You might also like

- Establish & Maintain An Accural Accounting SystemDocument34 pagesEstablish & Maintain An Accural Accounting SystemMagarsaa Hirphaa100% (2)

- 05 Cash Cash EquivalentsDocument54 pages05 Cash Cash EquivalentsFordan Antolino83% (12)

- Distance Education: Instructional ModuleDocument10 pagesDistance Education: Instructional ModuleRD Suarez100% (3)

- Adjusting EntriesDocument7 pagesAdjusting EntriesJon PangilinanNo ratings yet

- Inancial CCTG: Adjusting The AccountsDocument28 pagesInancial CCTG: Adjusting The AccountsLj BesaNo ratings yet

- Grade11 Fabm1 Q2 Week1Document22 pagesGrade11 Fabm1 Q2 Week1Mickaela MonterolaNo ratings yet

- FABM AJE and Adjusted Trial Balance Service BusinessDocument18 pagesFABM AJE and Adjusted Trial Balance Service BusinessMarchyrella Uoiea Olin Jovenir50% (4)

- Basic Accounting Concepts, Conventions, Bases & Policies, Concept of Balance SheetDocument44 pagesBasic Accounting Concepts, Conventions, Bases & Policies, Concept of Balance SheetVivan Menezes86% (7)

- Fabm1: Quarter 4 - Module 9: Preparing Adjusting EntriesDocument17 pagesFabm1: Quarter 4 - Module 9: Preparing Adjusting EntriesIva Milli Ayson100% (3)

- CESGA Programme Overview-2020.09Document16 pagesCESGA Programme Overview-2020.09KK LeeNo ratings yet

- FABM 1 Q2 Weeks 1 2Document12 pagesFABM 1 Q2 Weeks 1 2Maria Hannahlyn Batumbakal DimakulanganNo ratings yet

- The Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingDocument12 pagesThe Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingKim Patrick Victoria100% (1)

- Customer Information FormDocument2 pagesCustomer Information FormNeil Ramoneda59% (17)

- Result Amazon OsirishDocument3 pagesResult Amazon OsirishRoby WahyudiNo ratings yet

- ABM FABM1-Q4-Week-1Document26 pagesABM FABM1-Q4-Week-1Just OkayNo ratings yet

- FabmDocument68 pagesFabmAllyzza Jayne Abelido100% (1)

- 2b. Manufacturing Overhead CR PDFDocument15 pages2b. Manufacturing Overhead CR PDFpoNo ratings yet

- ACCTG Module - Unit 4 Adjusting The AccountsDocument8 pagesACCTG Module - Unit 4 Adjusting The AccountsMary Lou SouribioNo ratings yet

- Fabm1 Q3 M7 WK7 9 For DigitizedDocument16 pagesFabm1 Q3 M7 WK7 9 For Digitizedquaresmarenzel715No ratings yet

- Philippine School of Business Administration: Cpa ReviewDocument13 pagesPhilippine School of Business Administration: Cpa ReviewLoi GachoNo ratings yet

- Business Finance Module Week 2 3Document17 pagesBusiness Finance Module Week 2 3Camille CornelioNo ratings yet

- Rangkuman UTS (AutoRecovered) (Repaired) (Repaired)Document44 pagesRangkuman UTS (AutoRecovered) (Repaired) (Repaired)Maulani DwiNo ratings yet

- Iii. The Adjusting ProcessDocument4 pagesIii. The Adjusting Processby ScribdNo ratings yet

- PPT Week 2 OkDocument28 pagesPPT Week 2 OkmyliteguessNo ratings yet

- Castellano Fa1 Midterm Module Ba1 ABC LeganesDocument28 pagesCastellano Fa1 Midterm Module Ba1 ABC Leganesma. tricia soberanoNo ratings yet

- Math 11 ABM FABM1 Q2 Week 1 For StudentsDocument19 pagesMath 11 ABM FABM1 Q2 Week 1 For StudentsRich Allen Mier UyNo ratings yet

- Concept Note No.1Document7 pagesConcept Note No.1ISIDRO, PAULA S. 12 ABM 7ANo ratings yet

- Module 3 - The Adjusting ProcessDocument2 pagesModule 3 - The Adjusting ProcessTBA PacificNo ratings yet

- Module 6Document13 pagesModule 6kohi jellyNo ratings yet

- Lecture - Notes On Accounting ProcessDocument7 pagesLecture - Notes On Accounting ProcessNica PunzalanNo ratings yet

- Business Math 9: Department of Education SPTVEDocument10 pagesBusiness Math 9: Department of Education SPTVESunday MochicanaNo ratings yet

- Abm 1-W6.M3.T1.L3Document21 pagesAbm 1-W6.M3.T1.L3mbiloloNo ratings yet

- Explain The Accrual Basis of Accounting and The Reasons For Adjusting EntriesDocument5 pagesExplain The Accrual Basis of Accounting and The Reasons For Adjusting EntrieshelenaNo ratings yet

- Business FInance Week 5 and 6Document51 pagesBusiness FInance Week 5 and 6Jonathan De villa100% (1)

