You might also like

- Company Accounts NotesDocument66 pagesCompany Accounts NotesRam krushna PandaNo ratings yet

- OrganizedDocument71 pagesOrganizedRam krushna PandaNo ratings yet

- Scope of Income - MergedDocument9 pagesScope of Income - MergedDipayan DeyNo ratings yet

- Salary PerkDocument20 pagesSalary PerkDipayan DeyNo ratings yet

- Essential Element of Valid Contract ActDocument11 pagesEssential Element of Valid Contract ActDipayan DeyNo ratings yet

- 9 Set Off & Carry ForwardDocument25 pages9 Set Off & Carry Forward21BAM025 RENGARAJANNo ratings yet

- ENVIRONMENTAL CHEMISTRYDocument16 pagesENVIRONMENTAL CHEMISTRYashishdabola219No ratings yet

- 01 ChemicalBondingDocument93 pages01 ChemicalBondingRIP- PIRNo ratings yet

- IIT Chemistry Inorganic Salt Analysis DPPDocument49 pagesIIT Chemistry Inorganic Salt Analysis DPPiitian rankerNo ratings yet

- IIT Mathematics Probability ExercisesDocument40 pagesIIT Mathematics Probability ExercisesKumbhar SaketNo ratings yet

- Raaize e CVT 1Document1 pageRaaize e CVT 1Kathrina Raiza A. MacadagdagNo ratings yet

- Q Star - (Waste Management)Document14 pagesQ Star - (Waste Management)Anonymous Y5cnLVYMGNo ratings yet

- IIT Chemistry: NurtureDocument41 pagesIIT Chemistry: NurtureVibhas SharmaNo ratings yet

- IIT Chemistry: d-Block ElementsDocument55 pagesIIT Chemistry: d-Block Elementsuser 12No ratings yet

- Analysis of Pakistan Textile SectorDocument28 pagesAnalysis of Pakistan Textile SectorKatimaa RizviiNo ratings yet

- UOS Exam Fee ReceiptDocument1 pageUOS Exam Fee ReceiptAbrar ArainNo ratings yet

- Residential Status and Scope of Total IncomeDocument3 pagesResidential Status and Scope of Total IncomePankajSaraogiNo ratings yet

- CS Professional MarathonDocument34 pagesCS Professional Marathonkhanazhar9506No ratings yet

- The Markets on Friday: Sensex up 135.8 points, Nifty gains 28.4 pointsDocument1 pageThe Markets on Friday: Sensex up 135.8 points, Nifty gains 28.4 pointsSiddharth PujariNo ratings yet

- Online Deposit Slip for STS ExamDocument1 pageOnline Deposit Slip for STS ExamemaanNo ratings yet

- Long Term Equity Fund Long Term Equity Fund: It Took Approximately 7 Years To Build The First FlightDocument3 pagesLong Term Equity Fund Long Term Equity Fund: It Took Approximately 7 Years To Build The First Flightashish ujjwalNo ratings yet

- Financial analysis of 3 companiesDocument1 pageFinancial analysis of 3 companiesShadab khanNo ratings yet

- IIT Chemistry: EnthuseDocument48 pagesIIT Chemistry: EnthuseArjun SabnisNo ratings yet

- Shri Ram Castings GST Purchase File FY 2018-19Document3 pagesShri Ram Castings GST Purchase File FY 2018-19Anonymous Q1frWgetsENo ratings yet

- Audit Short NotesDocument22 pagesAudit Short NotesRavindra GehlotNo ratings yet

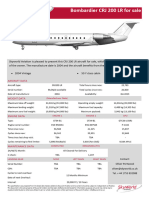

- CRJ200LR Jul 23 Op 1Document1 pageCRJ200LR Jul 23 Op 1SaveThe AirbusA340No ratings yet

- Cooling Food Prices Pull Inflation Down To Five-Month Low: LIC Registers Multifold Jump in Profit at 683 Crore in Q1Document36 pagesCooling Food Prices Pull Inflation Down To Five-Month Low: LIC Registers Multifold Jump in Profit at 683 Crore in Q1f20213093No ratings yet

- SNS Travel Product TampletDocument24 pagesSNS Travel Product TampletMilan DevkotaNo ratings yet

