You might also like

- CPA Exam Regulation - Entity Comparison ChartDocument5 pagesCPA Exam Regulation - Entity Comparison ChartMelissa Abel100% (1)

- Syllabus Criminal Procedure 2021-2022Document23 pagesSyllabus Criminal Procedure 2021-2022alfie100% (5)

- Small Claims FormDocument7 pagesSmall Claims FormAtty. Emmanuel Sandicho100% (3)

- G.R. No. 138031Document4 pagesG.R. No. 138031Beverly LegaspiNo ratings yet

- ST Joseph College Vs MirandaDocument2 pagesST Joseph College Vs MirandaKevinPR100% (5)

- Law of Torts in KenyaDocument41 pagesLaw of Torts in KenyaMwaura Kamau93% (28)

- Parole Board of Canada Decision: Name: Institution: FPS: File NoDocument5 pagesParole Board of Canada Decision: Name: Institution: FPS: File NoRosieGroverNo ratings yet

- 1ongsuco Vs MalonesDocument10 pages1ongsuco Vs MalonesRai-chan Junior ÜNo ratings yet

- Ongsuco V MalonesDocument10 pagesOngsuco V MalonesJane CuizonNo ratings yet

- Art 8 Onsuco Vs Malones 604 Scra 499Document9 pagesArt 8 Onsuco Vs Malones 604 Scra 499Omar Nasseef BakongNo ratings yet

- Ongsuco Vs MalonesDocument10 pagesOngsuco Vs MalonesLouie816No ratings yet

- Ongsuco vs. Malones, G.R. No. 182065, October 27, 2009Document9 pagesOngsuco vs. Malones, G.R. No. 182065, October 27, 2009JemNo ratings yet

- Ongsuco Vs Malones PDFDocument5 pagesOngsuco Vs Malones PDFLu CasNo ratings yet

- Ongsuco vs. MalonesDocument2 pagesOngsuco vs. MalonesPaola CamilonNo ratings yet

- Ongsuco Vs MalonesDocument3 pagesOngsuco Vs MalonesG Ant MgdNo ratings yet

- Ongsuco vs. MalonesDocument1 pageOngsuco vs. Malonesxx_stripped52100% (1)

- Ongsuco vs. MalonesDocument10 pagesOngsuco vs. MalonesAngelo LopezNo ratings yet

- Manila Electric Company, vs. Nelia A. BarlisDocument6 pagesManila Electric Company, vs. Nelia A. BarlisDNAANo ratings yet

- Ongsuco Vs MalonesDocument2 pagesOngsuco Vs MaloneswesleybooksNo ratings yet

- ONGSUCO V MALONESDocument4 pagesONGSUCO V MALONESSuzyNo ratings yet

- Lucero Vs City Government of PasigDocument3 pagesLucero Vs City Government of PasigMelody Lim DayagNo ratings yet

- Hagonoy Market Vendor Association Vs Municipality of HagonoyDocument3 pagesHagonoy Market Vendor Association Vs Municipality of HagonoyRaymond Roque100% (2)

- 6 Jardine Davis Vs AliposaDocument9 pages6 Jardine Davis Vs AliposaAnty CastilloNo ratings yet

- 4 Jardine Davies Insurance Brokerage v. AliposaDocument4 pages4 Jardine Davies Insurance Brokerage v. AliposaFrancis Leo TianeroNo ratings yet

- Hagonoy v. CIRDocument8 pagesHagonoy v. CIRVener Angelo MargalloNo ratings yet

- Napocor Vs Municipality of NavotasDocument2 pagesNapocor Vs Municipality of NavotasAmeir MuksanNo ratings yet

- Testate Estate of Concordia Lim VS City of ManilaDocument2 pagesTestate Estate of Concordia Lim VS City of ManilaRia GabsNo ratings yet

- G.R. Nos. 120681-83: 1âwphi1.nêtDocument21 pagesG.R. Nos. 120681-83: 1âwphi1.nêtCarmil WishnieNo ratings yet

- Case DigestedDocument19 pagesCase DigestedJean Sibongga57% (7)

