You might also like

- Investment in Debt SecuritiesDocument29 pagesInvestment in Debt SecuritiesDjunah ArellanoNo ratings yet

- I. Financial Assets - FVPLDocument17 pagesI. Financial Assets - FVPLShane Aberie Villaroza AmidaNo ratings yet

- P7 - Investment in Debt Securities & Other Non-Current Financial AssetsDocument46 pagesP7 - Investment in Debt Securities & Other Non-Current Financial AssetsNashiel AnneNo ratings yet

- Investment in Equity AnnotatedDocument8 pagesInvestment in Equity AnnotatedLloydNo ratings yet

- Bond Investment - FVOCI: Subject Intermediate Accounting Teacher Dessa Dianna MadridDocument23 pagesBond Investment - FVOCI: Subject Intermediate Accounting Teacher Dessa Dianna MadridJohn Warren MestiolaNo ratings yet

- Debt-Securities-Reclassification 2Document13 pagesDebt-Securities-Reclassification 2TrixieNo ratings yet

- #14 Investments in Debt InstrumentsDocument5 pages#14 Investments in Debt InstrumentsMakoy Bixenman100% (1)

- Preparation of Separate Financial StatementsDocument29 pagesPreparation of Separate Financial StatementschingNo ratings yet

- Crash Landing On You Company Financial StatementsDocument6 pagesCrash Landing On You Company Financial StatementsEmar KimNo ratings yet

- VALUING SYNERGIES IN M&A-Data Revised Jan 2020Document7 pagesVALUING SYNERGIES IN M&A-Data Revised Jan 2020Aninda Dutta100% (1)

- 21 Problems - and - Answers - Reclassification - of - Financial - AssetDocument30 pages21 Problems - and - Answers - Reclassification - of - Financial - AssetSheila Grace BajaNo ratings yet

- Basic 6 Treasury AccountingDocument25 pagesBasic 6 Treasury AccountingShailjaNo ratings yet

- Financial Assets at Fair Value CH 15Document14 pagesFinancial Assets at Fair Value CH 15Cheska AgrabioNo ratings yet

- CH 17 InvestmentsDocument18 pagesCH 17 InvestmentsAbdi hasenNo ratings yet

- Microsoft Word - FAR01 - Accounting For Equity InvestmentsDocument4 pagesMicrosoft Word - FAR01 - Accounting For Equity InvestmentsDisguised owlNo ratings yet

- Non Financial Liabilities Provision and Contingencies.v2Document44 pagesNon Financial Liabilities Provision and Contingencies.v2Angelica Mingaracal RosarioNo ratings yet

- FA@FV and AC. Initial Subsequent Measurement. ReclassificationDocument4 pagesFA@FV and AC. Initial Subsequent Measurement. ReclassificationMiccah Jade CastilloNo ratings yet

- Week 06 2022 Topic 6 Lecture Financial Instruments Part BDocument15 pagesWeek 06 2022 Topic 6 Lecture Financial Instruments Part BErnest LeongNo ratings yet

- Module Far1 Unit-1 Part-1c.4Document2 pagesModule Far1 Unit-1 Part-1c.4KezNo ratings yet

- Financial Statements of Companies - DPP 01 II Udesh Fastrack Accounting (Group 1)Document8 pagesFinancial Statements of Companies - DPP 01 II Udesh Fastrack Accounting (Group 1)ajay singhNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument7 pages© The Institute of Chartered Accountants of IndiaSarvesh JoshiNo ratings yet

- 21NDocument22 pages21NWinnie GNo ratings yet

- Required: Prepare Entries For Year 1 and 2 in The Books of Victoria CorporationDocument9 pagesRequired: Prepare Entries For Year 1 and 2 in The Books of Victoria CorporationJennica CruzadoNo ratings yet

- Solution of Past PaperDocument17 pagesSolution of Past Papermishal zikriaNo ratings yet

