You might also like

- TDS Chart FY 23-24Document6 pagesTDS Chart FY 23-24kuldeep singhNo ratings yet

- TDS Rates Chart For Financial Year 2021 22 Assessment Year 2022 23 1Document5 pagesTDS Rates Chart For Financial Year 2021 22 Assessment Year 2022 23 1Audit ManifestNo ratings yet

- Ssra Tds Rates 2021-2022Document10 pagesSsra Tds Rates 2021-2022deepu kNo ratings yet

- TDS Rate Chart For Financial Year 2022 23 Assessment Year 2023 24Document9 pagesTDS Rate Chart For Financial Year 2022 23 Assessment Year 2023 24Sumukh TemkarNo ratings yet

- TDS RATE CHART FY 2021-22-FinalDocument5 pagesTDS RATE CHART FY 2021-22-FinalLeenaNo ratings yet

- Tds Rate Chart Fy 2021-22Document3 pagesTds Rate Chart Fy 2021-22Kadambari ShelkeNo ratings yet

- TDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inDocument15 pagesTDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inSachin GuptaNo ratings yet

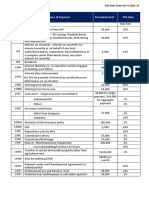

- TDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersDocument7 pagesTDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersRajNo ratings yet

- Tds Rate Chart Fy 2020Document4 pagesTds Rate Chart Fy 2020KAUTUK KOLINo ratings yet

- Section 192:: Payment of SalaryDocument7 pagesSection 192:: Payment of SalaryCacptCoachingNo ratings yet

- TDS RATE CHART F.Y. 2019-20 (A.Y. 2020-21) : WWW - Bharatax.inDocument1 pageTDS RATE CHART F.Y. 2019-20 (A.Y. 2020-21) : WWW - Bharatax.inGajendra Singh Rajpurohit Chadwas IIINo ratings yet

- TDS Rates ChartDocument11 pagesTDS Rates ChartSarat KumarNo ratings yet

- C.H. Padliya & Co.: Chartered AccountantsDocument5 pagesC.H. Padliya & Co.: Chartered AccountantsSarat KumarNo ratings yet

- Current Changes of TDS: Presented By, Ghanshyam WatekarDocument10 pagesCurrent Changes of TDS: Presented By, Ghanshyam Watekarpraful_watekarNo ratings yet

- TDS_and_TCS-rate-chart-2025Document5 pagesTDS_and_TCS-rate-chart-2025jsparakhNo ratings yet

- TDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Document3 pagesTDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Prince RaichandNo ratings yet

- Tds BookletDocument22 pagesTds BookletSanjayThakkarNo ratings yet

- Tax Deducted at Source (TDS)Document7 pagesTax Deducted at Source (TDS)Rupali SinghNo ratings yet

- TDS Rates Applicable from 01.10.2009Document2 pagesTDS Rates Applicable from 01.10.2009Gaurav MalhotraNo ratings yet

- TDS Rates For The ADocument1 pageTDS Rates For The AsadathnooriNo ratings yet

- Rates of TDSDocument30 pagesRates of TDSsudhanshu88g1No ratings yet

- Tds Rate ChartDocument49 pagesTds Rate ChartSANJEEVNo ratings yet

- Revised TDS Wef 14.05.20Document7 pagesRevised TDS Wef 14.05.20MANAN KOTHARINo ratings yet

- TDS RatesDocument9 pagesTDS RatesCharu JagetiaNo ratings yet

- C.H. Padliya & Co.: Chartered AccountantsDocument6 pagesC.H. Padliya & Co.: Chartered AccountantsSarat KumarNo ratings yet

- Tds Rate ChartDocument15 pagesTds Rate ChartJain MjNo ratings yet

- WWW - Taxguru.in: TDS Rate Chart For Financial Year 2018-19Document1 pageWWW - Taxguru.in: TDS Rate Chart For Financial Year 2018-19Sunny NarangNo ratings yet

- Tds Income Tax Rates Fy 2010-11Document13 pagesTds Income Tax Rates Fy 2010-11Surender KumarNo ratings yet

- Accounts & Taxations Interview Related NotesDocument5 pagesAccounts & Taxations Interview Related NotesRahul Baburao AbhaleNo ratings yet

- Notification TDS Rates - FV AMC BillDocument8 pagesNotification TDS Rates - FV AMC Billamit chavariaNo ratings yet