- American Bible Society Vs City of Manila 101 Phil 386Document13 pagesAmerican Bible Society Vs City of Manila 101 Phil 386Leomar Despi LadongaNo ratings yet

- Venus Vs DesiertoDocument12 pagesVenus Vs DesiertoSon Gabriel UyNo ratings yet

- Miller Vs MardoDocument6 pagesMiller Vs MardoDax MonteclarNo ratings yet

- NPC Vs Mun. of NavotasDocument2 pagesNPC Vs Mun. of NavotasClaudine Christine A. VicenteNo ratings yet

- G.R. No. 186014 PDFDocument9 pagesG.R. No. 186014 PDFReginald Matt Aquino SantiagoNo ratings yet

- Republic of Tile Philippines Court of Tax Appeals Quezon CityDocument43 pagesRepublic of Tile Philippines Court of Tax Appeals Quezon CityCL DelabahanNo ratings yet

- Antonio v. Commission On ElectionsDocument11 pagesAntonio v. Commission On ElectionsMark Jeson Lianza PuraNo ratings yet

- Coca-Cola Bottlers Philippines, Inc. vs. City of Manila PDFDocument15 pagesCoca-Cola Bottlers Philippines, Inc. vs. City of Manila PDFGiuliana FloresNo ratings yet

- Lita Enterprises Vs IacDocument3 pagesLita Enterprises Vs Iactwenty19 lawNo ratings yet

- Tax 2 2018 CasesDocument400 pagesTax 2 2018 CasesRussel SirotNo ratings yet

- 2 ANTONIO v. MIRANDA GR No. 135869 22 September 1999Document7 pages2 ANTONIO v. MIRANDA GR No. 135869 22 September 1999Jaime Rariza Jr.No ratings yet

- Commisioner of Customs Vs Pilipinas Shell Petroleum CorporationDocument10 pagesCommisioner of Customs Vs Pilipinas Shell Petroleum CorporationMaan ManagaytayNo ratings yet

- 04-01.city Sheriff Iligan City v. FortunadoDocument6 pages04-01.city Sheriff Iligan City v. FortunadoOdette JumaoasNo ratings yet

- SPC Realty Corp. v. Municipal Treasurer of Cainta, C.T.A. AC No. 77, (15 November 2012) PDFDocument8 pagesSPC Realty Corp. v. Municipal Treasurer of Cainta, C.T.A. AC No. 77, (15 November 2012) PDFAna EndayaNo ratings yet

- 7 Allied BankingDocument11 pages7 Allied BankingGracia SullanoNo ratings yet

- 36 - G.R. No. 137621 - Hagonoy Market Vendor Assoc v. Mun. of HagonoyDocument9 pages36 - G.R. No. 137621 - Hagonoy Market Vendor Assoc v. Mun. of HagonoyMichael HizonNo ratings yet

- City of Manila vs. Coca ColaDocument9 pagesCity of Manila vs. Coca ColaARCHIE AJIASNo ratings yet

- Nursery Care Corporation vs. AcevedoDocument8 pagesNursery Care Corporation vs. AcevedoARCHIE AJIASNo ratings yet

- Tayaban VS PeopleDocument6 pagesTayaban VS PeopleRijane CantanillaNo ratings yet

- Bardillon Vs Bgy MasiliDocument3 pagesBardillon Vs Bgy MasiliQuoleteNo ratings yet

- G.R. No. 180651Document9 pagesG.R. No. 180651Ran NgiNo ratings yet

- 124125-1998-City Sheriff Iligan City v. FortunadoDocument6 pages124125-1998-City Sheriff Iligan City v. FortunadoHershey GabiNo ratings yet

- Jardine v. AliposaDocument5 pagesJardine v. AliposaJoy RaguindinNo ratings yet

- City Sheriff Iligian v. Fortunado G.R. No. 80390Document4 pagesCity Sheriff Iligian v. Fortunado G.R. No. 80390fgNo ratings yet

