You might also like

- Carbon Capture, Utilization, and Storage Game Changers in Asia and the Pacific: 2022 Compendium of Technologies and EnablersFrom EverandCarbon Capture, Utilization, and Storage Game Changers in Asia and the Pacific: 2022 Compendium of Technologies and EnablersNo ratings yet

- IA 1 Valix 2020 Ver. Problem 28Document6 pagesIA 1 Valix 2020 Ver. Problem 28Ariean Joy DequiñaNo ratings yet

- Universal Company mining journal entries 2020-2022Document2 pagesUniversal Company mining journal entries 2020-2022Jerbert JesalvaNo ratings yet

- Module 8Document6 pagesModule 8Althea mary kate MorenoNo ratings yet

- A2 Natural ResourcesDocument2 pagesA2 Natural ResourcesPasaoa Clarice V.No ratings yet

- Asset Depreciation and Revaluation ReportDocument10 pagesAsset Depreciation and Revaluation ReportAaliyah ManuelNo ratings yet

- Casey Sarah R. Erato Block D: Amount Paid For The Property AcquiredDocument3 pagesCasey Sarah R. Erato Block D: Amount Paid For The Property AcquiredJerbert JesalvaNo ratings yet

- Report EconomicoDocument10 pagesReport EconomicoMartin Torres RuedaNo ratings yet

- Cost production reportsDocument26 pagesCost production reportsEi HmmmNo ratings yet

- Depletion PDFDocument3 pagesDepletion PDFAlexly Gift UntalanNo ratings yet

- Khadi & Village Industries Commission Project Profile For Gramodyog Rozgar Yojana Handmade Paper Conversion UnitDocument2 pagesKhadi & Village Industries Commission Project Profile For Gramodyog Rozgar Yojana Handmade Paper Conversion UnitAKvermaNo ratings yet

- Group2 PPEDocument2 pagesGroup2 PPELeane MarcoletaNo ratings yet

- Anugerah E11. 18-19 Anugerah AldiDocument2 pagesAnugerah E11. 18-19 Anugerah AldiAnugerah AldiNo ratings yet

- Resource Company Required Debit Credit 2020 Rock and Gravel PropertyDocument10 pagesResource Company Required Debit Credit 2020 Rock and Gravel PropertyAnonnNo ratings yet

- ACCT 4410 Depreciation Allowance Illustration (DA) (2023S)Document2 pagesACCT 4410 Depreciation Allowance Illustration (DA) (2023S)何健珩No ratings yet

- PA1 Group1 P10Document8 pagesPA1 Group1 P10Phuong Nguyen MinhNo ratings yet

- Solution 34-6 Answer CDocument1 pageSolution 34-6 Answer CChammy TeyNo ratings yet

- Lec04 SolutionDocument12 pagesLec04 SolutionedrianclydeNo ratings yet

- Chapter 17 - Depletion of Mineral ResourcesDocument3 pagesChapter 17 - Depletion of Mineral ResourcesXiena50% (2)

- Financial Accounting Reviewer - Chapter 58Document13 pagesFinancial Accounting Reviewer - Chapter 58Coursehero PremiumNo ratings yet

- PA1 Group1 Week8Document8 pagesPA1 Group1 Week8Phuong Nguyen MinhNo ratings yet

- RevaluationDocument3 pagesRevaluationJerbert JesalvaNo ratings yet

- Pengakun CH 09Document10 pagesPengakun CH 09nadia salsabilaNo ratings yet

- D10 Spring2010Document7 pagesD10 Spring2010meelas123No ratings yet

- Guide to Non-Current Asset AccountingDocument3 pagesGuide to Non-Current Asset Accountingshera haniNo ratings yet

- Production of Oxalic AcidDocument2 pagesProduction of Oxalic AcidnoviNo ratings yet

- Depletion: Problem 34-1 (IFRS)Document20 pagesDepletion: Problem 34-1 (IFRS)수지100% (8)

