You might also like

- Is 40,000. Year Is 20,000 Year Is 5,000. Depreciation For The Year Is 3,000. Use of The Equipment Is Transferred To The Branch P10,000Document5 pagesIs 40,000. Year Is 20,000 Year Is 5,000. Depreciation For The Year Is 3,000. Use of The Equipment Is Transferred To The Branch P10,000Justine CruzNo ratings yet

- Home Office and Branch AccountingDocument2 pagesHome Office and Branch AccountingMae TndnNo ratings yet

- Agency and Branch Accounting Journal EntriesDocument9 pagesAgency and Branch Accounting Journal EntriesAnna TaylorNo ratings yet

- ExerciseDocument4 pagesExerciseMae RxNo ratings yet

- Ibro Answer 1Document4 pagesIbro Answer 1Abdi Mucee TubeNo ratings yet

- Home and Branch Part 1Document4 pagesHome and Branch Part 1Jessica Libunao100% (1)

- HOBA - SeatworkDocument2 pagesHOBA - Seatworkahyenn cabelloNo ratings yet

- HOBADocument9 pagesHOBAJulie Mae Caling MalitNo ratings yet

- Material 11Document6 pagesMaterial 11alyssa100% (1)

- Billed price calculations for home office and branch shipmentsDocument4 pagesBilled price calculations for home office and branch shipmentsJohnmichael Coroza0% (1)

- Document 1 Hoem BranchDocument38 pagesDocument 1 Hoem BranchNadi HoodNo ratings yet

- AFAR2 - Sales Agency, H.O., & Branch AccountingDocument18 pagesAFAR2 - Sales Agency, H.O., & Branch AccountingVon Andrei MedinaNo ratings yet

- Name: Jean Rose T. Bustamante Bsma-3: Let's CheckDocument10 pagesName: Jean Rose T. Bustamante Bsma-3: Let's CheckJean Rose Tabagay BustamanteNo ratings yet

- Chapter 9 Exercises SolutionsDocument21 pagesChapter 9 Exercises SolutionsErra PeñafloridaNo ratings yet

- Practical Accounting Problems II SolutionsDocument9 pagesPractical Accounting Problems II SolutionsEunice BernalNo ratings yet

- Advanced Accounting Home Office, Branch and Agency TransactionsDocument7 pagesAdvanced Accounting Home Office, Branch and Agency TransactionsMajoy Bantoc100% (1)

- Home Office and Branch Accounting H2Document3 pagesHome Office and Branch Accounting H2Nye NyeNo ratings yet

- Module 3 - Home Office Brancg Acctg Part 1Document13 pagesModule 3 - Home Office Brancg Acctg Part 1May P. Huit100% (1)

- Home Office and Branch Accounting ProceduresDocument24 pagesHome Office and Branch Accounting ProceduresFrances Chariz YbioNo ratings yet

- BADVAC1X - MOD 6 TemplatesDocument16 pagesBADVAC1X - MOD 6 TemplatesDarius DelacruzNo ratings yet

- Home Office and Branch Accounting: Trial Balances, Adjustments, and Financial StatementsDocument4 pagesHome Office and Branch Accounting: Trial Balances, Adjustments, and Financial StatementsMaurice AgbayaniNo ratings yet

- Advanced Accounting Part II Quiz 1 Home Office and Branch AccountingDocument10 pagesAdvanced Accounting Part II Quiz 1 Home Office and Branch AccountingAzyrah Lyren Seguban UlpindoNo ratings yet

- Activity 1Document4 pagesActivity 1Fernando III PerezNo ratings yet

- AFAR2 - Sales Agency, H.O., & Branch AccountingDocument12 pagesAFAR2 - Sales Agency, H.O., & Branch AccountingjajajaredredNo ratings yet

- Combined Profit of Home Office and BranchDocument59 pagesCombined Profit of Home Office and BranchAllecks Juel LuchanaNo ratings yet

