You might also like

- UniqloDocument17 pagesUniqloUmar GondalNo ratings yet

- Fa4e SM Ch01Document21 pagesFa4e SM Ch01michaelkwok1100% (1)

- Reliance Retail Limited: Total Amount (In Words) Four Hundred Seventy Rupees and Eighty Two Paise OnlyDocument2 pagesReliance Retail Limited: Total Amount (In Words) Four Hundred Seventy Rupees and Eighty Two Paise OnlymohitahirNo ratings yet

- BAV Lecture 1 and 2Document19 pagesBAV Lecture 1 and 2Fluid TrapsNo ratings yet

- Module 1 Financial Accounting For MBAs - 6th EditionDocument15 pagesModule 1 Financial Accounting For MBAs - 6th EditionjoshNo ratings yet

- Auditing Overview and Financial Statement AuditsDocument8 pagesAuditing Overview and Financial Statement AuditsjhienellNo ratings yet

- ALEX'S 304 AssignmentDocument5 pagesALEX'S 304 Assignmentmuriithialex2030No ratings yet

- RUKIA'S 304 AssignmentDocument4 pagesRUKIA'S 304 Assignmentmuriithialex2030No ratings yet

- AAS CH1 2 1 - MergedDocument19 pagesAAS CH1 2 1 - MergedRoel PaisteNo ratings yet

- Patterns of Earnings ManagementDocument6 pagesPatterns of Earnings ManagementAnis SofiaNo ratings yet

- Akka HyuiDocument15 pagesAkka HyuiAkkamaNo ratings yet

- Intermediate - Accounting - Spiceland - Sepe - Nelson - 8th - Ed - CHPT - 01 - Exercises AnswerDocument27 pagesIntermediate - Accounting - Spiceland - Sepe - Nelson - 8th - Ed - CHPT - 01 - Exercises AnswerMelissaNo ratings yet

- Group 1 Chapter 1 The Demand For Auditing and Assurance ServicesDocument23 pagesGroup 1 Chapter 1 The Demand For Auditing and Assurance ServicestristahmncdldyNo ratings yet

- The Economic and Institutional Setting For Financial ReportingDocument48 pagesThe Economic and Institutional Setting For Financial Reportingcatelyne santosNo ratings yet

- Document 7Document12 pagesDocument 7Ram PagongNo ratings yet

- Financial Statement Analysis - Chp03 - Summary NotesDocument6 pagesFinancial Statement Analysis - Chp03 - Summary NotesBrainNo ratings yet

- Module 3 Topic 3 in Cooperative ManagementDocument34 pagesModule 3 Topic 3 in Cooperative Managementharon franciscoNo ratings yet

- Chapter 1 - AACA P1Document7 pagesChapter 1 - AACA P1Toni Rose Hernandez LualhatiNo ratings yet

- CH 1Document34 pagesCH 1Ram KumarNo ratings yet

- Answer KeyDocument6 pagesAnswer KeyClaide John OngNo ratings yet

- Chapter 1 - Financial ReportingDocument7 pagesChapter 1 - Financial ReportingrtohattonNo ratings yet

- Accounting For Lawyers by Solicitor KatuDocument45 pagesAccounting For Lawyers by Solicitor KatuFrancisco Hagai GeorgeNo ratings yet

- Financial Statements Explained: Balance Sheet, Income Statement & Cash FlowDocument12 pagesFinancial Statements Explained: Balance Sheet, Income Statement & Cash FlowDurdana NasserNo ratings yet

- The Environment of Financial Accounting and ReportingDocument59 pagesThe Environment of Financial Accounting and ReportingHeisei De LunaNo ratings yet

- Accounting for Management AssignmentDocument23 pagesAccounting for Management Assignmentgarusha gautamNo ratings yet

- Overview of Auditing and Audit TypesDocument8 pagesOverview of Auditing and Audit TypesPol AnduLanNo ratings yet

- Audit theory and practice explores assurance and expectationsDocument10 pagesAudit theory and practice explores assurance and expectationsSimonsNo ratings yet

