You might also like

- Hampton Suggested AnswersDocument5 pagesHampton Suggested Answersenkay12100% (3)

- Fat Test (Jawaban)Document19 pagesFat Test (Jawaban)Carat ForeverNo ratings yet

- Cash Flow Analysis and StatementDocument127 pagesCash Flow Analysis and Statementsnhk679546100% (6)

- Accounting Test TravelokaDocument8 pagesAccounting Test TravelokaGabriella CikaNo ratings yet

- General Ledger Account Number Account Title January 1 Opening BalanceDocument31 pagesGeneral Ledger Account Number Account Title January 1 Opening BalanceKim FloresNo ratings yet

- Adjusting EntriesDocument38 pagesAdjusting EntriesKae Abegail GarciaNo ratings yet

- 1210 B C A T A (1071)Document6 pages1210 B C A T A (1071)rindah100% (3)

- HW 7Document2 pagesHW 7Mishalm96No ratings yet

- Part B - Equitable Treatment of ShareholdersDocument12 pagesPart B - Equitable Treatment of ShareholdersYogaNo ratings yet

- Adjusting The Records: Bookkeeping Nciii Training CourseDocument46 pagesAdjusting The Records: Bookkeeping Nciii Training CourseKim Audrey JalalainNo ratings yet

- Casos de Ajuste.Document9 pagesCasos de Ajuste.Alguien algunoNo ratings yet

- 4281554Document6 pages4281554mohitgaba19No ratings yet

- Prepare Adjusting Entry - Accounting in ActionDocument3 pagesPrepare Adjusting Entry - Accounting in ActionJabbar aqwanNo ratings yet

- 7 - ACCOUNTING CYCLE STEP 4 - ADJUSTING ENTRIES and ADJUSTED TRIAL BALANCE PREPDocument5 pages7 - ACCOUNTING CYCLE STEP 4 - ADJUSTING ENTRIES and ADJUSTED TRIAL BALANCE PREPBataknese ArtsNo ratings yet

- Fabm 1 - 6 1Document10 pagesFabm 1 - 6 1awitakintoNo ratings yet

- Revision SolutionsDocument10 pagesRevision SolutionsHan Hung GiaNo ratings yet

- Accrual & PrepaymentsDocument4 pagesAccrual & PrepaymentsronstarcaristaNo ratings yet

- MerchandisingDocument11 pagesMerchandisingAIRA NHAIRE MECATE100% (1)

- MerchandisingDocument11 pagesMerchandisingAIRA NHAIRE MECATE100% (1)

- Fatimatuz Zahro - Exercise CHP 8 Dan 9Document6 pagesFatimatuz Zahro - Exercise CHP 8 Dan 9Fatimatuz ZahroNo ratings yet

- Accounting Cycle Exercises IIIDocument25 pagesAccounting Cycle Exercises IIIzelalem kumiNo ratings yet

- Accruals and Deferral Chapter 4 ExercisesDocument6 pagesAccruals and Deferral Chapter 4 ExercisesSiraj KabbaraNo ratings yet

- Session 25 Accruals, Prepayments and Other Adjustments For Financial StatementsDocument10 pagesSession 25 Accruals, Prepayments and Other Adjustments For Financial Statementsol.iv.e.a.gui.l.ar412No ratings yet

- 1st AssignmentDocument12 pages1st AssignmentAnonymous f7wV1lQKRNo ratings yet

- Problem 1: CSA 200 Z.Samlal, Mba, Cfa & PHDDocument8 pagesProblem 1: CSA 200 Z.Samlal, Mba, Cfa & PHDallijahNo ratings yet

- BUS 142 - Exercises CH 8Document22 pagesBUS 142 - Exercises CH 8Jess IcaNo ratings yet

- ACT72 Closingentries OnlinenotesDocument3 pagesACT72 Closingentries OnlinenotesHimanshuNo ratings yet

- Chap 3 & 4 Handout V2015Document12 pagesChap 3 & 4 Handout V2015Julz JuliaNo ratings yet

- BUS 591 WK 6 Template - 092417Document43 pagesBUS 591 WK 6 Template - 092417kapil sharma100% (2)

- Chapter 8Document6 pagesChapter 8swaroopcharmiNo ratings yet

- ACCA F3 CH#10: Accruals and Prepayments NotesDocument26 pagesACCA F3 CH#10: Accruals and Prepayments NotesMuhammad AzamNo ratings yet

- Chapter 10 - Adjusting The RecordsDocument24 pagesChapter 10 - Adjusting The RecordsJesseca JosafatNo ratings yet