- Home Office and Branch Accounting: RequiredDocument6 pagesHome Office and Branch Accounting: RequiredLewell PaoloNo ratings yet

- Trial Balance Home Office DR (CR) Branch Office DR (CR)Document2 pagesTrial Balance Home Office DR (CR) Branch Office DR (CR)Adriana CarinanNo ratings yet

- Home Office and Branch AccountingDocument6 pagesHome Office and Branch AccountingJasmine LimNo ratings yet

- OLF Fatima University Partnership Formation GuideDocument3 pagesOLF Fatima University Partnership Formation GuideSky RamirezNo ratings yet

- Vergil Joseph I. Literal, DBA, CPA: Page 1 of 3Document3 pagesVergil Joseph I. Literal, DBA, CPA: Page 1 of 3hsjhsNo ratings yet

- M2 - Home Office and Branch Accounting - Specific ProceduresDocument15 pagesM2 - Home Office and Branch Accounting - Specific ProceduresJohn Michael A. PaclibareNo ratings yet

- Problem #1: Adjusting EntriesDocument5 pagesProblem #1: Adjusting EntriesShahzad AsifNo ratings yet

- Test Bank Paccounting Information Systems Test Bank Paccounting Information SystemsDocument23 pagesTest Bank Paccounting Information Systems Test Bank Paccounting Information SystemsFrylle Kanz Harani PocsonNo ratings yet

- Agency and Branch Accounting - General Procedures - v.2.0Document3 pagesAgency and Branch Accounting - General Procedures - v.2.0Catherine SelladoNo ratings yet

- Question 2 CashFlowDocument6 pagesQuestion 2 CashFlowsuraj lamaNo ratings yet

- Partnership FormationDocument13 pagesPartnership FormationPhilip Dan Jayson LarozaNo ratings yet

- P2 Branch Accounting M2020Document6 pagesP2 Branch Accounting M2020Charla SuanNo ratings yet

- Accounting For Decentralized Operations: Inventory at Cost of P40,000Document6 pagesAccounting For Decentralized Operations: Inventory at Cost of P40,000Nicole Allyson AguantaNo ratings yet

- Excercises On Branch and Home Office Chapter TwoDocument3 pagesExcercises On Branch and Home Office Chapter Twoሔርሞን ይድነቃቸው50% (4)

- Home Office and Branch AccountingDocument12 pagesHome Office and Branch AccountingKrizia Mae FloresNo ratings yet

- Hoba AcctgDocument5 pagesHoba Acctgfer maNo ratings yet

- Lesson 1 Home Office and Branch AccountingDocument4 pagesLesson 1 Home Office and Branch AccountingAndy Lalu100% (3)

- Instructions: Place The Letter Corresponding To Your Answers On The Box Provided BelowDocument3 pagesInstructions: Place The Letter Corresponding To Your Answers On The Box Provided Belowgazer beamNo ratings yet

- Account For Home Office and Branch Transactions. ProblemDocument2 pagesAccount For Home Office and Branch Transactions. ProblemDevine Grace A. MaghinayNo ratings yet

- Corporate Liquidation (Integration) PDFDocument5 pagesCorporate Liquidation (Integration) PDFCatherine Simeon100% (1)

- ECU TOPIC ONE BranchesDocument7 pagesECU TOPIC ONE BranchesPinky RoseNo ratings yet

- AuditDocument4 pagesAuditRoxanneNo ratings yet

- Closing and Post-Closing EntriesDocument13 pagesClosing and Post-Closing EntriesBrian Reyes GangcaNo ratings yet

- Corporate Liquidation Home Office and Branch Accounting ProblemsDocument5 pagesCorporate Liquidation Home Office and Branch Accounting ProblemsJustine CruzNo ratings yet

- ABC - Exercises (Answer Key 1)Document5 pagesABC - Exercises (Answer Key 1)Crystal ApinesNo ratings yet

- AFAR - 2.0 5.0 - Corp Liq and Hob - ASSESSMENTDocument5 pagesAFAR - 2.0 5.0 - Corp Liq and Hob - ASSESSMENTMakisa YuNo ratings yet

