You might also like

- Determinants of Coffee Export Supply in Ethiopia: Error Correction Modeling ApproachDocument9 pagesDeterminants of Coffee Export Supply in Ethiopia: Error Correction Modeling Approachyusuf mohammedNo ratings yet

- Coffee Determinants NewpdfDocument20 pagesCoffee Determinants NewpdfaychiluhimchulaNo ratings yet

- Berhanu Lakew Determinants of Ethiopia ExportDocument26 pagesBerhanu Lakew Determinants of Ethiopia ExportaychiluhimchulaNo ratings yet

- The Contribution of Export Diversification For Economic GrowthDocument6 pagesThe Contribution of Export Diversification For Economic Growthet0293pteshaleNo ratings yet

- Fitsum Senior EsayDocument43 pagesFitsum Senior Esaykassahun meseleNo ratings yet

- Determinants of Egyptian Agricultural Exports: A Gravity Model ApproachDocument10 pagesDeterminants of Egyptian Agricultural Exports: A Gravity Model ApproachHugo Gallardo SejasNo ratings yet

- Chapter 2 Litreature ReviewDocument5 pagesChapter 2 Litreature ReviewyabsirayabumanNo ratings yet

- The Effect of Exchange Rates On Exports and Imports of Emerging CountriesDocument14 pagesThe Effect of Exchange Rates On Exports and Imports of Emerging CountriesAnwar ul Haq ShahNo ratings yet

- Factors Affecting Gross Domestic Product: Department of Management Information Systems (MIS), University of DhakaDocument9 pagesFactors Affecting Gross Domestic Product: Department of Management Information Systems (MIS), University of DhakaGolam Mehbub SifatNo ratings yet

- Us Universitycollege Distance Education ProgramDocument31 pagesUs Universitycollege Distance Education ProgramGeleta FesehaNo ratings yet

- Exports Innovation EgyptDocument19 pagesExports Innovation Egyptnyman493130No ratings yet

- Sample ProjectDocument17 pagesSample ProjectPaeaNo ratings yet

- Analysis of World Market For Mangoes and Its Importance For Developing CountriesDocument11 pagesAnalysis of World Market For Mangoes and Its Importance For Developing CountriesFahim KhalidNo ratings yet

- MPRA Paper 108785Document40 pagesMPRA Paper 108785Jhanelly A. BermeoNo ratings yet

- Castro ExportCostsDocument47 pagesCastro ExportCostsTan Jiunn WoeiNo ratings yet

- Impact of Exchange Rate On Exports and ImportsDocument8 pagesImpact of Exchange Rate On Exports and ImportsAli RazaNo ratings yet

- The Measurement of Total Factor ProductivityDocument27 pagesThe Measurement of Total Factor ProductivityzamirNo ratings yet

- Benchmarking Cost of Milk Production in 46 Countries PDFDocument17 pagesBenchmarking Cost of Milk Production in 46 Countries PDFJunaid MazharNo ratings yet

- Importaciones IDocument29 pagesImportaciones IMaria ColmenarezNo ratings yet

- Financial CrisisDocument46 pagesFinancial CrisisDragomirescu SpiridonNo ratings yet

- Chapter One: 1.1 Background of The StudyDocument41 pagesChapter One: 1.1 Background of The Studykassahun meseleNo ratings yet

- Export Performane of EthiopiaDocument17 pagesExport Performane of Ethiopiayusuf mohammedNo ratings yet

- Tekalign MehareDocument12 pagesTekalign MehareaychiluhimchulaNo ratings yet

- Ejw 022Document23 pagesEjw 022Tariku NetoNo ratings yet

- Estimation and Machine Learning Prediction of Imports of Goods in European Countries in The Period 2010-2019Document18 pagesEstimation and Machine Learning Prediction of Imports of Goods in European Countries in The Period 2010-2019AJHSSR JournalNo ratings yet

- Aaccsa Draft Part IIDocument4 pagesAaccsa Draft Part IIsimbiroNo ratings yet

- Determinants of Economic Growth in Ethiopia: Evidence From ARDL Approach AnalysisDocument4 pagesDeterminants of Economic Growth in Ethiopia: Evidence From ARDL Approach Analysismisganawgetachew453No ratings yet

- Buzunesh CabDocument29 pagesBuzunesh CablegasuNo ratings yet

- Bussiness ChallengeDocument31 pagesBussiness ChallengedanigeletaNo ratings yet

- Empirical Study on Import, Export and Economic Growth in AlbaniaDocument11 pagesEmpirical Study on Import, Export and Economic Growth in AlbaniaChan WhNo ratings yet

