 402 AssignmentDocument5 pagesACCT 402 AssignmentDaniel TackieNo ratings yet

- Taxation - Direct and IndirectDocument6 pagesTaxation - Direct and IndirectSahiba SadanaNo ratings yet

- CAF2 Workshop (Business Income and STX Questions)Document9 pagesCAF2 Workshop (Business Income and STX Questions)Abdul qadirNo ratings yet

- Paper 4Document16 pagesPaper 4Kali KhannaNo ratings yet

- 54606bos43769 p4Document27 pages54606bos43769 p4HARSHAL MITTALNo ratings yet

- Tax Midterm Practise SolutionsDocument5 pagesTax Midterm Practise SolutionsShan Ali ShahNo ratings yet

- CH 2.TaxSalary IncomeDocument13 pagesCH 2.TaxSalary IncomeSajid AhmedNo ratings yet

- Faq'S & Guidlines On Income TaxDocument50 pagesFaq'S & Guidlines On Income TaxRavikarthik GurumurthyNo ratings yet

- Taxation Test 4 Scheduled Nov 2023 Solution 1689761654Document15 pagesTaxation Test 4 Scheduled Nov 2023 Solution 1689761654mwmw4prdy2No ratings yet

- Income From BusinessDocument8 pagesIncome From BusinessSuyash PrakashNo ratings yet

- DeductionsDocument13 pagesDeductionsShivaram ShivaramNo ratings yet

- Dardarat Dilg Budget ReportsDocument4 pagesDardarat Dilg Budget ReportsApril Joy Sumagit HidalgoNo ratings yet

- Salary and Wages 940,000 Gross Profit 2,600,000 Rent Expense 200,000 Gain On Sale of Building (Note-1) 100,000Document5 pagesSalary and Wages 940,000 Gross Profit 2,600,000 Rent Expense 200,000 Gain On Sale of Building (Note-1) 100,000Samia AkterNo ratings yet

- 6167f0c20cf2c12cd8917628 OriginalDocument34 pages6167f0c20cf2c12cd8917628 OriginalTM GamingNo ratings yet

- Mauritian Taxation - Ba Acctg and FinanceDocument8 pagesMauritian Taxation - Ba Acctg and Financemissyemylia27novNo ratings yet

- (April-19) (MBC-106) Ii Semester Income Tax Law and Practice Time: 3 Hours Max - Marks: 60Document3 pages(April-19) (MBC-106) Ii Semester Income Tax Law and Practice Time: 3 Hours Max - Marks: 60Bhuvaneswari karuturiNo ratings yet

- Final BLT203 SemIV Bcom Spring 2020Document4 pagesFinal BLT203 SemIV Bcom Spring 2020SunnyNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- MS Excel Workshop - B 30Document26 pagesMS Excel Workshop - B 30kalyanikamineniNo ratings yet

- Money Market Instruments (Original Maturity Up To One Year)Document11 pagesMoney Market Instruments (Original Maturity Up To One Year)kalyanikamineniNo ratings yet

- Sec 194 Ic, 194la, 194J (TDS)Document3 pagesSec 194 Ic, 194la, 194J (TDS)kalyanikamineniNo ratings yet

- Consignment Meaning of ConsignmentDocument1 pageConsignment Meaning of ConsignmentkalyanikamineniNo ratings yet

- V'Smart Academy (88883 88886) Chapter 6:standard CostingDocument13 pagesV'Smart Academy (88883 88886) Chapter 6:standard CostingSANTHOSH KUMAR T MNo ratings yet

- Global Superstore DatasetDocument5,701 pagesGlobal Superstore DatasetHaroon FareedNo ratings yet

- Vision - 2Document1 pageVision - 2kalyanikamineniNo ratings yet

- FMS PPT Group5Document22 pagesFMS PPT Group5kalyanikamineniNo ratings yet

- Ifos Part 2Document2 pagesIfos Part 2kalyanikamineniNo ratings yet

- Over SubscriptionDocument3 pagesOver SubscriptionkalyanikamineniNo ratings yet

- Intro To Company AccDocument6 pagesIntro To Company AcckalyanikamineniNo ratings yet

- GAPs Model Survey QuestionsDocument3 pagesGAPs Model Survey QuestionskalyanikamineniNo ratings yet

- Good Will in PatnershipDocument6 pagesGood Will in PatnershipkalyanikamineniNo ratings yet

- As - 9Document1 pageAs - 9kalyanikamineniNo ratings yet

- Auditing BitsDocument48 pagesAuditing BitskalyanikamineniNo ratings yet

- Method 3 of GoodwillDocument3 pagesMethod 3 of GoodwillkalyanikamineniNo ratings yet

- Assesment of Individuals Q-1Document4 pagesAssesment of Individuals Q-1kalyanikamineniNo ratings yet

- SalaryDocument80 pagesSalarykalyanikamineniNo ratings yet

- Agricultural IncomeDocument2 pagesAgricultural IncomekalyanikamineniNo ratings yet

- Bna Article-8Document5 pagesBna Article-8kalyanikamineniNo ratings yet

- C2 - Human Resource Management-Class of 2024 - Trimester IIDocument8 pagesC2 - Human Resource Management-Class of 2024 - Trimester IIkalyanikamineniNo ratings yet

- GAPs Model Survey QuestionsDocument3 pagesGAPs Model Survey QuestionskalyanikamineniNo ratings yet

