You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Group 8 - Exercise 03Document3 pagesGroup 8 - Exercise 03Tuấn Anh CaoNo ratings yet

- Introductory Differential Equations: with Boundary Value Problems, Student Solutions Manual (e-only)From EverandIntroductory Differential Equations: with Boundary Value Problems, Student Solutions Manual (e-only)No ratings yet

- Group 1 - Exercise 3-1Document5 pagesGroup 1 - Exercise 3-1Quynh Nhu NguyenNo ratings yet

- A2 Exercise 3 Group 6Document5 pagesA2 Exercise 3 Group 6Le Hong Ngoc DoanNo ratings yet

- Group 3 - Exercise 3Document6 pagesGroup 3 - Exercise 3Như Tâm HoàngNo ratings yet

- Tutorial-2-Repaired - Hi This Is My Doc Tutorial-2-Repaired - Hi This Is MyDocument11 pagesTutorial-2-Repaired - Hi This Is My Doc Tutorial-2-Repaired - Hi This Is MyHùng LêNo ratings yet

- Self-Test Problems Problem 1: Bond ValuationDocument5 pagesSelf-Test Problems Problem 1: Bond ValuationSeulgi MoonNo ratings yet

- Supplemental Notes On CH 6 PDFDocument2 pagesSupplemental Notes On CH 6 PDFRuel Jr DellovaNo ratings yet

- Lecture notes week 2-2Document32 pagesLecture notes week 2-2Dang QuangNo ratings yet

- Solution of Simple Interest To Compound Interest PDFDocument5 pagesSolution of Simple Interest To Compound Interest PDFSherri BonquinNo ratings yet

- Accountancy Review: Assignment Lpu Review For Submission After April 30, 2020Document5 pagesAccountancy Review: Assignment Lpu Review For Submission After April 30, 2020jackie delos santosNo ratings yet

- How To Value Straight Vanilla Bonds (Solutions)Document9 pagesHow To Value Straight Vanilla Bonds (Solutions)hadosib264No ratings yet

- Bond Valuation ProblemsDocument4 pagesBond Valuation ProblemsMary Justine Paquibot100% (1)

- Time Value of Money: Lumpsum Cases: in This Case, We Calculate The Present Value and Future Value For ADocument10 pagesTime Value of Money: Lumpsum Cases: in This Case, We Calculate The Present Value and Future Value For Asuman chaudharyNo ratings yet

- Pama - Assignment 1 CENENECODocument4 pagesPama - Assignment 1 CENENECOCeddi PamiNo ratings yet

- Required Rate of Return 8% Required Rate of Return 11%Document3 pagesRequired Rate of Return 8% Required Rate of Return 11%Krishele G. GotejerNo ratings yet

- FM Textbook Solutions Chapter 8 Second EditionDocument11 pagesFM Textbook Solutions Chapter 8 Second EditionlibredescargaNo ratings yet

- FM Practice Questions KeyDocument7 pagesFM Practice Questions KeykeshavNo ratings yet

- Time Value of MoneyDocument19 pagesTime Value of MoneyPULKIT DEVPURANo ratings yet

- Ce40-2 - CW1Document2 pagesCe40-2 - CW1Julya AndengNo ratings yet

- Chapter-10: Valuation & Rates of ReturnDocument22 pagesChapter-10: Valuation & Rates of ReturnTajrian RahmanNo ratings yet

- Exercise 1 SolutionsDocument7 pagesExercise 1 SolutionsBen SaadNo ratings yet

- Topic 3 2020Document40 pagesTopic 3 2020GloriaNo ratings yet

- Installments in Compound InterestDocument12 pagesInstallments in Compound InterestRitwikNo ratings yet

- HW Set 4Document3 pagesHW Set 4Maria CiucaNo ratings yet

- Anna FM AnswersDocument4 pagesAnna FM AnswersFrank Hobab MumbiNo ratings yet

- Mortgage Refinance SavingsDocument13 pagesMortgage Refinance SavingsangelNo ratings yet

- Chapter-3-Answers To Practice QuestionsDocument4 pagesChapter-3-Answers To Practice QuestionsqadirqadilNo ratings yet

- Time Value of Money: Gitman and Hennessey, Chapter 5Document43 pagesTime Value of Money: Gitman and Hennessey, Chapter 5Faye Del Gallego EnrileNo ratings yet

- Chapter 10 - Valuation of Risk and ReturnDocument22 pagesChapter 10 - Valuation of Risk and ReturnSamin HaqueNo ratings yet

