You might also like

- Extract The MFT With Icat and Parse It With analyzeMFTDocument9 pagesExtract The MFT With Icat and Parse It With analyzeMFTCarlos CajigasNo ratings yet

- Financial Statements: Statement of Profit or Loss and Other Comprehensive Income DR CRDocument8 pagesFinancial Statements: Statement of Profit or Loss and Other Comprehensive Income DR CRTawanda Tatenda HerbertNo ratings yet

- Accounting Lesson 17 - Royalty AccountsDocument38 pagesAccounting Lesson 17 - Royalty AccountsRameshKumarMurali79% (19)

- Philippine Accountancy Review For Excellence: A. Format of Computation (Bir Form 1801)Document17 pagesPhilippine Accountancy Review For Excellence: A. Format of Computation (Bir Form 1801)beayaoNo ratings yet

- Leases Study MaterialDocument37 pagesLeases Study MaterialHammadNo ratings yet

- Lecture 4 Part 1Document12 pagesLecture 4 Part 1Hoàng NhiNo ratings yet

- IND AS 116 - RegularDocument54 pagesIND AS 116 - Regularkapsemansi1No ratings yet

- Readme JumboDocument4 pagesReadme JumboJulzNo ratings yet

- 6-IFRS 16 - SummaryDocument6 pages6-IFRS 16 - SummaryMushahid IslamNo ratings yet

- MAFP - Finance - Accounts Receivables ProcessesDocument96 pagesMAFP - Finance - Accounts Receivables ProcessesabdelrahmaanmedhatNo ratings yet

- 7.2 Tex LTD - Lease Payment Schedule and Journal EntriesDocument2 pages7.2 Tex LTD - Lease Payment Schedule and Journal EntriesSesethuNo ratings yet

- 20201104044854Document27 pages20201104044854hasharawanNo ratings yet

- Books of Intermediate Lessor Operating LeaseDocument2 pagesBooks of Intermediate Lessor Operating LeaseCzar Ysmael RabayaNo ratings yet

- CHAPTER 21 (Accounting of Leases) AnswerDocument2 pagesCHAPTER 21 (Accounting of Leases) AnswerShofaa HaniifahNo ratings yet

- ATM Session 5Document14 pagesATM Session 5Saksham AgrawalNo ratings yet

- 7.2 Finance Lease Payment Schedule and Journal Entries - BarDocument2 pages7.2 Finance Lease Payment Schedule and Journal Entries - BarBennie KingNo ratings yet

- Fin - BIP-ACC-211-Week-8-9Document10 pagesFin - BIP-ACC-211-Week-8-9gelNo ratings yet

- From Deposit: Currency Deposit Funds B.)Document4 pagesFrom Deposit: Currency Deposit Funds B.)thea balinasNo ratings yet

- Statement of Financial PositionDocument3 pagesStatement of Financial PositionClemyNo ratings yet

- Income Tax - VK SinghaniaDocument598 pagesIncome Tax - VK SinghaniaKartik67% (3)

- State of Financial PositionDocument1 pageState of Financial PositionlancealcarazNo ratings yet

- ScreenshotDocument1 pageScreenshotKalyanGurramNo ratings yet

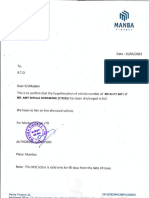

- Manba Finance Closing LetterDocument2 pagesManba Finance Closing LetterRudhvi100% (1)

- Royalty AccountingDocument10 pagesRoyalty AccountingsmlingwaNo ratings yet

- Reporting Mid 3Document5 pagesReporting Mid 3asmaNo ratings yet

- Initial Measurement:: Year Lease Payment Discount Factor Present Value of Lease PaymentDocument4 pagesInitial Measurement:: Year Lease Payment Discount Factor Present Value of Lease PaymentTuan Huy Cao pcpNo ratings yet

- (HO 1) ERG-TAX 1-Estate TaxDocument15 pages(HO 1) ERG-TAX 1-Estate Taxyna kyleneNo ratings yet

- ACTBFAR - Unit 1 - Manufacturing - Part 3 - Financial Statements - Study Guide PDFDocument7 pagesACTBFAR - Unit 1 - Manufacturing - Part 3 - Financial Statements - Study Guide PDFAlyx Gabrielle GocoNo ratings yet

- 04-Loans-001 - Loan Statement OverviewDocument4 pages04-Loans-001 - Loan Statement OverviewKeszeg Beáta ZsuzsánnaNo ratings yet

