You might also like

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- National University of Science and TechnologyDocument5 pagesNational University of Science and TechnologyPATIENCE MUSHONGANo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Csec Poa January 2012 p2Document9 pagesCsec Poa January 2012 p2Renelle RampersadNo ratings yet

- RATIO QuestionsDocument5 pagesRATIO QuestionsikkaNo ratings yet

- AFA Tutorial 11: Analyzing Financial Statements and RatiosDocument9 pagesAFA Tutorial 11: Analyzing Financial Statements and RatiosJIA HUI LIMNo ratings yet

- poa_2012_Jan_p.2.q.1_1Document4 pagespoa_2012_Jan_p.2.q.1_1RealGenius (Carl)No ratings yet

- F&AQPmidsem summer22Document2 pagesF&AQPmidsem summer22kanika thakurNo ratings yet

- Gujarat Technological UniversityDocument6 pagesGujarat Technological UniversitymansiNo ratings yet

- What Are The Advantages To A Business of Being Formed As A Company? What Are The Disadvantages?Document12 pagesWhat Are The Advantages To A Business of Being Formed As A Company? What Are The Disadvantages?Nguyễn HoàngNo ratings yet

- Unit 1 - QuestionsDocument4 pagesUnit 1 - QuestionsMohanNo ratings yet

- PDE4232 Individual Coursework - 2023-24 UpdatedDocument5 pagesPDE4232 Individual Coursework - 2023-24 UpdatedTariq KhanNo ratings yet

- BU51009 (5BA) - Assessed Coursework - EBT 2019-20Document2 pagesBU51009 (5BA) - Assessed Coursework - EBT 2019-20Sravya MagantiNo ratings yet

- Financial Performance Evaluation of Smithson PlcDocument5 pagesFinancial Performance Evaluation of Smithson PlcAyesha SheheryarNo ratings yet

- Incomplete Accounting RecordsDocument5 pagesIncomplete Accounting RecordsTawanda Tatenda Herbert100% (1)

- Mba ZC415 Ec-3r First Sem 2022-2023Document4 pagesMba ZC415 Ec-3r First Sem 2022-2023Ravi KaviNo ratings yet

- Cash Flow Statement Cash AnalysisDocument21 pagesCash Flow Statement Cash Analysisshrestha.aryxnNo ratings yet

- Tutorial 4B : Excel: More Applications in AccountingDocument7 pagesTutorial 4B : Excel: More Applications in Accountingasdsad dsadsaNo ratings yet

- CAC1201201008 Financial Accounting 1BDocument6 pagesCAC1201201008 Financial Accounting 1Bnyasha gundaniNo ratings yet

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan BrohiNo ratings yet

- Account 1srsDocument5 pagesAccount 1srsNayan KcNo ratings yet

- T Fraser, Motif and Meath Cash Flow QuestionsDocument5 pagesT Fraser, Motif and Meath Cash Flow Questionschalah DeriNo ratings yet

- Management Accounting QBDocument31 pagesManagement Accounting QBrising dragonNo ratings yet

- Cashflow Statements Ias7Document11 pagesCashflow Statements Ias7Foni NancyNo ratings yet

- CourseworkDocument9 pagesCourseworkAbhishek DebNo ratings yet

- MANAGEMENT ACCOUNTING & CONTROL 306 Ele Paper IIIDocument5 pagesMANAGEMENT ACCOUNTING & CONTROL 306 Ele Paper IIItadepalli patanjaliNo ratings yet

- Excel Academy Financial StatementsDocument5 pagesExcel Academy Financial Statementsfaith olaNo ratings yet

- ACC101 Chapter2newDocument19 pagesACC101 Chapter2newDEREJENo ratings yet

- Accounting For Transactions: Key Terms and Concepts To KnowDocument19 pagesAccounting For Transactions: Key Terms and Concepts To KnowMaria Nicole OroNo ratings yet

- Accounting For Transactions: Key Terms and Concepts To KnowDocument19 pagesAccounting For Transactions: Key Terms and Concepts To KnowAileenNo ratings yet

- Acc_N2020_P3_(1)Document7 pagesAcc_N2020_P3_(1)chauromweaNo ratings yet

- District Resource Centre Mahbubnagar:, Pre-Final Examinations - Jan / Feb - 2011 Management AccountingDocument5 pagesDistrict Resource Centre Mahbubnagar:, Pre-Final Examinations - Jan / Feb - 2011 Management Accountingtadepalli patanjaliNo ratings yet

- Financial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Test Bank 1Document36 pagesFinancial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Test Bank 1ericsuttonybmqwiorsa100% (28)