- D2 Paperon Exportandproductivityfor WB2018 ConferenceDocument72 pagesD2 Paperon Exportandproductivityfor WB2018 ConferenceFriday Tube (Tango)No ratings yet

- Balance of Payment of PakistanDocument12 pagesBalance of Payment of PakistanKalsum FayazNo ratings yet

- Impacts of Exports, Imports, Exchange Rates on Indonesia's GDPDocument29 pagesImpacts of Exports, Imports, Exchange Rates on Indonesia's GDPhikmah olaNo ratings yet

- Economies: Technical E Developing Countries: The Case of EthiopiaDocument27 pagesEconomies: Technical E Developing Countries: The Case of EthiopiaGirmaTeklehanaNo ratings yet

- Assessment of Ethiopia's Export Performance & Its Determinants by Getaneh ZelalemDocument16 pagesAssessment of Ethiopia's Export Performance & Its Determinants by Getaneh ZelalemAschalew AdaneNo ratings yet

- Effect of International Trade On Economic Growth in KenyaDocument8 pagesEffect of International Trade On Economic Growth in KenyaAlexander Decker100% (1)

- 1Document15 pages1LeulNo ratings yet

- An Assessment of The Impact of Trade Liberalisation On Welfare in Pakistan: A General Equilibrium AnalysisDocument42 pagesAn Assessment of The Impact of Trade Liberalisation On Welfare in Pakistan: A General Equilibrium AnalysisM.AliKemalNo ratings yet

- 2012.export Economic GrowthDocument15 pages2012.export Economic GrowthIpan Parin Sopian HeryanaNo ratings yet

- Dire Dawa University: College of Business and Economics Department of EconomicsDocument24 pagesDire Dawa University: College of Business and Economics Department of Economicsmulugeta teferyNo ratings yet

- ARDL by Narayan2005 - Conteng 30 MayDocument16 pagesARDL by Narayan2005 - Conteng 30 MayNurin SyafiqahNo ratings yet

- The Impacts of Tariff Rate Import Quotas On Market Access 2Document31 pagesThe Impacts of Tariff Rate Import Quotas On Market Access 2Ali HusanenNo ratings yet

- The Impace of Exchange Rates On ASEAN TradeDocument30 pagesThe Impace of Exchange Rates On ASEAN TradeDo HuongNo ratings yet

- Technology Capital - Paper - IAAE - Submit IIDocument20 pagesTechnology Capital - Paper - IAAE - Submit IIusefullakhwatNo ratings yet

- Macro PresentationDocument28 pagesMacro Presentationyared mekonnenNo ratings yet

- Economics ReportDocument6 pagesEconomics ReportMuhammadAli AbidNo ratings yet

- The Impacts of Tariff-Rate Import Quotas On MarketDocument32 pagesThe Impacts of Tariff-Rate Import Quotas On MarketPhong Lê Trần ĐăngNo ratings yet

- A6Document32 pagesA6nkemghaguivisNo ratings yet

- Public Policy Article ReviewDocument8 pagesPublic Policy Article Reviewsintayto geremewNo ratings yet

- Multisectoral Thirlwall's Law: Evidence From Ecuador (1987-2008)Document21 pagesMultisectoral Thirlwall's Law: Evidence From Ecuador (1987-2008)Marco Arroyo LazoNo ratings yet

- Total Factor Productivity Growth in European AgricultureDocument25 pagesTotal Factor Productivity Growth in European AgricultureNamagua LeeNo ratings yet

- 32 Unsh PDFDocument51 pages32 Unsh PDFKhishigbayar PurevdavgaNo ratings yet

- Relationship Between FDI, Exports, and Economic Growth in PakistanDocument8 pagesRelationship Between FDI, Exports, and Economic Growth in Pakistanmustafa hasanNo ratings yet

- 1 s2.0 S2212567116302040 MainDocument10 pages1 s2.0 S2212567116302040 MainNovitaNo ratings yet

- Determinants of ExportDocument6 pagesDeterminants of ExportGetaw AlamnewNo ratings yet

- RIFT VALLEY UNIVERSITY Group ProjectDocument13 pagesRIFT VALLEY UNIVERSITY Group Projecthassoviyan9No ratings yet

- International Journal of Production EconomicsDocument12 pagesInternational Journal of Production Economicsmaria shintaNo ratings yet

- Turkish Journal of Agriculture - Food Science and TechnologyDocument7 pagesTurkish Journal of Agriculture - Food Science and TechnologyaychiluhimchulaNo ratings yet

