You might also like

- Study On Fish Marketing and Packaging System in Natore, BangladeshDocument8 pagesStudy On Fish Marketing and Packaging System in Natore, BangladeshEskinder SahlemariamNo ratings yet

- Plants From Pitlakes: An inventory of plants from the pitlakes of Eastern Coalfields, IndiaFrom EverandPlants From Pitlakes: An inventory of plants from the pitlakes of Eastern Coalfields, IndiaNo ratings yet

- Soumyadip Purkait, Et AlDocument14 pagesSoumyadip Purkait, Et AlManu SivaramanNo ratings yet

- Status, Prospects and Market Potentials of The Sea Cucumber Fisheries With Special Reference On Their Proper Utilization and TradeDocument18 pagesStatus, Prospects and Market Potentials of The Sea Cucumber Fisheries With Special Reference On Their Proper Utilization and Tradeyeasmin fmbNo ratings yet

- Baseline Survey Report On Seaweed Cultivation, Processing, and Marketing For Employment Generation in Bangladesh's Coastal Poor CommunitiesDocument9 pagesBaseline Survey Report On Seaweed Cultivation, Processing, and Marketing For Employment Generation in Bangladesh's Coastal Poor CommunitiesInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Crab Culture Potential in Southwestern Bangladesh: Alternative To Shrimp Culture For Climate Change AdaptionDocument18 pagesCrab Culture Potential in Southwestern Bangladesh: Alternative To Shrimp Culture For Climate Change AdaptionMohammad ShahnurNo ratings yet

- Profitability and Viability Analysis of Aquaculture Production in Central Uganda. Acase of Urban and Peri Urban Areas - 2 PDFDocument11 pagesProfitability and Viability Analysis of Aquaculture Production in Central Uganda. Acase of Urban and Peri Urban Areas - 2 PDFEko MojoNo ratings yet

- Marketing Channels of Mud Crab (Scylla Serrata) at Nijhum Dwip, Noakhali, Bangladesh A Value Chain AnalysisDocument7 pagesMarketing Channels of Mud Crab (Scylla Serrata) at Nijhum Dwip, Noakhali, Bangladesh A Value Chain AnalysisAbdulla-Al-AsifNo ratings yet

- Seaweed Fertilizers in Modern Agriculture: October 2018Document8 pagesSeaweed Fertilizers in Modern Agriculture: October 2018JELICEL ATENo ratings yet

- FreezerTrawler Catch ReportDocument11 pagesFreezerTrawler Catch ReportCelltron SolutionsNo ratings yet

- Indigenous KnowledgeDocument6 pagesIndigenous KnowledgeBharat SontakkiNo ratings yet

- IJCRTDRBC078 HowtomDocument9 pagesIJCRTDRBC078 Howtompro officialNo ratings yet

- Crab Farming Business PlanDocument30 pagesCrab Farming Business Plandarkportrait50% (2)

- Market Participation and Value Chain of Cassava Farmers in Abia StateDocument11 pagesMarket Participation and Value Chain of Cassava Farmers in Abia Statesimeon OnyaNo ratings yet

- Greenhouse Gas Emissions From Aquaculture: A Life Cycle Assessment of Three Asian SystemsFrom EverandGreenhouse Gas Emissions From Aquaculture: A Life Cycle Assessment of Three Asian SystemsNo ratings yet

- Mapping Potential Areas for Pearl Oyster Farming in Lombok WatersDocument14 pagesMapping Potential Areas for Pearl Oyster Farming in Lombok WatersAbdul Hamid Al HabibNo ratings yet

- Final ReportDocument20 pagesFinal ReportRoseannae ParkNo ratings yet

- Chapter 2Document8 pagesChapter 2lamperalonitoNo ratings yet

- 2016 1 RJAVFS RasulDocument7 pages2016 1 RJAVFS Rasul020ANNISA NUR MAHARANINo ratings yet

- Book of Abstracts-9 BFRFDocument192 pagesBook of Abstracts-9 BFRFMd. Monjurul HasanNo ratings yet