- Krishna Hights MalkapurDocument3 pagesKrishna Hights Malkapursachindorlikar123No ratings yet

- F7 - Presenatation - Day 2Document30 pagesF7 - Presenatation - Day 2anon_17214281No ratings yet

- Chapter A: ComputationeDocument2 pagesChapter A: ComputationeMechaella Shella Ningal ApolinarioNo ratings yet

- Problem Set 3Document7 pagesProblem Set 3Jade BilisNo ratings yet

- Important Questions For May 22 - Compressed - Watermark - Ac43aff8 Ccb7 4278 Bf94 Fa8e7c7f105bDocument22 pagesImportant Questions For May 22 - Compressed - Watermark - Ac43aff8 Ccb7 4278 Bf94 Fa8e7c7f105bannabsn0No ratings yet

- Specimen of A Trial Balance: S.No. Particulars L.F. Debit CreditDocument1 pageSpecimen of A Trial Balance: S.No. Particulars L.F. Debit CreditArun SankarNo ratings yet

- Previous: QuestionsDocument6 pagesPrevious: Questions2erwrNo ratings yet

- Previous: QuestionsDocument6 pagesPrevious: QuestionsSuyash PandeyNo ratings yet

- Clause 44-Working NotesDocument3 pagesClause 44-Working NotesFaizan AhmedNo ratings yet

- Admission of A PartnerDocument23 pagesAdmission of A Partner20CMH35 DHATCHAYAYINI. KNo ratings yet

- Pert 3 (Laporan Keuangan 2)Document7 pagesPert 3 (Laporan Keuangan 2)Yani SupriyaniNo ratings yet

- Property Summary Sheet: I. Unit PricingDocument43 pagesProperty Summary Sheet: I. Unit PricingSG PropTalkNo ratings yet

- Final Accounts: PruningDocument27 pagesFinal Accounts: PruningSarmad Sadiq E4 42No ratings yet

- AUDIT L12 NBFC NewDocument3 pagesAUDIT L12 NBFC NewRemaining lifeNo ratings yet

- 7.4 Motor Spares Ltd-Lease Identification, Journal Entries and DisclosureDocument5 pages7.4 Motor Spares Ltd-Lease Identification, Journal Entries and DisclosureSesethuNo ratings yet

- Accountancy All FormulaDocument23 pagesAccountancy All FormulaThe Unknown vlogger100% (1)

- Partnership Reviewer Part 2 of 2Document23 pagesPartnership Reviewer Part 2 of 2Chelit LadylieGirl FernandezNo ratings yet

- Transfer: &business TaxationDocument13 pagesTransfer: &business TaxationSophia LadrilloNo ratings yet

- 4.0 Royalties Accounts-1Document12 pages4.0 Royalties Accounts-1Victor KiruiNo ratings yet

- Certificate of Payment: tJ6/IlDocument6 pagesCertificate of Payment: tJ6/IlAjay MedikondaNo ratings yet

- Provisional Tax Calculation For The Financial Year 2010-2011 Name Divyesh Desai ID Pan No. Designation SexDocument3 pagesProvisional Tax Calculation For The Financial Year 2010-2011 Name Divyesh Desai ID Pan No. Designation Sexdivyesh_desaiNo ratings yet

- Ias 36Document21 pagesIas 36f9vertexlearningsolutionsNo ratings yet

- Robinsons Daiso v. CIRDocument35 pagesRobinsons Daiso v. CIRaudreydql5No ratings yet

- Mea TkawmdkwmkmwkDocument40 pagesMea TkawmdkwmkmwkIvo MahesaNo ratings yet

- Tampoa Ae211 Unit 1 Assessment ProblemsDocument12 pagesTampoa Ae211 Unit 1 Assessment ProblemsJahna Kay TampoaNo ratings yet

- S.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDocument11 pagesS.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDheer BhanushaliNo ratings yet

- Sis 873 Rel Interfield Const Corp 03 13 18Document3 pagesSis 873 Rel Interfield Const Corp 03 13 18dean winterNo ratings yet

- FAR - MIDTERM - SEATWORK - Accruals, Depreciation and Bad DebtsDocument4 pagesFAR - MIDTERM - SEATWORK - Accruals, Depreciation and Bad Debtsshe kioraNo ratings yet

- MA Burlington 02 (Neopost11)Document11 pagesMA Burlington 02 (Neopost11)jjkkjjkkjjNo ratings yet