- Total Cost of Natural Resource: Depletion 250,000Document3 pagesTotal Cost of Natural Resource: Depletion 250,000Fenladen AmbayNo ratings yet

- REVALUATION MODEL SantosDocument20 pagesREVALUATION MODEL SantosStefany M. SantosNo ratings yet

- BudgetDocument7 pagesBudgetvasanthgurusamynsNo ratings yet

- Sol. Man. - Chapter 17 - Depletion of Mineral Resources - Ia Part 1B 1Document6 pagesSol. Man. - Chapter 17 - Depletion of Mineral Resources - Ia Part 1B 1Rezzan Joy Camara Mejia67% (6)

- 108A W23++Homework+8Document8 pages108A W23++Homework+8Julius SuhermanNo ratings yet

- Airline pricing considerations beyond costDocument10 pagesAirline pricing considerations beyond costZoeNo ratings yet

- Unit of production depreciation (manufacuring)Document14 pagesUnit of production depreciation (manufacuring)lpetjaNo ratings yet

- ACC107 MOD10&11 IllustrationsDocument8 pagesACC107 MOD10&11 IllustrationsDanah EstilloreNo ratings yet

- T 4Document3 pagesT 4Muntasir AhmmedNo ratings yet

- Property, Plant and Equipment DepreciationDocument13 pagesProperty, Plant and Equipment DepreciationJannelle SalacNo ratings yet

- Answers AdvancedAccounts Full Length 2 280324Document10 pagesAnswers AdvancedAccounts Full Length 2 280324jj4223062003No ratings yet

- Ia3 FinalsDocument4 pagesIa3 FinalsGeraldine MayoNo ratings yet

- Depreciation, impairment, and revaluation calculationsDocument10 pagesDepreciation, impairment, and revaluation calculationsMarjon Godfrey Dojillo CaveNo ratings yet

- Ppe - Intpraa - 03182020 - Part 2Document6 pagesPpe - Intpraa - 03182020 - Part 2Mich ClementeNo ratings yet

- Project Report On General StoreDocument10 pagesProject Report On General StoreApplication's ManagerNo ratings yet

- CMA Garrison SuggestedSolutions Chap2Document12 pagesCMA Garrison SuggestedSolutions Chap2PIYUSH SINGHNo ratings yet

- Diamond CompanyDocument1 pageDiamond CompanyKillua ZOLDYNo ratings yet

- Machine Hour Cost Sheet Mechanical Ventilation BoxDocument10 pagesMachine Hour Cost Sheet Mechanical Ventilation BoxLAURA VANESSA MENDIVELSO SANCHEZNo ratings yet

- Problems DepletionDocument21 pagesProblems DepletionSharmin ReulaNo ratings yet

- QUIZ - CHAPTER 16 - PPE PART 2 - 2020edDocument5 pagesQUIZ - CHAPTER 16 - PPE PART 2 - 2020edjanna napiliNo ratings yet

- Manufacturing of Detergent Powder & CakeDocument2 pagesManufacturing of Detergent Powder & Cakeramu_uppadaNo ratings yet

- Midterms Problems Answer KeyDocument20 pagesMidterms Problems Answer KeyErica Estelle May MagrareNo ratings yet

- Working CapitalDocument2 pagesWorking CapitalPayal bhatiaNo ratings yet

- CFAS - Depreciation Methods - Barcelona, JoyceAnnDocument9 pagesCFAS - Depreciation Methods - Barcelona, JoyceAnnJoyce Ann Agdippa BarcelonaNo ratings yet

- Chapter 17 Depletion of Mineral Resources ProblemsDocument3 pagesChapter 17 Depletion of Mineral Resources ProblemsMahasia MANDIGANNo ratings yet

