You might also like

- Business Combination Part 2Document4 pagesBusiness Combination Part 2Charizza Amor TejadaNo ratings yet

- Module 2Document5 pagesModule 2Alpha RamoranNo ratings yet

- QUIZ 2 (Part 2) SolutionsDocument3 pagesQUIZ 2 (Part 2) SolutionsCharizza Amor TejadaNo ratings yet

- Accounting Special TransactionDocument25 pagesAccounting Special TransactionMarinel Mae ChicaNo ratings yet

- Business Combi. Chapter 1 PROBLEM 3Document4 pagesBusiness Combi. Chapter 1 PROBLEM 3latte aeriNo ratings yet

- 2076 - Varias, Aizel Ann B - Module 1Document18 pages2076 - Varias, Aizel Ann B - Module 1Aizel Ann VariasNo ratings yet

- AssetsDocument1 pageAssetsxenniNo ratings yet

- 2076 - Varias, Aizel Ann B - Module 2Document20 pages2076 - Varias, Aizel Ann B - Module 2Aizel Ann VariasNo ratings yet

- Castro, Geene - Activity 1 - Bsma 3205Document6 pagesCastro, Geene - Activity 1 - Bsma 3205Geene CastroNo ratings yet

- Module 1Document4 pagesModule 1Jacqueline OrtegaNo ratings yet

- Business Combi Quiz (Part1)Document9 pagesBusiness Combi Quiz (Part1)Rica Joy RuzgalNo ratings yet

- Corporate LiquidationDocument8 pagesCorporate LiquidationKyo TieNo ratings yet

- Cfas AnswersDocument5 pagesCfas AnswersPATRICIA SANTOSNo ratings yet

- Chapter 4Document36 pagesChapter 4MARRIETTE JOY ABADNo ratings yet

- ASSIGNMENT 2 Business CombinationDocument3 pagesASSIGNMENT 2 Business CombinationApril ManjaresNo ratings yet

- Chapter 5 SpreadsheetDocument7 pagesChapter 5 SpreadsheetChâu Trần Dương MinhNo ratings yet

- Module 1Document4 pagesModule 1Alpha RamoranNo ratings yet

- Adv Acc 2 Module 1 Topic1.2Document5 pagesAdv Acc 2 Module 1 Topic1.2James CantorneNo ratings yet

- Use The Following Information For The Next Two Items:: 1. Prepare The Consolidated Statement of Financial PositionDocument15 pagesUse The Following Information For The Next Two Items:: 1. Prepare The Consolidated Statement of Financial PositionJacqueline OrtegaNo ratings yet

- PANOPIO Activity1 BLOCK3209Document6 pagesPANOPIO Activity1 BLOCK3209panopiojessiemae4No ratings yet

- Quiz 14 SolutionsDocument16 pagesQuiz 14 SolutionsAlex OzfordNo ratings yet

- Business Combinations (Part 2) : Problem 1: True or FalseDocument12 pagesBusiness Combinations (Part 2) : Problem 1: True or FalseAlexanderJacobVielMartinez100% (3)

- Profe03 Act 1Document2 pagesProfe03 Act 1Red MarieeNo ratings yet

- Accounting 7an Business CombinationDocument8 pagesAccounting 7an Business CombinationLabLab ChattoNo ratings yet

- Lesson 3. Consolidated Financial StatementsDocument6 pagesLesson 3. Consolidated Financial StatementsKsUnlockerNo ratings yet

- Ast 2.1Document5 pagesAst 2.1Patrick Alvin100% (1)

- Practice Set 1Document3 pagesPractice Set 1ARIOLA, DIANA REMOLINNo ratings yet

- Business CombinationDocument2 pagesBusiness CombinationJezelle NanoNo ratings yet

- Corporate LiquidationDocument4 pagesCorporate LiquidationAngela Marie PenarandaNo ratings yet

- Latihan AKLDocument4 pagesLatihan AKLMin RinNo ratings yet

- NUDJPIA FAR AND AFAR SOLUTIONS - Partnership FormationDocument3 pagesNUDJPIA FAR AND AFAR SOLUTIONS - Partnership FormationKyla Artuz Dela CruzNo ratings yet

- Mendoza, Keije Lawrence M.Document10 pagesMendoza, Keije Lawrence M.21-39693No ratings yet

