You might also like

- Quiz 1Document3 pagesQuiz 1Van MateoNo ratings yet

- Suggested Answers - Audit of Cash AR Liab HandoutsDocument10 pagesSuggested Answers - Audit of Cash AR Liab HandoutsBanna SplitNo ratings yet

- Cebu Cpar Center, Inc.: QuestionsDocument1 pageCebu Cpar Center, Inc.: Questionsriza147No ratings yet

- Chapter 08 - Bank and CashDocument13 pagesChapter 08 - Bank and CashMkhonto XuluNo ratings yet

- Auditing Quiz Audit of CashDocument4 pagesAuditing Quiz Audit of CashLoveli Breindaelyn Rivera0% (2)

- College Accounting Final ExamDocument17 pagesCollege Accounting Final ExamAiron Keith Along100% (1)

- ReSA CPA Review Batch 42 Audit Problems SolutionsDocument12 pagesReSA CPA Review Batch 42 Audit Problems SolutionsMellaniNo ratings yet

- Review For EA05 and EA06 - BSA16Document34 pagesReview For EA05 and EA06 - BSA16NwjwNo ratings yet

- Advanced-Auditing-2016-Solution ManualDocument156 pagesAdvanced-Auditing-2016-Solution ManualAly grace gamuedaNo ratings yet

- Bank Reconciliation HandoutsDocument7 pagesBank Reconciliation HandoutsRODELYN PERALESNo ratings yet

- 112 ReconSeatworkDocument2 pages112 ReconSeatworkGinie Lyn RosalNo ratings yet

- Final Exam 12 PDF FreeDocument17 pagesFinal Exam 12 PDF FreeEmey CalbayNo ratings yet

- Solution Chapter 12 Bank ReconciliationDocument5 pagesSolution Chapter 12 Bank Reconciliationsaiful syahmiNo ratings yet

- Activity 2Document3 pagesActivity 2kathie alegarmeNo ratings yet

- Cash and Cash Equivalent: Problem 1Document4 pagesCash and Cash Equivalent: Problem 1Ab CNo ratings yet

- Espinilla Auditing 2016Document157 pagesEspinilla Auditing 2016Mayarra Gumpic50% (2)

- Ga Problem SolvingDocument9 pagesGa Problem SolvinggarciarhodjeannemarthaNo ratings yet

- Topic 7: Cash Management and Control, Preparation Bank Reconciliations and Maintaining A Petty Cash System Solutions To Tutorial QuestionsDocument3 pagesTopic 7: Cash Management and Control, Preparation Bank Reconciliations and Maintaining A Petty Cash System Solutions To Tutorial QuestionsMitchell BylartNo ratings yet

- Preliminary Exams-Aud 301A YmataDocument6 pagesPreliminary Exams-Aud 301A YmataMa Yra YmataNo ratings yet

- Assignment No. 2 (Solution)Document5 pagesAssignment No. 2 (Solution)Christine MalayoNo ratings yet

- AUD2016Ed Espenilla Solution GuideV2Document156 pagesAUD2016Ed Espenilla Solution GuideV2Stephanie Ann AsuncionNo ratings yet

- QII Answer KeyDocument12 pagesQII Answer KeyJane GavinoNo ratings yet

- End of Chapter Problems 3-1 (Cash Count)Document3 pagesEnd of Chapter Problems 3-1 (Cash Count)Exzyl Vixien Iexsha LoxinthNo ratings yet

- Philippine Politics and Governance DLPDocument6 pagesPhilippine Politics and Governance DLPDMarrie Abao Boniao-LabadanNo ratings yet

- Bank Reconcilation Statement Example PDFDocument4 pagesBank Reconcilation Statement Example PDFZara ShoukatNo ratings yet

- Tutorial Sheet 4Document8 pagesTutorial Sheet 4Hhvvgg BbbbNo ratings yet

- Home Office and Branch Accounting: Solutions To Multiple Choice Problems Problem 1Document6 pagesHome Office and Branch Accounting: Solutions To Multiple Choice Problems Problem 1Jason BautistaNo ratings yet

