You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- SSC CGL Preparatory Guide -Mathematics (Part 2)From EverandSSC CGL Preparatory Guide -Mathematics (Part 2)Rating: 4 out of 5 stars4/5 (1)

- Sahodaya Accountancy AKDocument23 pagesSahodaya Accountancy AKrthi kusumNo ratings yet

- Accountancy Set B (Answer Key)Document23 pagesAccountancy Set B (Answer Key)Santhi SNo ratings yet

- FT GR12 Acak Set1 - 17832Document5 pagesFT GR12 Acak Set1 - 17832Amaan AbbasNo ratings yet

- Solution Manual For Managerial Economics 6th Edition For KeatDocument7 pagesSolution Manual For Managerial Economics 6th Edition For KeatBiancaNortonmtckNo ratings yet

- Advanced Financial AccountingDocument4 pagesAdvanced Financial AccountingBhavi GolchhaNo ratings yet

- Answer Key 2Document8 pagesAnswer Key 2Hari prakarsh NimiNo ratings yet

- BE Operation Question and AnswerDocument5 pagesBE Operation Question and AnswerJhanella Faith FagarNo ratings yet

- Answer Keys & Marking Scheme Acc XiiDocument8 pagesAnswer Keys & Marking Scheme Acc XiiGHOST FFNo ratings yet

- Managerial Accounting: SectionDocument17 pagesManagerial Accounting: SectionNostecNo ratings yet

- Marking Scheme Mock Test I 2023 24Document9 pagesMarking Scheme Mock Test I 2023 24HARSH CHAURASIYANo ratings yet

- MS Xii Accountancy Set 1Document10 pagesMS Xii Accountancy Set 1arikoff07No ratings yet

- MS Accountancy PB Xii Set 2Document9 pagesMS Accountancy PB Xii Set 2DakshitaNo ratings yet

- Assignment Leverage Analysis: Financial ManagementDocument2 pagesAssignment Leverage Analysis: Financial ManagementVishal ChandakNo ratings yet

- Unit 3 PDFDocument13 pagesUnit 3 PDFganaNo ratings yet

- MS Accountancy XIIDocument8 pagesMS Accountancy XIISahil RaikwarNo ratings yet

- 02c Analysis of FADocument12 pages02c Analysis of FASaad ZamanNo ratings yet

- Solution Maf503 - Jun 2016 AmmendDocument10 pagesSolution Maf503 - Jun 2016 Ammendanis izzatiNo ratings yet

- 2023 CBSE I Succeed Accountancy 12th SQP 10Document12 pages2023 CBSE I Succeed Accountancy 12th SQP 10shubhramavat1322No ratings yet

- SMS 11 AccountancyDocument11 pagesSMS 11 AccountancyacguptaclassesNo ratings yet

- MS G12 Acc PT1 2023Document8 pagesMS G12 Acc PT1 2023Ethan LourdesNo ratings yet

- 1MS-CLASS XII ACC - Common Board-2022-23 (2) - 230329 - 142033Document21 pages1MS-CLASS XII ACC - Common Board-2022-23 (2) - 230329 - 142033jiya.mehra.2306No ratings yet

- Cbse SQP 22-23 MSDocument12 pagesCbse SQP 22-23 MSPankaj KumarNo ratings yet

- Set 2 MS, 2ND PBDocument10 pagesSet 2 MS, 2ND PBHarini NarayananNo ratings yet

- Solution To CVP ProblemsDocument8 pagesSolution To CVP ProblemsGizachew NadewNo ratings yet

- Solution Assignment Chapter 9 10 1Document14 pagesSolution Assignment Chapter 9 10 1Huynh Ng Quynh NhuNo ratings yet

- P1. PRO O.L Solution CMA September 2022 ExaminationDocument6 pagesP1. PRO O.L Solution CMA September 2022 ExaminationAwal ShekNo ratings yet

- F2 - Mock A - Answers-2-11 143Document10 pagesF2 - Mock A - Answers-2-11 143MD KaifNo ratings yet

- Answer Key 3Document8 pagesAnswer Key 3Hari prakarsh NimiNo ratings yet

- DK Goel Accountancy Solutions Class 12 Vol 1 Chapter 1Document4 pagesDK Goel Accountancy Solutions Class 12 Vol 1 Chapter 1AYUSHMAAN SAININo ratings yet

- 2023 24 Xii Pre Board 1 MsDocument13 pages2023 24 Xii Pre Board 1 MsacguptaclassesNo ratings yet

- Cpa Review School of The Philippines.2Document6 pagesCpa Review School of The Philippines.2Snow TurnerNo ratings yet

- 3.2 Yrs Proposal A Pay Back PeriodDocument3 pages3.2 Yrs Proposal A Pay Back PeriodAbdulmajed Unda MimbantasNo ratings yet

- EE - Assignment Chapter 9-10 SolutionDocument11 pagesEE - Assignment Chapter 9-10 SolutionXuân ThànhNo ratings yet

- Marking SchemeDocument6 pagesMarking Schemeraghu monnappaNo ratings yet

- Accountancy MSDocument13 pagesAccountancy MSJas Singh DevganNo ratings yet

- Solution Ultimate Sample Paper 4Document5 pagesSolution Ultimate Sample Paper 4Karthick KarthickNo ratings yet

- Final Practrice (Unit 4 and 5)Document9 pagesFinal Practrice (Unit 4 and 5)mjlNo ratings yet

- Hsslive Xii Acc 3 Admission of A Partner KeyDocument8 pagesHsslive Xii Acc 3 Admission of A Partner KeyShinu ShinadNo ratings yet

- Commerce Paathshaala: Pu-Ii Annual Examination April-May-2022 Accountancy Key Answers Section A (1 Mark Answers)Document12 pagesCommerce Paathshaala: Pu-Ii Annual Examination April-May-2022 Accountancy Key Answers Section A (1 Mark Answers)Ashok dore Ashok doreNo ratings yet

- 2 H077 BK 15 Numericals AssignmentDocument15 pages2 H077 BK 15 Numericals AssignmentIsha KatiyarNo ratings yet

- F2 - MOCK A - ANSWERS NowDocument11 pagesF2 - MOCK A - ANSWERS NowRoronoa ZoroNo ratings yet

- Discounted Cash Flow of ReturnDocument12 pagesDiscounted Cash Flow of ReturnTHE TERMINATORNo ratings yet

- Lecture 5 - 3Document7 pagesLecture 5 - 3ahmedgalalabdalbaath2003No ratings yet

- Study DK Goel Accountancy Class 12 - Volume 1 Chapter 3Document6 pagesStudy DK Goel Accountancy Class 12 - Volume 1 Chapter 3kamalpanjwani07No ratings yet

- MS Accountancy XIIDocument8 pagesMS Accountancy XIITûshar ThakúrNo ratings yet

- Untitled DocumentDocument3 pagesUntitled DocumentPratham sadanaNo ratings yet

- Quiz 1 Answers and Solutions (Partnership Formation and Operation)Document6 pagesQuiz 1 Answers and Solutions (Partnership Formation and Operation)cpacpacpaNo ratings yet

- Problem Set 005 Q AnswersDocument5 pagesProblem Set 005 Q AnswersDennis Korir100% (1)

- CPA Review School of The Philippines ManilaDocument4 pagesCPA Review School of The Philippines ManilaSophia PerezNo ratings yet

- Paper2 Set2 SolutionDocument7 pagesPaper2 Set2 Solutionadityatiwari122006No ratings yet

- Solutions 6352 To 6372Document33 pagesSolutions 6352 To 6372river garciaNo ratings yet

- Marking Scheme 2020Document5 pagesMarking Scheme 2020Joanna GarciaNo ratings yet

- Advanced Financial AccountingDocument4 pagesAdvanced Financial AccountingBhavi GolchhaNo ratings yet

- Bajaj Finserv Investor Presentation - Q2 FY2018-19Document19 pagesBajaj Finserv Investor Presentation - Q2 FY2018-19AmarNo ratings yet

- Investment Decision TheoryDocument71 pagesInvestment Decision TheorykaranvishweshsharmaNo ratings yet

- Solved Pu 2 Annual QP Accountancy 2024Document10 pagesSolved Pu 2 Annual QP Accountancy 2024tommyvercetti880055No ratings yet

- Engineering Economy Solution of HW2: Exercise 1Document5 pagesEngineering Economy Solution of HW2: Exercise 1Moe ShNo ratings yet

- ParCor Chapter 3 - Hernandez - BSA 1-1 PDFDocument11 pagesParCor Chapter 3 - Hernandez - BSA 1-1 PDFBSA 1-1No ratings yet

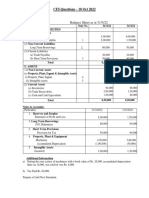

- CFS Format - Oct 2022Document2 pagesCFS Format - Oct 2022Kartik SujanNo ratings yet

- Xii Ip Labworksheet-5Document1 pageXii Ip Labworksheet-5Kartik SujanNo ratings yet

- Kartik Business ProjectDocument11 pagesKartik Business ProjectKartik SujanNo ratings yet

- Xii Ip Labworksheet-2Document1 pageXii Ip Labworksheet-2Kartik SujanNo ratings yet

- Xii Ip Labworksheet-1Document2 pagesXii Ip Labworksheet-1Kartik SujanNo ratings yet

- Xii Ip Labworksheet-4Document2 pagesXii Ip Labworksheet-4Kartik SujanNo ratings yet

- Kartik Lab Assignment DocumentedDocument75 pagesKartik Lab Assignment DocumentedKartik SujanNo ratings yet

