You might also like

- Module 01 (Q1-Week 1): SFP Elements & FormsDocument7 pagesModule 01 (Q1-Week 1): SFP Elements & FormsChristian ZebuaNo ratings yet

- FABM 2 DemoDocument29 pagesFABM 2 DemoJerwin LaddaranNo ratings yet

- Identifying Money Management Philosophy: LearningDocument2 pagesIdentifying Money Management Philosophy: LearningDe Nev OelNo ratings yet

- Ans Mini Case 2 - A171 - LecturerDocument14 pagesAns Mini Case 2 - A171 - LecturerXue Yin Lew100% (1)

- Detailed Lesson Plan EDITEDDocument6 pagesDetailed Lesson Plan EDITEDJoylen AcopNo ratings yet

- DLL Fundamentals May 2 - 6Document6 pagesDLL Fundamentals May 2 - 6Ma. Grace HermogenesNo ratings yet

- ABM 1 LP COT Aug 29Document6 pagesABM 1 LP COT Aug 29ßella DC Reponoya100% (1)

- Week 2Document5 pagesWeek 2Jemar Alipio100% (1)

- Fundamentals of Accountancy Business and Management 1 11 3 QuarterDocument4 pagesFundamentals of Accountancy Business and Management 1 11 3 QuarterPaulo Amposta CarpioNo ratings yet

- Bank Account FundamentalsDocument6 pagesBank Account FundamentalsAmimah Balt GuroNo ratings yet

- Business Math Week 10Document9 pagesBusiness Math Week 10Jester Guballa de LeonNo ratings yet

- Lesson Plan: Department of EducationDocument2 pagesLesson Plan: Department of EducationMary Grace Pagalan Ladaran100% (1)

- Fabm1 Summative ExamDocument8 pagesFabm1 Summative ExamAbegail PanangNo ratings yet

- Entrepreneurship Lesson 1Document46 pagesEntrepreneurship Lesson 1Mark Nelson A. MontemayorNo ratings yet

- Fabm1 LPDocument2 pagesFabm1 LPRaul Soriano CabantingNo ratings yet

- Fatima EAPP-Q1 M5Document30 pagesFatima EAPP-Q1 M512 - ICT 1 Gerald K. MamasalanangNo ratings yet

- DLL Abm 1 Week 7-8Document4 pagesDLL Abm 1 Week 7-8Christopher Selebio100% (1)

- Bookkeeping Lesson PlanDocument4 pagesBookkeeping Lesson PlanShanin Estavillo100% (1)

- Session 1 Session 2 Session 3 Session 4 Session 5: I. ObjectivesDocument3 pagesSession 1 Session 2 Session 3 Session 4 Session 5: I. ObjectivesLeighyo An MegastinoNo ratings yet

- ABM - FABM11-IIIg - J - 28Document2 pagesABM - FABM11-IIIg - J - 28Mary Grace Pagalan Ladaran0% (1)

- Lesson Plan Accounting 2.2Document2 pagesLesson Plan Accounting 2.2Jevie GibertasNo ratings yet

- Business Math Week 5Document9 pagesBusiness Math Week 5Ar-rafi GalamgamNo ratings yet

- Accounting Cycle - Transactions: Fundamentals of Accountancy Business and Management 1 11 3 QuarterDocument4 pagesAccounting Cycle - Transactions: Fundamentals of Accountancy Business and Management 1 11 3 QuarterPaulo Amposta CarpioNo ratings yet

- Computing commissions, down payments, and balancesDocument12 pagesComputing commissions, down payments, and balancesDearla BitoonNo ratings yet

- Tos in FABM2 Second QuarterDocument2 pagesTos in FABM2 Second QuarterLAARNI REBONGNo ratings yet

- Business MathDocument3 pagesBusiness MathRhea Pardo PeralesNo ratings yet

- FABM 1.module 1Document22 pagesFABM 1.module 1SHIERY MAE FALCONITINNo ratings yet

- FUNDAMENTALS OF ABM1, Q2-WEEKS 3 & 4 FinalDocument17 pagesFUNDAMENTALS OF ABM1, Q2-WEEKS 3 & 4 FinalMichelJoy De GuzmanNo ratings yet

- q4 Abm Fundamentals of Abm1 11 Week 3Document6 pagesq4 Abm Fundamentals of Abm1 11 Week 3Judy Ann Villanueva100% (1)

- Business Finance: Quarter 4 Module 10Document5 pagesBusiness Finance: Quarter 4 Module 10Adoree RamosNo ratings yet

