You might also like

- 2019 Vol 1 CH 5 AnswersDocument21 pages2019 Vol 1 CH 5 AnswersArkhie Davocol80% (5)

- Estimation of Doubtful Accounts: Problem 12-1 (AICPA Adapted)Document15 pagesEstimation of Doubtful Accounts: Problem 12-1 (AICPA Adapted)Janine Lerum100% (2)

- Tugas 4 - AkuntansiDocument3 pagesTugas 4 - AkuntansiYusuf HadiNo ratings yet

- Acc2202 w21 Excel Assignment 1 Student File FinalDocument10 pagesAcc2202 w21 Excel Assignment 1 Student File FinalHao FanNo ratings yet

- (Module 4) ProblemsDocument6 pages(Module 4) ProblemsYanie Dela Cruz100% (1)

- ADJUSTING ENTRIES Answer QUIZ ACCRUALS & DEFERRALSDocument5 pagesADJUSTING ENTRIES Answer QUIZ ACCRUALS & DEFERRALSHassanhor Guro BacolodNo ratings yet

- National Economics University assignment on financial statementsDocument7 pagesNational Economics University assignment on financial statementsLuna LeeNo ratings yet

- San Beda College Alabang: INSTRUCTION: Worksheet PreparationDocument1 pageSan Beda College Alabang: INSTRUCTION: Worksheet PreparationMarriel Fate CullanoNo ratings yet

- Types and techniques of reinsurance: proportional, non-proportional, facultative, treatyDocument21 pagesTypes and techniques of reinsurance: proportional, non-proportional, facultative, treatyradhay mahajan100% (2)

- Good Loan Policy Sample BankDocument57 pagesGood Loan Policy Sample Bankdetri100% (3)

- Adjusting entries and financial statements for Praca General ServicesDocument45 pagesAdjusting entries and financial statements for Praca General ServicesKarla pauline BernasNo ratings yet

- Accumulated Depreciation - Office Equipment: Date Description P/ R Debit CreditDocument3 pagesAccumulated Depreciation - Office Equipment: Date Description P/ R Debit CreditAllyza WinonaNo ratings yet

- Financial Accounting & Reporting 2: Sec - 7 - Short Quiz 1 SolutionDocument4 pagesFinancial Accounting & Reporting 2: Sec - 7 - Short Quiz 1 SolutionDump DumpNo ratings yet

- Adjusting Entries for Uncollectible AccountsDocument6 pagesAdjusting Entries for Uncollectible AccountsKristine IvyNo ratings yet

- Advanced 1Document90 pagesAdvanced 1NhicoleChoiNo ratings yet

- University of Luzon College of Accountancy Adjusting EntriesDocument91 pagesUniversity of Luzon College of Accountancy Adjusting EntriestaurusNo ratings yet

- Midterm Exam-Adjusting EntriesDocument5 pagesMidterm Exam-Adjusting EntriesHassanhor Guro BacolodNo ratings yet

- University of Luzon College of Accountancy Adjusting EntriesDocument91 pagesUniversity of Luzon College of Accountancy Adjusting EntriesIL MareNo ratings yet

- Asm 2 AcDocument19 pagesAsm 2 AcNguyen Duc Quang (BTEC HN)No ratings yet

- Assignment 3 - Financial Accounting - February 4Document7 pagesAssignment 3 - Financial Accounting - February 4Ednalyn PascualNo ratings yet

- Pre-Assessment ReviewDocument6 pagesPre-Assessment ReviewKelly TesoreroNo ratings yet

- ACCTG1 PrefinalsDocument23 pagesACCTG1 PrefinalsJAN RAY CUISON VISPERAS100% (1)

- Of Alabang Inc.: Prelim Examination Bsa 32E1Document16 pagesOf Alabang Inc.: Prelim Examination Bsa 32E1Genevieve VargasNo ratings yet

- LENNYDocument4 pagesLENNYKim FloresNo ratings yet

- Date Description PR Debit Credit Dec - 31 1. Prepaid InsuranceDocument4 pagesDate Description PR Debit Credit Dec - 31 1. Prepaid InsuranceJackie EasterNo ratings yet

- Investment in Associate ExercisesDocument7 pagesInvestment in Associate ExercisesJo KeNo ratings yet

- AUDP DIS02 Receivables Key-AnswersDocument7 pagesAUDP DIS02 Receivables Key-AnswersKristina KittyNo ratings yet

- Accounting ExamDocument14 pagesAccounting ExamSally SalehNo ratings yet

- Asm 2 Ac Tiếng Anh FullDocument23 pagesAsm 2 Ac Tiếng Anh FullNguyen Duc Quang (BTEC HN)No ratings yet