- Finals Lecture NotesDocument6 pagesFinals Lecture NotesGreg Calibo LidasanNo ratings yet

- Chapter 3 - Concept Questions and Exercises StudentDocument6 pagesChapter 3 - Concept Questions and Exercises StudentVõ Lê Khánh HuyềnNo ratings yet

- Bond Market Analysis: Calculating Bond Prices and YieldsDocument2 pagesBond Market Analysis: Calculating Bond Prices and YieldsFazal Rehman Mandokhail100% (1)

- Capital FinancingDocument5 pagesCapital FinancingJohn Kenneth MantesNo ratings yet

- Ordinary AnnuityDocument2 pagesOrdinary Annuityolivia leonorNo ratings yet

- Time Value of MoneyDocument20 pagesTime Value of MoneyParesh AglaveNo ratings yet

- Chapter 4: Time Value of Money: FIN 301 Homework Solution Ch4Document8 pagesChapter 4: Time Value of Money: FIN 301 Homework Solution Ch4spicegyalNo ratings yet

- Assignment 3.Document5 pagesAssignment 3.Yusuf RaharjaNo ratings yet

- Econ 215-Ch.4-hwSMDocument12 pagesEcon 215-Ch.4-hwSMAnnNo ratings yet

- Vn1001630 - Vo Thi Phuong Thuy - CFDocument9 pagesVn1001630 - Vo Thi Phuong Thuy - CFThunder StormNo ratings yet

- 01 Time Value of Money Summary-3Document9 pages01 Time Value of Money Summary-3Thofik TufelNo ratings yet

- Bond Valuation and Yield CalculationsDocument51 pagesBond Valuation and Yield CalculationsPraveen KanmuseNo ratings yet

- Bond Valuation SolutionsDocument7 pagesBond Valuation SolutionsShubham AggarwalNo ratings yet

- Calculate bond prices and yieldsDocument14 pagesCalculate bond prices and yieldsPranoy SarkarNo ratings yet

- Engineering EconomyDocument23 pagesEngineering EconomyHajji Bañoc100% (1)

- Assignment 2Document2 pagesAssignment 2will.li.shuaiNo ratings yet

- Financial ManagementDocument6 pagesFinancial ManagementRon BoostNo ratings yet

- Chapter 10 FIXED INCOME SECURITIES PDFDocument21 pagesChapter 10 FIXED INCOME SECURITIES PDFJinal SanghviNo ratings yet

- Assignment Cover SheetDocument19 pagesAssignment Cover SheetMd. Ayman IqbalNo ratings yet

- Chapter 2 Lesson 3 - Discount, Inflation, and TaxDocument9 pagesChapter 2 Lesson 3 - Discount, Inflation, and TaxMae AsuncionNo ratings yet

- Assignment 2 - With Answer2022Document6 pagesAssignment 2 - With Answer2022Wai Lam HsuNo ratings yet

- Corporate Finance (Chapter 4) (7th Ed)Document27 pagesCorporate Finance (Chapter 4) (7th Ed)Israt Mustafa100% (1)

- Chapter 11 Compound Interest PDFDocument5 pagesChapter 11 Compound Interest PDFYAHIA ADELNo ratings yet

- Time Value of Money PDFDocument129 pagesTime Value of Money PDFDaniel Louise100% (1)

- Week 4 Assignement-Aulia Ridho MDocument4 pagesWeek 4 Assignement-Aulia Ridho MdhosmanyosNo ratings yet

- Chapter 2 Topic 3 Discount Inflation and TaxDocument9 pagesChapter 2 Topic 3 Discount Inflation and TaxJoash Normie DuldulaoNo ratings yet

- SolutionDocument3 pagesSolutionAshish PurohitNo ratings yet

- FMECO CONCEPT NOTES by Ca Test SeriesDocument329 pagesFMECO CONCEPT NOTES by Ca Test SeriesTanvirNo ratings yet

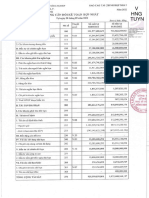

- 20221029NAFBao Cao Tai Chinh Hop Nhat Q3.2022 SignedDocument31 pages20221029NAFBao Cao Tai Chinh Hop Nhat Q3.2022 SignedTuấn Anh CaoNo ratings yet

- 2022INNBCTCQ3Hop Nhat SignatureDocument17 pages2022INNBCTCQ3Hop Nhat SignatureTuấn Anh CaoNo ratings yet