- LESSON PLAN Semi Detailed FinalDocument3 pagesLESSON PLAN Semi Detailed FinalGrace Gabe BatallaNo ratings yet

- Chapter 10 Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business 1Document37 pagesChapter 10 Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business 1Ian SumastreNo ratings yet

- Daily Lesson Plan on Accounting Principles and Major Account TypesDocument13 pagesDaily Lesson Plan on Accounting Principles and Major Account TypesJevie GibertasNo ratings yet

- Nature of Merchan Dising BusinessDocument17 pagesNature of Merchan Dising Businesskimberly anne feliano100% (1)

- Accounting Branches and ServicesDocument54 pagesAccounting Branches and ServicesGladzangel LoricabvNo ratings yet

- Business Finance - 12 - Third - Week 5Document11 pagesBusiness Finance - 12 - Third - Week 5AngelicaHermoParasNo ratings yet

- Module 4 MathDocument10 pagesModule 4 MathAlissa MayNo ratings yet

- A. Review Activity: Reviewing Previous Lesson or RelatingDocument4 pagesA. Review Activity: Reviewing Previous Lesson or RelatingsweetzelNo ratings yet

- Lesson PlanDocument5 pagesLesson PlanMa. Katrina BusaNo ratings yet

- Week 3 DLL Jan 15-19 XXXDocument7 pagesWeek 3 DLL Jan 15-19 XXXChristian TonogbanuaNo ratings yet

- Math 11 Fabm1 Abm q2 Week 7Document14 pagesMath 11 Fabm1 Abm q2 Week 7Marchyrella Uoiea Olin JovenirNo ratings yet

- Fabm2 - Se (2) Answer KeyDocument2 pagesFabm2 - Se (2) Answer Keyl m0% (2)

- DLL FabmDocument4 pagesDLL FabmjoanNo ratings yet

- Grade 11 Lesson Log Analyzes Markups, Margins, DiscountsDocument10 pagesGrade 11 Lesson Log Analyzes Markups, Margins, DiscountsAr-rafi GalamgamNo ratings yet

- DLL FABM Week5Document3 pagesDLL FABM Week5sweetzelNo ratings yet

- Statement of Changes in EquityDocument4 pagesStatement of Changes in EquityWella LozadaNo ratings yet

- FabmDocument26 pagesFabmErica Napigkit100% (1)

- Daily Lesson Log/Plan: Monday Tuesday Wednesday ThursdayDocument5 pagesDaily Lesson Log/Plan: Monday Tuesday Wednesday ThursdayJovelyn Ignacio VinluanNo ratings yet

- Department of Education: Republic of The PhilippinesDocument5 pagesDepartment of Education: Republic of The PhilippinesGlaiza Dalayoan FloresNo ratings yet

- Bank Reconciliation Statement LessonDocument2 pagesBank Reconciliation Statement LessonDimple Grace AstorgaNo ratings yet

- Fundamentals of ABM-2 Test ScoresDocument2 pagesFundamentals of ABM-2 Test Scoresmanuel hipolitoNo ratings yet

- Introduction To Accounting: Fundamentals of Accountancy, Business and Management 2Document4 pagesIntroduction To Accounting: Fundamentals of Accountancy, Business and Management 2Emariel CuarioNo ratings yet

- September 2 2019Document3 pagesSeptember 2 2019Vinza AcobNo ratings yet

- Budget of Work For FABM2Document2 pagesBudget of Work For FABM2Asi100% (1)

- Chapter 7 - Basic Documents and Transactions Related To Bank DepositsDocument12 pagesChapter 7 - Basic Documents and Transactions Related To Bank DepositsAmie Jane MirandaNo ratings yet

- Topic: Statement of Financial Position (SFP) : Individual Performance Task/ Activity (Week 1 in The Module)Document11 pagesTopic: Statement of Financial Position (SFP) : Individual Performance Task/ Activity (Week 1 in The Module)Joana Jean SuymanNo ratings yet

- Weekly Home Learning Plans for Business MathematicsDocument3 pagesWeekly Home Learning Plans for Business MathematicsBryan BejeranoNo ratings yet

- DLP EaaDocument6 pagesDLP EaaEmily A. AneñonNo ratings yet

- 4th FABM 2Document2 pages4th FABM 2Keisha MarieNo ratings yet

- Fabm Module03 File01Document8 pagesFabm Module03 File01PREFIX THAT IS LONG - Lester LoutteNo ratings yet