- TDS Rate Chart FY 2020-2021 (Covid-19) : Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) (Covid-19)Document4 pagesTDS Rate Chart FY 2020-2021 (Covid-19) : Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) (Covid-19)Sahay AlokNo ratings yet

- TDS Rate ChartDocument2 pagesTDS Rate Chartshashi370No ratings yet

- Karvy Group TDS Rates W.E.F. 01.04.2010 Rate of TDS Rate of TDS If PAN Providedif PAN Not ProvidedDocument1 pageKarvy Group TDS Rates W.E.F. 01.04.2010 Rate of TDS Rate of TDS If PAN Providedif PAN Not Providedarjun_cwaNo ratings yet

- TDS Provisions under Income Tax Act 1961Document77 pagesTDS Provisions under Income Tax Act 1961Sachin KumarNo ratings yet

- Particulars TDS Rates (In %) : Section 192 Section 192A Section 193Document7 pagesParticulars TDS Rates (In %) : Section 192 Section 192A Section 193ABHISHEKNo ratings yet

- TDS TCSDocument231 pagesTDS TCSNarinderpal SinghNo ratings yet

- C.H. Padliya & Co.: Chartered AccountantsDocument13 pagesC.H. Padliya & Co.: Chartered AccountantsSarat KumarNo ratings yet

- TDS RatesDocument11 pagesTDS RatesRAVI DWIVEDINo ratings yet

- TDS Rate Chart'Document8 pagesTDS Rate Chart'PUSHKAR GARGNo ratings yet

- Particulars TDS Rates (In %) : Section 192 Section 192A Section 193Document9 pagesParticulars TDS Rates (In %) : Section 192 Section 192A Section 193ajayNo ratings yet

- What Are The Incomes Specified For TDSDocument6 pagesWhat Are The Incomes Specified For TDSaniket thakurNo ratings yet

- Tax Deduction at SourceDocument13 pagesTax Deduction at SourceSwati SumanNo ratings yet

- TDS Rate & Tax Provisions For F.Y. 2019-20 (A.Y. 2020-21) : TDS Is Deducted On The Following Types of PaymentsDocument10 pagesTDS Rate & Tax Provisions For F.Y. 2019-20 (A.Y. 2020-21) : TDS Is Deducted On The Following Types of PaymentsnagallanraoNo ratings yet

- What Is TDS?: Tax Deducted at Source (TDS)Document8 pagesWhat Is TDS?: Tax Deducted at Source (TDS)Sandeep RajpootNo ratings yet

- IT Rates For Tax Deduction at SourceDocument12 pagesIT Rates For Tax Deduction at SourceArun EmmiNo ratings yet

- TDS - and - TCS Rate Chart 2024Document5 pagesTDS - and - TCS Rate Chart 2024Taxation KTPL (Kalyani Techpark Taxation)No ratings yet

- Tax Deducted at Source UnitDocument13 pagesTax Deducted at Source Unitsatyanarayan dashNo ratings yet

- TDS and TCS Rate Chart 2023Document5 pagesTDS and TCS Rate Chart 2023DEEPAK SHARMANo ratings yet

- TDS and TCS-rate-chart-2023 RemovedDocument4 pagesTDS and TCS-rate-chart-2023 Removeddurgeshsonawane65No ratings yet

- TDS Rates Chart Fy 2020 21 Ay 2021 22Document6 pagesTDS Rates Chart Fy 2020 21 Ay 2021 22Brijendra SinghNo ratings yet

- TDS (Tax Deducted at Source) Rate Chart For Financial Year 2010-11Document13 pagesTDS (Tax Deducted at Source) Rate Chart For Financial Year 2010-11av_meshramNo ratings yet

- Commonly used TDS Provisions for payments in IndiaDocument17 pagesCommonly used TDS Provisions for payments in IndiaSonika GuptaNo ratings yet

- Particulars TDS Rates (In %)Document6 pagesParticulars TDS Rates (In %)Amiy Anand PandeyNo ratings yet

- Intro of TdsDocument6 pagesIntro of Tdsshivani singhNo ratings yet

- TDS Concept and RatesDocument7 pagesTDS Concept and RatesThe Social KarkhanaNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Naxal WomenDocument2 pagesNaxal WomenRishabh SainiNo ratings yet