- Template Jawaban UTS Aplikasi Audit Ganjil 20Document14 pagesTemplate Jawaban UTS Aplikasi Audit Ganjil 20Steven TanNo ratings yet

- CH 02Document4 pagesCH 02flrnciairnNo ratings yet

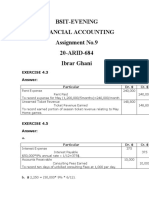

- Bsit-Evening Financial Accounting Assignment No.9 20-ARID-684 Ibrar GhaniDocument3 pagesBsit-Evening Financial Accounting Assignment No.9 20-ARID-684 Ibrar Ghaniibrar ghani100% (1)

- Module 5 Answer KeysDocument5 pagesModule 5 Answer KeysJaspreetNo ratings yet

- May 2018 and 2017 SolutionsDocument43 pagesMay 2018 and 2017 SolutionsgNo ratings yet

- REVIEW Chap 1 - 2 - 3Document9 pagesREVIEW Chap 1 - 2 - 3Khánh AnNo ratings yet

- ACCT 2211 Assignment 2Document17 pagesACCT 2211 Assignment 2Tannaz SNo ratings yet

- RtgsDocument3 pagesRtgsFungaiNo ratings yet

- Adjusting Entries and Worksheet Practice Set 2 Sept 19 AssignmentDocument3 pagesAdjusting Entries and Worksheet Practice Set 2 Sept 19 Assignmenthngrc29No ratings yet

- AccountsA MTP Foundation Oct19Document10 pagesAccountsA MTP Foundation Oct19backuphpdv6No ratings yet

- Accounting PDFDocument10 pagesAccounting PDFAhmer NaeemNo ratings yet

- BA 118.1 SME Exercise Set 5Document1 pageBA 118.1 SME Exercise Set 5Ian De DiosNo ratings yet

- BUSN7008 Week 3 Adjustments - Updated 2023Document33 pagesBUSN7008 Week 3 Adjustments - Updated 2023berfamenNo ratings yet

- ACCT 201 FA 21 Practice Homework Name: Thomas TermoteDocument4 pagesACCT 201 FA 21 Practice Homework Name: Thomas TermoteThomas TermoteNo ratings yet

- The Adjusting ProcessDocument9 pagesThe Adjusting Processmida0% (1)

- Analyzing TransactionsDocument8 pagesAnalyzing TransactionsUgaas yare21No ratings yet

- ACC 211 Week 10-12Document24 pagesACC 211 Week 10-12idontcaree123312No ratings yet

- Week3-Lecture 6 NotesDocument28 pagesWeek3-Lecture 6 Noteskk23212No ratings yet

- Chapter 4Document109 pagesChapter 4nadima behzadNo ratings yet

- Adjusting Journal EntriesDocument23 pagesAdjusting Journal EntriesAlliyah Manzano CalvoNo ratings yet

- Ch4 Completing The Accounting Cycle ACC101Document9 pagesCh4 Completing The Accounting Cycle ACC101Muhammad KridliNo ratings yet

- Accounting Chapter 5 SolutionsDocument13 pagesAccounting Chapter 5 Solutionsali sherNo ratings yet

- Asistensi 4Document6 pagesAsistensi 4William MangumbanNo ratings yet

- Review Questions & Answers For Midterm1: BA 203 - Financial Accounting Fall 2019-2020Document11 pagesReview Questions & Answers For Midterm1: BA 203 - Financial Accounting Fall 2019-2020Ulaş GüllenoğluNo ratings yet

- Problem Set For AR (Ctto)Document16 pagesProblem Set For AR (Ctto)Mariane Jean Guerrero100% (1)

- Seminar3 Accrual Accounting and IncomeDocument4 pagesSeminar3 Accrual Accounting and IncomeThomas ShelbyNo ratings yet

- C3 - Matching and Adjusting ProcessDocument12 pagesC3 - Matching and Adjusting ProcessIvy Jean Ybera-PapasinNo ratings yet

- P4A-33A (Similar To) : Date Accounts and Explanation Debit CreditDocument13 pagesP4A-33A (Similar To) : Date Accounts and Explanation Debit Creditspam.ml2023No ratings yet

- Case - 1 UnitDocument2 pagesCase - 1 UnitSowmya Vijaykumar SirsaliNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- ACC1701 Revision Session SlidesDocument38 pagesACC1701 Revision Session SlidesshermaineNo ratings yet

- ACC 1701 Group Project DetailsDocument8 pagesACC 1701 Group Project DetailsshermaineNo ratings yet

- ACC1701 Prerecorded Review Session For BAN - For StudentsDocument38 pagesACC1701 Prerecorded Review Session For BAN - For StudentsshermaineNo ratings yet