- Ang Ping Vs RTCDocument7 pagesAng Ping Vs RTCJoseph AbadianoNo ratings yet

- Du Vs JayomaDocument4 pagesDu Vs JayomaEricson MabaoNo ratings yet

- Cta 3D Ac 00077 D 2012nov15 Ass PDFDocument14 pagesCta 3D Ac 00077 D 2012nov15 Ass PDFr....aNo ratings yet

- 201288-2016-Commissioner of Customs v. Pilipinas Shell20220725-11-1bggqhwDocument11 pages201288-2016-Commissioner of Customs v. Pilipinas Shell20220725-11-1bggqhwKim FloresNo ratings yet

- Civ 2Document103 pagesCiv 2MitchayNo ratings yet

- Binay v. Sandiganbayan, GR 120681-83 (October 1, 1999)Document26 pagesBinay v. Sandiganbayan, GR 120681-83 (October 1, 1999)ChaMcbandNo ratings yet

- G.R. No. 120681-83binayDocument20 pagesG.R. No. 120681-83binayKameesa FateNo ratings yet

- Binay V SB G.R. Nos. 120681-83 and 128136Document16 pagesBinay V SB G.R. Nos. 120681-83 and 128136Alessandra Mae SalvacionNo ratings yet

- Case Digest Political LawDocument48 pagesCase Digest Political LawDexter Jonas M. LumanglasNo ratings yet

- Kilusang Bayan, Etc Vs DominguezDocument13 pagesKilusang Bayan, Etc Vs DominguezCharmaine Valientes CayabanNo ratings yet

- NPC Vs NavotasDocument12 pagesNPC Vs Navotasyan_saavedra_1No ratings yet

- 2) Atwel Vs Concepcion Progressive CorpDocument8 pages2) Atwel Vs Concepcion Progressive Corpaljohn pantaleonNo ratings yet

- Patent Laws of the Republic of Hawaii and Rules of Practice in the Patent OfficeFrom EverandPatent Laws of the Republic of Hawaii and Rules of Practice in the Patent OfficeNo ratings yet

- Petition Guardianship 1Document5 pagesPetition Guardianship 1Rijane CantanillaNo ratings yet

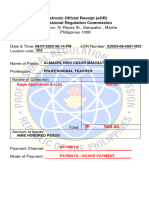

- Electronic Official Receipt (eOR) Professional Regulation CommissionDocument1 pageElectronic Official Receipt (eOR) Professional Regulation CommissionRijane CantanillaNo ratings yet

- Legaspi VS City of CebuDocument9 pagesLegaspi VS City of CebuRijane CantanillaNo ratings yet

- Cantanilla, Rijane A: Phone: +63 927 918 6062 Email: Address: P-4 Mambalite, Daet, Camarines NorteDocument2 pagesCantanilla, Rijane A: Phone: +63 927 918 6062 Email: Address: P-4 Mambalite, Daet, Camarines NorteRijane CantanillaNo ratings yet

- Real Estate MortgageDocument2 pagesReal Estate MortgageRijane CantanillaNo ratings yet

- Application LetterDocument2 pagesApplication LetterRijane CantanillaNo ratings yet

- Pauper Litigant FormatDocument2 pagesPauper Litigant FormatRijane CantanillaNo ratings yet

- PEOPLE OF THE PHILIPPINES Plaintiff Appellee v. MARTIN SIMON y SUNGA Respondent.Document30 pagesPEOPLE OF THE PHILIPPINES Plaintiff Appellee v. MARTIN SIMON y SUNGA Respondent.Rijane CantanillaNo ratings yet

- Tort MockDocument6 pagesTort MockNabil HazzazNo ratings yet

- In The Matter of The Claim of Juan J. Jimenez v. City of New York, Et Al.Document6 pagesIn The Matter of The Claim of Juan J. Jimenez v. City of New York, Et Al.Eric SandersNo ratings yet

- Contract To Sell BlankDocument3 pagesContract To Sell Blankmarc marcNo ratings yet

- National Sports Management V JR RickertDocument5 pagesNational Sports Management V JR RickertDarren Adam HeitnerNo ratings yet