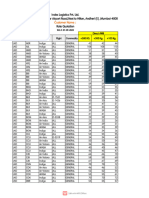

- Index Logistics Pvt. Ltd. Ffice No. 105, Ascot Center, Sahar Airport Road, Next To Hilton, Andheri (E), Mumbai-40009 Customer Name: Rate QuotationDocument4 pagesIndex Logistics Pvt. Ltd. Ffice No. 105, Ascot Center, Sahar Airport Road, Next To Hilton, Andheri (E), Mumbai-40009 Customer Name: Rate Quotationprince aryaNo ratings yet

- Complex Number SheetDocument75 pagesComplex Number SheetHarsh ChaudharyNo ratings yet

- Guide to Set Off & Carry Forward of LossesDocument4 pagesGuide to Set Off & Carry Forward of Lossesanudeepb1604No ratings yet

- Royai Airport ServicesDocument20 pagesRoyai Airport ServicesAhmad QureshiNo ratings yet

- Pt. KMJ Pt. KMJ Pt. KMJ Pt. KMJ Pt. KMJDocument1 pagePt. KMJ Pt. KMJ Pt. KMJ Pt. KMJ Pt. KMJSabrinaAmmarNo ratings yet

- Indian airline fleet sizes over 10 yearsDocument4 pagesIndian airline fleet sizes over 10 yearsAbhishek AbhiranjanNo ratings yet

- Business Standard English DelhiDocument34 pagesBusiness Standard English DelhiManish SatapathyNo ratings yet

- Probability Work BookDocument13 pagesProbability Work BookyayNo ratings yet

- Date: Date: Script ScriptDocument2 pagesDate: Date: Script ScriptShadab khanNo ratings yet

- Ujjala 2022Document62 pagesUjjala 2022Akshay Kumar PrajapatiNo ratings yet

- A Goal Without A Plan Is Just A Wish: Every Thing About CPLDocument4 pagesA Goal Without A Plan Is Just A Wish: Every Thing About CPLIfly CharanNo ratings yet

- Shell Global Solutions Catalogue ReportDocument40 pagesShell Global Solutions Catalogue ReportZahir IlhamNo ratings yet

- Air Regs NotesDocument36 pagesAir Regs NotesFlying DiariesNo ratings yet

- BCOK230300004735Document1 pageBCOK230300004735Khunmoni VlogsNo ratings yet

- Gwen's JVSDocument150 pagesGwen's JVSanon-211661No ratings yet

- MKT-case StudyDocument7 pagesMKT-case StudyJoe Thampi KuruppumadhomNo ratings yet

- University of Sindh Examination Fee Payment ReceiptDocument1 pageUniversity of Sindh Examination Fee Payment ReceiptSyed Shafqat ShahNo ratings yet

- IIT Chemistry: LeaderDocument37 pagesIIT Chemistry: LeaderNamanNo ratings yet

- D006842245 2861592768784284 SchedulescDocument2 pagesD006842245 2861592768784284 SchedulescShubrojyoti Chowdhury0% (1)

- MoU 2019-20Document9 pagesMoU 2019-20Viral KachhadiyaNo ratings yet

- Insttumentation Limited: Ijifi. ( T)Document4 pagesInsttumentation Limited: Ijifi. ( T)soorajssNo ratings yet

- FM Unveils 6-trn Plan To Monetise Assets: Eicher Reappoints Lal, Revises Pay StructureDocument18 pagesFM Unveils 6-trn Plan To Monetise Assets: Eicher Reappoints Lal, Revises Pay StructureNeeraj KumarNo ratings yet

- GST 2024Document236 pagesGST 2024angelkakkallil9929No ratings yet

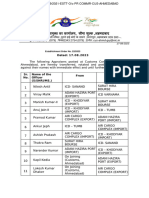

- EO No. 22 2023 Dated 17.08.2023 Customs AppraisersDocument2 pagesEO No. 22 2023 Dated 17.08.2023 Customs AppraisersGaurang BhattNo ratings yet

- JASO Engine Oil Standards Implementation Panel: (Filed Two Cycle Gasoline Engine Oil List) 1 March 2017Document17 pagesJASO Engine Oil Standards Implementation Panel: (Filed Two Cycle Gasoline Engine Oil List) 1 March 2017Abink Yac100% (1)

- Central India Version (Cin)Document2 pagesCentral India Version (Cin)Pallavi ChawlaNo ratings yet

- Contacts JPGDocument96 pagesContacts JPGYassine ZemmouriNo ratings yet

- Govt Budget Questions BoardDocument20 pagesGovt Budget Questions BoardMuskan DhankherNo ratings yet

- Bir Ruling 197-93 (May 7, 1993)Document5 pagesBir Ruling 197-93 (May 7, 1993)matinikkiNo ratings yet

- Individual TaxpayersDocument3 pagesIndividual TaxpayersJoy Orena100% (2)

- Taxation Activity1Document2 pagesTaxation Activity1Creativexie ResinNo ratings yet

- Shraddha Tax ProjectDocument19 pagesShraddha Tax ProjectDeepak Maheshwari67% (3)

- Tax 2 Syllabus - DDL - 2019 PartA 11jan2019Document7 pagesTax 2 Syllabus - DDL - 2019 PartA 11jan2019ebernardo19No ratings yet

- ANI Technologies Private LimitedDocument1 pageANI Technologies Private Limitedgaddam harikrishnaNo ratings yet

- Handout On Piecewise Functions PDFDocument2 pagesHandout On Piecewise Functions PDFryle34100% (1)

- Compounding Taxes in Oracle R12 E-Business TaxDocument4 pagesCompounding Taxes in Oracle R12 E-Business TaxMahesh Jain100% (1)

- Tax Exemption For NgoDocument4 pagesTax Exemption For NgoAdithya Shanker100% (1)

- Prentice Halls Federal Taxation 2013 Individuals 26th Edition Pope Solutions ManualDocument29 pagesPrentice Halls Federal Taxation 2013 Individuals 26th Edition Pope Solutions Manualterrycrossixoqdcfnrg100% (29)

- Payment of Wages Act QuizDocument3 pagesPayment of Wages Act QuizAndy RussellNo ratings yet

- Soneri Bank Limited Balance SheetDocument3 pagesSoneri Bank Limited Balance SheetSaad Ur RehmanNo ratings yet

- Business and Transfer Taxation - Multiple ChoiceDocument7 pagesBusiness and Transfer Taxation - Multiple ChoiceEuli Mae SomeraNo ratings yet

- Ticket Encashment: New Prices Study For 2018Document12 pagesTicket Encashment: New Prices Study For 2018Anonymous IY4ZHvU2HHNo ratings yet

- InvoiceDocument1 pageInvoiceAman MadhukarNo ratings yet

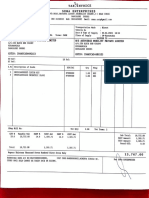

- Tax Invoice for Bluewud Concepts Pvt. LtdDocument1 pageTax Invoice for Bluewud Concepts Pvt. LtdNavdeep MinhasNo ratings yet

- Determinants of Ethiopian Tax RevenueDocument102 pagesDeterminants of Ethiopian Tax RevenueamanualNo ratings yet

- Solved You Are The Tax Manager in A Cpa Office OneDocument1 pageSolved You Are The Tax Manager in A Cpa Office OneAnbu jaromiaNo ratings yet

- Adobe Scan 23 Jan 2024Document1 pageAdobe Scan 23 Jan 2024rajeshNo ratings yet

- Tds - NCLT Directs Tax Department To Return TDS To Bankrupt Precision Fasteners - The Economic TimesDocument1 pageTds - NCLT Directs Tax Department To Return TDS To Bankrupt Precision Fasteners - The Economic TimescreateNo ratings yet

- GST ChallanDocument1 pageGST ChallanWilfred DsouzaNo ratings yet

- Home Loan Interest Deduction Under Section 24 of Income TaxDocument6 pagesHome Loan Interest Deduction Under Section 24 of Income TaxshahpinkalNo ratings yet

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruMithlesh KumarNo ratings yet

- Statement of Submissin of Audit Report in Form-704Document704 pagesStatement of Submissin of Audit Report in Form-704Suruchi Kejriwal GoyalNo ratings yet

- T2 Corporation – Income Tax Guide 2020Document137 pagesT2 Corporation – Income Tax Guide 2020Toofan KhanNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document5 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Sourabh PunshiNo ratings yet

- Taxation of Partnerships PowerpointDocument7 pagesTaxation of Partnerships PowerpointALAJID, KIM EMMANUELNo ratings yet

- 3113 4 Zero Rated TransactionsDocument5 pages3113 4 Zero Rated TransactionsConic DurangparangNo ratings yet

- Finnish TaxationDocument217 pagesFinnish TaxationTobi MemoryNo ratings yet