- 87 Arbitetal-2019Document11 pages87 Arbitetal-2019Nabila Anindya PutriNo ratings yet

- Naharetal.2021Document13 pagesNaharetal.2021Kumar DevNo ratings yet

- 2. DiversityofseabassgearscraftsBJFDocument10 pages2. DiversityofseabassgearscraftsBJFKumar DevNo ratings yet

- Book Chapter RichardDocument22 pagesBook Chapter RichardADJEI FREY EMMANUELNo ratings yet

- No 10 24 JAPH Cultivation SriLankaDocument16 pagesNo 10 24 JAPH Cultivation SriLankaCalamianes Seaweed Marketing CooperativeNo ratings yet

- Culture Performance and Economic Return of Brown ShrimpDocument8 pagesCulture Performance and Economic Return of Brown ShrimpLuã OliveiraNo ratings yet

- Invasionrisk Epaetal.Document18 pagesInvasionrisk Epaetal.Prof. U.P.K. Epa - University of KelaniyaNo ratings yet

- Oyster Condition: Research Journal of Chemistry and Environment March 2014Document6 pagesOyster Condition: Research Journal of Chemistry and Environment March 2014Tony NicholasNo ratings yet

- The Business Prospect of Climbing Perch Fish Farming With Bio Oc Technology at De' Papuyu Farm BanjarbaruDocument10 pagesThe Business Prospect of Climbing Perch Fish Farming With Bio Oc Technology at De' Papuyu Farm Banjarbarudesikudi9000No ratings yet

- Ali.2023.HatcherysegmentDocument22 pagesAli.2023.Hatcherysegmentprem kumarNo ratings yet

- Marketing strategies for frozen fish exporters to expand markets and handle risksDocument3 pagesMarketing strategies for frozen fish exporters to expand markets and handle risksdewiNo ratings yet

- Journal Homepage: - : IntroductionDocument8 pagesJournal Homepage: - : IntroductionIJAR JOURNALNo ratings yet

- Profitability Analysis of BRRI Dhan 29 in Some Selected Areas of BangladeshDocument6 pagesProfitability Analysis of BRRI Dhan 29 in Some Selected Areas of BangladeshAkm Golam Kausar KanchanNo ratings yet

- BiofloctechnologyforshrimpcultureAftabUddinetal.Document8 pagesBiofloctechnologyforshrimpcultureAftabUddinetal.Kumar DevNo ratings yet

- Present Status and Problems of Fish Market in SylhetDocument11 pagesPresent Status and Problems of Fish Market in Sylhet66No ratings yet

- Impacts of Shrimp Farming On The Coastal Environment of Bangladesh and Approach For ManagementDocument23 pagesImpacts of Shrimp Farming On The Coastal Environment of Bangladesh and Approach For Managementrifat sharkerNo ratings yet

- Guidelines For Cage Culture in Inland Open Water Bodies of IndiaDocument20 pagesGuidelines For Cage Culture in Inland Open Water Bodies of IndiaNehaNo ratings yet

- Shrimp Farming and The EnvironmentDocument8 pagesShrimp Farming and The Environmentpedro lopezNo ratings yet

- Smallscale Fisheries PDocument145 pagesSmallscale Fisheries PDominic YuvanNo ratings yet

- Application of Costing Techniques in Ornamental Fish CultureDocument10 pagesApplication of Costing Techniques in Ornamental Fish Cultureraj kiranNo ratings yet

- Book Biosocioeconomic Assessment (2)Document33 pagesBook Biosocioeconomic Assessment (2)r.smg313hzNo ratings yet

- Marketing Strategies For Frozen Fish Exporters in BangladeshDocument8 pagesMarketing Strategies For Frozen Fish Exporters in BangladeshDoc JoeyNo ratings yet

- Cassava Utilization As Livestock Feed 1Document106 pagesCassava Utilization As Livestock Feed 1Rico AwanNo ratings yet

