You might also like

- The Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeFrom EverandThe Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeNo ratings yet

- Particulars TDS Rates (In %)Document6 pagesParticulars TDS Rates (In %)Amiy Anand PandeyNo ratings yet

- Particulars TDS Rates (In %) : Section 192 Section 192A Section 193Document9 pagesParticulars TDS Rates (In %) : Section 192 Section 192A Section 193ajayNo ratings yet

- Notification TDS Rates - FV AMC BillDocument8 pagesNotification TDS Rates - FV AMC Billamit chavariaNo ratings yet

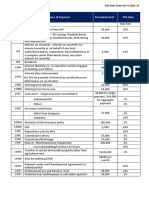

- TDS Rate Chart'Document8 pagesTDS Rate Chart'PUSHKAR GARGNo ratings yet

- TDS Rates For FY 2021-22Document12 pagesTDS Rates For FY 2021-222022 YearNo ratings yet

- TDS RatesDocument9 pagesTDS RatesCharu JagetiaNo ratings yet

- Tds Rate ChartDocument15 pagesTds Rate ChartJain MjNo ratings yet

- TDS Rates Ay 2022-23Document10 pagesTDS Rates Ay 2022-23Suriyakumar ShanmugavelNo ratings yet

- Particulars TDS Rates (In %) : Section 192 Section 192A Section 193Document7 pagesParticulars TDS Rates (In %) : Section 192 Section 192A Section 193ABHISHEKNo ratings yet

- TDS Rate Chart For FY 2021-22 - AY 2022-23 - UpdatedDocument13 pagesTDS Rate Chart For FY 2021-22 - AY 2022-23 - UpdatedAnkur ShahNo ratings yet

- IT Rates For Tax Deduction at SourceDocument12 pagesIT Rates For Tax Deduction at SourceArun EmmiNo ratings yet

- Section 192:: Payment of SalaryDocument7 pagesSection 192:: Payment of SalaryCacptCoachingNo ratings yet

- TDS Rate Chart: (For Assessment Year 2017-18)Document10 pagesTDS Rate Chart: (For Assessment Year 2017-18)Ajay SimonNo ratings yet

- What Are The Incomes Specified For TDSDocument6 pagesWhat Are The Incomes Specified For TDSaniket thakurNo ratings yet

- TDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inDocument15 pagesTDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inSachin GuptaNo ratings yet

- Tds Rate Chart Fy 2021-22Document3 pagesTds Rate Chart Fy 2021-22Kadambari ShelkeNo ratings yet

- TDS Rates Chart FY 2020-21: Key DetailsDocument9 pagesTDS Rates Chart FY 2020-21: Key Detailsjibin samuelNo ratings yet

- TDS RATE CHART FY 2021-22-FinalDocument5 pagesTDS RATE CHART FY 2021-22-FinalLeenaNo ratings yet

- TDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersDocument7 pagesTDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersRajNo ratings yet

- Ty Tax Project (Final)Document14 pagesTy Tax Project (Final)raj_s_harmaNo ratings yet

- Income Tax TDS RateDocument7 pagesIncome Tax TDS RateSuresh KesavanNo ratings yet

- Tds Rate Chart Fy 2020Document4 pagesTds Rate Chart Fy 2020KAUTUK KOLINo ratings yet

- Presentation On TDS Provision: by Nilesh Deharkar & AMAN BhattacharyaDocument15 pagesPresentation On TDS Provision: by Nilesh Deharkar & AMAN BhattacharyaAman BhattacharyaNo ratings yet

- Ssra Tds Rates 2021-2022Document10 pagesSsra Tds Rates 2021-2022deepu kNo ratings yet

- TDS Rate Chart FY 2020-2021 (Covid-19) : Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) (Covid-19)Document4 pagesTDS Rate Chart FY 2020-2021 (Covid-19) : Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) (Covid-19)Sahay AlokNo ratings yet

- Some Issues On Practice of TDS Law Seminar by NIRCDocument29 pagesSome Issues On Practice of TDS Law Seminar by NIRCHarish KalidasNo ratings yet

- Some Issues On Practice of TDS Law Some Issues On Practice of TDS Law Seminar by NIRC Seminar by NIRCDocument29 pagesSome Issues On Practice of TDS Law Some Issues On Practice of TDS Law Seminar by NIRC Seminar by NIRCJinoy P MathewNo ratings yet

- TDS Rates Chart Fy 2020 21 Ay 2021 22Document6 pagesTDS Rates Chart Fy 2020 21 Ay 2021 22Brijendra SinghNo ratings yet

