You might also like

- Bilal Hyder I170743 20-SEPDocument10 pagesBilal Hyder I170743 20-SEPUbaid0% (1)

- ACI PRC-364.6-22: Concrete Removal in Repairs Involving Corroded Reinforcing Steel-TechnoteDocument3 pagesACI PRC-364.6-22: Concrete Removal in Repairs Involving Corroded Reinforcing Steel-TechnoteMoGHNo ratings yet

- Aircraft ValuationsDocument11 pagesAircraft ValuationsZain MirzaNo ratings yet

- There May Case in Which It Is 0 When Total Revenue Is Not Able To Cover TVC. LOOK at Two Things: 1.total Revenue Exceeds Total Variable Cost. 2. MR Cuts MC From BelowDocument6 pagesThere May Case in Which It Is 0 When Total Revenue Is Not Able To Cover TVC. LOOK at Two Things: 1.total Revenue Exceeds Total Variable Cost. 2. MR Cuts MC From BelowNaeem Ahmed HattarNo ratings yet

- Case 14: Euro Seafood: PromptDocument6 pagesCase 14: Euro Seafood: PromptDuong TranNo ratings yet

- TLE-7 8 Cookery Q1 Week7-8Document10 pagesTLE-7 8 Cookery Q1 Week7-8Heidee Basas50% (2)

- Lecture No 4 - Supply and DemandDocument72 pagesLecture No 4 - Supply and DemandAhsan AtifNo ratings yet

- Supply and DemandDocument111 pagesSupply and Demandhassankazimi23No ratings yet

- Ch.4Supply and DemandDocument75 pagesCh.4Supply and DemandTed LewisNo ratings yet

- Applied Economics: Quarter 3 - Module 3 Market Demand, Market Supply and Market EquilibriumDocument10 pagesApplied Economics: Quarter 3 - Module 3 Market Demand, Market Supply and Market EquilibriumRon TabioloNo ratings yet

- 03 - Theory of Consumer BehaviorDocument11 pages03 - Theory of Consumer BehaviorKeir BalasaNo ratings yet

- Sample SBA - Nuts MixDocument11 pagesSample SBA - Nuts MixAneira G.No ratings yet

- Consumer Choice TheoryDocument62 pagesConsumer Choice TheoryCHARMAINE ALONZONo ratings yet

- Microeconomics Adel LauretoDocument105 pagesMicroeconomics Adel Lauretomercy5sacrizNo ratings yet

- ECON101 2015-16 Fall Final Answer KeyDocument8 pagesECON101 2015-16 Fall Final Answer Keytrungly doNo ratings yet

- NUNING Prak PHP, Tugas Market Share DLLDocument15 pagesNUNING Prak PHP, Tugas Market Share DLLnuningNo ratings yet

- Assignment1 2021Document6 pagesAssignment1 2021NickNo ratings yet

- CH 4 WrittenDocument6 pagesCH 4 WrittenYahiko KenshinNo ratings yet

- Consumer Behavior - Topic1Document19 pagesConsumer Behavior - Topic1Abhishek PatilNo ratings yet

- MIcro For Teaching IDocument27 pagesMIcro For Teaching IgauravpalgarimapalNo ratings yet

- Module IIDocument36 pagesModule IIYash UpasaniNo ratings yet

- Marketing Metrics - Chapter 3Document28 pagesMarketing Metrics - Chapter 3Hoang Yen NhiNo ratings yet

- Chapter V GerylleDocument15 pagesChapter V GerylleBernadeth CiprianoNo ratings yet

- Designation Basic Salary House Rent Medical Allowance: MHR Corp Salary SheetDocument16 pagesDesignation Basic Salary House Rent Medical Allowance: MHR Corp Salary SheetMehedi HasanNo ratings yet

- SKIM October 2015 Pricing WebinarDocument55 pagesSKIM October 2015 Pricing WebinarShilpi IslamNo ratings yet

- CH 23 - Study QuestionsDocument5 pagesCH 23 - Study QuestionsKiranNo ratings yet

- Micro Eportfolio Part 2Document5 pagesMicro Eportfolio Part 2api-240741436No ratings yet

- Perfectly Competitive Supply and Monopolies-1Document62 pagesPerfectly Competitive Supply and Monopolies-1Samiur RahmanNo ratings yet

- Micro Eco, Ch-6Document20 pagesMicro Eco, Ch-6Umma Tanila RemaNo ratings yet

- H. Abellana ST., Canduman, Mandaue CityDocument9 pagesH. Abellana ST., Canduman, Mandaue City김나연No ratings yet

- Perfect Competetion in Laundry MarketDocument26 pagesPerfect Competetion in Laundry MarketBalpreet KaurNo ratings yet