- Feeding future generations: How finance can boost innovation in agri-food - Executive SummaryFrom EverandFeeding future generations: How finance can boost innovation in agri-food - Executive SummaryNo ratings yet

- Coff. RoastingDocument31 pagesCoff. Roastingyenealem Abebe100% (1)

- ES 3.16 Feasibility Study and Equipment Installation To Produce Pellets From Coffee Pulp PDFDocument3 pagesES 3.16 Feasibility Study and Equipment Installation To Produce Pellets From Coffee Pulp PDFesulawyer2001No ratings yet

- ES 3.16 Feasibility Study and Equipment Installation To Produce Pellets From Coffee Pulp PDFDocument3 pagesES 3.16 Feasibility Study and Equipment Installation To Produce Pellets From Coffee Pulp PDFesulawyer2001No ratings yet

- Coff. RoastingDocument31 pagesCoff. Roastingyenealem Abebe100% (1)

- ECX Coffee Contracts Approved by ECEA March 29 2018 PDFDocument13 pagesECX Coffee Contracts Approved by ECEA March 29 2018 PDFesulawyer2001100% (1)

- CoffeeContracts PDFDocument13 pagesCoffeeContracts PDFesulawyer2001No ratings yet

- Business Development Strategy For Specialty CoffeeDocument11 pagesBusiness Development Strategy For Specialty CoffeeManita KunwarNo ratings yet

- Pre-Feasibility Study Restoring Coffee Landscapes PDFDocument74 pagesPre-Feasibility Study Restoring Coffee Landscapes PDFesulawyer2001No ratings yet

- CoffeeContracts PDFDocument13 pagesCoffeeContracts PDFesulawyer2001No ratings yet

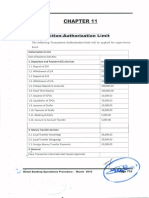

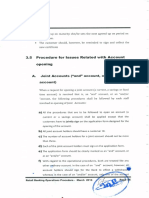

- Retail Banking Operation Procedure Part 2Document39 pagesRetail Banking Operation Procedure Part 2esulawyer2001No ratings yet

- CoffeeContracts PDFDocument13 pagesCoffeeContracts PDFesulawyer2001No ratings yet

- CoffeeContracts PDFDocument13 pagesCoffeeContracts PDFesulawyer2001No ratings yet

- Retail Banking Operation Procedure Page 45Document1 pageRetail Banking Operation Procedure Page 45esulawyer2001No ratings yet

- Coffee Production Constraints and Opportunities at Major Growing Districts of Southern EthiopiaDocument36 pagesCoffee Production Constraints and Opportunities at Major Growing Districts of Southern EthiopiaMulatu SimeonNo ratings yet

- Coffee Annual - Addis Ababa - Ethiopia - 5-29-2019 PDFDocument6 pagesCoffee Annual - Addis Ababa - Ethiopia - 5-29-2019 PDFesulawyer2001No ratings yet

- 0.diaspora Banking ProcedureDocument48 pages0.diaspora Banking Procedureesulawyer2001No ratings yet

- Coffee Annual - Addis Ababa - Ethiopia - 5-29-2019 PDFDocument6 pagesCoffee Annual - Addis Ababa - Ethiopia - 5-29-2019 PDFesulawyer2001No ratings yet

- 00... Additional Internal Controls For Payment Transaction 2Document2 pages00... Additional Internal Controls For Payment Transaction 2esulawyer2001No ratings yet

- Abay Gift Card ProcedureDocument12 pagesAbay Gift Card Procedureesulawyer2001No ratings yet

- 00... Additional Internal Controls For Payment Transaction 2Document2 pages00... Additional Internal Controls For Payment Transaction 2esulawyer2001No ratings yet

- 00 Chartable Saving Account ProcedureDocument18 pages00 Chartable Saving Account Procedureesulawyer2001No ratings yet

- Ifrs13 Fair ValueDocument19 pagesIfrs13 Fair Valueesulawyer2001No ratings yet

- 0.consumer Loan Procedure For NGO EmployeesDocument13 pages0.consumer Loan Procedure For NGO Employeesesulawyer2001No ratings yet

- Ifrs 8 and Ias 34-Operating Segments & Interim ReportingDocument46 pagesIfrs 8 and Ias 34-Operating Segments & Interim Reportingesulawyer2001No ratings yet

- IFRS Full GuideDocument84 pagesIFRS Full Guideesulawyer2001No ratings yet

- IFRS 9 FINANCIAL INSTRUMENTS-AddisDocument35 pagesIFRS 9 FINANCIAL INSTRUMENTS-Addisesulawyer2001No ratings yet

