You might also like

- Aug 2017 PDFDocument4 pagesAug 2017 PDFfurqan yaseenNo ratings yet

- 50 Financial Analyst Interview Questions and AnswersDocument19 pages50 Financial Analyst Interview Questions and AnswerskahladimayahlaNo ratings yet

- QUIZ 2-Mid.-Problems On Statement of Cash FlowsDocument2 pagesQUIZ 2-Mid.-Problems On Statement of Cash FlowsMonica GeronaNo ratings yet

- Chapter 6 ADVAC (Excel +Document43 pagesChapter 6 ADVAC (Excel +Christine Jane RamosNo ratings yet

- May 2017Document7 pagesMay 2017Patrick Arazo0% (1)

- Cash Flow Statements Study GuideDocument37 pagesCash Flow Statements Study GuideAshekin MahadiNo ratings yet

- QUIZ 2-Mid.-Problems On Statement of Cash FlowsDocument2 pagesQUIZ 2-Mid.-Problems On Statement of Cash FlowsMonica GeronaNo ratings yet

- Chapter 18 CompilationDocument21 pagesChapter 18 CompilationMaria Licuanan0% (1)

- Interview Material @SAP - 07..3.22 - With YouDocument270 pagesInterview Material @SAP - 07..3.22 - With YouAjit K. Panigrahi100% (1)

- Final RequirementDocument18 pagesFinal RequirementZandra GonzalesNo ratings yet

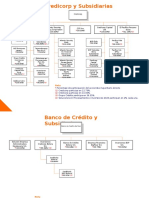

- Organigrama CredicorpDocument7 pagesOrganigrama CredicorpCarlos RamosNo ratings yet

- ASSIGNMENTSDocument13 pagesASSIGNMENTSJpzelleNo ratings yet

- IA Quiz ImadeDocument4 pagesIA Quiz ImadeKuro ZetsuNo ratings yet

- Lab 3 Stock InvestmentDocument4 pagesLab 3 Stock InvestmentAlvira FajriNo ratings yet

- FS Consolidation at The Date of Acquisition v2Document16 pagesFS Consolidation at The Date of Acquisition v2Pagatpat, Apple Grace C.No ratings yet

- CH 04Document9 pagesCH 04Antonios FahedNo ratings yet

- Intermediate Accounting Unit4 - Topic4Document8 pagesIntermediate Accounting Unit4 - Topic4Lea Polinar100% (1)

- CH 4 In-Class ExerciseDocument4 pagesCH 4 In-Class ExerciseAbdullah alhamaadNo ratings yet

- Service Business Accounting CycleDocument6 pagesService Business Accounting CycleMarie Kairish Damag Vivar100% (1)

- CH 12 - SolutionDocument50 pagesCH 12 - SolutionMuhammad RehmanNo ratings yet

- GEN4Document7 pagesGEN4Mylene HeragaNo ratings yet

- Solutions For Notes and Loans ReceivableDocument4 pagesSolutions For Notes and Loans ReceivableKenaniah SanchezNo ratings yet

- Review of Financial Statements and Its Analysis: Rheena B. Delos Santos BSBA-1A (FM2)Document12 pagesReview of Financial Statements and Its Analysis: Rheena B. Delos Santos BSBA-1A (FM2)RHIAN B.No ratings yet

- Warner Company Statement of Cash FlowsDocument2 pagesWarner Company Statement of Cash FlowsKailash KumarNo ratings yet

- Chapter 7 Inclass Problems Day 1 SOLUTIONSDocument3 pagesChapter 7 Inclass Problems Day 1 SOLUTIONSAbdullah alhamaadNo ratings yet

- Angelo Fernando - 01012190021 - Tugas Akuntansi Menengah 2 - Pertemuan 5Document4 pagesAngelo Fernando - 01012190021 - Tugas Akuntansi Menengah 2 - Pertemuan 5ANGELOXAK202No ratings yet

- Tax Quiz 1Document3 pagesTax Quiz 1KimbabNo ratings yet

- Investment in AssociatesDocument6 pagesInvestment in Associates2022104429No ratings yet

- ACC 203 Ch05 SolutionDocument11 pagesACC 203 Ch05 Solutionomaritani2005No ratings yet

- Recording Adjustments For Revenues & Recording EquityDocument7 pagesRecording Adjustments For Revenues & Recording Equitypratibha jaggan martinNo ratings yet

- Problem 1 ReqDocument5 pagesProblem 1 ReqAgent348No ratings yet

- Intermediate Accounting 1 (Chap 17)Document10 pagesIntermediate Accounting 1 (Chap 17)Natalie Anne Bambico MercadoNo ratings yet

- FAOMA Part 3 Quiz Complete SolutionsDocument3 pagesFAOMA Part 3 Quiz Complete SolutionsMary De JesusNo ratings yet

- Online Ass Advance Acc NEWDocument6 pagesOnline Ass Advance Acc NEWRara Rarara30No ratings yet

- Ch04 Consolidation TechniquesDocument54 pagesCh04 Consolidation TechniquesRizqita Putri Ramadhani0% (1)

- Materi Lab 3 - Stock Investment PDFDocument4 pagesMateri Lab 3 - Stock Investment PDFPUTRI YANINo ratings yet

- Introduction To Accounting and Business: Discussion QuestionsDocument46 pagesIntroduction To Accounting and Business: Discussion QuestionsCyyyNo ratings yet

- Sole Trader Accounting Handout 3Document5 pagesSole Trader Accounting Handout 3DenishNo ratings yet

- FCR Final With SignaturesDocument18 pagesFCR Final With SignaturesSeguros, pensiones y fianzas SIMON RODRIGUEZNo ratings yet

- Acg5205 Solutions Ch.08 - SL - Christensen 12eDocument15 pagesAcg5205 Solutions Ch.08 - SL - Christensen 12eRyan NguyenNo ratings yet

- FS AnalysisDocument1 pageFS AnalysisLark WarNo ratings yet

- Chapter 6: Consolidated Financial Statements (Part 3) : Compilation of ReportsDocument43 pagesChapter 6: Consolidated Financial Statements (Part 3) : Compilation of ReportsKriz TanNo ratings yet

- Gialogo, Jessie Lyn San Sebastian College - Recoletos Quiz: Required: Answer The FollowingDocument12 pagesGialogo, Jessie Lyn San Sebastian College - Recoletos Quiz: Required: Answer The FollowingMeidrick Rheeyonie Gialogo AlbaNo ratings yet

- Fin 4500 sAMPLE Midterm Questions and AnswersDocument6 pagesFin 4500 sAMPLE Midterm Questions and AnswersmohamedNo ratings yet

- Tugas Aklan TM7Document7 pagesTugas Aklan TM7AdnanNo ratings yet

- Accounting Cycle 2Document6 pagesAccounting Cycle 2Ahmer NaeemNo ratings yet

- FABULAR Intercompany DividendsDocument6 pagesFABULAR Intercompany DividendsRico, Jalaica B.No ratings yet

- Ch23 StatementofCashFlowExamples Zeke and ZoeDocument4 pagesCh23 StatementofCashFlowExamples Zeke and ZoeHossein ParvardehNo ratings yet

- Problem 2.19Document3 pagesProblem 2.19CNo ratings yet

- ch12 Problem Set CDocument2 pagesch12 Problem Set CMutiara TenriNo ratings yet

- Ch02 SolutionDocument6 pagesCh02 SolutionMalekNo ratings yet

- Suggested Single EntryDocument5 pagesSuggested Single Entrya73512463No ratings yet

- DUAZO - 6th EXAM SIM ANSWERSDocument7 pagesDUAZO - 6th EXAM SIM ANSWERSJeric TorionNo ratings yet

- Good InformationDocument3 pagesGood InformationHoshen MollaNo ratings yet

- Guided Exercises Investment in AssociateDocument2 pagesGuided Exercises Investment in AssociateMireya YueNo ratings yet

- Date Account Titles & Explanation Debit Credit: A. Prepare EntriesDocument4 pagesDate Account Titles & Explanation Debit Credit: A. Prepare Entriesyogi fetriansyahNo ratings yet

- Chapter 5 - Selected SolutionsDocument13 pagesChapter 5 - Selected SolutionsNouh Al-SayyedNo ratings yet

- Jun Zen Ralph Yap BSA - 3 Year Let's CheckDocument2 pagesJun Zen Ralph Yap BSA - 3 Year Let's CheckJunzen Ralph Yap100% (1)

- Solutions Ch08Document19 pagesSolutions Ch08KyleNo ratings yet

- Ac208 2019 11Document6 pagesAc208 2019 11brian mgabi100% (1)

- May 2017 PDF FreeDocument7 pagesMay 2017 PDF FreeJorenz UndagNo ratings yet

- Reporting Financial Results: Practice Session and Revision LectureDocument53 pagesReporting Financial Results: Practice Session and Revision LectureNurt TurdNo ratings yet

- PricewaterhouseCoopers' Guide to the New Tax RulesFrom EverandPricewaterhouseCoopers' Guide to the New Tax RulesNo ratings yet

- Advanced Accounting Chapter 3 AnswersDocument2 pagesAdvanced Accounting Chapter 3 AnswersMaria PiaNo ratings yet

- Chapter 2 Questions-AnswersDocument20 pagesChapter 2 Questions-AnswersMaria PiaNo ratings yet

- ACC 402 - Question 33Document3 pagesACC 402 - Question 33Maria PiaNo ratings yet

- Chapter 6 QuizDocument3 pagesChapter 6 QuizMaria PiaNo ratings yet

- Chapter 5 QuizDocument5 pagesChapter 5 QuizMaria Pia100% (1)

- Chapter 4 QuizDocument5 pagesChapter 4 QuizMaria PiaNo ratings yet

- Chapter 3 QuizDocument7 pagesChapter 3 QuizMaria PiaNo ratings yet

- Chapter 2 QuizDocument4 pagesChapter 2 QuizMaria PiaNo ratings yet

- PWC-UIAS 29 Practical ExampleDocument51 pagesPWC-UIAS 29 Practical ExampleCem SamurcayNo ratings yet

- REO - AFAR - PreWeek - 3rd BatchDocument18 pagesREO - AFAR - PreWeek - 3rd BatchLeocadia GalnayonNo ratings yet

- Assignmnet 5.5Document2 pagesAssignmnet 5.5chrislupinjrNo ratings yet

- Indian Unicorn ReportDocument10 pagesIndian Unicorn ReportV KeshavdevNo ratings yet

- Paymore Products Places Orders For Goods Equal To 75 ofDocument1 pagePaymore Products Places Orders For Goods Equal To 75 ofAmit PandeyNo ratings yet

- fcs340 Document HousingmarketassignmentDocument9 pagesfcs340 Document Housingmarketassignmentapi-468161460No ratings yet

- Chattel Mortgage Without Separate Promissory NoteDocument2 pagesChattel Mortgage Without Separate Promissory NoteJson GalvezNo ratings yet

- Part II: Discussion QuestionsDocument8 pagesPart II: Discussion Questionssamuel39No ratings yet

- Group7 ZA BLKL PaperDocument14 pagesGroup7 ZA BLKL PaperAudrey ArivianaNo ratings yet

- Inet Account Statement: Nadeeem Jamshed 117,044.40Document4 pagesInet Account Statement: Nadeeem Jamshed 117,044.40mubeen khanNo ratings yet

- LIC Jeevan Labh Plan (836) DetailsDocument12 pagesLIC Jeevan Labh Plan (836) DetailsMuthukrishnan SankaranNo ratings yet

- Payment Slip: Summary of Charges / Payments Current Bill AnalysisDocument4 pagesPayment Slip: Summary of Charges / Payments Current Bill AnalysisJumain B SaideNo ratings yet

- Account AssignmentDocument7 pagesAccount AssignmentPororoTix Jie GNo ratings yet

- Opening Balance As Of: 47,889.36: Description Reference Value Date Debit Credit DateDocument1 pageOpening Balance As Of: 47,889.36: Description Reference Value Date Debit Credit DateSayed Rasully SadatNo ratings yet

- GST ChallanDocument2 pagesGST ChallanArun KumarNo ratings yet

- Chapter 3 Cost of CapitalDocument15 pagesChapter 3 Cost of Capitalfirst breakNo ratings yet

- Assignment 4 Class XI Accounting Eq 20230704163852515Document4 pagesAssignment 4 Class XI Accounting Eq 20230704163852515saumya guptaNo ratings yet

- Literature Review CompletedDocument19 pagesLiterature Review CompletedRana Tahir100% (1)

- Arul SPF 2000Document13 pagesArul SPF 2000ADLFVNRNo ratings yet

- Key-Facts-Statement-Signature-Priority-Account UBLDocument4 pagesKey-Facts-Statement-Signature-Priority-Account UBLMuhammadDanialNo ratings yet

- Module 4Document10 pagesModule 4ANSLEY CATE C. GUEVARRANo ratings yet

- Deposit Guarantee Scheme - : Depositor Information SheetDocument2 pagesDeposit Guarantee Scheme - : Depositor Information SheetdeepakaggairbnbNo ratings yet

- 1 SPDocument22 pages1 SPnxshadetyNo ratings yet

- MTBSL: MTB Securities LimitedDocument2 pagesMTBSL: MTB Securities LimitedMuhammad Ziaul HaqueNo ratings yet

- Investment Company Association of The PhilippinesDocument3 pagesInvestment Company Association of The PhilippinesHeinson R. VariasNo ratings yet