- HW3 Monroes Motivated Sequence Analysis Enigma BC T122WSB 8 PhanThiPhuongNguyen 21001068Document5 pagesHW3 Monroes Motivated Sequence Analysis Enigma BC T122WSB 8 PhanThiPhuongNguyen 21001068Tuấn Anh CaoNo ratings yet

- Group 8 - Exercise 3Document5 pagesGroup 8 - Exercise 3Tuấn Anh CaoNo ratings yet

- Valvula Contrabalance CBV1 10 S O A 30Document21 pagesValvula Contrabalance CBV1 10 S O A 30Judith Daza SilvaNo ratings yet

- Underwater vessels, sensors, weapons and control systemsDocument1 pageUnderwater vessels, sensors, weapons and control systemsNguyễn ThaoNo ratings yet

- Biology 1090 Exam 1 Study GuideDocument5 pagesBiology 1090 Exam 1 Study GuideAmandaNo ratings yet

- Ancient South Arabian TradeDocument16 pagesAncient South Arabian TradeAbo AliNo ratings yet

- POMR Satiti Acute CholangitisDocument30 pagesPOMR Satiti Acute CholangitisIka AyuNo ratings yet

- PhotosynthesisDocument30 pagesPhotosynthesisAngela CanlasNo ratings yet

- DBMS Notes For BCADocument9 pagesDBMS Notes For BCAarndm8967% (6)

- Mahatma Gandhi Institute of Pharmacy, LucknowDocument1 pageMahatma Gandhi Institute of Pharmacy, LucknowMukesh TiwariNo ratings yet

- LLM Thesis On Human RightsDocument7 pagesLLM Thesis On Human Rightswssotgvcf100% (2)

- Wilkinson 2001Document44 pagesWilkinson 2001Toño Gaspar MuñozNo ratings yet

- Dead Reckoning and Estimated PositionsDocument20 pagesDead Reckoning and Estimated Positionscarteani100% (1)

- Ergonomía y Normatividad en 3Document5 pagesErgonomía y Normatividad en 3Rogers DiazNo ratings yet

- 4 McdonaldizationDocument17 pages4 McdonaldizationAngelica AlejandroNo ratings yet

- Zero-Force Members: Hapter Tructural NalysisDocument3 pagesZero-Force Members: Hapter Tructural NalysistifaNo ratings yet

- Kanak Dhara StottramDocument9 pagesKanak Dhara Stottramdd bohraNo ratings yet

- Manual THT70 PDFDocument54 pagesManual THT70 PDFwerterNo ratings yet

- Pe 3 (Module 1) PDFDocument6 pagesPe 3 (Module 1) PDFJoshua Picart100% (1)

- Digital Fuel Calculation v.1Document4 pagesDigital Fuel Calculation v.1Julian ChanNo ratings yet

- NEM Report - IntroDocument11 pagesNEM Report - IntroRoshni PatelNo ratings yet

- I. VHF CommunicationsDocument12 pagesI. VHF CommunicationsSamuel OyelowoNo ratings yet

- Southwest Globe Times - Sep 8, 2011Document16 pagesSouthwest Globe Times - Sep 8, 2011swglobetimesNo ratings yet

- 1-Knowledge Assurance SM PDFDocument350 pages1-Knowledge Assurance SM PDFShahid MahmudNo ratings yet

- Criminal VIIIDocument31 pagesCriminal VIIIAnantHimanshuEkkaNo ratings yet

- Hexadecimal Numbers ExplainedDocument51 pagesHexadecimal Numbers Explainedmike simsonNo ratings yet

- Cardio Fitt Pin PostersDocument5 pagesCardio Fitt Pin Postersapi-385952225No ratings yet

- Monitoring Rock and Soil Mass Performance: To The ConferenceDocument1 pageMonitoring Rock and Soil Mass Performance: To The ConferenceÉrica GuedesNo ratings yet

- Samantha Serpas ResumeDocument1 pageSamantha Serpas Resumeapi-247085580No ratings yet

- Budha Dal Aarti Aarta FULLDocument1 pageBudha Dal Aarti Aarta FULLVishal Singh100% (1)

- Implementing Cisco Application Centric Infrastructure: (Dcaci)Document2 pagesImplementing Cisco Application Centric Infrastructure: (Dcaci)radsssssNo ratings yet

- Gender SensitizationDocument3 pagesGender SensitizationTANU AGARWAL 49 BVOC2019No ratings yet

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000From EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Rating: 4.5 out of 5 stars4.5/5 (86)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 5 out of 5 stars5/5 (2)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet