You might also like

- Adjustments:: Outstanding/Prepaid ExpenditureDocument25 pagesAdjustments:: Outstanding/Prepaid ExpenditureParag DhandeNo ratings yet

- SYJCBKLMRDocument33 pagesSYJCBKLMRghostinhouse223No ratings yet

- KanchuDocument1 pageKanchukanchi sharmaNo ratings yet

- S.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDocument11 pagesS.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDheer BhanushaliNo ratings yet

- Cash BookDocument3 pagesCash Bookchandan YNo ratings yet

- Kendriya Vidyalaya Sangathan Jaipur Region: Last Minutes Revision Material Subject: AccountancyDocument20 pagesKendriya Vidyalaya Sangathan Jaipur Region: Last Minutes Revision Material Subject: AccountancyMohd AyazNo ratings yet

- Chapter 04 - Income Tax Schemes, Accounting Periods, Methods, and ReportingDocument2 pagesChapter 04 - Income Tax Schemes, Accounting Periods, Methods, and ReportingZen SantosNo ratings yet

- INCOMPLETE RECORDS O LevelDocument5 pagesINCOMPLETE RECORDS O LevelRECALL JIRIVENGWA100% (1)

- Appendix 20 - Sabudb - Far 2Document1 pageAppendix 20 - Sabudb - Far 2pdmu regionixNo ratings yet

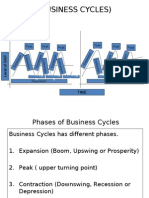

- (Business Cycles) : Throug H Throug H Throug H Throug H Throug H ThroughDocument10 pages(Business Cycles) : Throug H Throug H Throug H Throug H Throug H ThroughPrachi ChaudharyNo ratings yet

- A Invoices:: DvanceDocument6 pagesA Invoices:: DvanceAishwarya PillaiNo ratings yet

- Profit Total (Incomes + Gains) Total (Expenses + Losses)Document12 pagesProfit Total (Incomes + Gains) Total (Expenses + Losses)Daya AnandNo ratings yet

- Salary Tds Computation Sheet Sec 192bDocument1 pageSalary Tds Computation Sheet Sec 192bpradhan13No ratings yet

- Catherinebernabeabad: Page1of3 Blk4Lot10Azurestpacita2Bsan 6 3 9 5 - 0 6 4 2 - 0 5 Pedrolaguna Lagunasanpedro 4 0 2 3Document6 pagesCatherinebernabeabad: Page1of3 Blk4Lot10Azurestpacita2Bsan 6 3 9 5 - 0 6 4 2 - 0 5 Pedrolaguna Lagunasanpedro 4 0 2 3aldrin lapitanNo ratings yet

- Accountancy All FormulaDocument23 pagesAccountancy All FormulaThe Unknown vlogger100% (1)

- Balance Sheet NotesDocument4 pagesBalance Sheet NotesAudrey RolandNo ratings yet

- Financial Statements Receipts & Payments A/c Income & Expenditure A/c Balance SheetDocument14 pagesFinancial Statements Receipts & Payments A/c Income & Expenditure A/c Balance SheetAnita YadavNo ratings yet

- Accounts of Clubs and SocietiesDocument5 pagesAccounts of Clubs and SocietiesJunaid Islam100% (1)

- S A 20190625Document4 pagesS A 20190625Mary Ann Gamela IturiagaNo ratings yet

- 09 Lecture Notes - Trust Accounts 2021Document16 pages09 Lecture Notes - Trust Accounts 2021Chamela MahiepalaNo ratings yet

- Final Accounts: PruningDocument27 pagesFinal Accounts: PruningSarmad Sadiq E4 42No ratings yet

- Accounting Procedures-Rules of Debit and CreditDocument14 pagesAccounting Procedures-Rules of Debit and CreditDevam junejaNo ratings yet

- Partnership Final Accounts PDFDocument97 pagesPartnership Final Accounts PDFKaushik Patel75% (4)

- Edilbertotalegatojr: Page1of4 Barangayzone4Talisaycity 9 1 8 9 - 1 6 1 6 - 4 3 Negrosoccidentaltalisay 6 1 1 5Document4 pagesEdilbertotalegatojr: Page1of4 Barangayzone4Talisaycity 9 1 8 9 - 1 6 1 6 - 4 3 Negrosoccidentaltalisay 6 1 1 5Arthus TernalNo ratings yet

- YourShare Winter 2010Document8 pagesYourShare Winter 2010Oklahoma Employees Credit UnionNo ratings yet

- Solution Final Mock Paper (Sure Shot Questions) Class 12 - AccountancyDocument10 pagesSolution Final Mock Paper (Sure Shot Questions) Class 12 - AccountancyPratik PrakashNo ratings yet

- VOUCHER StaffNurse 241Document1 pageVOUCHER StaffNurse 241MIR SARTAJNo ratings yet

- Revenue Memorandum Circular No. 016-13: February 8, 2013 February 8, 2013Document2 pagesRevenue Memorandum Circular No. 016-13: February 8, 2013 February 8, 2013Ravenclaws91No ratings yet

- Elc - Acc113 - CH 11 - SM - 2nd SemDocument19 pagesElc - Acc113 - CH 11 - SM - 2nd SemAlmaali BookshopNo ratings yet

- KFS MdaDocument2 pagesKFS MdaMohsinNo ratings yet

- Solicitor's Accounts EnglishDocument7 pagesSolicitor's Accounts EnglishDananjaya RajapakshaNo ratings yet

- Sa20190515 PDFDocument4 pagesSa20190515 PDFMitess Boñon BrusolaNo ratings yet

- 4 General Accounts of Partnership FirmDocument16 pages4 General Accounts of Partnership FirmNisarga T DaryaNo ratings yet

- Dasal Sa PilgrimageDocument4 pagesDasal Sa PilgrimageMabel SantosNo ratings yet

- Form12BB FY2324Document6 pagesForm12BB FY2324manjushivaramNo ratings yet

- S A 20190623Document4 pagesS A 20190623Ralph Bernard Dela RosaNo ratings yet

- New FileDocument3 pagesNew Filesatya8851691224No ratings yet

- Collections Draftv1Document1 pageCollections Draftv1Dayward BorjaNo ratings yet

- Format Subscription Account SubscriptionDocument1 pageFormat Subscription Account SubscriptionAdeena0% (1)

- 01A Flows of Economic ActivitiesDocument7 pages01A Flows of Economic ActivitiesGaurav GhareNo ratings yet

- E 5 e 55 Fbae 4Document4 pagesE 5 e 55 Fbae 4Faye Isabelle SantiagoNo ratings yet

- 02 Partnership Final AccountsDocument43 pages02 Partnership Final AccountsroyNo ratings yet

- Far Ra 10964 - ExendedDocument33 pagesFar Ra 10964 - ExendedKenneth Cyrus OlivarNo ratings yet

- Financial StatementDocument19 pagesFinancial StatementCS SNo ratings yet

- Account CurrentDocument13 pagesAccount Currentfathima.comafug23No ratings yet

- Format of Trading Profit Loss Account Balance Sheet PDFDocument6 pagesFormat of Trading Profit Loss Account Balance Sheet PDFsonika7100% (1)

- Challan Form: Challan Form Provincial Challan Form Provincial Original Challan Form ProvincialDocument1 pageChallan Form: Challan Form Provincial Challan Form Provincial Original Challan Form ProvincialShaIzMuhammadNo ratings yet

- New John V ExDocument1 pageNew John V Exxfzm99mr8rNo ratings yet

- Payment Form: Kawanihan NG Rentas InternasDocument8 pagesPayment Form: Kawanihan NG Rentas InternasChieMae Benson QuintoNo ratings yet

- CA20191216Document4 pagesCA20191216DonaldDeLeonNo ratings yet

- Adobe Scan Jun 30, 2023Document2 pagesAdobe Scan Jun 30, 2023peninahkiraboNo ratings yet

- Revenues and Costs Plus Sources of FinanceDocument3 pagesRevenues and Costs Plus Sources of FinancesabinaNo ratings yet

- Account Determination MM en PKDocument27 pagesAccount Determination MM en PKHammad KahnNo ratings yet

- T1DF PBM IBM Payer Manufacturer Map 2017.03.01Document1 pageT1DF PBM IBM Payer Manufacturer Map 2017.03.01The Type 1 Diabetes Defense FoundationNo ratings yet

- LIVE Financial Analysis - Marketing - Blackbrick Sandton 1 ShortstayDocument2 pagesLIVE Financial Analysis - Marketing - Blackbrick Sandton 1 Shortstayzimk.careNo ratings yet

- CMAINTER SelfBalLedgDocument13 pagesCMAINTER SelfBalLedgnobi85804No ratings yet

- Trial Balance and Rectification of Errors Class 11 NotesDocument43 pagesTrial Balance and Rectification of Errors Class 11 NotesAkhil SaxenaNo ratings yet

- G. Statement of Receipts and DisbursementsDocument2 pagesG. Statement of Receipts and DisbursementsMark LopezNo ratings yet

- Defining Globalization Through FriendshipDocument18 pagesDefining Globalization Through FriendshipRachel PetersNo ratings yet