- Consumer Behavior - Cardinal Utility TheoryDocument14 pagesConsumer Behavior - Cardinal Utility Theorykajal goyalNo ratings yet

- BME Topic 7Document33 pagesBME Topic 7Nathaniel Bocauto IINo ratings yet

- Pig Farming BusinessDocument8 pagesPig Farming BusinessOni SundayNo ratings yet

- Perfect Competition: By: Cherryzza Mae B. DumasigDocument9 pagesPerfect Competition: By: Cherryzza Mae B. DumasigAngelica VailocesNo ratings yet

- 3a-Demand and Supply - UploadDocument47 pages3a-Demand and Supply - UploadTay Kai XianNo ratings yet

- Transfer Pricing Examples - Matz&UDocument13 pagesTransfer Pricing Examples - Matz&UMuhammad azeemNo ratings yet

- Lecture Notes - CH 6 Consumer Behavior: Total and Marginal UtilityDocument11 pagesLecture Notes - CH 6 Consumer Behavior: Total and Marginal UtilityPerbz JayNo ratings yet

- Monopolistic Competition and Oligopoly: ECON 0100Document51 pagesMonopolistic Competition and Oligopoly: ECON 0100hussnain tararNo ratings yet

- The Market Putting Supply and Demand TogetherDocument6 pagesThe Market Putting Supply and Demand TogetherHimesh ReshamiaNo ratings yet

- Healthy Bread DelightDocument11 pagesHealthy Bread DelightSetty HakeemaNo ratings yet

- Consumer Behavior: Why Is The Demand Curve Downward Sloping?Document23 pagesConsumer Behavior: Why Is The Demand Curve Downward Sloping?Theo DayoNo ratings yet

- Distribution ExamplesDocument16 pagesDistribution ExamplesVivek KatyalNo ratings yet

- 6.2 - Tutorial QuestionsDocument14 pages6.2 - Tutorial QuestionsMacxy TanNo ratings yet

- Chapter - V OriginalDocument15 pagesChapter - V OriginalBernadeth CiprianoNo ratings yet

- Distribution ExamplesDocument32 pagesDistribution ExamplesWasp_007_007No ratings yet

- Assignment 3: Course Title: ECO101Document4 pagesAssignment 3: Course Title: ECO101Rashik AhmedNo ratings yet

- Chapter Four: Supply II: Managerial Economics Lecturer: Chu-Bin Lin Southwest Jiaotong UniversityDocument29 pagesChapter Four: Supply II: Managerial Economics Lecturer: Chu-Bin Lin Southwest Jiaotong Universitymaria rafiqNo ratings yet

- ME Class 1-7Document59 pagesME Class 1-7sunit dasNo ratings yet

- Unitron CorporationDocument8 pagesUnitron CorporationImeldaNo ratings yet

- Maths Sba LovaDocument6 pagesMaths Sba LovaAleah AliNo ratings yet

- Presentation 2 - Micro Economics 9-3Document18 pagesPresentation 2 - Micro Economics 9-3Hesham EllakanyNo ratings yet

- Unit 3 SupplyDocument54 pagesUnit 3 SupplySwapnil Devang (Lens Stories.)No ratings yet

- Managerial EconomicsDocument9 pagesManagerial EconomicsAbhishek ModakNo ratings yet

- Chapter 4 Theory of Consumer BehaviourDocument9 pagesChapter 4 Theory of Consumer BehaviourYus Linda100% (1)

- Zoca Courtyard DPRDocument24 pagesZoca Courtyard DPRbrijeshbabu1019No ratings yet

- Introductory MicroeconomicsDocument13 pagesIntroductory Microeconomicsgh982487No ratings yet

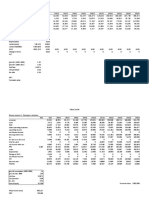

- Price $4.00 Demand 29000 Unit Cost $0.45 Fixed Cost $45,000.00 Revenue $116,000.00 Variable Cost $13,050.00 Profit $57,950.00Document16 pagesPrice $4.00 Demand 29000 Unit Cost $0.45 Fixed Cost $45,000.00 Revenue $116,000.00 Variable Cost $13,050.00 Profit $57,950.00Subhasish PattnaikNo ratings yet

- RUNNING HEAD: Accounting Questions 1Document5 pagesRUNNING HEAD: Accounting Questions 1Chirayu ThapaNo ratings yet

- Perfect Competition Profit MacDocument51 pagesPerfect Competition Profit MacSmurf AccountNo ratings yet

- Snipers, Shills, and Sharks: eBay and Human BehaviorFrom EverandSnipers, Shills, and Sharks: eBay and Human BehaviorRating: 2 out of 5 stars2/5 (1)