- PPE Accounting Answers Module 2"TITLE"Property, Plant and Equipment Assessment Answers" TITLE"Module 2 Answer Key on PPE AccountingDocument7 pagesPPE Accounting Answers Module 2"TITLE"Property, Plant and Equipment Assessment Answers" TITLE"Module 2 Answer Key on PPE AccountingLoven BoadoNo ratings yet

- Solution Job Order CostingDocument1 pageSolution Job Order Costingaiza eroyNo ratings yet

- P21-1A Journal Entries for Raw Material, WIP, Factory Overhead, Finished Goods and Cost of Goods SoldDocument8 pagesP21-1A Journal Entries for Raw Material, WIP, Factory Overhead, Finished Goods and Cost of Goods SoldVõ Huỳnh BăngNo ratings yet

- Honey House and Honey Processing Plant IndiaDocument2 pagesHoney House and Honey Processing Plant IndiasedianpoNo ratings yet

- PreviewDocument11 pagesPreviewapi-584609390No ratings yet

- Inventory, Purchases, Sales and Expenses ReportDocument10 pagesInventory, Purchases, Sales and Expenses ReportnovyNo ratings yet

- Economics of Climate Change Mitigation in Central and West AsiaFrom EverandEconomics of Climate Change Mitigation in Central and West AsiaNo ratings yet

- Equity (Annotated)Document19 pagesEquity (Annotated)LloydNo ratings yet

- Audit Planning Risk Assessment (APRADocument6 pagesAudit Planning Risk Assessment (APRALloydNo ratings yet

- Understanding Internal Control and the COSO FrameworkDocument4 pagesUnderstanding Internal Control and the COSO FrameworkLloydNo ratings yet

- Audit of InvestmentsDocument4 pagesAudit of InvestmentsLloydNo ratings yet

- Audit of PPE AnnotatedDocument10 pagesAudit of PPE AnnotatedLloydNo ratings yet

- Audit of Investments AnnotatedDocument8 pagesAudit of Investments AnnotatedLloydNo ratings yet

- Investment in Debt Securities AnnotatedDocument8 pagesInvestment in Debt Securities AnnotatedLloydNo ratings yet

- 05 - Business CombinationsDocument3 pages05 - Business CombinationsLloydNo ratings yet

- Consolidation of Parent and Subsidiary FinancialsDocument18 pagesConsolidation of Parent and Subsidiary FinancialsLloydNo ratings yet

- HOBA AnnotatedDocument13 pagesHOBA AnnotatedLloydNo ratings yet

- 06 - PpeDocument4 pages06 - PpeLloydNo ratings yet

- Intangible Assets AnnotatedDocument9 pagesIntangible Assets AnnotatedLloydNo ratings yet

- Bicol College Compliance Certification Proposal DefenseDocument17 pagesBicol College Compliance Certification Proposal DefenseLloydNo ratings yet

- Manuscript Pa Hard BoundDocument99 pagesManuscript Pa Hard BoundLloydNo ratings yet

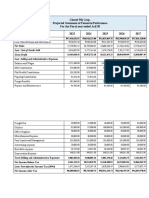

- Glazed Pili Corp. Projected Statement of Financial Performnce For The Fiscal Year Ended Aril 30 2023 2024 2025 2026 2027Document11 pagesGlazed Pili Corp. Projected Statement of Financial Performnce For The Fiscal Year Ended Aril 30 2023 2024 2025 2026 2027LloydNo ratings yet

- List of Tables, Figures & GraphsDocument2 pagesList of Tables, Figures & GraphsLloydNo ratings yet

- List of TablesDocument1 pageList of TablesLloydNo ratings yet

- Argumentative EssayDocument1 pageArgumentative EssaySophia CassandraNo ratings yet

- Test_Ch 2Document4 pagesTest_Ch 2luvkumar3532No ratings yet

- Letter To The Hon David Parker 27.08.2021Document6 pagesLetter To The Hon David Parker 27.08.2021Stuff NewsroomNo ratings yet

- STATCON Prelims Reviewer PDFDocument42 pagesSTATCON Prelims Reviewer PDFLes PaulNo ratings yet