- Our WorkDocument16 pagesOur Workroro522011No ratings yet

- DocxDocument7 pagesDocxHeni OktaviantiNo ratings yet

- Audit theory and practice explores assurance and expectationsDocument10 pagesAudit theory and practice explores assurance and expectationsSimonsNo ratings yet

- Kiprono Assingment BBM 304Document4 pagesKiprono Assingment BBM 304muriithialex2030No ratings yet

- A Conceptual Framework For Financial Accounting and ReportingDocument70 pagesA Conceptual Framework For Financial Accounting and ReportingAyesha ZakiNo ratings yet

- The Timing of Asset Sales and Earnings MDocument8 pagesThe Timing of Asset Sales and Earnings MRizqullazid MufiddinNo ratings yet

- babe oyeDocument4 pagesbabe oyejashanvipan1290No ratings yet

- Financial Statement Analysis ExplainedDocument36 pagesFinancial Statement Analysis ExplainedFiriehiwot BirhanieNo ratings yet

- Jawaban Assigment CH 1Document5 pagesJawaban Assigment CH 1AjiwNo ratings yet

- Consolidated Financial StatementsDocument32 pagesConsolidated Financial StatementsPeetu WadhwaNo ratings yet

- Chapter 1 AuditDocument13 pagesChapter 1 AuditMisshtaC100% (1)

- Screenshot 2023-12-26 at 7.44.54 PMDocument79 pagesScreenshot 2023-12-26 at 7.44.54 PMrishivardhan050No ratings yet

- FSA&V Case StudyDocument10 pagesFSA&V Case StudyAl Qur'anNo ratings yet

- IASB Conceptual Framework for Financial AccountingDocument9 pagesIASB Conceptual Framework for Financial AccountingAmelia TaylorNo ratings yet

- AC201 Notes PART 1Document25 pagesAC201 Notes PART 1mollymgonigle1No ratings yet

- Week 2 Questions AnswersDocument2 pagesWeek 2 Questions Answers啵啵贊贊No ratings yet

- Financial Statement AnalysisDocument27 pagesFinancial Statement AnalysisJayvee Balino100% (1)

- Orca Share Media1668925931673 6999982710921667804Document26 pagesOrca Share Media1668925931673 6999982710921667804Chekani Kristine MamhotNo ratings yet

- SFAC 1 Objective of Financial ReportingDocument18 pagesSFAC 1 Objective of Financial Reportingrhima_No ratings yet

- Updated Report AUDITINGDocument9 pagesUpdated Report AUDITINGJanelleNo ratings yet

- Audit Planning and Materiality: Concept Checks P. 209Document37 pagesAudit Planning and Materiality: Concept Checks P. 209hsingting yuNo ratings yet

- Long-Term Investment and Accounting: Overcoming Short-Term BiasDocument24 pagesLong-Term Investment and Accounting: Overcoming Short-Term BiasKristina KittyNo ratings yet

- Module Fs AnalysisDocument12 pagesModule Fs AnalysisCeejay RoblesNo ratings yet

- Efficient Contracting Approach to Decision UsefulnessDocument17 pagesEfficient Contracting Approach to Decision UsefulnessFebNo ratings yet

- Creative Accounting: Case Study:WorldcomDocument11 pagesCreative Accounting: Case Study:WorldcomVikash KumarNo ratings yet

- Chapter 3Document5 pagesChapter 3Janah MirandaNo ratings yet

- Hero Moto Corp Financial AnalysisDocument16 pagesHero Moto Corp Financial AnalysisUmeshchandu4a9No ratings yet

- Accounting Theory Handout 1Document43 pagesAccounting Theory Handout 1Ockouri Barnes100% (3)

- Company Management. The Management Team Needs To Understand TheDocument3 pagesCompany Management. The Management Team Needs To Understand TheGopali AoshieaneNo ratings yet

- Midterm Fin Oo4Document82 pagesMidterm Fin Oo4patricia gunio100% (1)

- Accounts NotesDocument15 pagesAccounts NotessharadkulloliNo ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- Financial Intelligence: Mastering the Numbers for Business SuccessFrom EverandFinancial Intelligence: Mastering the Numbers for Business SuccessNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- 4Ms OPERATIONS ENTREPRENEURSHIPDocument42 pages4Ms OPERATIONS ENTREPRENEURSHIPKniwt AdarecrohNo ratings yet