- Chapter 1 Abc Suggested SolutionsDocument7 pagesChapter 1 Abc Suggested SolutionsAlthea Lyn ReyesNo ratings yet

- Quiz 1 SolutionsDocument4 pagesQuiz 1 SolutionsLJ BNo ratings yet

- Let's Analyze: Pacalna, Anifah BDocument2 pagesLet's Analyze: Pacalna, Anifah BAnifahchannie PacalnaNo ratings yet

- Chapter 1Document9 pagesChapter 1Rufina B VerdeNo ratings yet

- 2Document1 page2Trixie IdananNo ratings yet

- Business Combination - ExercisesDocument36 pagesBusiness Combination - ExercisesJessalyn CilotNo ratings yet

- TPBALANCESHEET DeloyDocument1 pageTPBALANCESHEET DeloyJen DeloyNo ratings yet

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- Business Combinations - Net Asset AcquisitionDocument15 pagesBusiness Combinations - Net Asset AcquisitionLyca Mae CubangbangNo ratings yet

- Silver Company Provided The Following Information at Year-EndDocument1 pageSilver Company Provided The Following Information at Year-EndKatrina Dela CruzNo ratings yet

- Partnership ActivityDocument12 pagesPartnership ActivityTeresa Pantallano DivinagraciaNo ratings yet

- Abc Chapter 1 Solman 2020 Millan Abc - CompressDocument9 pagesAbc Chapter 1 Solman 2020 Millan Abc - CompressErna DavidNo ratings yet

- Bus. Com. Part 1Document10 pagesBus. Com. Part 1Jaycel BayronNo ratings yet

- CABINAS - Partnership Formation & OperationDocument16 pagesCABINAS - Partnership Formation & OperationJoshua CabinasNo ratings yet

- Particulars Debit CreditDocument10 pagesParticulars Debit CreditJasmine ActaNo ratings yet

- Statement of Financial PositionDocument6 pagesStatement of Financial PositionAnne Angelie Gomez SebialNo ratings yet

- P3.5 Different Forms of Business CombinationDocument8 pagesP3.5 Different Forms of Business CombinationAgnes CahyaNo ratings yet

- Nudjpia Far and Afar Solutions - Conceptual FrameworkDocument1 pageNudjpia Far and Afar Solutions - Conceptual FrameworkKyla Artuz Dela CruzNo ratings yet

- Business CombinationDocument10 pagesBusiness CombinationJaira ClavoNo ratings yet

- FAOMA Part 3 Quiz Complete SolutionsDocument3 pagesFAOMA Part 3 Quiz Complete SolutionsMary De JesusNo ratings yet

- Buscom TP 2Document4 pagesBuscom TP 2anna mae orcioNo ratings yet

- Fischer10h Ch21 TBDocument2 pagesFischer10h Ch21 TBLouiza Kyla AridaNo ratings yet

- Sol. Man. Chapter 4 Consol. Fs Part 1Document37 pagesSol. Man. Chapter 4 Consol. Fs Part 1itsmenatoy43% (7)

- Statement of AffairsDocument2 pagesStatement of AffairsShoyo HinataNo ratings yet

- Accounting For Business Combination - PRELIMDocument5 pagesAccounting For Business Combination - PRELIMAnonymouslyNo ratings yet

- Buenaventura PREA4Document9 pagesBuenaventura PREA4Buenaventura, Elijah B.No ratings yet

- Finals Quiz No. 1 AnswersDocument4 pagesFinals Quiz No. 1 AnswersMergierose DalgoNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Exercise - Gross EstateDocument2 pagesExercise - Gross EstateAndree PereaNo ratings yet

- Exercise - Vanishing DeductionsDocument1 pageExercise - Vanishing DeductionsAndree PereaNo ratings yet

- Calculus - Practice QuizDocument1 pageCalculus - Practice QuizAndree PereaNo ratings yet

- P.E - Notes 1Document9 pagesP.E - Notes 1Andree PereaNo ratings yet

- Finance - Notes Part 2Document10 pagesFinance - Notes Part 2Andree PereaNo ratings yet

- Finance - Notes Part 1Document6 pagesFinance - Notes Part 1Andree PereaNo ratings yet

- Marketing - Notes 3Document4 pagesMarketing - Notes 3Andree PereaNo ratings yet

- Reaction Paper On Corruption in The PhilippinesDocument1 pageReaction Paper On Corruption in The PhilippinesJalalodin AminolaNo ratings yet