- Asymptotic Expansion of Bessel Functions for ElectromagneticsDocument11 pagesAsymptotic Expansion of Bessel Functions for ElectromagneticsDanish NaeemNo ratings yet

- Financial Distress (2008)Document24 pagesFinancial Distress (2008)Ira Putri100% (1)

- DL Services Acknowledgement RohitDocument1 pageDL Services Acknowledgement RohitHoney SinghNo ratings yet

- Assignment Help Journal Ledger and MyodDocument9 pagesAssignment Help Journal Ledger and MyodrajeshNo ratings yet

- IntervalsDocument10 pagesIntervalsJohn Leal100% (2)

- AC ENTERPRISES V FRABELLE PROPERTIES CORPDocument3 pagesAC ENTERPRISES V FRABELLE PROPERTIES CORPRhodz Coyoca EmbalsadoNo ratings yet

- Rbi Guidelines On NRODocument6 pagesRbi Guidelines On NROGahininathJagannathGadeNo ratings yet

- ITP PaintingDocument1 pageITP PaintingYash Sharma100% (3)

- Loose Constructionism vs. Strict ConstructionismDocument4 pagesLoose Constructionism vs. Strict ConstructionismClaudia SilvaNo ratings yet

- Address:: Terminal Road 1 Corner, F. Imperial Street, Legazpi Port District, Legazpi City, Albay, PhilippinesDocument4 pagesAddress:: Terminal Road 1 Corner, F. Imperial Street, Legazpi Port District, Legazpi City, Albay, PhilippinesYani BarriosNo ratings yet

- 19 - BPI Employees Union v. BPI - G.R. No. 178699. September 21, 2011Document2 pages19 - BPI Employees Union v. BPI - G.R. No. 178699. September 21, 2011Jesi CarlosNo ratings yet

- Stan Stuart v. Linda Mendenhall, 11th Cir. (2014)Document12 pagesStan Stuart v. Linda Mendenhall, 11th Cir. (2014)Scribd Government DocsNo ratings yet

- MC 9 Equity A201 StudentDocument4 pagesMC 9 Equity A201 StudentKkk.sssNo ratings yet

- History Final Project by Noah A and Xavier HDocument18 pagesHistory Final Project by Noah A and Xavier Hapi-232469506No ratings yet

- BCT Lecture7 8 Superposition TheoremDocument46 pagesBCT Lecture7 8 Superposition TheoremShaleva SinghNo ratings yet

- WEB Threat AssessmentDocument3 pagesWEB Threat AssessmentWilliam N. GriggNo ratings yet

- Emphasis On Cloud: This Photo CC By-SaDocument33 pagesEmphasis On Cloud: This Photo CC By-SaDavid CowenNo ratings yet

- LANPoker EULA ENGDocument2 pagesLANPoker EULA ENGMealone NiceNo ratings yet

- Compania Maritima vs. Allied Free Workers UnionDocument18 pagesCompania Maritima vs. Allied Free Workers UnionAngelReaNo ratings yet

- Memorandum of Understanding For Contract Research Between Icar-Central Avian Research INSTITUTE, IZATNAGAR ANDDocument6 pagesMemorandum of Understanding For Contract Research Between Icar-Central Avian Research INSTITUTE, IZATNAGAR ANDQuality JiveNo ratings yet

- 18 Financial StatementsDocument35 pages18 Financial Statementswsahmed28No ratings yet

- Obligations of The VendorDocument4 pagesObligations of The VendorHenri VasquezNo ratings yet

- Conformity Certificate TemplateDocument1 pageConformity Certificate TemplateShahbaz Khan100% (1)

- Christopher Shelton ObituaryDocument3 pagesChristopher Shelton Obituaryifly2bwiNo ratings yet

- Dhaka Club Areya BaseDocument63 pagesDhaka Club Areya BaseAbu Bakkar Siddiq100% (1)

- Rules of The Road Purpose and ScopeDocument137 pagesRules of The Road Purpose and Scopesid bez100% (2)

- Computer Age Management Services LimitedDocument1 pageComputer Age Management Services LimitedAbhishek JainNo ratings yet

- Caselman DIY AMG + Multimedia (Copyleft)Document106 pagesCaselman DIY AMG + Multimedia (Copyleft)cliftoncage100% (1)

- Psref 325Document285 pagesPsref 325Alex OmegaNo ratings yet