- Assignment 1 - Probability TheoryDocument2 pagesAssignment 1 - Probability TheorykalyanikamineniNo ratings yet

- Sec 194 IDocument4 pagesSec 194 IkalyanikamineniNo ratings yet

- Edited Auditing BitsDocument48 pagesEdited Auditing BitskalyanikamineniNo ratings yet

- Calls in Arrers ND Calls in AdvanceDocument3 pagesCalls in Arrers ND Calls in AdvancekalyanikamineniNo ratings yet

- Transfer Pricing - 1Document2 pagesTransfer Pricing - 1kalyanikamineniNo ratings yet

- BoS - Session 1Document37 pagesBoS - Session 1kalyanikamineni100% (1)

- Reissue Q-2Document4 pagesReissue Q-2kalyanikamineniNo ratings yet

- PDF Manuel Dx27instructions Minicap Flex CompressDocument91 pagesPDF Manuel Dx27instructions Minicap Flex CompressShoaib AhmedNo ratings yet

- Tutorial Letter 201/1/2020: Financial Accounting Principles For Law PractitionersDocument6 pagesTutorial Letter 201/1/2020: Financial Accounting Principles For Law Practitionersall green associates100% (1)

- MONTHLYDocument2 pagesMONTHLYBoulos NassarNo ratings yet

- Pro Forma Balance Sheet Template: Company NameDocument5 pagesPro Forma Balance Sheet Template: Company NamePhương ĐinhNo ratings yet

- Adjusting Entries: Prepaid Expenses (Its An Assets)Document3 pagesAdjusting Entries: Prepaid Expenses (Its An Assets)Hira SialNo ratings yet

- State Bank of Patiala Balance Sheet Department Welcomes Participants To SeminarDocument19 pagesState Bank of Patiala Balance Sheet Department Welcomes Participants To SeminarKunal ParmarNo ratings yet

- Feasibility EvaluationDocument1 pageFeasibility EvaluationRuby De GranoNo ratings yet

- Chapter 4Document28 pagesChapter 4Nhi Phan TúNo ratings yet

- Regular Income Tax: Bacc8 TaxationDocument18 pagesRegular Income Tax: Bacc8 TaxationsoonsNo ratings yet

- RMC No. 46-2021Document1 pageRMC No. 46-2021Joel SyNo ratings yet

- Toaz - Info Tata Consultancy Services Payslip PRDocument2 pagesToaz - Info Tata Consultancy Services Payslip PRRLP TECHNOLOGYNo ratings yet

- Chapter 3: Introduction To Income TaxationDocument15 pagesChapter 3: Introduction To Income TaxationRover RossNo ratings yet

- Income Tax - Guidelines Financial Year 2022-23Document13 pagesIncome Tax - Guidelines Financial Year 2022-23Pradeep KVKNo ratings yet

- Annex ' F '' Certification: Taxpayer Identification Number Amount of Compensation Tax Due Withheld and RemittedDocument4 pagesAnnex ' F '' Certification: Taxpayer Identification Number Amount of Compensation Tax Due Withheld and Remittedivs accountingNo ratings yet

- Solution Test 2 (1) June 19Document5 pagesSolution Test 2 (1) June 19Nur Dina AbsbNo ratings yet

- Activity - Estate Tax ComputationDocument2 pagesActivity - Estate Tax ComputationEki SunriseNo ratings yet

- Exempt Organization Business Income Tax Return 990-T: (And Proxy Tax Under Section 6033 (E) )Document13 pagesExempt Organization Business Income Tax Return 990-T: (And Proxy Tax Under Section 6033 (E) )greenwellNo ratings yet

- E34Document9 pagesE34Nguyen Nguyen KhoiNo ratings yet

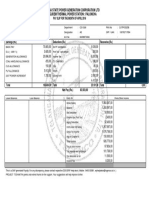

- Telangana State Power Generation Corporation LTD Kothagudem Thermal Power Station: PalonchaDocument1 pageTelangana State Power Generation Corporation LTD Kothagudem Thermal Power Station: PalonchaKANNE NITHINNo ratings yet

- Tax 70%Document19 pagesTax 70%Akshat ShahNo ratings yet

- Chick-Fil-A 2009 Tax RecordsDocument57 pagesChick-Fil-A 2009 Tax RecordsSergio Nahuel CandidoNo ratings yet

- Direct and Indirect TaxDocument12 pagesDirect and Indirect TaxSresth VermaNo ratings yet

- Central Investigation & Security Services LTD Mumbai QuotationDocument2 pagesCentral Investigation & Security Services LTD Mumbai QuotationPradeep PanigrahiNo ratings yet

- Draft: The Return Should Reach Mra Electronicallt at Latest On 15 October 2021Document7 pagesDraft: The Return Should Reach Mra Electronicallt at Latest On 15 October 2021DstormNo ratings yet

- TCSDocument23 pagesTCSSatyendra13kumarNo ratings yet

- Module 3 Income Tax On IndividualsDocument77 pagesModule 3 Income Tax On IndividualsAriza CastroverdeNo ratings yet

- I Nvoi Ce: Law Office of Aviral AsthanaDocument1 pageI Nvoi Ce: Law Office of Aviral AsthanaAviral AsthanaNo ratings yet

- Airfreight 2100, Inc.Document2 pagesAirfreight 2100, Inc.ben carlo ramos srNo ratings yet