- Answer:: Business Process Reengineering Interview QuestionsDocument22 pagesAnswer:: Business Process Reengineering Interview QuestionsShahedul IslamNo ratings yet

- DLL FABM Week17Document3 pagesDLL FABM Week17sweetzelNo ratings yet

- Evoe MarketingDocument1 pageEvoe MarketingSwapnil NagareNo ratings yet

- Doles Vs AngelesDocument2 pagesDoles Vs Angelesfermo ii ramosNo ratings yet

- Group 9 Eabdm s13Document3 pagesGroup 9 Eabdm s13DIOUF SHAJAHAN K TNo ratings yet

- Hypothesis-Driven DevelopmentDocument2 pagesHypothesis-Driven DevelopmentMuhammad El-FahamNo ratings yet

- Zudio Marketing PlanDocument2 pagesZudio Marketing PlanAmir KhanNo ratings yet

- Representation ContractDocument5 pagesRepresentation ContractJhoAn RaMosNo ratings yet

- High Low MethodDocument4 pagesHigh Low MethodSamreen LodhiNo ratings yet

- Semper Avanti - InfopackDocument9 pagesSemper Avanti - InfopackFlorinel Valentin AlbuNo ratings yet

- Operations Management (Zheng) SU2016 PDFDocument9 pagesOperations Management (Zheng) SU2016 PDFdarwin12No ratings yet

- Understanding Mergers and Acquisitions (M&A) Introduction: Mergers and Acquisitions (M&A) Are Complex Financial Transactions That InvolveDocument2 pagesUnderstanding Mergers and Acquisitions (M&A) Introduction: Mergers and Acquisitions (M&A) Are Complex Financial Transactions That InvolveSebastian StolkinerNo ratings yet

- Zambia National Commercial Bank PLC ProspectusDocument104 pagesZambia National Commercial Bank PLC ProspectusBilly LeeNo ratings yet

- Individual Assigment 1 - Enterpreneurship - Yosef Budiman - JB200230Document10 pagesIndividual Assigment 1 - Enterpreneurship - Yosef Budiman - JB200230Yosef Budiman yosefbudiman.2020No ratings yet

- Solved - Shown in The Figure Below Is A Simplified Dynamic ...Document2 pagesSolved - Shown in The Figure Below Is A Simplified Dynamic ...juenkkinNo ratings yet

- Just Dial Limited Letter of OfferDocument68 pagesJust Dial Limited Letter of Offervarun_bhuNo ratings yet

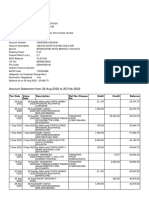

- Bank StatementDocument5 pagesBank StatementSANJIB GHOSHNo ratings yet

- Módulo 22: Pasivos y Patrimonio: Fundación IFRS: Material de Formación Sobre LaDocument64 pagesMódulo 22: Pasivos y Patrimonio: Fundación IFRS: Material de Formación Sobre LaDAYANA ANDREA DAMS MOLINANo ratings yet

- 1.10 International Organization NewDocument14 pages1.10 International Organization NewArbind YadavNo ratings yet

- Sales Order FormDocument1 pageSales Order FormDeepthireddyNo ratings yet

- Irrevocable Letter of CreditDocument1 pageIrrevocable Letter of CreditJunvy AbordoNo ratings yet

- How To Become An EntrepreneurDocument4 pagesHow To Become An EntrepreneurAndrej DimovskiNo ratings yet

- EContent 1 2023 06 24 10 20 29 QTDM Studymaterialfeb23pdf 2023 03 15 11 44 02Document23 pagesEContent 1 2023 06 24 10 20 29 QTDM Studymaterialfeb23pdf 2023 03 15 11 44 02Tom CruiseNo ratings yet

- Amigo Manufacturing V. Cluett Peabody CoDocument3 pagesAmigo Manufacturing V. Cluett Peabody CoShiela Arboleda MagnoNo ratings yet

- 773531Document38 pages773531Mohammed Khaja MohinuddinNo ratings yet

- Sample Copy - Mphasis &finsource PDFDocument2 pagesSample Copy - Mphasis &finsource PDFSameer ShaikhNo ratings yet

- Business Management - Study and Revision Guide - Paul Hoang - Hodder 2016Document194 pagesBusiness Management - Study and Revision Guide - Paul Hoang - Hodder 2016Cecy Vallejo LeónNo ratings yet

- Final Exam Theories ValuationDocument6 pagesFinal Exam Theories ValuationBLN-Hulo- Ronaldo M. Valdez SRNo ratings yet

- Grade 8 Term 1 NotesDocument26 pagesGrade 8 Term 1 NotesShadow WalkerNo ratings yet