- Operating Cycle of A Merchandising BusinessDocument10 pagesOperating Cycle of A Merchandising BusinessJanelle FortesNo ratings yet

- Self Assessment QuizesDocument41 pagesSelf Assessment QuizesStephanie NaamaniNo ratings yet

- Wholesale Banking Operation HDFCDocument43 pagesWholesale Banking Operation HDFCVishal Sonawane50% (2)

- PFRS UPDATES ON ACCOUNTING CHANGES AND ERRORSDocument11 pagesPFRS UPDATES ON ACCOUNTING CHANGES AND ERRORSMark GerwinNo ratings yet

- ACCO 20043 FormationDocument2 pagesACCO 20043 FormationClarissePelayoNo ratings yet

- SAP NoteBookDocument31 pagesSAP NoteBookMuhammad Kashif ShabbirNo ratings yet

- 1 Notice To Setoff AccountsDocument2 pages1 Notice To Setoff Accountsexousiallc100% (7)

- Accounting Is The Process of Keeping Track of A Business' FinancesDocument52 pagesAccounting Is The Process of Keeping Track of A Business' FinancesJowjie TV100% (1)

- The Golden Rules of AccountingDocument1 pageThe Golden Rules of AccountingRamesh ManiNo ratings yet

- This Is RealDocument17 pagesThis Is RealCheemee LiuNo ratings yet

- Organizational Structure, Pricing, Credit Checks, and Sales ProcessesDocument19 pagesOrganizational Structure, Pricing, Credit Checks, and Sales Processesramesh100% (1)

- Materials Management - Multiple Choice QuestionerDocument8 pagesMaterials Management - Multiple Choice QuestionerHimanshu DesaiNo ratings yet

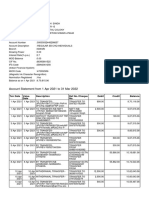

- Account Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument12 pagesAccount Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceNiwadi PremiNo ratings yet

- Financial Accounting CIA-1 (B)Document24 pagesFinancial Accounting CIA-1 (B)EKANSH DANGAYACH 20212619No ratings yet

- Sub Ledger AccountingDocument13 pagesSub Ledger Accountingkiran2891No ratings yet

- B.B.M. (I.B.) (Semester - I) : Q1) Answer The Following in 20 Words Each (Any Ten)Document106 pagesB.B.M. (I.B.) (Semester - I) : Q1) Answer The Following in 20 Words Each (Any Ten)KuNdAn DeOrENo ratings yet

- Buscom ReviewerDocument16 pagesBuscom ReviewereysiNo ratings yet

- Lembar Jawaban Kosong-AkuntansiDocument38 pagesLembar Jawaban Kosong-AkuntansiKIKI AMELIA HUTAJULU100% (1)

- Partnership Accounting ReviewerDocument10 pagesPartnership Accounting ReviewerJEFFERSON CUTENo ratings yet

- Audit stockholder's equity and liabilities problemsDocument7 pagesAudit stockholder's equity and liabilities problemsCiatto SpotifyNo ratings yet

- Financial Assets and InventoriesDocument17 pagesFinancial Assets and InventoriesCrazy Solo67% (3)

- Soon Heng (01.03-15.03.2023) Soa PDFDocument2 pagesSoon Heng (01.03-15.03.2023) Soa PDFSicklyangel LokeNo ratings yet

- Cash and Cash EquivalentsDocument23 pagesCash and Cash EquivalentsGennelyn Grace Penaredondo100% (1)

- Special Journal and Subsidiary LedgerDocument25 pagesSpecial Journal and Subsidiary LedgerMilenia Theresia NarwastuNo ratings yet

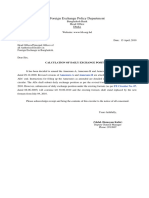

- 3 Calculation of Daily Exchange PositionDocument10 pages3 Calculation of Daily Exchange PositionTalha AdilNo ratings yet

- Financial Accounting Config S4HANADocument64 pagesFinancial Accounting Config S4HANAalegpontonNo ratings yet

- CSEC Study Guide - March 22, 2011Document12 pagesCSEC Study Guide - March 22, 2011ChantelleMorrisonNo ratings yet

- AsdasdasdsadDocument4 pagesAsdasdasdsadWinston Mark KahidNo ratings yet

- SBI Acc InsDocument11 pagesSBI Acc InsAnonymous UjEPpvYDNo ratings yet

- Accbp100 2nd Exam Part 1Document2 pagesAccbp100 2nd Exam Part 1emem resuento100% (1)