- Nutrientpaper fishDocument10 pagesNutrientpaper fishMaruf khanNo ratings yet

- 15 Microbial Status - YenDocument6 pages15 Microbial Status - YenShamsuddin BabuNo ratings yet

- Handbook On Opensea Cage CultureDocument154 pagesHandbook On Opensea Cage CultureVijayagopal PanikkerNo ratings yet

- Shrimp CultureDocument10 pagesShrimp Culturefirefly_nnc100% (2)

- Fish Breeding BookDocument84 pagesFish Breeding Booksarveshnema100% (1)

- Fish Book Web SizeDocument94 pagesFish Book Web SizeariNo ratings yet

- Good Practices For Community Based Plann PDFDocument26 pagesGood Practices For Community Based Plann PDFDavid Antonio Culqui GarciaNo ratings yet

- Manual On Best Practise of Seaweed Cultivation: Kappaphycus AlvareziiDocument29 pagesManual On Best Practise of Seaweed Cultivation: Kappaphycus AlvareziigraddeeNo ratings yet

- Farmer Participatory Characterization of Coconut Varieties in 2 Indian SitesDocument55 pagesFarmer Participatory Characterization of Coconut Varieties in 2 Indian SitesJayasekhar SomasekharanNo ratings yet

- Constraints Production Bamboo and RatanDocument250 pagesConstraints Production Bamboo and Ratanjkarlsr69100% (2)

- Ecology and reproductive biology of commercial mud crab in BangladeshDocument21 pagesEcology and reproductive biology of commercial mud crab in BangladeshRian Dani TumanggorNo ratings yet

- Economics of Marigold Cultivation in Some SelectedDocument11 pagesEconomics of Marigold Cultivation in Some SelectedAtthaphon KhamwangprukNo ratings yet

- Induced Fish Breeding: A Practical Guide for HatcheriesFrom EverandInduced Fish Breeding: A Practical Guide for HatcheriesRating: 5 out of 5 stars5/5 (1)

- Fishes 09 00002 v2Document30 pagesFishes 09 00002 v2Satrio Hani SamudraNo ratings yet

- 2022 FR RasulDocument24 pages2022 FR Rasuldoanhoangthai12.ltp22No ratings yet

- Develop Sustainable Shrimp ClustersDocument12 pagesDevelop Sustainable Shrimp ClustershartatiNo ratings yet

- Selectivity of Fishing Gears and Their Effects On Fisheries Diversity of Rabnabad Channel of Patuakhali District in BangladeshDocument14 pagesSelectivity of Fishing Gears and Their Effects On Fisheries Diversity of Rabnabad Channel of Patuakhali District in BangladeshGedoNo ratings yet

- QCA After Mid QuizDocument5 pagesQCA After Mid QuizHaris MalikNo ratings yet

- Undertaking Business Permit-ToledoDocument2 pagesUndertaking Business Permit-Toledojunjunsscribdaccount100% (1)

- Loadmasters Customs Services, Inc. v. Glodel Brokerage Corporation, G.R. No. 179446, 10 January 2011, (639 SCRA 69)Document3 pagesLoadmasters Customs Services, Inc. v. Glodel Brokerage Corporation, G.R. No. 179446, 10 January 2011, (639 SCRA 69)Christian Talisay100% (1)

- Vega Agnitya E.P.-17312053 Soal UAS Semester Antara - 2019-2020 - AyuCL-MCSDocument5 pagesVega Agnitya E.P.-17312053 Soal UAS Semester Antara - 2019-2020 - AyuCL-MCSVEGA AGNITYA EKA PANGESTINo ratings yet

- Managing IT Integration Risk in AcquisitionsDocument20 pagesManaging IT Integration Risk in AcquisitionsYurnida PangestutiNo ratings yet

- Special TopicsDocument89 pagesSpecial TopicsPeter Banjao100% (2)

- Corporate Finance 11Th Edition Ross Solutions Manual Full Chapter PDFDocument35 pagesCorporate Finance 11Th Edition Ross Solutions Manual Full Chapter PDFvernon.amundson153100% (10)