- Seminar On TDSDocument29 pagesSeminar On TDSCA Virendra ChhajerNo ratings yet

- Some Issues On Practice of TDS Law Seminar by NIRCDocument29 pagesSome Issues On Practice of TDS Law Seminar by NIRCShashank Deva SunnyNo ratings yet

- Comparisn Section 19AAAA Section 19AAAAA Section 19BBBBB Section 82BB PDFDocument6 pagesComparisn Section 19AAAA Section 19AAAAA Section 19BBBBB Section 82BB PDFPopy AkterNo ratings yet

- TDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Document3 pagesTDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Prince RaichandNo ratings yet

- TDS Rate chart FY 2024-25Document4 pagesTDS Rate chart FY 2024-25MOQADDARNo ratings yet

- TDS SummaryDocument4 pagesTDS Summaryshubhamsingh143deepNo ratings yet

- Instapdf - in Tds Rate Chart Fy 2023 24 Ay 2024 25 355Document7 pagesInstapdf - in Tds Rate Chart Fy 2023 24 Ay 2024 25 355skassociatetaxconsultantNo ratings yet

- TDS Tax Challan Filing GuideDocument3 pagesTDS Tax Challan Filing GuideSURABHI PATRANo ratings yet

- TDS_and_TCS-rate-chart-2025Document5 pagesTDS_and_TCS-rate-chart-2025jsparakhNo ratings yet

- TDS Chart FY 23-24Document6 pagesTDS Chart FY 23-24kuldeep singhNo ratings yet

- TDS EntryDocument11 pagesTDS Entryश्रीनाथ राजाराम दातेNo ratings yet

- TDS Rates For The ADocument1 pageTDS Rates For The AsadathnooriNo ratings yet

- TDS rates for various income types under Sections 192-194LBA of the Income Tax ActDocument3 pagesTDS rates for various income types under Sections 192-194LBA of the Income Tax ActSridharan DhanasekaranNo ratings yet

- All About TDS Part 2Document9 pagesAll About TDS Part 2Animesh Kumar TilakNo ratings yet

- Section 195 TDS On Non-Resident PaymentsDocument1 pageSection 195 TDS On Non-Resident Paymentskumarsanjeev079No ratings yet

- Tax Deducted at Source UnitDocument13 pagesTax Deducted at Source Unitsatyanarayan dashNo ratings yet

- TDS and TCS Rate Chart 2023Document5 pagesTDS and TCS Rate Chart 2023DEEPAK SHARMANo ratings yet

- TDS and TCS-rate-chart-2023 RemovedDocument4 pagesTDS and TCS-rate-chart-2023 Removeddurgeshsonawane65No ratings yet

- Tax Deduction at Source Sections ExplainedDocument4 pagesTax Deduction at Source Sections ExplainedVidit GuptaNo ratings yet

- Tds On Dividend 24062022Document6 pagesTds On Dividend 24062022thimothiNo ratings yet

- TDS Rates Chart For Financial Year 2021 22 Assessment Year 2022 23 1Document5 pagesTDS Rates Chart For Financial Year 2021 22 Assessment Year 2022 23 1Audit ManifestNo ratings yet

- Commonly used TDS Provisions for payments in IndiaDocument17 pagesCommonly used TDS Provisions for payments in IndiaSonika GuptaNo ratings yet

- Tax Deduction at Source: Subject NameDocument7 pagesTax Deduction at Source: Subject Nameharshita23hrNo ratings yet

- Understanding Regular Income TaxDocument2 pagesUnderstanding Regular Income Taxace zeroNo ratings yet

- Revised TDS Wef 14.05.20Document7 pagesRevised TDS Wef 14.05.20MANAN KOTHARINo ratings yet

- WWW - Taxguru.in: TDS Rate Chart For Financial Year 2018-19Document1 pageWWW - Taxguru.in: TDS Rate Chart For Financial Year 2018-19Sunny NarangNo ratings yet

- Budget 2019 Updates - Key Income Tax Changes and TDS RatesDocument6 pagesBudget 2019 Updates - Key Income Tax Changes and TDS RatesAjeet KumarNo ratings yet

- Tax Deposit-Challan 281-Excel FormatDocument5 pagesTax Deposit-Challan 281-Excel FormatpreetNo ratings yet

- Items of Gross Income Subject To RegularDocument2 pagesItems of Gross Income Subject To Regularhannah drew ovejasNo ratings yet

- 10574-Oracle Support Council - Understanding and Troubleshooting GST - Functionality and New Diagnostic Tools-Presentation - 788Document28 pages10574-Oracle Support Council - Understanding and Troubleshooting GST - Functionality and New Diagnostic Tools-Presentation - 788moin786mirza100% (1)