- Kin Pang Holdings Limited 建 鵬 控 股 有 限 公 司: Audited Annual Results Announcement For The Year Ended 31 December 2021Document37 pagesKin Pang Holdings Limited 建 鵬 控 股 有 限 公 司: Audited Annual Results Announcement For The Year Ended 31 December 2021ALNo ratings yet

- IN Financial Management 1: Leyte CollegesDocument20 pagesIN Financial Management 1: Leyte CollegesJeric LepasanaNo ratings yet

- Activity 2 SCIDocument2 pagesActivity 2 SCIAshley BabiaNo ratings yet

- Ch7 Problems SolutionDocument22 pagesCh7 Problems Solutionwong100% (8)

- SolMan Chapter 4 (Partial)Document9 pagesSolMan Chapter 4 (Partial)zaounxosakubNo ratings yet

- Test 2023Document12 pagesTest 2023paingheinkhanttNo ratings yet

- UntitledDocument176 pagesUntitledPriya NairNo ratings yet

- AP-LIABS-3 (With Answers)Document4 pagesAP-LIABS-3 (With Answers)Kendrew SujideNo ratings yet

- AFD Practice Questions Mock (3399)Document7 pagesAFD Practice Questions Mock (3399)AbhiNo ratings yet

- Chương 3Document22 pagesChương 3Mai Duong ThiNo ratings yet

- Advanced Financial Management - Finals-11Document2 pagesAdvanced Financial Management - Finals-11graalNo ratings yet

- T7 - Long-Lived AssetsDocument42 pagesT7 - Long-Lived AssetsJhonatan Perez VillanuevaNo ratings yet

- Basel Disclosure Ashad2080Document4 pagesBasel Disclosure Ashad2080Na Bee NaNo ratings yet

- Putting IFRS 9 Into Practice Presentation By: CPA Stephen Obock February 2018Document38 pagesPutting IFRS 9 Into Practice Presentation By: CPA Stephen Obock February 2018syed younasNo ratings yet

- Chapter 2 - Statement of Comprehensive Income - UnlockedDocument2 pagesChapter 2 - Statement of Comprehensive Income - UnlockedJerome_JadeNo ratings yet

- Chapter 12 Assigned Question SOLUTIONSDocument61 pagesChapter 12 Assigned Question SOLUTIONSDang ThanhNo ratings yet

- Financial Report - EditedDocument7 pagesFinancial Report - EditedMaina PeterNo ratings yet

- Joaxjill NotesDocument6 pagesJoaxjill NotesAlliah Czyrielle Amorado PersinculaNo ratings yet

- Quiz I. Problem Solving: Property of STIDocument2 pagesQuiz I. Problem Solving: Property of STIarisuNo ratings yet

- Cash Flow: AssumptionsDocument3 pagesCash Flow: AssumptionsSudhanshu Kumar SinghNo ratings yet

- Group AssignmentDocument6 pagesGroup AssignmentIshiyaku Adamu NjiddaNo ratings yet

- Fourth Quarter 2009 Financial ResultsDocument26 pagesFourth Quarter 2009 Financial ResultsZerohedgeNo ratings yet

- Case 1Document4 pagesCase 1Roger BartelsNo ratings yet

- Wa0035.Document5 pagesWa0035.Barack MikeNo ratings yet

- SBR Mock1 As - s20 j21Document14 pagesSBR Mock1 As - s20 j21percy mapetereNo ratings yet

- Investment in Debt SecuritiesDocument9 pagesInvestment in Debt SecuritiesKimivy BusaNo ratings yet

- Solution - (Ust-Jpia) Ca51016 Ia3 Mock Preliminary Examination ReviewerDocument11 pagesSolution - (Ust-Jpia) Ca51016 Ia3 Mock Preliminary Examination Reviewerhpp academicmaterialsNo ratings yet