- Commodity Market Trading and Investment: A Practitioners Guide to the MarketsFrom EverandCommodity Market Trading and Investment: A Practitioners Guide to the MarketsNo ratings yet

- Accounting For Factory OverheadDocument51 pagesAccounting For Factory OverheadtempoNo ratings yet

- AACE Paper 2005 - Est08 - Controlling Non-ConstructionDocument7 pagesAACE Paper 2005 - Est08 - Controlling Non-ConstructionmangeshjoNo ratings yet

- Dependency Theory in Latin American History - Latin American Studies - Oxford BibliographiesDocument23 pagesDependency Theory in Latin American History - Latin American Studies - Oxford BibliographiesSebastian Diaz Angel100% (1)

- INCOTERMS 2020 QUIZ - Chancafe-Reategui-SaenzDocument6 pagesINCOTERMS 2020 QUIZ - Chancafe-Reategui-SaenzJuliana Chancafe IncioNo ratings yet

- Certificate of Increase of Capital StockDocument2 pagesCertificate of Increase of Capital StockmarkNo ratings yet

- Evaluation and Analysis of Wear in Progressive Cavity Pumps: The University of HullDocument174 pagesEvaluation and Analysis of Wear in Progressive Cavity Pumps: The University of HullNicolas CalvoNo ratings yet

- Click Here: Join Our '42 Days IB ACIO BatchDocument16 pagesClick Here: Join Our '42 Days IB ACIO Batchdoli sindhujaNo ratings yet

- Basements: Costs: Cost Study of Houses With BasementsDocument32 pagesBasements: Costs: Cost Study of Houses With BasementsJeff TanNo ratings yet

- NetscapeDocument3 pagesNetscapeulix1985No ratings yet

- Data Sheet 26 - Fig FT702 150 T StrainerDocument1 pageData Sheet 26 - Fig FT702 150 T StrainerSteve NewmanNo ratings yet

- Joist Dimension and SpanDocument4 pagesJoist Dimension and SpanJC TsuiNo ratings yet

- 02 - STD - MCCB - Moulded Case Circuit Breakers - (2.23 - 2.24)Document2 pages02 - STD - MCCB - Moulded Case Circuit Breakers - (2.23 - 2.24)ThilinaNo ratings yet

- CH 09Document172 pagesCH 09ErkanNo ratings yet

- 04. دورِ جدید میں بینک کے فرائض و وظائف PDFDocument14 pages04. دورِ جدید میں بینک کے فرائض و وظائف PDFfaridNo ratings yet

- (Financial Figures in 000) : ARR Calculation: Invest LimitedDocument15 pages(Financial Figures in 000) : ARR Calculation: Invest LimitedYenJangNo ratings yet

- Fountom Composite Anel and ProfilesDocument24 pagesFountom Composite Anel and ProfilesBruno ManestarNo ratings yet

- Pengadaan Various Valve DKMDocument4 pagesPengadaan Various Valve DKMyulianzoneNo ratings yet

- Arun Motors: TAX INVOICE, Issued Under Rule 46 of CGST/SGST Rules, 2017Document2 pagesArun Motors: TAX INVOICE, Issued Under Rule 46 of CGST/SGST Rules, 2017AshokNo ratings yet

- Ductile-Brittle Transition Temperature and Impact Energy Tests - Yena EngineeringDocument7 pagesDuctile-Brittle Transition Temperature and Impact Energy Tests - Yena EngineeringKASHFI UDDINNo ratings yet

- PMC Bid Document DasarhalliDocument66 pagesPMC Bid Document DasarhalliBharath RajNo ratings yet

- 4.1. Simple and Compound InterestDocument5 pages4.1. Simple and Compound InterestIsagaki RikuNo ratings yet

- Micro Eco Quick Revison Notes DR - Asad KVIIM LucknowDocument18 pagesMicro Eco Quick Revison Notes DR - Asad KVIIM LucknowKushagra Shukla 11ANo ratings yet

- Crossword - Intro To EconomicsDocument2 pagesCrossword - Intro To EconomicsFrances JalandoniNo ratings yet

- Wepp C8bvfeDocument2 pagesWepp C8bvfeg-13168129No ratings yet

- Badminton Sponcer LetterDocument2 pagesBadminton Sponcer LetterSeriseran JothiNo ratings yet

- Introduction To International Economics (Lecture 1)Document25 pagesIntroduction To International Economics (Lecture 1)Roite BeteroNo ratings yet

- Iemco Group Profile WNWF 3-10-2015Document26 pagesIemco Group Profile WNWF 3-10-2015MowheadAdelNo ratings yet

- OFDI052022Document32 pagesOFDI052022jessica mathurNo ratings yet