- Prepare financial statementsDocument4 pagesPrepare financial statementsxiu yingNo ratings yet

- IA2 Quiz1 (ANTIDO)Document4 pagesIA2 Quiz1 (ANTIDO)Claire Magbunag AntidoNo ratings yet

- Answer Key - Quizzer On AJEDocument2 pagesAnswer Key - Quizzer On AJEClarissa De GuzmanNo ratings yet

- APPLIED AUDITING PRELIM EXAMDocument9 pagesAPPLIED AUDITING PRELIM EXAMChristopher NogotNo ratings yet

- Review of Accounting Cycle Review of Accounting CycleDocument4 pagesReview of Accounting Cycle Review of Accounting CycleJerome BaluseroNo ratings yet

- Adjusting Journal EntriesDocument3 pagesAdjusting Journal EntriesZonio Nina Bonita T.No ratings yet

- ADJUSTING Activities With AnswersDocument5 pagesADJUSTING Activities With AnswersRenz RaphNo ratings yet

- Current Liabilities - PROBLEMSDocument11 pagesCurrent Liabilities - PROBLEMSIra Grace De Castro100% (2)

- Solutions - LiabilitiesDocument10 pagesSolutions - LiabilitiesjhobsNo ratings yet

- Top Education Adjusted Trial BalanceDocument9 pagesTop Education Adjusted Trial BalanceAN HỒ QUÝNo ratings yet

- Tutorial On AdjustmentsDocument8 pagesTutorial On AdjustmentsPushpa ValliNo ratings yet

- Republic of The Philippines: Final Project on Simple and Compound Interest RatesDocument11 pagesRepublic of The Philippines: Final Project on Simple and Compound Interest RatesTimothy LeomoNo ratings yet

- Chapter 3 exercisesDocument8 pagesChapter 3 exercisesNguyen Khanh Ly K17 HLNo ratings yet

- E3-5 (LO 3) Adjusting Entries: InstructionsDocument6 pagesE3-5 (LO 3) Adjusting Entries: InstructionsAntonios Fahed0% (1)

- Midterm Review QuestionsDocument19 pagesMidterm Review Questionschiji chzzzmeowNo ratings yet

- BSA2201 BDD MBCarolino M8Activityno.2Document5 pagesBSA2201 BDD MBCarolino M8Activityno.2Earl Carolino100% (1)

- Carl Jake Lastimosa Grade 12 Abm IX. Adjusting Journal EntriesDocument3 pagesCarl Jake Lastimosa Grade 12 Abm IX. Adjusting Journal EntriesCarl Jake LastimosaNo ratings yet

- Assignment Chapter 3 Problem 1 SolutionDocument13 pagesAssignment Chapter 3 Problem 1 SolutionMUHAMMAD AMMAD ARSHADNo ratings yet

- 2019 Vol 1 CH 5 AnswersDocument23 pages2019 Vol 1 CH 5 AnswersDummy Number 2No ratings yet

- Adjusting Entries for Cesar Cifra Accounting FirmDocument3 pagesAdjusting Entries for Cesar Cifra Accounting FirmJohn CalvinNo ratings yet

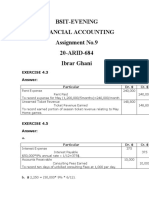

- BSIT-EVENING Financial Accounting Assignment SolutionsDocument3 pagesBSIT-EVENING Financial Accounting Assignment Solutionsibrar ghani100% (1)

- ACC01B1 REK1B01 MAIN.pdfDocument10 pagesACC01B1 REK1B01 MAIN.pdfLebohang NgubaneNo ratings yet

- Problem 5Document3 pagesProblem 5Rudy LugasNo ratings yet

- ReviewDocument38 pagesReviewFiana DolinogNo ratings yet

- FAR 01Q Review of Accounting Cycle QuizDocument4 pagesFAR 01Q Review of Accounting Cycle Quizbyunb3617No ratings yet

- Answer Key - Problem Sets - Adjusting EntriesDocument2 pagesAnswer Key - Problem Sets - Adjusting EntriesAlexa AbaryNo ratings yet

- Resa Afar 1Document26 pagesResa Afar 1Princess JoannaNo ratings yet

- INTACC RECEIVABLESDocument9 pagesINTACC RECEIVABLESaugustokita5No ratings yet

- Solution Chapter 20 Intermediate Accounting ValixDocument5 pagesSolution Chapter 20 Intermediate Accounting Valixnameless0% (1)

