You might also like

- Chapter 8 Cost ConceptsDocument28 pagesChapter 8 Cost ConceptsRajveer SinghNo ratings yet

- Economics Group PresentationDocument16 pagesEconomics Group Presentationaditya.babarNo ratings yet

- Cost ConceptsDocument13 pagesCost Conceptssachin8910No ratings yet

- Cost Analysis ConceptsDocument30 pagesCost Analysis ConceptsPooja SheoranNo ratings yet

- Theory of Cost & Break Even AnalysisDocument27 pagesTheory of Cost & Break Even AnalysisSandeep Singh SikerwarNo ratings yet

- CH 5 - COP - ECO120Document17 pagesCH 5 - COP - ECO120Muhammad SyukranNo ratings yet

- Lecture 6-2Document13 pagesLecture 6-2Крістіна ДобромільськаNo ratings yet

- Theory of Cost: General EconomicsDocument54 pagesTheory of Cost: General EconomicsSuman DasNo ratings yet

- Theory of CostDocument42 pagesTheory of CostSujan BhattaraiNo ratings yet

- Unit 3Document64 pagesUnit 3Soumya Ranjan DasNo ratings yet

- Session - 7 - 8 - 9 - 10 - Theory of Cost and ProductionDocument51 pagesSession - 7 - 8 - 9 - 10 - Theory of Cost and ProductionYogita ChoudharyNo ratings yet

- Econ - Unit - 5 - Cost TheoryDocument39 pagesEcon - Unit - 5 - Cost TheorySampurnaa DasNo ratings yet

- GRP PPT Cost CurvesDocument49 pagesGRP PPT Cost Curvesparulmathur85No ratings yet

- Understanding Cost: Why It Exists and Its Importance in BusinessDocument27 pagesUnderstanding Cost: Why It Exists and Its Importance in BusinessDARSHANA SNo ratings yet

- Chapter 7 Cost Theory: Topics To Be DiscussedDocument8 pagesChapter 7 Cost Theory: Topics To Be DiscussedMadhunikaNo ratings yet

- Cost Analysis: Dr. Mohsina HayatDocument36 pagesCost Analysis: Dr. Mohsina HayatFaizan QudsiNo ratings yet

- Theory of Cost: General EconomicsDocument56 pagesTheory of Cost: General Economics565 Akash SinghNo ratings yet

- COSTDocument12 pagesCOSTsatya narayanaNo ratings yet

- ProductionDocument37 pagesProductionDavidNo ratings yet

- Cost Concepts: Dr. Saad NawazDocument16 pagesCost Concepts: Dr. Saad NawazArslan MunawarNo ratings yet

- 16793theory of CostDocument55 pages16793theory of CostAnonymous 1ClGHbiT0JNo ratings yet

- Cost Concepts: Dr. Saad NawazDocument16 pagesCost Concepts: Dr. Saad NawazAhmed HamzaNo ratings yet

- Chapter 7 (Pindyck)Document31 pagesChapter 7 (Pindyck)Rahul SinhaNo ratings yet

- Understand Cost and Revenue ConceptsDocument59 pagesUnderstand Cost and Revenue ConceptsSangam KarkiNo ratings yet

- The Theory of Production and CostDocument23 pagesThe Theory of Production and CostKareem Dad MaharNo ratings yet

- Theory of Cost: Short and Long Run AnalysisDocument54 pagesTheory of Cost: Short and Long Run AnalysisHardik SharmaNo ratings yet

- TopicThree-Theory of Costs-ECO 401Document18 pagesTopicThree-Theory of Costs-ECO 401Mister PhilipsNo ratings yet

- Cost Analysis: Maximizing ProfitsDocument9 pagesCost Analysis: Maximizing ProfitsAnkit KagraNo ratings yet

- Traditional and Modern Theory of Cost)Document39 pagesTraditional and Modern Theory of Cost)LALIT SONDHI100% (4)

- The Cost of ProductionDocument75 pagesThe Cost of Productionmuhammadtaimoorkhan100% (4)

- Analysis of Cost and RevenueDocument28 pagesAnalysis of Cost and RevenueSaurav SubediNo ratings yet

- Cost NotesDocument12 pagesCost NotesGoransh KhandelwalNo ratings yet

- Cost of Production: Dr. S P SinghDocument31 pagesCost of Production: Dr. S P Singhtacamp daNo ratings yet