- Business Transactions and Their Analysis As Applied To The Accounting Cycle of A Service BusinessDocument8 pagesBusiness Transactions and Their Analysis As Applied To The Accounting Cycle of A Service BusinessNinia Cresil Ann JalagatNo ratings yet

- Business FInance Week 3 and 4Document68 pagesBusiness FInance Week 3 and 4Jonathan De villa100% (1)

- Business FInance Week 3 and 4Document75 pagesBusiness FInance Week 3 and 4Hyakkima NasumeNo ratings yet

- Administer Subsidiary Accounts and LedgersDocument43 pagesAdminister Subsidiary Accounts and LedgersrameNo ratings yet

- Assignm NTDocument12 pagesAssignm NTSami ullah khan BabarNo ratings yet

- Q3 Module 1Document15 pagesQ3 Module 1shamrockjusayNo ratings yet

- Adjusting Entries - MaravillaDocument3 pagesAdjusting Entries - MaravillaJustine MaravillaNo ratings yet

- Measuring Business Income: The Adjusting Process: Chapter OutlineDocument4 pagesMeasuring Business Income: The Adjusting Process: Chapter OutlineARSLAN HUSSAINNo ratings yet

- Measuring Profitability and Financial Position On The Financial Statements Chapter 4Document66 pagesMeasuring Profitability and Financial Position On The Financial Statements Chapter 4Rupesh Pol100% (1)

- 1st Semester (Digital Notebook - FABM2)Document5 pages1st Semester (Digital Notebook - FABM2)Raven RubiNo ratings yet

- Chapter 2 Accounting CycleDocument17 pagesChapter 2 Accounting CycleEzy playboyNo ratings yet

- The Adjusting Process PDFDocument3 pagesThe Adjusting Process PDFMaria Cristina ArcillaNo ratings yet

- Accounting: Ankon Gopal BanikDocument9 pagesAccounting: Ankon Gopal BanikAnkon Gopal BanikNo ratings yet

- Balance Sheet AccountingDocument7 pagesBalance Sheet AccountingGauravNo ratings yet

- FOW 9 - PA - Notes Session 2Document15 pagesFOW 9 - PA - Notes Session 223006022No ratings yet

- Financial Statement AnalysisDocument32 pagesFinancial Statement AnalysisMuhammad KhawajaNo ratings yet

- Lesson 1 - Adjusting Entries 2 - Worksheet With Adjustments 3 - Financial Statements 4 - Closing Entries and Post-Closing Trial BalanceDocument40 pagesLesson 1 - Adjusting Entries 2 - Worksheet With Adjustments 3 - Financial Statements 4 - Closing Entries and Post-Closing Trial BalanceAngel LuzlesNo ratings yet

- Our Lady of The Pillar College Cauayan: Prelim Examination Accounting 1 &2Document8 pagesOur Lady of The Pillar College Cauayan: Prelim Examination Accounting 1 &2John Lloyd LlananNo ratings yet

- 100 006 Measuring Business IncomeDocument4 pages100 006 Measuring Business IncomeaymieNo ratings yet

- Lesson 1 Analyzing Recording TransactionsDocument6 pagesLesson 1 Analyzing Recording TransactionsklipordNo ratings yet

- Adjusting EntriesDocument5 pagesAdjusting EntriesDyenNo ratings yet

- Name: OBJECTIVE: To Test The Employees Identifying, Analyzation and Journalizing. Highlight Your AnswersDocument7 pagesName: OBJECTIVE: To Test The Employees Identifying, Analyzation and Journalizing. Highlight Your AnswersErica NicolasuraNo ratings yet

- Financial Acctg Reporting 1 Chapter 5Document20 pagesFinancial Acctg Reporting 1 Chapter 5Charise Jane ZullaNo ratings yet

- Fabm 1 - Q2 - Week 1 - Module 1 - Preparing Adjusting Entries of A Service Business - For ReproductionDocument16 pagesFabm 1 - Q2 - Week 1 - Module 1 - Preparing Adjusting Entries of A Service Business - For ReproductionJosephine C QuibidoNo ratings yet

- Basic AccountingDocument13 pagesBasic AccountingPavan Kumar RNo ratings yet

- Module 005 Week002-Finacct3 Review of The Accounting ProcessDocument7 pagesModule 005 Week002-Finacct3 Review of The Accounting Processman ibeNo ratings yet

- Accounting Lesson 3Document4 pagesAccounting Lesson 3SayyedKhawarAbbasNo ratings yet

- 03 - Adjusting EntriesDocument3 pages03 - Adjusting EntriesJamie ToriagaNo ratings yet

- FCA Notes 01Document8 pagesFCA Notes 01US10No ratings yet

- Adjusting The Accounts: Learning ObjectivesDocument6 pagesAdjusting The Accounts: Learning ObjectivesArif HasanNo ratings yet

- Meghan Swarga ResailedDocument2 pagesMeghan Swarga ResailedJanice SeterraNo ratings yet

- Honeybrook Noncomplying MuricesDocument2 pagesHoneybrook Noncomplying MuricesJanice SeterraNo ratings yet