- Audit of Cash PDFDocument3 pagesAudit of Cash PDFVincent SampianoNo ratings yet

- ABM 6 CE4 Cash FINALDocument1 pageABM 6 CE4 Cash FINALPotatoNo ratings yet

- Problems Bank Reconciliation: With Analysis & SolutionsDocument20 pagesProblems Bank Reconciliation: With Analysis & SolutionscsolutionNo ratings yet

- Answer Key Quiz 5 Actbas2 T3 PDFDocument5 pagesAnswer Key Quiz 5 Actbas2 T3 PDFCharles TuazonNo ratings yet

- Orca Share Media1506255759817Document156 pagesOrca Share Media1506255759817Pauline Kisha Castro86% (7)

- Chapter 4 - Teacher's Manual - Ifa Part 1aDocument16 pagesChapter 4 - Teacher's Manual - Ifa Part 1aCharmae Agan CaroroNo ratings yet

- Quiz 3-Audit CashDocument8 pagesQuiz 3-Audit CashCindy CrausNo ratings yet

- Test I. TRUE OR FALSE (25 Points)Document10 pagesTest I. TRUE OR FALSE (25 Points)Charmaine Mari OlmosNo ratings yet

- Answer Key. 3-9Document1 pageAnswer Key. 3-9Teree ZuNo ratings yet

- PDF Prac Acc Chapter 15 16docxdocx DDDocument37 pagesPDF Prac Acc Chapter 15 16docxdocx DDBetty SantiagoNo ratings yet

- Aud. Prob.Document16 pagesAud. Prob.Ria Alanis CastilloNo ratings yet

- ABC Company Bank Reconciliation ProblemsDocument4 pagesABC Company Bank Reconciliation ProblemsFrancis Lloyd TongsonNo ratings yet

- Chapter 3 - Bank ReconciliationDocument2 pagesChapter 3 - Bank ReconciliationJerome_JadeNo ratings yet

- Bank ReconDocument2 pagesBank ReconEnitsuj Eam EugarbalNo ratings yet

- Auditing EspinillaDocument156 pagesAuditing EspinillaMin100% (1)

- V1620034 - Dzaky FarhansyahDocument11 pagesV1620034 - Dzaky FarhansyahDzaky FarhansyahNo ratings yet

- Quiz 1 On Applied AuditingDocument4 pagesQuiz 1 On Applied AuditingVixen Aaron EnriquezNo ratings yet

- Sol. Man. - Chapter 3 - Bank Reconciliation - Ia Part 1aDocument16 pagesSol. Man. - Chapter 3 - Bank Reconciliation - Ia Part 1aMiguel AmihanNo ratings yet

- Advanced Auditing 2016 Solution GuideDocument10 pagesAdvanced Auditing 2016 Solution GuideSchool FilesNo ratings yet

- Apino Jan Dave T. BSA 4-1 QuizDocument14 pagesApino Jan Dave T. BSA 4-1 QuizRosemarie RamosNo ratings yet

- This Study Resource Was: Guerrero / German Siy / de Jesus / Lim / FerrerDocument5 pagesThis Study Resource Was: Guerrero / German Siy / de Jesus / Lim / FerrerKyla Dane P. PradoNo ratings yet

- CCE Quiz - SolutionDocument2 pagesCCE Quiz - SolutionJoovs JoovhoNo ratings yet

- Quiz No. 2 Multiple Choice and Problem Solving QuestionsDocument6 pagesQuiz No. 2 Multiple Choice and Problem Solving QuestionsNonami AbicoNo ratings yet

- Bank Reconciliation ProblemsDocument37 pagesBank Reconciliation ProblemsAldrin Lozano87% (15)

- Perilla Geriqjoedn 1Document20 pagesPerilla Geriqjoedn 1Geriq Joeden PerillaNo ratings yet

- Soal A - Home Office Vs Branch (40%) : DimintaDocument2 pagesSoal A - Home Office Vs Branch (40%) : DimintaAlvin Prabu WNo ratings yet

- Assignment No 4Document3 pagesAssignment No 4analyngrace1No ratings yet

- Review On Financial Statements AnalysisDocument2 pagesReview On Financial Statements AnalysisJohn Carl SoledadNo ratings yet

- Ref 1 Prelim Quiz 1Document7 pagesRef 1 Prelim Quiz 1Melanie MinaNo ratings yet

- Quiz - Chapter 3 - Bank ReconciliationDocument6 pagesQuiz - Chapter 3 - Bank ReconciliationSHE80% (10)

- Accounts Payable: A Guide to Running an Efficient DepartmentFrom EverandAccounts Payable: A Guide to Running an Efficient DepartmentNo ratings yet

- IV - Audit of The Investing and Financing CycleDocument8 pagesIV - Audit of The Investing and Financing CycleVan MateoNo ratings yet

- II - Audit of The Revenue and Receipt CycleDocument13 pagesII - Audit of The Revenue and Receipt CycleVan MateoNo ratings yet

- BSA 1B Obligations and ContractDocument1 pageBSA 1B Obligations and ContractVan MateoNo ratings yet

- III - A Audit of The Expenditure and Disbursements CycleDocument10 pagesIII - A Audit of The Expenditure and Disbursements CycleVan MateoNo ratings yet

- Audit of CashDocument6 pagesAudit of CashVan MateoNo ratings yet

- Audit of CashDocument6 pagesAudit of CashVan MateoNo ratings yet

- Auditing Theories and Problems Quiz WEEK 1Document19 pagesAuditing Theories and Problems Quiz WEEK 1Sarah GNo ratings yet

- Module For Fundamentals of AccountingDocument26 pagesModule For Fundamentals of AccountingVan MateoNo ratings yet

- Album of Lyre and DrumsDocument3 pagesAlbum of Lyre and DrumsVan MateoNo ratings yet

- Chapter I Introduction To AccountinngDocument17 pagesChapter I Introduction To AccountinngVan MateoNo ratings yet

- Acorns Securities LLC: Tax Information Account 00179240287154Document12 pagesAcorns Securities LLC: Tax Information Account 00179240287154ivanmarquezlariosNo ratings yet

- Confidential Advanced Taxation Mid-Semester Assessment QuestionsDocument5 pagesConfidential Advanced Taxation Mid-Semester Assessment QuestionsSanthiya MogenNo ratings yet

- Top 30 MCQ - Banking Reform & NationalizationDocument4 pagesTop 30 MCQ - Banking Reform & NationalizationEthan HuntNo ratings yet

- Hakeem Ullah 0xutxhDocument5 pagesHakeem Ullah 0xutxhHakeem UllahNo ratings yet

- Macroeconomics VII: Aggregate Supply: Gavin Cameron Lady Margaret HallDocument18 pagesMacroeconomics VII: Aggregate Supply: Gavin Cameron Lady Margaret HallTendai MatsikureNo ratings yet

- MM Cia 1Document7 pagesMM Cia 1debarati majiNo ratings yet

- FSA Chapter 7Document3 pagesFSA Chapter 7Nadia ZahraNo ratings yet

- Key External Factors Opportunities: External Factor Evaluation (EFE) MatrixDocument11 pagesKey External Factors Opportunities: External Factor Evaluation (EFE) MatrixCamilleNo ratings yet

- AI assignment_KAUR_GURNOOR (1)Document9 pagesAI assignment_KAUR_GURNOOR (1)gurnoorkaurgilllNo ratings yet

- 52413A91C69B46EDA3EA049FDE2295C9Document10 pages52413A91C69B46EDA3EA049FDE2295C9ProjectinsightNo ratings yet

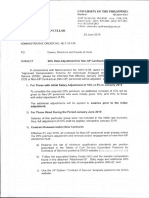

- 20% Rate Adjustment For Non-UP Contractual PersonnelDocument5 pages20% Rate Adjustment For Non-UP Contractual PersonnelKristine CruzNo ratings yet

- VSL Strand Post Tensioning Systems Technical Catalogue - 2019 01Document55 pagesVSL Strand Post Tensioning Systems Technical Catalogue - 2019 01Frederick NaplesNo ratings yet

- Material Wealth and Hard Work Material Wealth A Better LifeDocument9 pagesMaterial Wealth and Hard Work Material Wealth A Better LifeNgọc HânNo ratings yet

- HDFC Bank Credit Card Customer Care Number - 24x7Document5 pagesHDFC Bank Credit Card Customer Care Number - 24x7Baswamy CseNo ratings yet

- Beijing Review - March 05, 2020Document54 pagesBeijing Review - March 05, 2020NISHANT SRIVASTAVANo ratings yet

- MoneyDocument2 pagesMoneyLet's do thisNo ratings yet

- JIN Yihong. Rethinking The Iron Girls' PDFDocument22 pagesJIN Yihong. Rethinking The Iron Girls' PDFEdelson ParnovNo ratings yet

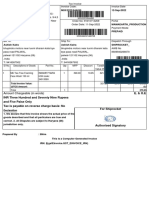

- INR Three Hundred and Seventy Nine Rupees and Five Paise Only Tax Is Payable On Reverse Charge Basis: No E. & O.EDocument1 pageINR Three Hundred and Seventy Nine Rupees and Five Paise Only Tax Is Payable On Reverse Charge Basis: No E. & O.EArnav KalraNo ratings yet

- Audit Risk of Harvey Co.Document2 pagesAudit Risk of Harvey Co.Anirosh ShresthaNo ratings yet

- FINANCIAL ACCOUNTING 1 CASH AND CASH EQUIVALENTSDocument9 pagesFINANCIAL ACCOUNTING 1 CASH AND CASH EQUIVALENTSPau Santos76% (29)

- Eurocontrol Lssip 2022 Bosnia HerzegovinaDocument133 pagesEurocontrol Lssip 2022 Bosnia HerzegovinaDeniNo ratings yet

- Micro Plastics India - Micro Plastics To Invest 500 CR in Tamil Nadu Toy Plant - The Economic TimesDocument1 pageMicro Plastics India - Micro Plastics To Invest 500 CR in Tamil Nadu Toy Plant - The Economic TimescreateNo ratings yet

- RMC No. 19-2022Document7 pagesRMC No. 19-2022Shiela Marie MaraonNo ratings yet

- Registered Post: On 29 Sep 2022 Vide This Officeletter No. 8926/07/E8 DT 29 Sep 2022. andDocument1 pageRegistered Post: On 29 Sep 2022 Vide This Officeletter No. 8926/07/E8 DT 29 Sep 2022. andSunil SalunkeNo ratings yet

- PETRONAS Activity Outlook 2020 2022 PDFDocument80 pagesPETRONAS Activity Outlook 2020 2022 PDFIsmail SayutiNo ratings yet

- Money Banking Imp QuestionsDocument22 pagesMoney Banking Imp QuestionsAshwani PathakNo ratings yet

- 1 Understanding - Expected - ReturnsDocument9 pages1 Understanding - Expected - ReturnsRoshan JhaNo ratings yet

- Pestel Analysis of Cleaning Service IndustryDocument4 pagesPestel Analysis of Cleaning Service IndustryRh Wribhu100% (1)

- ELEM-District: - Particular Amount: Actual MOOE Expenses 2015 For The Month ofDocument1 pageELEM-District: - Particular Amount: Actual MOOE Expenses 2015 For The Month ofCHANIELOU MARTINEZNo ratings yet

- Architect ListDocument22 pagesArchitect ListNikhil WangeNo ratings yet