- Classroom Exerisises On Presentation of Financial Statements PDFDocument2 pagesClassroom Exerisises On Presentation of Financial Statements PDFalyssaNo ratings yet

- Act201 AssignmentDocument4 pagesAct201 Assignmentmahmud100% (1)

- ACCT10002 Tutorial 2 Exercises, 2020 SM1Document6 pagesACCT10002 Tutorial 2 Exercises, 2020 SM1JING NIENo ratings yet

- First 1302020Document9 pagesFirst 1302020fNo ratings yet

- Zimbabwe School Examinations Council: Accounts 7112/1Document4 pagesZimbabwe School Examinations Council: Accounts 7112/1Munashe BinhaNo ratings yet

- Decision Case 12-4Document2 pagesDecision Case 12-4cbarajNo ratings yet

- Balance Sheet and Transactions Analysis for Charles CompanyDocument14 pagesBalance Sheet and Transactions Analysis for Charles CompanyArunesh SN100% (1)

- 286practice Questions - AnswerDocument17 pages286practice Questions - Answerma sthaNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument7 pages© The Institute of Chartered Accountants of IndiaSarvesh JoshiNo ratings yet

- Statement of CashflowDocument9 pagesStatement of CashflowOwen Lustre50% (2)

- ACCT10002 tutorial exercisesDocument5 pagesACCT10002 tutorial exercisesJING NIENo ratings yet

- National University of Science and TechnologyDocument8 pagesNational University of Science and TechnologyPATIENCE MUSHONGANo ratings yet

- seminar 8 PART BDocument3 pagesseminar 8 PART BGaba RieleNo ratings yet

- Cash Flow (Exercise)Document5 pagesCash Flow (Exercise)abhishekvora7598752100% (1)

- Chapter 2. Understanding The Income StatementDocument10 pagesChapter 2. Understanding The Income StatementVượng TạNo ratings yet

- Bacc 237 Assignment two ( Multiple choice) (2)Document10 pagesBacc 237 Assignment two ( Multiple choice) (2)TarusengaNo ratings yet

- 2020 Acc 410 Test 1Document8 pages2020 Acc 410 Test 1Kesa Metsi100% (1)

- Cash FlowDocument8 pagesCash FlowTarmak LyonNo ratings yet

- Accounting IAS Model Answers Series 2 2010Document17 pagesAccounting IAS Model Answers Series 2 2010Aung Zaw HtweNo ratings yet

- A Level QP3 Acc PB2022Document12 pagesA Level QP3 Acc PB2022Kalash JainNo ratings yet

- Acp - Acc417 Case Study 1Document6 pagesAcp - Acc417 Case Study 1Faker MejiaNo ratings yet

- ACCT10002 Tutorial 9 ExercisesDocument6 pagesACCT10002 Tutorial 9 ExercisesJING NIENo ratings yet

- Amended - Final - Unit 5 - AAB-Accounting Principles - A2Document6 pagesAmended - Final - Unit 5 - AAB-Accounting Principles - A2Quang MinhNo ratings yet

- Fund Flow Statement: by Dr. Aleem AnsariDocument18 pagesFund Flow Statement: by Dr. Aleem AnsariPRIYAL GUPTANo ratings yet

- ACCA F9 Mock Examination 2Document5 pagesACCA F9 Mock Examination 2daria0% (1)

- Cash Flow 8 AprilDocument17 pagesCash Flow 8 AprilMayank MalhotraNo ratings yet

- FAR - Final Preboard CPAR 92Document14 pagesFAR - Final Preboard CPAR 92joyhhazelNo ratings yet

- National University of Science and TechnologyDocument8 pagesNational University of Science and TechnologyPATIENCE MUSHONGANo ratings yet

- Accounting Notes PDFDocument129 pagesAccounting Notes PDFLeeroy Gift100% (1)

- National University of Science and TechnologyDocument8 pagesNational University of Science and TechnologyPATIENCE MUSHONGANo ratings yet

- UntitledDocument7 pagesUntitledPATIENCE MUSHONGANo ratings yet

- Partnership Bar QuestionsDocument4 pagesPartnership Bar QuestionsYollaine GaliasNo ratings yet

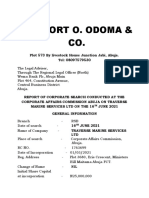

- Comfort O. Odoma & CO.: Plot 573 by Livestock House Junction Jabi, Abuja. Tel: 08097579530Document4 pagesComfort O. Odoma & CO.: Plot 573 by Livestock House Junction Jabi, Abuja. Tel: 08097579530Comfort OdomaNo ratings yet