- L11ECO113 Cost Analysis PDFDocument18 pagesL11ECO113 Cost Analysis PDFVineet KumarNo ratings yet

- Costs of Production: Factors, Types, Curves, and AnalysisDocument23 pagesCosts of Production: Factors, Types, Curves, and AnalysisManish GuptaNo ratings yet

- Current NewsDocument24 pagesCurrent NewsShivam YadavNo ratings yet

- 11 SlidesDocument27 pages11 SlidesHameed MNo ratings yet

- CUT COSTS OR ELSE PUT THE SHUTTERS DOWNDocument78 pagesCUT COSTS OR ELSE PUT THE SHUTTERS DOWN0241ASHAYNo ratings yet

- Analysis of Perfectly Competitive MarketsDocument6 pagesAnalysis of Perfectly Competitive MarketsSunny KhatriNo ratings yet

- Cost Concepts in EconomicsDocument18 pagesCost Concepts in EconomicsHimaani ShahNo ratings yet

- Cost and Revenue Analysis in ProductionDocument36 pagesCost and Revenue Analysis in ProductionDuma DumaiNo ratings yet

- Cost Analysis: Presented By: Anindita Samajpati Sonam Aggarwal Sonal Taneja Pankaj MahajanDocument18 pagesCost Analysis: Presented By: Anindita Samajpati Sonam Aggarwal Sonal Taneja Pankaj Mahajansonal_tanejaNo ratings yet

- CostDocument69 pagesCostNITISH BHARDWAJNo ratings yet

- Cost of Production/Theory of CostDocument55 pagesCost of Production/Theory of CostBalasingam PrahalathanNo ratings yet

- Cost AnalysisDocument48 pagesCost AnalysisSADEEQ AKBARNo ratings yet

- The Analysis of Costs, & Revenue: By: Gaurav ShreekantDocument25 pagesThe Analysis of Costs, & Revenue: By: Gaurav ShreekantMayank AroraNo ratings yet

- Costs of Production: Short and Long Run Cost Curves ExplainedDocument24 pagesCosts of Production: Short and Long Run Cost Curves Explainedakshat guptaNo ratings yet

- Cost of Production: Importance of The TheoryDocument2 pagesCost of Production: Importance of The TheoryLahiru SenadheeraNo ratings yet

- Lecture 5 & 6: Theory of CostsDocument14 pagesLecture 5 & 6: Theory of CoststagashiiNo ratings yet

- Cost Theory and Estimation: Short-Run Cost FunctionsDocument22 pagesCost Theory and Estimation: Short-Run Cost Functionsbakhtiar2014No ratings yet

- 2 - Chapter 5 - Supply Decision - Short & Long Run CostDocument38 pages2 - Chapter 5 - Supply Decision - Short & Long Run CostHadilNo ratings yet

- Managerial Economics Production and Cost AnalysisDocument17 pagesManagerial Economics Production and Cost AnalysisAeyNo ratings yet

- Lecture - 8 - HL - Firm - Theory - Cost - Revenue - Profit 3Document54 pagesLecture - 8 - HL - Firm - Theory - Cost - Revenue - Profit 3L SNo ratings yet

- PAN African E-Network Project D B M: Iploma in Usiness AnagementDocument77 pagesPAN African E-Network Project D B M: Iploma in Usiness AnagementOttilieNo ratings yet

- Cost Concepts in Economics Explained: Opportunity, Fixed, VariableDocument19 pagesCost Concepts in Economics Explained: Opportunity, Fixed, VariablePrabha Karan100% (1)

- 13 Micro 3r TrimesstreDocument46 pages13 Micro 3r TrimesstreArnau CanelaNo ratings yet

- Microeconomics P8Document15 pagesMicroeconomics P8Lee Wei ChuenNo ratings yet

- How costs vary with output in the short and long run: Short and long run cost curvesDocument69 pagesHow costs vary with output in the short and long run: Short and long run cost curvesKavisha RatraNo ratings yet

- Costs of Production PDFDocument31 pagesCosts of Production PDFmarkNo ratings yet

- Republic Act No. 7942Document42 pagesRepublic Act No. 7942Paul John Page PachecoNo ratings yet

- Piling Works Tender For NrepDocument10 pagesPiling Works Tender For NrepPratik GuptaNo ratings yet