- 0315富邦年報 - 英文.indd 1 2021/5/17 下午 02:54:09Document32 pages0315富邦年報 - 英文.indd 1 2021/5/17 下午 02:54:09YudyChenNo ratings yet

- Notes To and Forming Part of The Financial StatementsDocument7 pagesNotes To and Forming Part of The Financial StatementsMBAM2292No ratings yet

- Shareholders EquityDocument6 pagesShareholders Equity1701791No ratings yet

- Audit of Investments AnnotatedDocument8 pagesAudit of Investments AnnotatedLloydNo ratings yet

- Investment Quizzers Investment QuizzersDocument16 pagesInvestment Quizzers Investment QuizzersAnna Taylor0% (1)

- Fin2001 Pset4Document10 pagesFin2001 Pset4Valeria MartinezNo ratings yet

- Ativision Blizzard Inc Valuation - Final WorkDocument24 pagesAtivision Blizzard Inc Valuation - Final WorkMichael Andres Gamarra TorresNo ratings yet

- Assignment #2 Investment & Portfolio Management Group 3 (GEN) (G1)Document3 pagesAssignment #2 Investment & Portfolio Management Group 3 (GEN) (G1)ramyNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Internal ControlDocument4 pagesInternal ControlLloydNo ratings yet

- Equity (Annotated)Document19 pagesEquity (Annotated)LloydNo ratings yet

- Audit of Investments AnnotatedDocument8 pagesAudit of Investments AnnotatedLloydNo ratings yet

- Audit of InvestmentsDocument4 pagesAudit of InvestmentsLloydNo ratings yet

- Audit of PPE AnnotatedDocument10 pagesAudit of PPE AnnotatedLloydNo ratings yet

- Audit Planning (Annotated)Document6 pagesAudit Planning (Annotated)LloydNo ratings yet

- HOBA AnnotatedDocument13 pagesHOBA AnnotatedLloydNo ratings yet

- 06 Consolidation AnnotatedDocument18 pages06 Consolidation AnnotatedLloydNo ratings yet

- 05 - Business CombinationsDocument3 pages05 - Business CombinationsLloydNo ratings yet

- 06 - PpeDocument4 pages06 - PpeLloydNo ratings yet

- Intangible Assets AnnotatedDocument9 pagesIntangible Assets AnnotatedLloydNo ratings yet

- Bicol College, IncDocument17 pagesBicol College, IncLloydNo ratings yet

- Wasting Assets AnnotatedDocument3 pagesWasting Assets AnnotatedLloydNo ratings yet

- Manuscript Pa Hard BoundDocument99 pagesManuscript Pa Hard BoundLloydNo ratings yet

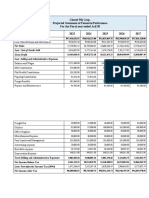

- Glazed Pili Corp. Projected Statement of Financial Performnce For The Fiscal Year Ended Aril 30 2023 2024 2025 2026 2027Document11 pagesGlazed Pili Corp. Projected Statement of Financial Performnce For The Fiscal Year Ended Aril 30 2023 2024 2025 2026 2027LloydNo ratings yet

- List of TablesDocument1 pageList of TablesLloydNo ratings yet

- List of Tables, Figures & GraphsDocument2 pagesList of Tables, Figures & GraphsLloydNo ratings yet

- Verilog Code For Traffic Light Control Using FSMDocument7 pagesVerilog Code For Traffic Light Control Using FSMEr Pradip PatelNo ratings yet

- Fundamental of HDD Technology (3) : OutlineDocument8 pagesFundamental of HDD Technology (3) : OutlineJoseMNo ratings yet

- Sop Welder TigDocument2 pagesSop Welder TigShahid RazaNo ratings yet

- Clinical Assignment 1Document5 pagesClinical Assignment 1Muhammad Noman bin FiazNo ratings yet

- NDA Report No DSSC-452-01 - Geological Disposal - Engineered Barrier System Status ReportDocument146 pagesNDA Report No DSSC-452-01 - Geological Disposal - Engineered Barrier System Status ReportVincent LinNo ratings yet