- CL2022 - 23 - Guidelines On Domestic Investments That Do Not Require Prior ApprovalDocument6 pagesCL2022 - 23 - Guidelines On Domestic Investments That Do Not Require Prior ApprovaldignaNo ratings yet

- Understanding IAS 37 Provisions Continge PDFDocument8 pagesUnderstanding IAS 37 Provisions Continge PDFSweet EmmeNo ratings yet

- Heath Pro Infinity BrochureDocument5 pagesHeath Pro Infinity BrochureMayank SrivastavaNo ratings yet

- EmbutidoDocument46 pagesEmbutidoFrances Mae Ortiz MaglinteNo ratings yet

- Far - First Preboard QuestionnaireDocument14 pagesFar - First Preboard QuestionnairewithyouidkNo ratings yet

- Claim ClosedDocument2 pagesClaim ClosedpruthviNo ratings yet

- HVCCI UPI Form No. 3 Summary ReportDocument2 pagesHVCCI UPI Form No. 3 Summary ReportAzumi AyuzawaNo ratings yet

- Social Security Numbers and CardsDocument2 pagesSocial Security Numbers and CardsHector HurtadoNo ratings yet

- Taxation Management (FIN623) : Assignment # 02Document2 pagesTaxation Management (FIN623) : Assignment # 02Rajesh KumarNo ratings yet

- Execution of Agreement/AwardDocument20 pagesExecution of Agreement/AwardJosephus DeysolongNo ratings yet

- Post Employment BenefitsDocument31 pagesPost Employment BenefitsSky SoronoiNo ratings yet

- May-23 412105Document4 pagesMay-23 412105Rakesh PawarNo ratings yet

- Origin and Evolution of Insurance in IndiaDocument78 pagesOrigin and Evolution of Insurance in IndiaVedant GoswamiNo ratings yet

- COS Lec 2 1Document7 pagesCOS Lec 2 1Jaypee Verzo SaltaNo ratings yet

- Using the GY Modifier for Statutory Exclusions and Non-Covered ServicesDocument1 pageUsing the GY Modifier for Statutory Exclusions and Non-Covered ServicesvidhunenNo ratings yet

- Employee Benefits PolicyDocument6 pagesEmployee Benefits PolicyDivyaNo ratings yet

- Lengo Savings Plan PremierDocument9 pagesLengo Savings Plan PremierPado DjochieNo ratings yet

- 40yrs MOST18 NEW 112222Document5 pages40yrs MOST18 NEW 112222Lance AunzoNo ratings yet

- Chapter 4 Case Study - New Century Health ClinicDocument3 pagesChapter 4 Case Study - New Century Health ClinicGeorge RamosNo ratings yet

- Tata AIA Life Insurance Fortune Guarantee Plus Savings PlanDocument13 pagesTata AIA Life Insurance Fortune Guarantee Plus Savings PlanAkshay SaxenaNo ratings yet

- SARS PAYE BRS PAYE Employer Reconciliation V15!0!0Document106 pagesSARS PAYE BRS PAYE Employer Reconciliation V15!0!0lebomaedi5No ratings yet

- Small Business Accounting GuideDocument30 pagesSmall Business Accounting GuideKamlesh Singh100% (1)

- Financcial LiteracyDocument3 pagesFinanccial LiteracyTushar GuptaNo ratings yet

- Managing Business Finance During Challenging TimesDocument36 pagesManaging Business Finance During Challenging TimesYong Chun WahNo ratings yet

- BIMCO clauses for ISPS, customs, piracy and moreDocument5 pagesBIMCO clauses for ISPS, customs, piracy and morePeter BaloghNo ratings yet

- Maturity Form: Policy InformationDocument2 pagesMaturity Form: Policy Informationroodra singh ranawatNo ratings yet

- Pyla Santhosh Kumar Offer Letter FinalDocument18 pagesPyla Santhosh Kumar Offer Letter FinalSantosh KumarNo ratings yet

- True Value Pick UpDocument8 pagesTrue Value Pick UpNikhil Agrawal0% (1)

- A Minor Project Report On: "Mutual Fund Investments"Document24 pagesA Minor Project Report On: "Mutual Fund Investments"Srijan RishiNo ratings yet

- Sbi Life Insurance ProjectDocument72 pagesSbi Life Insurance ProjectDevaraj Nanda Kumar100% (6)

- Unfair Labor Practices and the Struggles of Healthcare WorkersDocument2 pagesUnfair Labor Practices and the Struggles of Healthcare WorkersKubrick RabbitNo ratings yet