- Intros Vaporate KavitaDocument2 pagesIntros Vaporate KavitaJanice SeterraNo ratings yet

- Module 7 ICT 141Document7 pagesModule 7 ICT 141Janice SeterraNo ratings yet

- Module 1 ICT 141 Module 1: Definition of AccountingDocument4 pagesModule 1 ICT 141 Module 1: Definition of AccountingJanice SeterraNo ratings yet

- Module 2 ICT 141 Module 2: Branches of AccountingDocument4 pagesModule 2 ICT 141 Module 2: Branches of AccountingJanice SeterraNo ratings yet

- Module 4 ICT 141 Module 4: Forms of Business OrganizationsDocument4 pagesModule 4 ICT 141 Module 4: Forms of Business OrganizationsJanice SeterraNo ratings yet

- Physical Science Quarter 2 Module 9 Dual Nature of ElectronsDocument33 pagesPhysical Science Quarter 2 Module 9 Dual Nature of ElectronsJanice SeterraNo ratings yet

- q4 Module 8 Physical ScienceDocument25 pagesq4 Module 8 Physical ScienceJanice SeterraNo ratings yet

- From:: Domestic Wire Transfer RequestDocument3 pagesFrom:: Domestic Wire Transfer RequestWidya AyuNo ratings yet

- Bafia 1989 & Cba 2009Document13 pagesBafia 1989 & Cba 2009Mahyuddin KhalidNo ratings yet

- E11 Optimum Capital StructureDocument10 pagesE11 Optimum Capital StructureTENGKU ANIS TENGKU YUSMANo ratings yet

- New Start Up Account SocDocument1 pageNew Start Up Account SocMoorthi VNo ratings yet

- Disclosure No. 140 2021 Annual Report For Fiscal Year Ended September 30 2020 SEC Form 17 ADocument153 pagesDisclosure No. 140 2021 Annual Report For Fiscal Year Ended September 30 2020 SEC Form 17 AJan Nicklaus S. BunagNo ratings yet

- P1-1A Analyze Transactions and Compute Net Income: InstructionsDocument14 pagesP1-1A Analyze Transactions and Compute Net Income: InstructionsIdrisNo ratings yet

- Revision Worksheet As LevelDocument2 pagesRevision Worksheet As LevelRuchira Sanket KaleNo ratings yet

- IIBF Journal Bank QuestDocument50 pagesIIBF Journal Bank QuestAbhishek Kumar SinghNo ratings yet

- Mini Case 8Document4 pagesMini Case 8JOBIN VARGHESENo ratings yet

- Accounting Practice Set Forms ANIMEDocument20 pagesAccounting Practice Set Forms ANIMETrishia Camille SatuitoNo ratings yet

- Micro Credit ThailandDocument4 pagesMicro Credit ThailandNISTYear5No ratings yet

- Unit 3-Time Value of MoneyDocument12 pagesUnit 3-Time Value of MoneyGizaw BelayNo ratings yet

- Far 102 - Cash - Bank Reconciliation PDFDocument3 pagesFar 102 - Cash - Bank Reconciliation PDFPatty LapuzNo ratings yet

- Basic Accounting-RatiosDocument22 pagesBasic Accounting-RatiosSala SahariNo ratings yet

- Multiple Choices QuestionsDocument7 pagesMultiple Choices QuestionsrenoNo ratings yet

- Financial StatementsDocument38 pagesFinancial StatementsRize TakatsukiNo ratings yet

- Interview Capsule by Bankers AddaDocument38 pagesInterview Capsule by Bankers Addadevendra_tomarNo ratings yet

- Review Chapter 8-10 WK Session With AnswerDocument13 pagesReview Chapter 8-10 WK Session With AnswerJijisNo ratings yet

- Full - Na Grade Group1 Job Organizasort Staff - PositionDocument74 pagesFull - Na Grade Group1 Job Organizasort Staff - PositionIrfan AhmadNo ratings yet

- Cherry Vantica - 201950336 - Uts - Ak318d - Apliaud - LBR JawabDocument13 pagesCherry Vantica - 201950336 - Uts - Ak318d - Apliaud - LBR JawabCherry VanticaNo ratings yet

- C GTQ W4 N Pyvg PFedhDocument2 pagesC GTQ W4 N Pyvg PFedhAbhinav VermaNo ratings yet

- Therefore, The Yield To Call For The Bond Is 6,65%Document3 pagesTherefore, The Yield To Call For The Bond Is 6,65%Bought By UsNo ratings yet

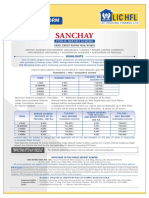

- LIC Housing Finance LTD FDDocument6 pagesLIC Housing Finance LTD FDBiswa Jyoti GuptaNo ratings yet

- ITC Financial Result Q4 FY2023 SfsDocument6 pagesITC Financial Result Q4 FY2023 Sfsaanchal prasadNo ratings yet

- Celesta Terms and ConditionsDocument6 pagesCelesta Terms and ConditionsLUCtech win10No ratings yet