- Microsoft Power Platform Adoption PlanningDocument84 pagesMicrosoft Power Platform Adoption PlanningcursurilemeleNo ratings yet

- LCOE CHILE Ene - 11052401aDocument23 pagesLCOE CHILE Ene - 11052401aLenin AgrinzoneNo ratings yet

- 7diesel 2016Document118 pages7diesel 2016JoãoCarlosDaSilvaBrancoNo ratings yet

- Health Tech Industry Accounting Guide 2023Document104 pagesHealth Tech Industry Accounting Guide 2023sabrinaNo ratings yet

- CF34-10E LM June 09 Print PDFDocument301 pagesCF34-10E LM June 09 Print PDFPiipe780% (5)

- UNIT V WearableDocument102 pagesUNIT V WearableajithaNo ratings yet

- LFT - Development Status and Perspectives: Prof. DR Michael SchemmeDocument7 pagesLFT - Development Status and Perspectives: Prof. DR Michael SchemmeabiliovieiraNo ratings yet

- Define Technical Settings For All Involved Systems: PrerequisitesDocument2 pagesDefine Technical Settings For All Involved Systems: PrerequisitesGK SKNo ratings yet

- DWC Ordering InformationDocument15 pagesDWC Ordering InformationbalaNo ratings yet

- Vanderbeck Solman ch01-10Document156 pagesVanderbeck Solman ch01-10Jelly AceNo ratings yet

- VDO Gauge - VL Hourmeter 12 - 24Document2 pagesVDO Gauge - VL Hourmeter 12 - 24HanNo ratings yet

- ValuenetAnewbusinessmodelforthefoodindustry PDFDocument23 pagesValuenetAnewbusinessmodelforthefoodindustry PDFneera mailNo ratings yet

- MCD2000CM4 T1 014 (8 7 12) - CompleteDocument1,062 pagesMCD2000CM4 T1 014 (8 7 12) - CompletePablo Marchant TorresNo ratings yet

- Problem 4. Markov Chains (Initial State Multiplication)Document7 pagesProblem 4. Markov Chains (Initial State Multiplication)Karina Salazar NuñezNo ratings yet

- List of Circulating Currencies by CountryDocument8 pagesList of Circulating Currencies by CountryVivek SinghNo ratings yet

- Business Models, Institutional Change, and Identity Shifts in Indian Automobile IndustryDocument26 pagesBusiness Models, Institutional Change, and Identity Shifts in Indian Automobile IndustryGowri J BabuNo ratings yet

- Cenomar Request PSA Form-NewDocument1 pageCenomar Request PSA Form-NewUpuang KahoyNo ratings yet

- Crime MappingDocument13 pagesCrime MappingRea Claire QuimnoNo ratings yet

- Golden Field Farmers Multi-Purpose Cooperative: Palay ProductionDocument3 pagesGolden Field Farmers Multi-Purpose Cooperative: Palay ProductionAps BautistaNo ratings yet

- Maluno Integrated School: Action Plan On Wins ProgramDocument1 pageMaluno Integrated School: Action Plan On Wins ProgramSherlymae Alejandro Avelino100% (2)

- Misuse of InternetDocument22 pagesMisuse of InternetPushparaj100% (1)

- ADM2341 CH 8 Capstone QDocument2 pagesADM2341 CH 8 Capstone QjuiceNo ratings yet

- 6 - Designing Manufacturing Processes - Hill - Product ProfilingDocument20 pages6 - Designing Manufacturing Processes - Hill - Product ProfilingLalit S KathpaliaNo ratings yet

- Con Law Koppelman HugeDocument203 pagesCon Law Koppelman HugemrstudynowNo ratings yet

- Growth of Luxury Market & Products in IndiaDocument60 pagesGrowth of Luxury Market & Products in IndiaMohammed Yunus100% (2)