- People vs. Iligan Case DigestDocument2 pagesPeople vs. Iligan Case DigestClaribel Domingo Bayani100% (1)

- People v. BernardoDocument1 pagePeople v. BernardoMaria AnalynNo ratings yet

- II. Right To Self OrganizationDocument47 pagesII. Right To Self OrganizationMA. TRISHA RAMENTONo ratings yet

- Revocation and Reduction of DonationsDocument5 pagesRevocation and Reduction of DonationsFhem WagisNo ratings yet

- Judge Valeriano Saucedo Commission on Judicial Performance Prosecution: Notice of Formal Proceedings & Charges - Tulare County Superior Court Hon. Valeriano Saucedo - Judge Judith L. Haller 4th District Court of Appeal - Judge Becky Lynn Dugan Riverside Superior Court - Judge Louis R. Hanoian San Diego County Superior Court - Victoria Henley Director-Chief Counsel California Commission on Judicial Performance - Judicial Council of California - Supreme Court of California - California State Bar AssociationDocument22 pagesJudge Valeriano Saucedo Commission on Judicial Performance Prosecution: Notice of Formal Proceedings & Charges - Tulare County Superior Court Hon. Valeriano Saucedo - Judge Judith L. Haller 4th District Court of Appeal - Judge Becky Lynn Dugan Riverside Superior Court - Judge Louis R. Hanoian San Diego County Superior Court - Victoria Henley Director-Chief Counsel California Commission on Judicial Performance - Judicial Council of California - Supreme Court of California - California State Bar AssociationCalifornia Judicial Branch News Service - Investigative Reporting Source Material & Story IdeasNo ratings yet

- BUS 2202 LJ Unit 8Document5 pagesBUS 2202 LJ Unit 8Su Myat NoeNo ratings yet

- JUDICIAL AFFIDAVIT (Nala)Document6 pagesJUDICIAL AFFIDAVIT (Nala)Edward Rey EbaoNo ratings yet

- Project DesignDocument3 pagesProject DesignCharles D. FloresNo ratings yet

- 2.undertaking Affidavite MembershipDocument1 page2.undertaking Affidavite MembershipAgilan SelvamNo ratings yet

- Vasu Tech Ltd. v. Ratna Enterprises Ltd.Document7 pagesVasu Tech Ltd. v. Ratna Enterprises Ltd.Deon FernandesNo ratings yet

- Shinji Higaki (Editor), Yuji Nasu (Editor) - Hate Speech in Japan - The Possibility of A Non-Regulatory Approach-Cambridge University Press (2021)Document526 pagesShinji Higaki (Editor), Yuji Nasu (Editor) - Hate Speech in Japan - The Possibility of A Non-Regulatory Approach-Cambridge University Press (2021)Nicole HartNo ratings yet

- Criminal IdentificationDocument70 pagesCriminal IdentificationLeah Moyao-DonatoNo ratings yet

- Cap 458 - Unconscionable Contracts OrdinanceDocument3 pagesCap 458 - Unconscionable Contracts OrdinanceCNo ratings yet

- Title Four Chapter One: Criminal Law (Articles 89-99 Notes)Document16 pagesTitle Four Chapter One: Criminal Law (Articles 89-99 Notes)ZHYRRA LOUISE BITUINNo ratings yet

- Nuique Vs SedilloDocument2 pagesNuique Vs SedilloCarlos JamesNo ratings yet

- 3.21.19 - With Profound Regret - Joel Geier Resigns From ISODocument5 pages3.21.19 - With Profound Regret - Joel Geier Resigns From ISOISO Leaks100% (1)

- Legal Office ProcedureDocument3 pagesLegal Office Procedureyes1nthNo ratings yet

- Heirs of Gozo V PH UnionDocument2 pagesHeirs of Gozo V PH UnionPamela ApacibleNo ratings yet

- Chap 3 - ExamDocument13 pagesChap 3 - ExamCandace LuhNo ratings yet

- Fundamental - Rights Chap5 - 8 - 24 PDFDocument152 pagesFundamental - Rights Chap5 - 8 - 24 PDFJassy BustamanteNo ratings yet