- LOGON AustriaDocument28 pagesLOGON AustriapapirihemijskaNo ratings yet

- City MGM'T Memo On Restoring Certain Long Beach Fire Services (Nov. 5, 2013)Document5 pagesCity MGM'T Memo On Restoring Certain Long Beach Fire Services (Nov. 5, 2013)Anonymous 3qqTNAAOQNo ratings yet

- Vip Case StudyDocument29 pagesVip Case StudyManjuGeethaSubramani83% (6)

- Introduction To Globalization-Contemporary WorldDocument29 pagesIntroduction To Globalization-Contemporary WorldBRILIAN TOMAS0% (1)

- FIN 600 - Midterm Sample With SolutionsDocument22 pagesFIN 600 - Midterm Sample With SolutionsVipul0% (2)

- Cityam 2012-02-23Document36 pagesCityam 2012-02-23City A.M.No ratings yet

- Idef0 and DFD ProjectDocument2 pagesIdef0 and DFD ProjectAl KamaraNo ratings yet

- DuniaDocument64 pagesDuniaAmith PanickerNo ratings yet

- Answer Key On Comprehensive ExerciseDocument13 pagesAnswer Key On Comprehensive ExerciseErickaNo ratings yet

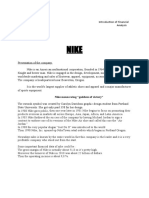

- Nike Presentation Intro of FinanceDocument11 pagesNike Presentation Intro of FinanceRashe FasiNo ratings yet

- General Principles of TaxationDocument17 pagesGeneral Principles of TaxationJericho Pedragosa33% (3)

- Digest RR 5-2015Document1 pageDigest RR 5-2015Cristine100% (1)

- Principles of AdvertisingDocument7 pagesPrinciples of AdvertisingOmolola MohammedNo ratings yet

- Angel David Guardiola Sepulveda: Employment HistoryDocument1 pageAngel David Guardiola Sepulveda: Employment HistoryAngelD GSNo ratings yet

- Project Report On Industrial RelationDocument109 pagesProject Report On Industrial Relationushasarthak57% (7)

- Apple Inc. Condensed Consolidated Statements of Operations (Unaudited)Document4 pagesApple Inc. Condensed Consolidated Statements of Operations (Unaudited)Eder Leal MNo ratings yet

- Chapter 6 MNGDocument45 pagesChapter 6 MNGMohamed Hassan Mohamed KulmiyeNo ratings yet

- Messari Report Crypto Theses For 2023Document168 pagesMessari Report Crypto Theses For 2023Akshat TennetiNo ratings yet

- MGT 333 - Group 8 - ReportDocument27 pagesMGT 333 - Group 8 - ReportSanaiya JokhiNo ratings yet

- Marxism and The Law - Preliminary AnalysesDocument27 pagesMarxism and The Law - Preliminary AnalysesRubensBordinhãoNetoNo ratings yet

- Oracle AP Invoices & Hold DetailsDocument12 pagesOracle AP Invoices & Hold DetailsDinesh Kumar Sivaji100% (1)

- Home Depot Balance SheetDocument4 pagesHome Depot Balance SheetNicolas ErnestoNo ratings yet

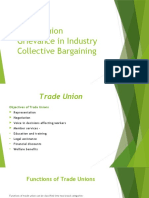

- Trade Union Grievance in Industry Collective BargainingDocument19 pagesTrade Union Grievance in Industry Collective Bargainingmamunur rashidNo ratings yet

- Selection & Recruitment 'Document95 pagesSelection & Recruitment 'SupriyaJKadianNo ratings yet

- You Should Seek Expert Advice On Matters Affecting Your Company's Employees As NecessaryDocument2 pagesYou Should Seek Expert Advice On Matters Affecting Your Company's Employees As Necessarylibokoh644No ratings yet

- Fm202 Exam Questions 2013Document12 pagesFm202 Exam Questions 2013Grace VersoniNo ratings yet

- Forbes - October 28 2013 USADocument132 pagesForbes - October 28 2013 USAalx_ppscuNo ratings yet

- Internship ReportDocument5 pagesInternship ReportThanhTrúcc100% (1)

- Intermediate Accounting TheoriesDocument12 pagesIntermediate Accounting TheoriesRayman MamakNo ratings yet