- Dagnachew GetachewDocument91 pagesDagnachew GetachewAhsan HumayunNo ratings yet

- Que For PG 98 Equity Val NotesDocument3 pagesQue For PG 98 Equity Val Notesrahul.modi18No ratings yet

- CH 10. Globalization of Ethical Decision Making. Ed.10Document39 pagesCH 10. Globalization of Ethical Decision Making. Ed.10Karola MocanNo ratings yet

- Group 2 Prado, Rhos Claries Vinluan, Jericho Oropesa, Mark Daniel Cristobal, Kyle Joshua Cortez, Gene RinchonDocument16 pagesGroup 2 Prado, Rhos Claries Vinluan, Jericho Oropesa, Mark Daniel Cristobal, Kyle Joshua Cortez, Gene Rinchonjek vinNo ratings yet

- Stryker Code of ConductDocument2 pagesStryker Code of Conductaditya permadiNo ratings yet

- INTRODUCTION To Bank of BarodaDocument11 pagesINTRODUCTION To Bank of BarodaNithinNo ratings yet

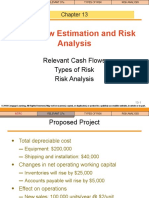

- Kuliah 11 Cash Flow Estimation and Risk AnalysisDocument39 pagesKuliah 11 Cash Flow Estimation and Risk AnalysisMutia WardaniNo ratings yet

- Bedri Managerial Economics ExamDocument3 pagesBedri Managerial Economics ExamBedri M AhmeduNo ratings yet

- Aurora's Business School Placement ReportDocument29 pagesAurora's Business School Placement ReportVivek TiwariNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument8 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceProficient CyberNo ratings yet

- RTM Cia 1Document9 pagesRTM Cia 1Shivani K Nair 2028149No ratings yet

- Week 1-2 Unit1 English For ItDocument6 pagesWeek 1-2 Unit1 English For Itapi-262133173No ratings yet

- KYC InglesDocument2 pagesKYC InglesJakeNo ratings yet

- American Eagle Sample Training ProgramDocument17 pagesAmerican Eagle Sample Training ProgramNisha BrosNo ratings yet

- Advanced Audit First AssignmentDocument2 pagesAdvanced Audit First AssignmentMegapoplocker MegapoplockerNo ratings yet

- Ca (Bsaf - Bba.mba)Document5 pagesCa (Bsaf - Bba.mba)kashif aliNo ratings yet

- Siebel Course ContentsDocument2 pagesSiebel Course ContentsChiranjeeviChNo ratings yet

- Lasting Connections with Seamless Cored WireDocument2 pagesLasting Connections with Seamless Cored WireEduardo FarfanNo ratings yet

- Cash Book - WFPDocument86 pagesCash Book - WFPdanielaossa789No ratings yet

- R13 Oracle SCM Maintenance (EAM) Cloud Features SummaryDocument17 pagesR13 Oracle SCM Maintenance (EAM) Cloud Features SummarySrinivasa Rao AsuruNo ratings yet

- HSP Faisal Hannan CVDocument3 pagesHSP Faisal Hannan CVmba2135156No ratings yet

- Commercial Invoice Po#6600210291-5057004301 PDFDocument1 pageCommercial Invoice Po#6600210291-5057004301 PDFSandra Lubana Garcia GomezNo ratings yet

- NUTECH Company Profile FinalDocument33 pagesNUTECH Company Profile FinalMohd KashifNo ratings yet

- Top Tables For The Sales and Distribution Module SD in SAP: Table - Name S/4HANA - Table and General NotesDocument7 pagesTop Tables For The Sales and Distribution Module SD in SAP: Table - Name S/4HANA - Table and General Notesramesh B100% (1)

- SITRAIN Training Course FeesDocument2 pagesSITRAIN Training Course FeesSead ArifagićNo ratings yet

- 1-1 Introduction To Failure Analysis and PreventionDocument21 pages1-1 Introduction To Failure Analysis and PreventionIAJM777No ratings yet

- September (1 - 13) October (1 - 13) Growth Diff (Unit) Result 2.466 1.377 FY21Document2 pagesSeptember (1 - 13) October (1 - 13) Growth Diff (Unit) Result 2.466 1.377 FY21Abd.Khaliq RahimNo ratings yet

- Event Tree Analysis ExplainedDocument13 pagesEvent Tree Analysis Explainedananthu.u100% (1)