- "A Study On Fundamental Analysis of Indian Infrastructure IndustryDocument18 pages"A Study On Fundamental Analysis of Indian Infrastructure IndustrySaadgi AgarwalNo ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- Laws Pertaining To Private Personal and Commercial RelationsDocument10 pagesLaws Pertaining To Private Personal and Commercial RelationsJean TubacNo ratings yet

- LOPEZ - S - Ass2 - The 3D Wheel of Architect's Services - Module1Document4 pagesLOPEZ - S - Ass2 - The 3D Wheel of Architect's Services - Module1qslmlopezNo ratings yet

- Lahore Waste Management Company PDFDocument3 pagesLahore Waste Management Company PDFBint e HawaNo ratings yet

- TYBCom-Sem-VI-Indirect Taxes-GST MCQsDocument10 pagesTYBCom-Sem-VI-Indirect Taxes-GST MCQsMâyúř PäťîĺNo ratings yet

- حق الاضراب لموظفي الدولةDocument67 pagesحق الاضراب لموظفي الدولةelmansoury hichamNo ratings yet

- ICH Q13 Business PlanDocument3 pagesICH Q13 Business PlanbioNo ratings yet

- Resistant Flooring Solutions For Biscuit Plant: Mondelez - Casablanca, MoroccoDocument2 pagesResistant Flooring Solutions For Biscuit Plant: Mondelez - Casablanca, Moroccobassem kooliNo ratings yet

- Intercompany Transactions Bonds LeasesDocument49 pagesIntercompany Transactions Bonds LeasesAndrea Mcnair-West100% (1)

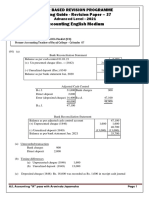

- Accounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Document6 pagesAccounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Malar SrirengarajahNo ratings yet

- The Following Selected Transactions Were Completed by Green Lawn SuppliesDocument1 pageThe Following Selected Transactions Were Completed by Green Lawn SuppliesAmit PandeyNo ratings yet

- PitchBook For Venture Capital Firms - Ebook - GlobalDocument20 pagesPitchBook For Venture Capital Firms - Ebook - GlobalHun Yao ChongNo ratings yet

- Sample Chart of Accounts: Account Name Code Financial Statement Group NormallyDocument2 pagesSample Chart of Accounts: Account Name Code Financial Statement Group NormallyQamar ShahzadNo ratings yet

- Identifying challenges in humanitarian logisticsDocument23 pagesIdentifying challenges in humanitarian logisticsEmil Emmanuel Estilo100% (1)

- Social Media Marketing Impact On Delivery CompaniesDocument12 pagesSocial Media Marketing Impact On Delivery CompaniesSaima AsadNo ratings yet

- ESPP Guidebook EnglishDocument22 pagesESPP Guidebook EnglishPandemicPlaysEverythingNo ratings yet

- 01 Activity 1Document1 page01 Activity 1Yvonne Mae TeopeNo ratings yet

- Field inspection plan for structural steel erectionDocument1 pageField inspection plan for structural steel erectionDelta akathehusky100% (1)

- How To Get Powerful Testimonials That SellDocument10 pagesHow To Get Powerful Testimonials That SellMobile MentorNo ratings yet

- How Much Does AdSense Pay Per 1000 Views Ultimate GuideDocument4 pagesHow Much Does AdSense Pay Per 1000 Views Ultimate GuideCreatom WorkNo ratings yet

- MARKET RESEARCH SwitChair: A 4-in-1 Multipurpose FurnitureDocument18 pagesMARKET RESEARCH SwitChair: A 4-in-1 Multipurpose FurnitureKayla RealNo ratings yet

- A Study On Consumer Behaviour Towards Bottled Drinking Water With Special Reference To Coimbatore City M. Sangeetha & Dr. K. BrindhaDocument4 pagesA Study On Consumer Behaviour Towards Bottled Drinking Water With Special Reference To Coimbatore City M. Sangeetha & Dr. K. BrindhaAnusha YemireddyNo ratings yet