- CFS - 18 Oct 2022Document11 pagesCFS - 18 Oct 2022Kartik SujanNo ratings yet

- CFS Questions - 18 - OCT - 2022Document5 pagesCFS Questions - 18 - OCT - 2022Kartik SujanNo ratings yet

- The Transactions Completed by Dancin Music During April 2008 WerDocument2 pagesThe Transactions Completed by Dancin Music During April 2008 WerAmit PandeyNo ratings yet

- The District Cooperative Central Bank LTD., Medak H.O. SangareddyDocument2 pagesThe District Cooperative Central Bank LTD., Medak H.O. SangareddyPonnam VenkateshamNo ratings yet

- Shipping Corporation of India: Project Report OnDocument6 pagesShipping Corporation of India: Project Report OnAnuj BhagatNo ratings yet

- Victor Kimutai Bank StatementDocument2 pagesVictor Kimutai Bank StatementVictor KimutaiNo ratings yet

- PassbookDocument42 pagesPassbookCharles OkwalingaNo ratings yet

- Sample Questions BMS SEM VI Orderwise PDFDocument41 pagesSample Questions BMS SEM VI Orderwise PDFAasim TajNo ratings yet

- Mr. Tibbs & Mr. Finch - HO InsuranceDocument6 pagesMr. Tibbs & Mr. Finch - HO InsuranceAlex RobertsNo ratings yet

- 3 Financial RatiosDocument29 pages3 Financial RatiosAB12P1 Sanchez Krisly AngelNo ratings yet

- Accounting Dr. Ashraf Lecture 02 PDFDocument24 pagesAccounting Dr. Ashraf Lecture 02 PDFMahmoud AbdullahNo ratings yet

- Exon Mobile Financial Data BloombergDocument32 pagesExon Mobile Financial Data BloombergShardul MudeNo ratings yet

- Application No./RECEIPT No: Receipt DateDocument1 pageApplication No./RECEIPT No: Receipt DateAnil kadamNo ratings yet

- Credit Cards TruistDocument1 pageCredit Cards TruistKerry HawkNo ratings yet

- SSM - pr191007 Annex 537c259b6d.enDocument41 pagesSSM - pr191007 Annex 537c259b6d.enPhanAnhNguyenNo ratings yet

- 2019 CFA LIII MockExamA-AM (With Solution)Document63 pages2019 CFA LIII MockExamA-AM (With Solution)Joseph MakNo ratings yet

- Valuation of SharesDocument23 pagesValuation of SharesRuchi SharmaNo ratings yet

- MUDRA - The Road Ahead ..: Jiji Mammen, Ceo, MudraDocument20 pagesMUDRA - The Road Ahead ..: Jiji Mammen, Ceo, MudraAbhishek RastogiNo ratings yet

- Assets & Liabilities Committee Report: Performance Management & MonitoringDocument15 pagesAssets & Liabilities Committee Report: Performance Management & MonitoringMichael OseleNo ratings yet

- ADJUSTING ENTRIES PPT Examples and ActivityDocument14 pagesADJUSTING ENTRIES PPT Examples and Activitytamorromeo908No ratings yet

- 01 ABM Financial Accounting Session1Document36 pages01 ABM Financial Accounting Session1DentatusNo ratings yet

- Ifrs s2 - Spanish VersionDocument37 pagesIfrs s2 - Spanish VersionComunicarSe-ArchivoNo ratings yet

- 7 - Co-Operative AccountingDocument4 pages7 - Co-Operative AccountingGaurav Chandrakant100% (1)

- Case Study On Bear StearnsDocument13 pagesCase Study On Bear StearnsBrayanJosueReyesHerreraNo ratings yet

- Mock Test (2018-19) For Clerical To Trainee Officer and JMGS-IDocument15 pagesMock Test (2018-19) For Clerical To Trainee Officer and JMGS-IRamachandran MNo ratings yet

- Comprehensive Study On The Product of Kotak Mahindra Life InsuranceDocument73 pagesComprehensive Study On The Product of Kotak Mahindra Life InsuranceMadhuKar RaiNo ratings yet

- Problem 7 - 6 & 7Document2 pagesProblem 7 - 6 & 7Micah April SabularseNo ratings yet

- Red Flags in Financial AnalysisDocument15 pagesRed Flags in Financial AnalysisHedayatullah PashteenNo ratings yet

- Accounting Formula Cheat SheetDocument1 pageAccounting Formula Cheat SheetMarta Fdez-FournierNo ratings yet

- LIC - Jeevan TarunDocument1 pageLIC - Jeevan TarunPraveen Kumar KNo ratings yet

- 10 Chapter 2Document42 pages10 Chapter 2sanjeet chhikaraNo ratings yet

- Description: Tags: 2001LendersRatesFY01Document33 pagesDescription: Tags: 2001LendersRatesFY01anon-222095No ratings yet