- Quiz 2 Kean TisonDocument7 pagesQuiz 2 Kean TisonMr. HahhaNo ratings yet

- Intermediate Accounting 3 Second Grading Quiz: Name: Date: Professor: Section: ScoreDocument2 pagesIntermediate Accounting 3 Second Grading Quiz: Name: Date: Professor: Section: ScoreGrezel NiceNo ratings yet

- Questions On ALOBIDocument3 pagesQuestions On ALOBIALIX V. LIMNo ratings yet

- Advanced Accounting (ACT 410)Document58 pagesAdvanced Accounting (ACT 410)Amr Amr Adel Ahmed MaamounNo ratings yet

- Advanced Accounting 2:: Home Office, Branch and Agency - General ProceduresDocument37 pagesAdvanced Accounting 2:: Home Office, Branch and Agency - General ProceduresIzzy B94% (16)

- Internal Control of Fixed Assets: A Controller and Auditor's GuideFrom EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideRating: 4 out of 5 stars4/5 (1)

- Understanding Internal Control and the COSO FrameworkDocument4 pagesUnderstanding Internal Control and the COSO FrameworkLloydNo ratings yet

- Audit of InvestmentsDocument4 pagesAudit of InvestmentsLloydNo ratings yet

- Audit of PPE AnnotatedDocument10 pagesAudit of PPE AnnotatedLloydNo ratings yet

- Audit Planning Risk Assessment (APRADocument6 pagesAudit Planning Risk Assessment (APRALloydNo ratings yet

- Equity (Annotated)Document19 pagesEquity (Annotated)LloydNo ratings yet

- Audit of Investments AnnotatedDocument8 pagesAudit of Investments AnnotatedLloydNo ratings yet

- Consolidation of Parent and Subsidiary FinancialsDocument18 pagesConsolidation of Parent and Subsidiary FinancialsLloydNo ratings yet

- Investment in Debt Securities AnnotatedDocument8 pagesInvestment in Debt Securities AnnotatedLloydNo ratings yet

- 06 - PpeDocument4 pages06 - PpeLloydNo ratings yet

- Intangible Assets AnnotatedDocument9 pagesIntangible Assets AnnotatedLloydNo ratings yet

- Wasting Assets AnnotatedDocument3 pagesWasting Assets AnnotatedLloydNo ratings yet

- 05 - Business CombinationsDocument3 pages05 - Business CombinationsLloydNo ratings yet

- Manuscript Pa Hard BoundDocument99 pagesManuscript Pa Hard BoundLloydNo ratings yet

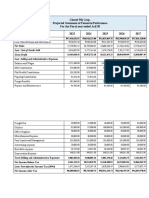

- Glazed Pili Corp. Projected Statement of Financial Performnce For The Fiscal Year Ended Aril 30 2023 2024 2025 2026 2027Document11 pagesGlazed Pili Corp. Projected Statement of Financial Performnce For The Fiscal Year Ended Aril 30 2023 2024 2025 2026 2027LloydNo ratings yet

- List of Tables, Figures & GraphsDocument2 pagesList of Tables, Figures & GraphsLloydNo ratings yet

- List of TablesDocument1 pageList of TablesLloydNo ratings yet

- Bicol College Compliance Certification Proposal DefenseDocument17 pagesBicol College Compliance Certification Proposal DefenseLloydNo ratings yet

- SaharaDocument103 pagesSaharaMahesh TejaniNo ratings yet

- Bai Tap Ve Cac Thi Qua Khu Don Tiep Dien Hoan Thanh Co Dap AnDocument4 pagesBai Tap Ve Cac Thi Qua Khu Don Tiep Dien Hoan Thanh Co Dap AnNguyễn Gia KhangNo ratings yet

- Corporate Strategy Assignment 2 ScriptDocument5 pagesCorporate Strategy Assignment 2 ScriptDelisha MartisNo ratings yet