- Riph Unit 4Document6 pagesRiph Unit 4Luna SebastianNo ratings yet

- Final - Published RFQ For UMRAHDocument7 pagesFinal - Published RFQ For UMRAHAndreas KamasahNo ratings yet

- 12 27 2022 The Crusie BEDDocument4 pages12 27 2022 The Crusie BEDDevi KhoirudinNo ratings yet

- Construction Contract Revenue RecognitionDocument2 pagesConstruction Contract Revenue RecognitionDevine Grace A. MaghinayNo ratings yet

- Visit: On The Left Side, On The Right SideDocument31 pagesVisit: On The Left Side, On The Right SideConcept TualNo ratings yet

- Factors Affecting Folk DanceDocument2 pagesFactors Affecting Folk DanceSheryll80% (10)

- BÀI TẬP NGỮ PHÁPDocument5 pagesBÀI TẬP NGỮ PHÁPKhanh Ha NguyenNo ratings yet

- Bangalore University Memorial Challenges Validity of Marriage Reforms OrdinanceDocument32 pagesBangalore University Memorial Challenges Validity of Marriage Reforms OrdinanceAnushka VermaNo ratings yet

- GJERDINGEN - The Future of Legal Scholarship and The Search For A Modern TheorDocument99 pagesGJERDINGEN - The Future of Legal Scholarship and The Search For A Modern TheorFarrah HabibieNo ratings yet

- Gerontologic Nursing 5th Edition Meiner Test BankDocument9 pagesGerontologic Nursing 5th Edition Meiner Test BankJenniferMartinezcgbms100% (12)

- Company Law Project Satyam ScamDocument11 pagesCompany Law Project Satyam ScamAbishek JamesNo ratings yet

- Aznar vs. COMELEC G.R. No. 83820Document2 pagesAznar vs. COMELEC G.R. No. 83820theresaNo ratings yet

- Kami Export - Mon - SSCG3.c-Constitution ReadingDocument3 pagesKami Export - Mon - SSCG3.c-Constitution ReadingMonica RobinsonNo ratings yet

- Senior HR Business Partner in NYC Resume Elizabeth MacKayDocument2 pagesSenior HR Business Partner in NYC Resume Elizabeth MacKayElizabethMacKayNo ratings yet

- Letter No 008 Reply by Authority EngineerDocument8 pagesLetter No 008 Reply by Authority EngineerAbhishek BhandariNo ratings yet

- Duties of An Advocate in Fair TrialDocument7 pagesDuties of An Advocate in Fair TrialAshish pariharNo ratings yet

- Reedy Creek BillDocument189 pagesReedy Creek BillSkyler Swisher100% (1)

- UAE Heritage MSC PROJECTDocument3 pagesUAE Heritage MSC PROJECTPMaliha MohamedNo ratings yet

- Arson PTTXDocument17 pagesArson PTTXMinalin Fire StationNo ratings yet

- Fetalino, Charlote Jennifer N. BS ENTREP 1B Purposive Comunication Comprehension QuestionsDocument2 pagesFetalino, Charlote Jennifer N. BS ENTREP 1B Purposive Comunication Comprehension QuestionsCharlote Jennifer Fetalino100% (3)

- G.R. No. 210975Document12 pagesG.R. No. 210975Ann ChanNo ratings yet

- PREAMBLEDocument3 pagesPREAMBLEGaurav ScribdNo ratings yet

- American Annexation of The PhilippinesDocument22 pagesAmerican Annexation of The PhilippinesCarl Jeremie LingatNo ratings yet

- RDO No. 30 - BinondoDocument201 pagesRDO No. 30 - BinondoBe YoungNo ratings yet

- Mighty CorporationDocument2 pagesMighty CorporationHarold Sargado LascuñaNo ratings yet

- Automated ElectionDocument38 pagesAutomated ElectionLeah MarshallNo ratings yet