- 10-Introduction To Discrete OptimizationDocument32 pages10-Introduction To Discrete OptimizationshermaineNo ratings yet

- 9-LP Sensitivity AnalysisDocument23 pages9-LP Sensitivity AnalysisshermaineNo ratings yet

- 8-Introduction To Linear OptimizationDocument21 pages8-Introduction To Linear OptimizationshermaineNo ratings yet

- 7 Decision TreeDocument55 pages7 Decision TreeshermaineNo ratings yet

- 5 Continuous ProbabilitiesDocument55 pages5 Continuous ProbabilitiesshermaineNo ratings yet

- Financial Analysis of A Selected CompanyDocument20 pagesFinancial Analysis of A Selected CompanyAmid Abdul-Karim100% (1)

- Audit of Prepayments and Intangible AssetsDocument4 pagesAudit of Prepayments and Intangible AssetsGille Rosa Abajar100% (1)

- Economics - Capital MarketDocument13 pagesEconomics - Capital MarketAll Time Gaming GeekNo ratings yet

- Solved Sum of Financial RatiosDocument11 pagesSolved Sum of Financial RatiosJessy NairNo ratings yet

- MiyawwDocument9 pagesMiyawwjessa mae zerdaNo ratings yet

- Women's Rights Are Human RightsDocument7 pagesWomen's Rights Are Human Rightstanmaya_purohitNo ratings yet

- FA II AssignmentDocument7 pagesFA II AssignmentmapNo ratings yet

- Question Bank SFM (Old and New)Document232 pagesQuestion Bank SFM (Old and New)MBaralNo ratings yet

- CHP 6 - Governance - Share Holders (SBL Notes by Sir Hasan Dossani)Document27 pagesCHP 6 - Governance - Share Holders (SBL Notes by Sir Hasan Dossani)JEFFNo ratings yet

- BAFINMAX Handout Introduction To Working Capital ManagementDocument2 pagesBAFINMAX Handout Introduction To Working Capital ManagementDeo CoronaNo ratings yet

- CBSE Class 12 Accountancy Accounting For Debentures WorksheetDocument13 pagesCBSE Class 12 Accountancy Accounting For Debentures WorksheetJenneil CarmichaelNo ratings yet

- FM Chapter 8 PDFDocument6 pagesFM Chapter 8 PDFSuzanne AcostaNo ratings yet

- Ac 2020 14Document8 pagesAc 2020 14vcpc2008No ratings yet

- Soal Uts 1Document5 pagesSoal Uts 1febiastyNo ratings yet

- Important Sections CMA Final LawDocument3 pagesImportant Sections CMA Final Lawsamsungkalra01No ratings yet

- Types of Corporations: Accounting Unit 1Document22 pagesTypes of Corporations: Accounting Unit 1Chevannese EllisNo ratings yet

- Sid - Sbi Multi Asset Allocation Fund PDFDocument95 pagesSid - Sbi Multi Asset Allocation Fund PDFANo ratings yet

- ICICI Direct - Research ReportDocument4 pagesICICI Direct - Research ReportMudit KediaNo ratings yet

- RT UAT Template - ResearchDocument168 pagesRT UAT Template - ResearchsujeetsinghjsrNo ratings yet

- Accounting For Management Question PaperDocument3 pagesAccounting For Management Question PaperVINOD KUMARNo ratings yet

- EW00467 Annual Report 2018Document148 pagesEW00467 Annual Report 2018rehan7777No ratings yet

- The Accounting EquationDocument19 pagesThe Accounting EquationAthena LansangNo ratings yet

- HM Phân Tích Báo Cáo Tài ChínhDocument7 pagesHM Phân Tích Báo Cáo Tài ChínhHoàng TrâmNo ratings yet

- ProfitabilityDocument25 pagesProfitabilitynira_11050% (2)

- Description Income Statement Adjustments Statement of Cash FlowsDocument2 pagesDescription Income Statement Adjustments Statement of Cash FlowsFhem Leighn SimetraNo ratings yet

- Consolidation With Intercompany TransactionsDocument26 pagesConsolidation With Intercompany TransactionsRoselyn mangaron sagcalNo ratings yet

- Reading 27 Applications of Financial Statement AnalysisDocument11 pagesReading 27 Applications of Financial Statement AnalysisARPIT ARYANo ratings yet

- Business Plan: The Role in Business & Issues in The Preparation of A Good Business PlanDocument13 pagesBusiness Plan: The Role in Business & Issues in The Preparation of A Good Business PlanMVK SRINIVASA RAONo ratings yet