- IAS 37 ProvisionDocument38 pagesIAS 37 Provisionesulawyer2001No ratings yet

- Ifrs 15 Revenue RecognitionDocument46 pagesIfrs 15 Revenue Recognitionesulawyer2001No ratings yet

- Ifrs 16 LeasesDocument33 pagesIfrs 16 Leasesesulawyer2001100% (1)

- SantaremDocument2 pagesSantaremYopaj Ob neonNo ratings yet

- Open Group Guide: Business CapabilitiesDocument25 pagesOpen Group Guide: Business Capabilitieshanan100% (1)

- DBMS worksheet answers guideDocument55 pagesDBMS worksheet answers guideDevansh Dixit:Musically YoursNo ratings yet

- Share Curriculum Vitae Ahmed SaadDocument7 pagesShare Curriculum Vitae Ahmed SaadDR ABO HAMZANo ratings yet

- The Value of Cleanliness in The View of The Students of Two Higher Education InstitutionsDocument7 pagesThe Value of Cleanliness in The View of The Students of Two Higher Education InstitutionsjueNo ratings yet

- Eticket MR GOVINDAN UDHAYAKUMARDocument4 pagesEticket MR GOVINDAN UDHAYAKUMARNaveen SNo ratings yet

- The PARC StoryDocument59 pagesThe PARC StoryRio AlmenaNo ratings yet

- Labor dispute and illegal dismissal caseDocument5 pagesLabor dispute and illegal dismissal caseRene ValentosNo ratings yet

- Maulik Shah ResumeDocument1 pageMaulik Shah ResumeDeepak SantNo ratings yet

- Name: Roll Number: Room No: Class: MKT1602: Student InformationDocument6 pagesName: Roll Number: Room No: Class: MKT1602: Student InformationNguyen Thi Thuy Linh (K16HL)No ratings yet

- Carta de Porte Ferroviario: Modelos de Contratos InternacionalesDocument5 pagesCarta de Porte Ferroviario: Modelos de Contratos InternacionalesJonathan RccNo ratings yet

- PIMENTELDocument5 pagesPIMENTELChingNo ratings yet

- Rules of The ASUN Senate, 76th SessionDocument23 pagesRules of The ASUN Senate, 76th SessionVis Lupi Est GrexNo ratings yet

- ICAR IARI 2021 Technician T1 Recruitment NotificationDocument38 pagesICAR IARI 2021 Technician T1 Recruitment NotificationJonee SainiNo ratings yet

- Persuasive EssayDocument4 pagesPersuasive Essayapi-338650494100% (7)

- Multi Q!Document112 pagesMulti Q!collinmandersonNo ratings yet

- Chart of AccountsDocument2 pagesChart of AccountsailihengNo ratings yet

- Unit 4 - CSDocument32 pagesUnit 4 - CSyuydokostaNo ratings yet

- Aerographer's Mate Second Class, Volume 2Document444 pagesAerographer's Mate Second Class, Volume 2Bob Kowalski100% (2)

- Hacking - Reconnaissance Reference SheetDocument1 pageHacking - Reconnaissance Reference SheetMigue FriasNo ratings yet

- Getting To Grips With A320 &Document88 pagesGetting To Grips With A320 &duythienddt100% (4)

- Novena To The Christ The KingDocument3 pagesNovena To The Christ The KingManuelito Uy100% (1)

- ISO 9001 Quality Objectives - What They Are and How To Write ThemDocument7 pagesISO 9001 Quality Objectives - What They Are and How To Write ThemankitNo ratings yet

- Weights and Measures 1Document11 pagesWeights and Measures 1Chuck Lizana100% (1)

- Resume-Roberta Strange 2014Document3 pagesResume-Roberta Strange 2014Jamie RobertsNo ratings yet

- Briefing The Yemen Conflict and CrisisDocument36 pagesBriefing The Yemen Conflict and CrisisFinlay AsherNo ratings yet

- Procedures For Connection of PV Plants To MEPSO Grid in North MacedoniaDocument17 pagesProcedures For Connection of PV Plants To MEPSO Grid in North MacedoniaAleksandar JordanovNo ratings yet

- CASE 9 AmazonDocument17 pagesCASE 9 AmazonNasir HussainNo ratings yet

- SnowflakeDocument6 pagesSnowflakeDivya SrijuNo ratings yet

- Draft Letter To Sophia Wisniewska (00131538xBF0F1)Document3 pagesDraft Letter To Sophia Wisniewska (00131538xBF0F1)sarah_larimerNo ratings yet