- SC102Document29 pagesSC102Jasper VincentNo ratings yet

- Partnership - ANSWERS TO DIAGNOSTIC EXERCISESDocument20 pagesPartnership - ANSWERS TO DIAGNOSTIC EXERCISESBrent LigsayNo ratings yet

- PF Checklist - SibDocument1 pagePF Checklist - SibdevilinpajamaNo ratings yet

- Amend Articles & By-Laws for Corps (SEC PHDocument1 pageAmend Articles & By-Laws for Corps (SEC PHIan Leoj GumbanNo ratings yet

- Biography: Joel Uzuriaga FDocument2 pagesBiography: Joel Uzuriaga FjoelNo ratings yet

- MACS - Assignment 3 - Answer BookDocument14 pagesMACS - Assignment 3 - Answer BookAudrey KhwinanaNo ratings yet

- Wallstreetjournaleurope 20160307 The Wall Street Journal EuropeDocument22 pagesWallstreetjournaleurope 20160307 The Wall Street Journal EuropestefanoNo ratings yet

- Hustler USA - Anniversary 2023Document138 pagesHustler USA - Anniversary 2023ธนวัฒน์ ปิยะวิสุทธิกุล67% (6)

- LIC Combined ReceiptsDocument6 pagesLIC Combined Receiptssumanpal78No ratings yet

- Finance Module 5 Sources of Short Term FundsDocument5 pagesFinance Module 5 Sources of Short Term FundsJOHN PAUL LAGAONo ratings yet

- How To Invest in Philippine Stock Market PDFDocument8 pagesHow To Invest in Philippine Stock Market PDFEduardo SantosNo ratings yet

- Strategy Nib BankDocument125 pagesStrategy Nib BankGedionNo ratings yet

- Measuring InflationDocument35 pagesMeasuring InflationFTU K59 Trần Yến LinhNo ratings yet

- RLB Construction Market Update Vietnam Q2 2018Document8 pagesRLB Construction Market Update Vietnam Q2 2018Miguel AcostaNo ratings yet

- Case Analysis SAMPLEDocument12 pagesCase Analysis SAMPLEStephen TylerNo ratings yet

- Types of Major AccountsDocument30 pagesTypes of Major AccountsEstelle GammadNo ratings yet

- Incorporating History Into Innovation A Case StudyDocument8 pagesIncorporating History Into Innovation A Case StudyNathania MichaelNo ratings yet

- Chapter 4 - LendingDocument64 pagesChapter 4 - LendingPhương NguyễnNo ratings yet

- Paper Title (24pt, Times New Roman, Upper Case) : Subtitle If Needed (14pt, Italic, Line Spacing: Before:8pt, After:16pt)Document6 pagesPaper Title (24pt, Times New Roman, Upper Case) : Subtitle If Needed (14pt, Italic, Line Spacing: Before:8pt, After:16pt)Parthi PNo ratings yet

- Cost Accounting Reviewer Chapter 1-4Document10 pagesCost Accounting Reviewer Chapter 1-4hanaNo ratings yet

- Determinants of Bank'S Profitability in Pakistan: A Latest Panel Data EvidenceDocument16 pagesDeterminants of Bank'S Profitability in Pakistan: A Latest Panel Data EvidencealibuxjatoiNo ratings yet

- Mine Card by Icicibank TNCDocument11 pagesMine Card by Icicibank TNCMari SelvamNo ratings yet

- NBPDebit Card FormDocument11 pagesNBPDebit Card Formƒム乄คneeร GamingNo ratings yet

- Slide 1: Features of Nepalese Economy and Its Nature (System)Document19 pagesSlide 1: Features of Nepalese Economy and Its Nature (System)Narayan TimilsainaNo ratings yet

- Cond and Other HoldingsDocument108 pagesCond and Other HoldingsLina Michelle Matheson Brual100% (1)

- Your GIRO Payment Plan For Income Tax: DBS/POSB xxxxxx9205Document2 pagesYour GIRO Payment Plan For Income Tax: DBS/POSB xxxxxx9205Karaoui LaidNo ratings yet

- Mailing List of The INSME Association - 2nd of April 2015Document33 pagesMailing List of The INSME Association - 2nd of April 2015Santosh DsouzaNo ratings yet

- National Manufacxturing PolicyDocument5 pagesNational Manufacxturing PolicyAaesta PriyestaNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyFrom EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyRating: 4.5 out of 5 stars4.5/5 (37)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesFrom EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesRating: 5 out of 5 stars5/5 (4)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceFrom EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceNo ratings yet

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)From EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- I'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)From EverandI'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)Rating: 4.5 out of 5 stars4.5/5 (24)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageFrom EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageRating: 4.5 out of 5 stars4.5/5 (109)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)