- Conflict ManagementDocument62 pagesConflict Managementjoseph syukur peranginangin100% (1)

- 5 Characteristics-Defined ProjectDocument1 page5 Characteristics-Defined ProjectHarpreet SinghNo ratings yet

- Massachusetts District Attorneys Agreement To Suspend Use of Breathalyzer Results in ProsecutionsDocument10 pagesMassachusetts District Attorneys Agreement To Suspend Use of Breathalyzer Results in ProsecutionsPatrick Johnson100% (1)

- Community Engagement Solidarity and Citizenship 1Document51 pagesCommunity Engagement Solidarity and Citizenship 1arnie rose BalaNo ratings yet

- US V RuizDocument2 pagesUS V RuizCristelle Elaine ColleraNo ratings yet

- Sany Introduction PDFDocument31 pagesSany Introduction PDFAnandkumar Pokala78% (9)

- Mariah by Che Husna AzhariDocument9 pagesMariah by Che Husna AzhariVagg NinitigaposenNo ratings yet

- Key Performance Indicators - Signposts To Loss PreventionDocument2 pagesKey Performance Indicators - Signposts To Loss PreventionSteve ForsterNo ratings yet

- Design & Development ISODocument6 pagesDesign & Development ISOمختار حنفىNo ratings yet

- ProCapture-T User Manual V1.1 - 20210903 PDFDocument65 pagesProCapture-T User Manual V1.1 - 20210903 PDFahmad khanNo ratings yet

- The Art of Strategic Leadership Chapter 2 - The BusinessDocument6 pagesThe Art of Strategic Leadership Chapter 2 - The BusinessAnnabelle SmythNo ratings yet

- First 1000 Words in Arabic by Hear AmeryDocument66 pagesFirst 1000 Words in Arabic by Hear AmeryCaroline ErstwhileNo ratings yet

- The Science of Cop Watching Volume 004Document1,353 pagesThe Science of Cop Watching Volume 004fuckoffanddie23579No ratings yet

- Tax QuizDocument2 pagesTax QuizMJ ArazasNo ratings yet

- National Educational PolicyDocument5 pagesNational Educational Policyarchana vermaNo ratings yet

- As 2214-2004 Certification of Welding Supervisors - Structural Steel WeldingDocument8 pagesAs 2214-2004 Certification of Welding Supervisors - Structural Steel WeldingSAI Global - APAC50% (2)

- Complaint Before A MagistrateDocument12 pagesComplaint Before A MagistrateZuhair SiddiquiNo ratings yet

- MINOR PPT 5th SEM-4Document22 pagesMINOR PPT 5th SEM-4parthasharma861No ratings yet

- Equatorial Realty v. Mayfair Theater ruling on ownership and fruitsDocument3 pagesEquatorial Realty v. Mayfair Theater ruling on ownership and fruitslinlin_17No ratings yet

- Ajanta Cave Art Work AnalysisDocument13 pagesAjanta Cave Art Work AnalysisannNo ratings yet

- Macro Solved Ma Econmoics NotesDocument120 pagesMacro Solved Ma Econmoics NotesSaif ali KhanNo ratings yet

- Introducing Bill Evans: Nat HentoffDocument2 pagesIntroducing Bill Evans: Nat HentoffSeda BalcıNo ratings yet

- Acheiving Audience Involvement PGDocument2 pagesAcheiving Audience Involvement PGapi-550123704No ratings yet

- Mobility Consulting Engineer - Job DescriptionDocument2 pagesMobility Consulting Engineer - Job DescriptionEdwin BrandNo ratings yet

- Research Paper On Tik TokDocument23 pagesResearch Paper On Tik Tokaskaboutaccounts2187100% (2)

- Response To Salazar TAA Labor Commission PetitionDocument15 pagesResponse To Salazar TAA Labor Commission Petitionrick siegelNo ratings yet

- ELECTORAL ROLLDocument30 pagesELECTORAL ROLLpRice88No ratings yet