You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Audit Planning (Annotated)Document6 pagesAudit Planning (Annotated)LloydNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Audit of InvestmentsDocument4 pagesAudit of InvestmentsLloydNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Internal ControlDocument4 pagesInternal ControlLloydNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Equity (Annotated)Document19 pagesEquity (Annotated)LloydNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Audit of PPE AnnotatedDocument10 pagesAudit of PPE AnnotatedLloydNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Audit of Investments AnnotatedDocument8 pagesAudit of Investments AnnotatedLloydNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- 06 Consolidation AnnotatedDocument18 pages06 Consolidation AnnotatedLloydNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Intangible Assets AnnotatedDocument9 pagesIntangible Assets AnnotatedLloydNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- HOBA AnnotatedDocument13 pagesHOBA AnnotatedLloydNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Investment in Debt Securities AnnotatedDocument8 pagesInvestment in Debt Securities AnnotatedLloydNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- 06 - PpeDocument4 pages06 - PpeLloydNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Wasting Assets AnnotatedDocument3 pagesWasting Assets AnnotatedLloydNo ratings yet

- Manuscript Pa Hard BoundDocument99 pagesManuscript Pa Hard BoundLloydNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Bicol College, IncDocument17 pagesBicol College, IncLloydNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

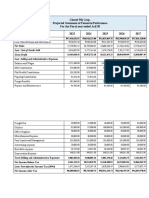

- Glazed Pili Corp. Projected Statement of Financial Performnce For The Fiscal Year Ended Aril 30 2023 2024 2025 2026 2027Document11 pagesGlazed Pili Corp. Projected Statement of Financial Performnce For The Fiscal Year Ended Aril 30 2023 2024 2025 2026 2027LloydNo ratings yet

- Merchant Banking: Financing Their ClientsDocument25 pagesMerchant Banking: Financing Their ClientsAsad MazharNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Cold Email Personalization at Scale - Becc HollandDocument34 pagesCold Email Personalization at Scale - Becc HollandGeorge GuerraNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Chapter 8 - ProblemDocument26 pagesChapter 8 - ProblemMa. Leonor Nikka CuevasNo ratings yet

- Horngrens Accounting Global Edition 10Th Edition Nobles Test Bank Full Chapter PDFDocument67 pagesHorngrens Accounting Global Edition 10Th Edition Nobles Test Bank Full Chapter PDFsaturnagamivphdh100% (9)

- GiftsDocument14 pagesGiftsJeon WonwooNo ratings yet

- Arthur - D. Little - & - UITP - Future - of - Mobility - 3 - Study - Compressed - PDFDocument100 pagesArthur - D. Little - & - UITP - Future - of - Mobility - 3 - Study - Compressed - PDFCarlos TondokNo ratings yet

- Test On Opportunity CostDocument1 pageTest On Opportunity CostTao RNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Job Analysis AssignmentDocument9 pagesJob Analysis AssignmentHazem AminNo ratings yet

- Covenant University Convocation List 2019 2020Document78 pagesCovenant University Convocation List 2019 2020CheckNo ratings yet

- Summarize The Concept of Consumer Learning PDFDocument18 pagesSummarize The Concept of Consumer Learning PDFPratipal SinghNo ratings yet

- Usa Facebook GroupDocument63 pagesUsa Facebook GroupSaad RabbiNo ratings yet

- ROI in Agile Transformation: Using Design Thinking To Deliver and Measure ResultsDocument46 pagesROI in Agile Transformation: Using Design Thinking To Deliver and Measure ResultsNeilFaverNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Understanding The Marketplace and ConsumersDocument15 pagesUnderstanding The Marketplace and ConsumersCatherine Mae MacailaoNo ratings yet

- PRTC - PREWEEK - NOTES - IN - TAXATION - MAY - 2022Document30 pagesPRTC - PREWEEK - NOTES - IN - TAXATION - MAY - 2022One DozenNo ratings yet

- Wolford EDM511 Case 4Document10 pagesWolford EDM511 Case 4geraldwolford1No ratings yet

- Colgate Max Fresh Global Brand Roll Out Case AnalysisDocument3 pagesColgate Max Fresh Global Brand Roll Out Case Analysiskartik singhNo ratings yet

- Green It Nutanix BrewtanixDocument12 pagesGreen It Nutanix BrewtanixGuillaume Soubielle0% (1)

- Budgeting (Refer To Chapter 9 of Hilton Text)Document3 pagesBudgeting (Refer To Chapter 9 of Hilton Text)ShiTheng Love UNo ratings yet

- MBA Finance Project On Credit Schemes of State Bank of India (SBI) and Other Banks in IndiaDocument13 pagesMBA Finance Project On Credit Schemes of State Bank of India (SBI) and Other Banks in IndiaDiwakar BandarlaNo ratings yet

- Deloitte GTCE VAT Refund Guide 2022Document164 pagesDeloitte GTCE VAT Refund Guide 2022Ali AyubNo ratings yet

- Partnership Deed - Parampara Engineering ServicesDocument7 pagesPartnership Deed - Parampara Engineering Servicesvijay basiyaNo ratings yet

- Assignment Business Strategy Change - Submission Date 10 Oct 2020 PDFDocument3 pagesAssignment Business Strategy Change - Submission Date 10 Oct 2020 PDFnat1asha-1No ratings yet

- Nihal SopDocument2 pagesNihal SopGopika GopakumarNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- A Review of Tools For Project Financial AssessmentDocument8 pagesA Review of Tools For Project Financial AssessmentSasha KingNo ratings yet

- This PDF by Stockmock - in Is For Personal Use Only. Do Not Share With OthersDocument4 pagesThis PDF by Stockmock - in Is For Personal Use Only. Do Not Share With OthersPdffNo ratings yet

- Entrepreneurship Ch.1Document39 pagesEntrepreneurship Ch.1Joseph Kinfe100% (1)

- SM7 Ch08 ProcessDocument6 pagesSM7 Ch08 ProcessMohammad FarazNo ratings yet

- PGP Course Outline CB OMK 2017Document10 pagesPGP Course Outline CB OMK 2017Aravind ParanthamanNo ratings yet

- IS4228 Lecture 1 Fall 2021Document43 pagesIS4228 Lecture 1 Fall 2021dgfsdfgsdfgsdfgNo ratings yet

- Chapter - 1: Introduction of Financial AccountingDocument21 pagesChapter - 1: Introduction of Financial AccountingMuhammad AdnanNo ratings yet

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet