You might also like

- To the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioFrom EverandTo the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioNo ratings yet

- Peer Company COmparision For Startups NewDocument2 pagesPeer Company COmparision For Startups NewBiki BhaiNo ratings yet

- FINANCIAL REPORTING ANALYSIS OF NISHAT AND CRESCENT TEXTILEDocument44 pagesFINANCIAL REPORTING ANALYSIS OF NISHAT AND CRESCENT TEXTILEAbdul KhaliqNo ratings yet

- Zylog SystemsDocument2 pagesZylog SystemsGirish RamachandraNo ratings yet

- CCAFDocument21 pagesCCAFsanket patilNo ratings yet

- H123 Report Card AnalysisSub-Title Key Operating Metrics and Financial RatiosDocument30 pagesH123 Report Card AnalysisSub-Title Key Operating Metrics and Financial RatiosNikhilKapoor29No ratings yet

- Hurdle Rare Benchamark - 0930Document3 pagesHurdle Rare Benchamark - 0930Pedro K. LatapíNo ratings yet

- QUESTIONSDocument19 pagesQUESTIONSrahidarzooNo ratings yet

- Peer Company Comparison For StartupsDocument2 pagesPeer Company Comparison For StartupsBiki BhaiNo ratings yet

- MCD IU FactSheet Nov 2020Document5 pagesMCD IU FactSheet Nov 2020Swati SNo ratings yet

- Profitability and solvency ratios show Varun Beverages' strong financial performanceDocument8 pagesProfitability and solvency ratios show Varun Beverages' strong financial performancesanket patilNo ratings yet

- ABL ModelDocument14 pagesABL ModelUmer FarooqNo ratings yet

- Total Income - Annual: Sales Sales YoyDocument16 pagesTotal Income - Annual: Sales Sales YoyKshatrapati SinghNo ratings yet

- Financial DepartmentDocument27 pagesFinancial DepartmentPiyu VyasNo ratings yet

- JK Paper DCFDocument42 pagesJK Paper DCFChintan MataliaNo ratings yet

- Financial Analysis (Detail)Document68 pagesFinancial Analysis (Detail)Paulo NascimentoNo ratings yet

- Trend and Common Size AnalysisDocument4 pagesTrend and Common Size AnalysisZuhair RiazNo ratings yet

- Fortnightly Banking Update: Deposit Growth Moderated But Bank Credit Growth Moderates Even MoreDocument3 pagesFortnightly Banking Update: Deposit Growth Moderated But Bank Credit Growth Moderates Even Morekumar ganeshNo ratings yet

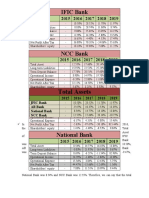

- IFIC Bank's Total Assets Grew Most in 2017Document8 pagesIFIC Bank's Total Assets Grew Most in 2017Rahnoma Bilkis NavaidNo ratings yet

- Gudang Garam (IDX GGRM) Financial Statement Forecasting and Discount Cash Flow (DCF) Valuation ModelDocument2 pagesGudang Garam (IDX GGRM) Financial Statement Forecasting and Discount Cash Flow (DCF) Valuation ModelAndi ErnandaNo ratings yet

- Pakistan Tobacco Company: A Subsidiary of British American Tobacco (BAT)Document15 pagesPakistan Tobacco Company: A Subsidiary of British American Tobacco (BAT)AbdulRehmanHaschameNo ratings yet

- Analyst Presentation 2018Document90 pagesAnalyst Presentation 2018Sanket SharmaNo ratings yet

- Equity Valuation Report - Corticeira AmorimDocument3 pagesEquity Valuation Report - Corticeira AmorimFEPFinanceClubNo ratings yet

- Commercial Planning V02.1Document35 pagesCommercial Planning V02.1nishant.mishraNo ratings yet

- Performance Evaluation Of: AB BankDocument15 pagesPerformance Evaluation Of: AB BankAuifuzzaman NoyunNo ratings yet

- Sugar Project FinalDocument27 pagesSugar Project FinalAtharvaNo ratings yet

- Bakery Case DataDocument6 pagesBakery Case DataMoritzNo ratings yet

- 2022 Asset Wealth ManagementDocument22 pages2022 Asset Wealth ManagementSankaty LightNo ratings yet

- Historicals: Terminal Growth Rate: 2.5% EV/EBIT Exit MultipleDocument10 pagesHistoricals: Terminal Growth Rate: 2.5% EV/EBIT Exit MultipleMary NingNo ratings yet

- Axis Bank InvestmentDocument32 pagesAxis Bank Investment22satendraNo ratings yet

- Keterangan 2015 2016 2017: Year To Year Anylisis Analisis Common SizeDocument9 pagesKeterangan 2015 2016 2017: Year To Year Anylisis Analisis Common SizeSahirah Hafizhah TaqiyyahNo ratings yet

- HR Team Day Out - May 2012 v3Document61 pagesHR Team Day Out - May 2012 v3sashaNo ratings yet

- Nvidia DCFDocument28 pagesNvidia DCFibs56225No ratings yet

- PG One Pager CopyDocument2 pagesPG One Pager CopyAlexandra Denise PeraltaNo ratings yet

- KPIT TechnologyDocument41 pagesKPIT Technologysanjayrathi457No ratings yet

- PE ModellingDocument8 pagesPE ModellingMona RishiNo ratings yet

- Profitability Ratio Analysis 2014-2018Document4 pagesProfitability Ratio Analysis 2014-2018Shahriar ShihabNo ratings yet

- How Long Will Tailwinds ContinueDocument27 pagesHow Long Will Tailwinds ContinuemijjNo ratings yet

- Bond Price Sensitivity AnalysisDocument5 pagesBond Price Sensitivity AnalysisZhenyi ZhuNo ratings yet

- PT Semen Indonesia, TBK: 1H 2015 Update - Weak MarginDocument7 pagesPT Semen Indonesia, TBK: 1H 2015 Update - Weak MarginRendy SentosaNo ratings yet

- Nucleus Software Exports LimitedDocument5 pagesNucleus Software Exports LimitedUmangNo ratings yet

- Core Income Down 3.2% in 2Q18, Behind Both COL and Consensus EstimatesDocument8 pagesCore Income Down 3.2% in 2Q18, Behind Both COL and Consensus EstimatesheheheheNo ratings yet

- 2018 08 01 PH e Urc - 2 PDFDocument8 pages2018 08 01 PH e Urc - 2 PDFherrewt rewterwNo ratings yet

- 2point2 Capital - Investor Update Q1 FY22Document6 pages2point2 Capital - Investor Update Q1 FY22Anil GowdaNo ratings yet

- SBI financial performance analysis 2015-2020Document26 pagesSBI financial performance analysis 2015-2020JAKKU SRI HARSHANo ratings yet

- Maruti India Limited: SuzukiDocument15 pagesMaruti India Limited: SuzukiNikhil AdesaraNo ratings yet

- Ceo2023 Crosstabs Final All 1Document14 pagesCeo2023 Crosstabs Final All 1Karlin RickNo ratings yet

- RatiosDocument25 pagesRatiosJarin Tasnim LiraNo ratings yet

- Amazon DCF: Ticker Implied Share Price Date Current Share PriceDocument4 pagesAmazon DCF: Ticker Implied Share Price Date Current Share PriceFrancesco GliraNo ratings yet

- HSBC Financial Analysis PPDocument68 pagesHSBC Financial Analysis PPKareem L SayidNo ratings yet

- Examining risk and return of two asset portfolioDocument10 pagesExamining risk and return of two asset portfoliosushant ahujaNo ratings yet

- Financial Management Analysis of Vardhman, Grasim, Raymond and SiyaramsDocument13 pagesFinancial Management Analysis of Vardhman, Grasim, Raymond and SiyaramsSaharsh SaraogiNo ratings yet

- Financial ModellingDocument13 pagesFinancial ModellingBrendon McNo ratings yet

- TWTR Final-Selected-Metrics-and-FinancialsDocument3 pagesTWTR Final-Selected-Metrics-and-FinancialsBonnie DebbarmaNo ratings yet

- Ch03 P15 SolutionsDocument16 pagesCh03 P15 SolutionsM E0% (1)

- Financial Projections Model v6.8.4Document28 pagesFinancial Projections Model v6.8.4george.komnasNo ratings yet

- Fmi S14Document66 pagesFmi S14Arpit JainNo ratings yet

- Excel Shortcut Master KeyDocument15 pagesExcel Shortcut Master KeyBajazid NadžakNo ratings yet

- Annual Letter 2016Document25 pagesAnnual Letter 2016Incandescent CapitalNo ratings yet

- Problem 1 San Pedro: AssetsDocument9 pagesProblem 1 San Pedro: AssetsGastelyn JacintoNo ratings yet

- Investors' Perceptions of Mutual Fund Risk and Returns in Hyderabad KarnatakaDocument13 pagesInvestors' Perceptions of Mutual Fund Risk and Returns in Hyderabad KarnatakaDR.VENGATESAN.G COMMERCE-CANo ratings yet

- Reviewer ToaDocument25 pagesReviewer ToaFlorence CuansoNo ratings yet

- IAI – How to Analyze Accounts ReceivableDocument7 pagesIAI – How to Analyze Accounts Receivablemarvin barlisoNo ratings yet

- Festival Bonanza: Smart Gift (Double Benefit)Document12 pagesFestival Bonanza: Smart Gift (Double Benefit)Sam sanNo ratings yet

- Phi Long WCWDocument48 pagesPhi Long WCWGia MinhNo ratings yet

- Homework Assignment Chapter 18 - 1Document4 pagesHomework Assignment Chapter 18 - 1adlkfjNo ratings yet

- Problem SDocument6 pagesProblem SNisha IndunilNo ratings yet

- Mutual FundsDocument32 pagesMutual Fundsapi-309082881No ratings yet

- Name: Vienna Jhane G. Mamaril Section: Bsa 1B: Queuing NeedsDocument2 pagesName: Vienna Jhane G. Mamaril Section: Bsa 1B: Queuing NeedsVienna MamarilNo ratings yet

- Balance Sheet RatiosDocument30 pagesBalance Sheet Ratiosumar iqbalNo ratings yet

- Entrepreneur's Awareness and Risk Perception To Equity Market On Stock InvestingDocument11 pagesEntrepreneur's Awareness and Risk Perception To Equity Market On Stock InvestingOm PatelNo ratings yet

- 90 Nielson & Company, Inc. v. Lepanto Consolidated Mining CompanyDocument5 pages90 Nielson & Company, Inc. v. Lepanto Consolidated Mining CompanyGain Dee100% (1)

- Banking Awareness Topic Wise - FDI &FPIDocument3 pagesBanking Awareness Topic Wise - FDI &FPIVeer AshutoshNo ratings yet

- Download Advanced Algos Outsmarting The Market One Algorithm At A Time A Comprehensive Algorithmic Trading Guide For 2024 Bissette full chapterDocument68 pagesDownload Advanced Algos Outsmarting The Market One Algorithm At A Time A Comprehensive Algorithmic Trading Guide For 2024 Bissette full chaptermary.gordon132100% (2)

- 0Document5 pages0Nicco Ortiz50% (2)

- CH 13Document28 pagesCH 13lupavNo ratings yet

- EZZSTEEL Strategic Audit: Presented To: Dr. Saneya El-GalalyDocument20 pagesEZZSTEEL Strategic Audit: Presented To: Dr. Saneya El-GalalyCarlos NgNo ratings yet

- Financial Statement Analysis: 17-5 The Dividend Yield Is TheDocument51 pagesFinancial Statement Analysis: 17-5 The Dividend Yield Is TheMafi De LeonNo ratings yet

- International Equity Markets ExplainedDocument36 pagesInternational Equity Markets ExplainedVrinda GargNo ratings yet

- Full Download Advanced Accounting 7th Edition Jeter Solutions ManualDocument35 pagesFull Download Advanced Accounting 7th Edition Jeter Solutions Manualjacksongubmor100% (17)

- 3 ProbabilityDocument54 pages3 ProbabilitySouvik Ghosh100% (1)

- Analysis Costco & Walt-Mart (Ratios) FinalDocument33 pagesAnalysis Costco & Walt-Mart (Ratios) FinalVerónica Aguilar Villacís100% (1)

- Stock ValuationDocument4 pagesStock ValuationMary Yvonne AresNo ratings yet

- 14 ROY v. HERBOSADocument2 pages14 ROY v. HERBOSAJul A.No ratings yet

- Module 2 - Forwards & FuturesDocument84 pagesModule 2 - Forwards & FuturesSanjay PatilNo ratings yet

- Understanding Mutual FundsDocument7 pagesUnderstanding Mutual FundsAnnalyn ArnaldoNo ratings yet

- Assignment Questions SapmDocument2 pagesAssignment Questions SapmKeerthini SadashivaNo ratings yet

- Performance and Awareness of Mutual FundsDocument53 pagesPerformance and Awareness of Mutual FundsBhavesh PatelNo ratings yet

- Syllabus - Mba Semester III (Full Time) - New CourseDocument40 pagesSyllabus - Mba Semester III (Full Time) - New CourseRam KrishnaNo ratings yet