- Revised Confirmation of Johor Student Leader Council (JSLC)Document6 pagesRevised Confirmation of Johor Student Leader Council (JSLC)Shahmel IrfanNo ratings yet

- LEK sharing-CM - AmCham Healthcare Trends 2021 - 2021MAR23bDocument30 pagesLEK sharing-CM - AmCham Healthcare Trends 2021 - 2021MAR23bRishabh RajNo ratings yet

- BATA Company AnalysisDocument21 pagesBATA Company AnalysisSuraj SatpathyNo ratings yet

- Export Advance Payment - ApplicationDocument1 pageExport Advance Payment - ApplicationKumar SwamyNo ratings yet

- Governance of EU Competition Policy Over Luxury BrandsDocument10 pagesGovernance of EU Competition Policy Over Luxury BrandsPATRICIA NIKOLE PEREZNo ratings yet

- Management Representation LetterDocument3 pagesManagement Representation LetterPreeti mittalNo ratings yet

- Ocobee River Rafting Company profit analysisDocument4 pagesOcobee River Rafting Company profit analysiskristine torresNo ratings yet

- International Economics Problem SetDocument5 pagesInternational Economics Problem Setgetu nigusieNo ratings yet

- MCQ Monopolistic & Oligopolistic Competition PDFDocument5 pagesMCQ Monopolistic & Oligopolistic Competition PDFAJAY KUMAR SAHUNo ratings yet

- Chapter 1 Business Information Systems in Your CareerDocument23 pagesChapter 1 Business Information Systems in Your CareermeriemNo ratings yet

- Chapter 11Document34 pagesChapter 11JaneNo ratings yet

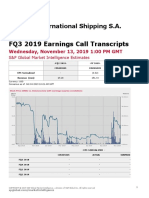

- D'amico International Shipping S.a., Q3 2019 Earnings Call, Nov 13, 2019Document11 pagesD'amico International Shipping S.a., Q3 2019 Earnings Call, Nov 13, 2019Chris WallerNo ratings yet

- Monginis PDF BBMDocument16 pagesMonginis PDF BBMFurkan AhmedNo ratings yet

- Cisco Registered Partner Minimum Eligibility RequirementsDocument2 pagesCisco Registered Partner Minimum Eligibility Requirementsmarcoant2287100% (1)

- Product Roadmap Guide by ProductPlanDocument68 pagesProduct Roadmap Guide by ProductPlananikbiswasNo ratings yet

- List of Delisted Withholding Agents - Non-IndividualDocument11 pagesList of Delisted Withholding Agents - Non-IndividualGennelyn OdulioNo ratings yet

- Startup Checklist for Your BusinessDocument3 pagesStartup Checklist for Your BusinessAJAY SHINDENo ratings yet

- Content Project Management 2020Document229 pagesContent Project Management 2020José Vicente100% (1)

- Customs Valuation SystemDocument3 pagesCustoms Valuation SystemJehiel CastilloNo ratings yet

- Chapter 9 Receivable FinancingDocument58 pagesChapter 9 Receivable FinancingMichelle J UrbodaNo ratings yet

- KL 39 H 3095 PDFDocument1 pageKL 39 H 3095 PDFSujith Raj SNo ratings yet

- Imc 40Document11 pagesImc 40Bella BrillantesNo ratings yet

- Ita Imia 2023 BDDocument28 pagesIta Imia 2023 BDKishor YenepalliNo ratings yet

- Sony Betamax Brand Failure: Hitesh BhasinDocument3 pagesSony Betamax Brand Failure: Hitesh Bhasinakash bathamNo ratings yet

- GX Global Powers of Luxury Goods 2023Document78 pagesGX Global Powers of Luxury Goods 2023xen101No ratings yet

- Account Reconciliation Policy - Sample 2Document5 pagesAccount Reconciliation Policy - Sample 2Muri EmJayNo ratings yet

- (Assignment) Finc 331 Project 1Document6 pages(Assignment) Finc 331 Project 1Nashon ChachaNo ratings yet