- Depreciation Account: Rahul Kumar Rahul KR Ambastha Rahul Nigam Rajeev RanjanDocument14 pagesDepreciation Account: Rahul Kumar Rahul KR Ambastha Rahul Nigam Rajeev RanjanPrincy KumariNo ratings yet

- The Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeFrom EverandThe Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeNo ratings yet

- This Is Not A Frank Ocean Cover Album: Alan ChazaroDocument9 pagesThis Is Not A Frank Ocean Cover Album: Alan ChazaroStacy HardyNo ratings yet

- Emona Communications Board - Dxiq-45G: Product ApplicationDocument2 pagesEmona Communications Board - Dxiq-45G: Product ApplicationtomichelNo ratings yet

- Mid TermDocument7 pagesMid TermPaulusHariRatnopanowoNo ratings yet

- Wyse 5020 Thin Client Data SheetDocument2 pagesWyse 5020 Thin Client Data SheetYasser AbdellaNo ratings yet

- BRB Siloen SR 383-1Document2 pagesBRB Siloen SR 383-1m daneshpour100% (1)

- Chapter 1 - 1 Introduction - A4-12pp - LOWRESDocument12 pagesChapter 1 - 1 Introduction - A4-12pp - LOWRESMarine DepartmentNo ratings yet

- Case StudyDocument22 pagesCase StudyAru Verma0% (1)

- Math Department Least Learned 4thDocument15 pagesMath Department Least Learned 4thFatima YZNo ratings yet

- Đề 49Document5 pagesĐề 49nhannguyen18102005No ratings yet

- AnswersDocument25 pagesAnswersjunk068100% (1)

- 1301 RDH 102 75 3 RevEDocument71 pages1301 RDH 102 75 3 RevEds temporalNo ratings yet

- Lesson Plan Gr. 9 Life Orientation T1 W 3&4Document4 pagesLesson Plan Gr. 9 Life Orientation T1 W 3&4jenoNo ratings yet

- Ahmad Ibrahim Memorial Lecture 2008 "Fifty Years of Constitutional Government in Malaysia"Document11 pagesAhmad Ibrahim Memorial Lecture 2008 "Fifty Years of Constitutional Government in Malaysia"PKMB1-0618 Jong Xiao WeiNo ratings yet

- Lesson Plan Grade 1Document4 pagesLesson Plan Grade 1Nhuquyen NguyenNo ratings yet

- Sample Letter Invitation To Attend Meeting To Discuss Putting in Place A Performance Improvement PlanDocument2 pagesSample Letter Invitation To Attend Meeting To Discuss Putting in Place A Performance Improvement PlanhenryNo ratings yet

- Laboratory Exercise 1 Matlab Introducction: Name SectionDocument7 pagesLaboratory Exercise 1 Matlab Introducction: Name SectionDean16031997No ratings yet

- Daily Math Review 5gradeDocument77 pagesDaily Math Review 5gradeSupriya100% (1)

- About Myself: - StrenghtsDocument2 pagesAbout Myself: - StrenghtsGabriela MoNo ratings yet

- Genesis 16:1-17:27: Ishmaelite Stories Ishmael's BirthDocument36 pagesGenesis 16:1-17:27: Ishmaelite Stories Ishmael's BirthPraise YahshuaNo ratings yet

- 10 Minute MailDocument2 pages10 Minute MailasdfaNo ratings yet

- Dynamics StudentDocument19 pagesDynamics StudentRioNo ratings yet

- Pre-Feasibility Report 1. Project Name of Company / Mine Owner LocationDocument10 pagesPre-Feasibility Report 1. Project Name of Company / Mine Owner Locationvarun2860No ratings yet

- Mercruiser QSD 2.8 L + 4.2 Engine Installation ManualDocument154 pagesMercruiser QSD 2.8 L + 4.2 Engine Installation ManualBas van den BrinkNo ratings yet

- A Grade Poetry Assessment Task From Scaffold Provided StudentDocument2 pagesA Grade Poetry Assessment Task From Scaffold Provided Studentapi-618196299No ratings yet

- Darwin WorksheetDocument2 pagesDarwin WorksheetjcrawlinsNo ratings yet

- Part A Noun and Noun PhraseDocument3 pagesPart A Noun and Noun PhraseTotoro YuNo ratings yet

- Financial Comparison of MTNL and BSNL: Project Report OnDocument5 pagesFinancial Comparison of MTNL and BSNL: Project Report OnGAURAV KUMAR CHAUHANNo ratings yet

- Working at Heights Step Ladder ChecklistDocument1 pageWorking at Heights Step Ladder ChecklistAku DaudNo ratings yet