- Brief ExercisesDocument13 pagesBrief ExercisesPhuong Ngo Tran QuynhNo ratings yet

- Pe2 SolutionDocument3 pagesPe2 SolutionRiezel PepitoNo ratings yet

- Answers To Handout 1 Financial AccountingDocument40 pagesAnswers To Handout 1 Financial AccountingMohand ElbakryNo ratings yet

- PricewaterhouseCoopers' Guide to the New Tax RulesFrom EverandPricewaterhouseCoopers' Guide to the New Tax RulesNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Audit ReportDocument71 pagesAudit ReportShruth ShahNo ratings yet

- Zarah Notes Insurance LawDocument32 pagesZarah Notes Insurance LawTinn ApNo ratings yet

- Suvigya: Details Furnished by You WereDocument1 pageSuvigya: Details Furnished by You WereMKMK JilaniNo ratings yet

- Finance Modeling Handbook (00000002)Document1 pageFinance Modeling Handbook (00000002)baronfgfNo ratings yet

- Manage your LANDBANK accounts online with iAccessDocument2 pagesManage your LANDBANK accounts online with iAccessMay Elaine BelgadoNo ratings yet

- Schedule Yuran Sem 1 Sesi 20202021 MBADocument1 pageSchedule Yuran Sem 1 Sesi 20202021 MBAM NaszriNo ratings yet

- AJE QuizDocument4 pagesAJE QuizJohn cookNo ratings yet

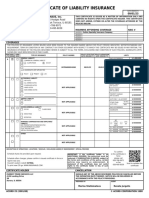

- Certificate of Liability Insurance: 17w045 Hodges Road Oakbrook Terrace, IL-60181 PH: 630-786-9971 Fax: 630-495-6039Document1 pageCertificate of Liability Insurance: 17w045 Hodges Road Oakbrook Terrace, IL-60181 PH: 630-786-9971 Fax: 630-495-6039arnur.toksanbay24No ratings yet

- Discussion QuestionsDocument22 pagesDiscussion QuestionsAndhikaa Nesansa NNo ratings yet

- Example - Seminar - Audit - CommunicationDocument7 pagesExample - Seminar - Audit - CommunicationmindpinkNo ratings yet

- 629 19PCM10 19PCZ09 Mcom Mcom CA 05 02 2022 FNDocument19 pages629 19PCM10 19PCZ09 Mcom Mcom CA 05 02 2022 FNMukesh kannan MahiNo ratings yet

- Rift Valley University Geda Campus Post Graduate Program Masters of Business Administration (MBA) Accounting For Managers Individual AssignmentDocument7 pagesRift Valley University Geda Campus Post Graduate Program Masters of Business Administration (MBA) Accounting For Managers Individual Assignmentgenemu fejoNo ratings yet

- Lesson 5 Statement of Cash FlowsDocument8 pagesLesson 5 Statement of Cash FlowsklipordNo ratings yet

- Retail LoansDocument3 pagesRetail LoansMonisha Bhatia0% (1)

- RDocument2 pagesRMukesh ManwaniNo ratings yet

- List of Investment Banks-UKDocument5 pagesList of Investment Banks-UKnnaemekenNo ratings yet

- Gujarat Technological UniversityDocument2 pagesGujarat Technological UniversitySaR aSNo ratings yet

- Mutual Fund Investment From An Individual's PerspectiveDocument89 pagesMutual Fund Investment From An Individual's PerspectiveSAJIDA SHAIKHNo ratings yet

- FINAL Ceilli English 20142015Document126 pagesFINAL Ceilli English 20142015Cheong Weng ChoyNo ratings yet

- Internship Report On UBLDocument45 pagesInternship Report On UBLWajid Ali100% (1)

- UBS & CS Merger PresentationDocument12 pagesUBS & CS Merger PresentationBilly LeeNo ratings yet

- CA Foundation June 23 BRS Problem - CTC ClassesDocument2 pagesCA Foundation June 23 BRS Problem - CTC ClassesMohit SharmaNo ratings yet

- Canara BankDocument6 pagesCanara Bankannu priyaNo ratings yet

- Gen - MathDocument4 pagesGen - MathJudith DelRosario De RoxasNo ratings yet

- BOP GUIDEDocument9 pagesBOP GUIDESujataNo ratings yet

- Article IFRS 3 Business Combinations PDFDocument14 pagesArticle IFRS 3 Business Combinations PDFEhsanulNo ratings yet

- Life insurance basics and applications report summaryDocument41 pagesLife insurance basics and applications report summaryIshika ThakurNo ratings yet