You might also like

- Trainer Activity: All Adrift!Document6 pagesTrainer Activity: All Adrift!DollyNo ratings yet

- Precision Motors Division CaseDocument9 pagesPrecision Motors Division CaseAliza Rizvi50% (2)

- ABC Corporation Financial Statement Analysis for Year 201B and 201ADocument4 pagesABC Corporation Financial Statement Analysis for Year 201B and 201AarisuNo ratings yet

- MBA 670 Quiz 1 SolutionsDocument2 pagesMBA 670 Quiz 1 SolutionsLauren LoshNo ratings yet

- Cargo Security Awareness - Etextbook - 2nd - Ed - 2016 - TCGP-79Document185 pagesCargo Security Awareness - Etextbook - 2nd - Ed - 2016 - TCGP-79kien Duy Phan80% (5)

- MODEL - Investment AnalysisDocument6 pagesMODEL - Investment AnalysisAndrei Cătălin UngureanuNo ratings yet

- L1 - Assignment 1 - Process CostingDocument2 pagesL1 - Assignment 1 - Process CostinglalalalaNo ratings yet

- 7 by ProductDocument36 pages7 by ProducthidaNo ratings yet

- Chap 4 Job CostingDocument9 pagesChap 4 Job CostingWadiah AkbarNo ratings yet

- Combined Profitability Analysis: January, 2020Document23 pagesCombined Profitability Analysis: January, 2020S PaulNo ratings yet

- Manacc CaseDocument3 pagesManacc Caseshivam kumarNo ratings yet

- 21.08.2020 L11-12Document10 pages21.08.2020 L11-12sajedulNo ratings yet

- Calculating Average Inventory, Payables and Receivables PeriodsDocument10 pagesCalculating Average Inventory, Payables and Receivables PeriodssajedulNo ratings yet

- 21.08.2020 L11-12Document10 pages21.08.2020 L11-12sajedulNo ratings yet

- Past Exam QuestionDocument2 pagesPast Exam QuestionWenhidzaNo ratings yet

- Item Units Unit Cost $ Qty/day Direct Costs Prod. Cost/day $ Prod. Cost/month $Document3 pagesItem Units Unit Cost $ Qty/day Direct Costs Prod. Cost/day $ Prod. Cost/month $jamazalaleNo ratings yet

- Calculating Production CostsDocument5 pagesCalculating Production CostsbereketNo ratings yet

- Dente Q2Document3 pagesDente Q2hanna fhaye denteNo ratings yet

- Acctg201 PCLosses PDFDocument11 pagesAcctg201 PCLosses PDFElla DavisNo ratings yet

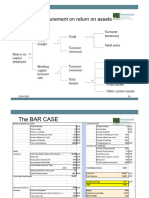

- Impact of Procurement On Return On Assets: Turnover (Revenue) Total CostsDocument3 pagesImpact of Procurement On Return On Assets: Turnover (Revenue) Total Costssithum877No ratings yet

- Group 5 - Sec D - MA - Shun ElectronicsDocument7 pagesGroup 5 - Sec D - MA - Shun ElectronicsYATIN BAJAJNo ratings yet

- Financial Modeling AssignmentDocument11 pagesFinancial Modeling AssignmentamerNo ratings yet

- Jawaban JOC - NewDocument15 pagesJawaban JOC - NewNabella Roma DesiNo ratings yet

- BUSINESS PLAN 2009-2011 LOTHO HK (Sunglasses Brand)Document8 pagesBUSINESS PLAN 2009-2011 LOTHO HK (Sunglasses Brand)Sebastien MorinNo ratings yet

- Project Cost Summary Report: ProjectsDocument3 pagesProject Cost Summary Report: ProjectsMahmoud A. YousefNo ratings yet

- Day 5 - Class ExerciseDocument5 pagesDay 5 - Class Exerciseum23328No ratings yet

- Cost Per Unit: BleachDocument13 pagesCost Per Unit: BleachjrmutengeraNo ratings yet

- Tut 8 - Management AccountingDocument29 pagesTut 8 - Management AccountingTao LoheNo ratings yet

- Balance Sheet: Assets Value Liabilities ValueDocument32 pagesBalance Sheet: Assets Value Liabilities ValueomernoumanNo ratings yet

- FAMA '22 SolutionDocument4 pagesFAMA '22 SolutionRushil JoshiNo ratings yet

- Process Costing SystemsDocument8 pagesProcess Costing SystemsArun kumarNo ratings yet

- DOCUMENTACIÓN Y NEGOCIACIÓN EN INGLÉS: PROPUESTA DE UN NUEVO PRODUCTO FERRERODocument19 pagesDOCUMENTACIÓN Y NEGOCIACIÓN EN INGLÉS: PROPUESTA DE UN NUEVO PRODUCTO FERREROJESSICA HURTADO LOZANONo ratings yet

- 02A Normal Absorption Costing ACC9811 2021 One Slide Per PageDocument15 pages02A Normal Absorption Costing ACC9811 2021 One Slide Per PageDANNo ratings yet

- CFM33A3 2022 AO5 MemoDocument5 pagesCFM33A3 2022 AO5 MemoLameck ZuluNo ratings yet

- Annual Fixed Cost, P/Yr FC D+I+Hti: Net Income Generated, Ph/Yr Ni (Co - Ra-Dca) Ca OpDocument14 pagesAnnual Fixed Cost, P/Yr FC D+I+Hti: Net Income Generated, Ph/Yr Ni (Co - Ra-Dca) Ca OpJan James GrazaNo ratings yet

- Business Results: Fiscal Year Ended March 31, 2021Document49 pagesBusiness Results: Fiscal Year Ended March 31, 2021atvoya JapanNo ratings yet

- Pdfanddoc 346021 PDFDocument41 pagesPdfanddoc 346021 PDFઅનુરુપ સોનીNo ratings yet

- CP9 - Job CostingDocument11 pagesCP9 - Job CostingesaiinternalauditNo ratings yet

- Analisa Beli Via BankDocument19 pagesAnalisa Beli Via Bankalim pujiantoNo ratings yet

- BEP - Breakeven Point ، نقطة تعادلDocument4 pagesBEP - Breakeven Point ، نقطة تعادلSalah HusseinNo ratings yet

- Feasibility study for small jewelry projectDocument11 pagesFeasibility study for small jewelry projectDonaldJenningsNo ratings yet

- Easy Feasibility Study For Small ProjectsDocument13 pagesEasy Feasibility Study For Small ProjectsOrcajada, Mariz Allysa S.No ratings yet

- Percale Bedding Linen + Skin Set / Curtain: Haji Ismail & Sons LimitedDocument4 pagesPercale Bedding Linen + Skin Set / Curtain: Haji Ismail & Sons LimitedIqbal MalikNo ratings yet

- Earned Value Management ExampleDocument1 pageEarned Value Management ExampleLuis Miguel Parra GNo ratings yet

- Joint cost allocation using sales value at split off pointDocument6 pagesJoint cost allocation using sales value at split off pointAiko KharendhaNo ratings yet

- San Nicolas UicrDocument1 pageSan Nicolas UicrHerwin NavarreteNo ratings yet

- Almost Real Unit and Cost Data Cutting Department ReportDocument20 pagesAlmost Real Unit and Cost Data Cutting Department ReportSymon AngeloNo ratings yet

- Seider Profitability Analysis-1.1Document21 pagesSeider Profitability Analysis-1.1LFNo ratings yet

- Plaid-Clad Manufacturing Cost ReportsDocument5 pagesPlaid-Clad Manufacturing Cost ReportsSalvador BrionesNo ratings yet

- Upm Interim Report q3 2023 enDocument31 pagesUpm Interim Report q3 2023 envyy6pngsqcNo ratings yet

- Day 4 (My)Document11 pagesDay 4 (My)Jhilmil JeswaniNo ratings yet

- Process CostingDocument4 pagesProcess CostingKrizia Mae FloresNo ratings yet

- Lecture 03Document30 pagesLecture 03Labib ShahNo ratings yet

- Brand X Company Cost of Production Report AnalysisDocument8 pagesBrand X Company Cost of Production Report AnalysisJessica MalijanNo ratings yet

- Actual Material Qty Schedule Units WD EUPDocument10 pagesActual Material Qty Schedule Units WD EUPJuMakMat MacNo ratings yet

- Given: March: Quantity ScheduleDocument10 pagesGiven: March: Quantity ScheduleVon Andrei MedinaNo ratings yet

- Standard Costing AnalysisDocument106 pagesStandard Costing AnalysisUsama Riaz100% (1)

- Hola KolaDocument3 pagesHola KolaAmit BiswalNo ratings yet

- Average Cost Method and FIFO Inventory CostingDocument7 pagesAverage Cost Method and FIFO Inventory CostingAnne MendozaNo ratings yet

- Software ExcelDocument12 pagesSoftware ExcelparvathysiyyerNo ratings yet

- Cost AccountingDocument29 pagesCost Accountingsino akoNo ratings yet

- The Bourne Identity ReviewDocument3 pagesThe Bourne Identity ReviewBoldizsár Zeyk AnnaNo ratings yet

- AST Study Centers 2021 Updated Till 25oct2021 GOVT DATADocument33 pagesAST Study Centers 2021 Updated Till 25oct2021 GOVT DATAprasadNo ratings yet

- Gabriel MarcelDocument6 pagesGabriel MarcelCeciBohoNo ratings yet

- Senior Power Apps Engineer JobDocument3 pagesSenior Power Apps Engineer JobMichałNo ratings yet

- Impromtu Speech Covid 19Document7 pagesImpromtu Speech Covid 19ESWARY A/P VASUDEVAN MoeNo ratings yet

- TECHNICALPAPER2Document8 pagesTECHNICALPAPER2spiderwebNo ratings yet

- Myths of Membership The Politics of Legitimation in UN Security Council ReformDocument20 pagesMyths of Membership The Politics of Legitimation in UN Security Council ReformCaroline GassiatNo ratings yet

- Materials that absorb and decayDocument2 pagesMaterials that absorb and decayDominic NoblezaNo ratings yet

- Medical Services Recruitment Board (MRB)Document20 pagesMedical Services Recruitment Board (MRB)durai PandiNo ratings yet

- Cement and Concrete Research: Amin Abrishambaf, Mário Pimentel, Sandra NunesDocument13 pagesCement and Concrete Research: Amin Abrishambaf, Mário Pimentel, Sandra NunesJoseluis Dejesus AnguloNo ratings yet

- Enthalpy ChangesDocument2 pagesEnthalpy Changesapi-296833859100% (1)

- Accenture Sustainable ProcurementDocument2 pagesAccenture Sustainable ProcurementAnupriyaSaxenaNo ratings yet

- Senthamarai Kannan S V (Kannan) Oracle SCM and Oracle MFG, Oracle ASCP (PTP/OTC/WMS/ASCP/INV/PIM/OPM) Manager/Sr Manager/Functional LeadDocument8 pagesSenthamarai Kannan S V (Kannan) Oracle SCM and Oracle MFG, Oracle ASCP (PTP/OTC/WMS/ASCP/INV/PIM/OPM) Manager/Sr Manager/Functional LeadKarunya KannanNo ratings yet

- AET Aetna 2017 Investor Day Presentation - Final (For Website) PDFDocument73 pagesAET Aetna 2017 Investor Day Presentation - Final (For Website) PDFAla BasterNo ratings yet

- Imeko WC 2012 TC21 O10Document5 pagesImeko WC 2012 TC21 O10mcastillogzNo ratings yet

- Choose the Right Low Boy Trailer ModelDocument42 pagesChoose the Right Low Boy Trailer ModelOdlnayer AllebramNo ratings yet

- Medical Education For Healthcare Professionals: Certificate / Postgraduate Diploma / Master of Science inDocument4 pagesMedical Education For Healthcare Professionals: Certificate / Postgraduate Diploma / Master of Science inDana MihutNo ratings yet

- Probability Concepts and Random Variable - SMTA1402: Unit - IDocument105 pagesProbability Concepts and Random Variable - SMTA1402: Unit - IVigneshwar SNo ratings yet

- LPI PH PDFDocument4 pagesLPI PH PDFHumberto Tapias CutivaNo ratings yet

- Intersecting Lines Intersecting Lines Parallel Lines Same LineDocument7 pagesIntersecting Lines Intersecting Lines Parallel Lines Same Lineapi-438357152No ratings yet

- Resume Masroor 3Document3 pagesResume Masroor 3mohammad masroor zahid ullahNo ratings yet

- Dual Domain Image Encryption Using Bit Plane Scrambling and Sub - Band ScramblingDocument16 pagesDual Domain Image Encryption Using Bit Plane Scrambling and Sub - Band Scramblingraja rishyantNo ratings yet

- My Personal TimelineDocument4 pagesMy Personal TimelineJerlando M. Pojadas Jr.67% (3)

- Otr Product CatalogDocument116 pagesOtr Product CatalogIwan KurniawanNo ratings yet

- CV of Dr. Mohammad TahirDocument12 pagesCV of Dr. Mohammad TahirMuhammad FayyazNo ratings yet

- m5 Mage The AscensionDocument20 pagesm5 Mage The AscensionQuentin Agnes0% (1)

- Ps1 GeneralDocument2 pagesPs1 Generalkulin123456No ratings yet

- Social Engineering For Pentester PenTest - 02 - 2013Document81 pagesSocial Engineering For Pentester PenTest - 02 - 2013Black RainNo ratings yet