You might also like

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- 8% Tax RuleDocument24 pages8% Tax Rulemarjorie blancoNo ratings yet

- Revenue Memorandum Order No.: Bureau of Internal RevenueDocument7 pagesRevenue Memorandum Order No.: Bureau of Internal RevenueJoyce Cariaga SalvadorNo ratings yet

- TRAIN LAW Compilation From NetDocument14 pagesTRAIN LAW Compilation From NetAnne Vernadice Areña-VelascoNo ratings yet

- Updates and Critical Areas in TaxationDocument32 pagesUpdates and Critical Areas in Taxationvanessa ocampoNo ratings yet

- Self-Employed And/ or Professionals (Sep) : Lesson 5Document2 pagesSelf-Employed And/ or Professionals (Sep) : Lesson 5Ash PadillaNo ratings yet

- TRAIN LAW UPDATES INCOME TAX RATESDocument23 pagesTRAIN LAW UPDATES INCOME TAX RATESNikki Estores GonzalesNo ratings yet

- Module 4 Optional Tax Rate For Self EmployedDocument7 pagesModule 4 Optional Tax Rate For Self EmployedJam HailNo ratings yet

- RMO No. 23-2018 DigestDocument4 pagesRMO No. 23-2018 DigestMary Joy NavajaNo ratings yet

- Selected TRAIN Law Amendments on 8% Tax Rate, Exemptions, Deductions & Aliens Employed by RHQs/ROHQs/OBUs/PSCsDocument80 pagesSelected TRAIN Law Amendments on 8% Tax Rate, Exemptions, Deductions & Aliens Employed by RHQs/ROHQs/OBUs/PSCsIah FriaNo ratings yet

- Amount of Net Taxable Income Rate Over But Not OverDocument1 pageAmount of Net Taxable Income Rate Over But Not OverDennah Faye SabellinaNo ratings yet

- Kinds of Income and Income Tax of Individuals: Take NoteDocument7 pagesKinds of Income and Income Tax of Individuals: Take NoteKen RaquinioNo ratings yet

- Philippine Tax System: Individual Income TaxationDocument27 pagesPhilippine Tax System: Individual Income TaxationeuniNo ratings yet

- Pa Tax Brief - March 2018Document11 pagesPa Tax Brief - March 2018Teresita TibayanNo ratings yet

- How To Tax An Individual 1Document25 pagesHow To Tax An Individual 1Lianna Xenia EspirituNo ratings yet

- 8% Income Tax OptionDocument14 pages8% Income Tax OptionZaaavnn VannnnnNo ratings yet

- Train I.ppt - Vers. 10.21.2018Document103 pagesTrain I.ppt - Vers. 10.21.2018Ellard28 saturnoNo ratings yet

- Chapter 7: Introduction To Regular Income TaxDocument5 pagesChapter 7: Introduction To Regular Income TaxArna Kaira Kjell DiestraNo ratings yet

- Income Tax On Individuals Part 2Document22 pagesIncome Tax On Individuals Part 2mmhNo ratings yet

- M8PLR The Value-Added Tax and Income TaxDocument3 pagesM8PLR The Value-Added Tax and Income TaxClaricel JoyNo ratings yet

- Week 7: Taxation of Individuals (Non Residents and Aliens) and General Professional PartnershipsDocument6 pagesWeek 7: Taxation of Individuals (Non Residents and Aliens) and General Professional PartnershipsEddie Mar JagunapNo ratings yet

- Reviewer (Tax) : National Internal Revenue Taxes Computation For Mixed Income Earner Who Availed 8%Document7 pagesReviewer (Tax) : National Internal Revenue Taxes Computation For Mixed Income Earner Who Availed 8%LeeshNo ratings yet

- Regular Income Tax GuideDocument32 pagesRegular Income Tax GuideElle VernezNo ratings yet

- 5.0 Intro To Income TaxDocument31 pages5.0 Intro To Income TaxAllan BacudioNo ratings yet

- Tax Sample ComputationDocument10 pagesTax Sample ComputationEryka Jo MonatoNo ratings yet

- Train Law & Tax UpdatesDocument211 pagesTrain Law & Tax UpdatesAlicia FelicianoNo ratings yet

- 2.0 Income Tax ReviewerDocument50 pages2.0 Income Tax ReviewerKrystal MaciasNo ratings yet

- Income Taxation of Individuals Under NIRC, As Amended by TRAIN Law Compensation Income Self Employment / Practice of Profession IncomeDocument1 pageIncome Taxation of Individuals Under NIRC, As Amended by TRAIN Law Compensation Income Self Employment / Practice of Profession Incomejim fiedacanNo ratings yet

- NIRC NotesDocument9 pagesNIRC NotesCen TanaNo ratings yet

- Other Percentage TaxDocument19 pagesOther Percentage TaxChristine AceronNo ratings yet

- 5 - Tax Rules For Individuals Earning Income Both From Compensation and From Self-EditedDocument5 pages5 - Tax Rules For Individuals Earning Income Both From Compensation and From Self-EditedKiara Marie P. LAGUDANo ratings yet

- TRAIN LAW - 3.9.18 - Laguna ChapterDocument408 pagesTRAIN LAW - 3.9.18 - Laguna ChapterDeoshel AlagonNo ratings yet

- TRAIN Law Updates on Personal Income TaxDocument51 pagesTRAIN Law Updates on Personal Income TaxZi VillarNo ratings yet

- Summary Notes Pecentage Tax On Vat Exempt Sales and Transactions Section 116, NIRCDocument2 pagesSummary Notes Pecentage Tax On Vat Exempt Sales and Transactions Section 116, NIRCalmira garciaNo ratings yet

- BIR Computations for Self-Employed ProfessionalsDocument10 pagesBIR Computations for Self-Employed Professionalsbull jackNo ratings yet

- Tax Sample ComputationDocument9 pagesTax Sample ComputationErykaNo ratings yet

- Provided, That Minimum Wage Earners As Defined in Section 22 (HH) of This Code ShallDocument5 pagesProvided, That Minimum Wage Earners As Defined in Section 22 (HH) of This Code ShallFrancis DiazNo ratings yet

- Regular Income Tax Inclusion RulesDocument33 pagesRegular Income Tax Inclusion RulesAaron BuendiaNo ratings yet

- How To Avail The 8 Tax Under Republic AcDocument7 pagesHow To Avail The 8 Tax Under Republic AcJan. ReyNo ratings yet

- Special Tax Regime For TradersDocument5 pagesSpecial Tax Regime For TradersArsalan LobaniyaNo ratings yet

- General Principles of Income TaxationDocument2 pagesGeneral Principles of Income TaxationJUST KINGNo ratings yet

- Income Tax Amendment Draft Bill 2016Document10 pagesIncome Tax Amendment Draft Bill 2016Muhammad KashifNo ratings yet

- Aprelim - Purely Business IncomeDocument37 pagesAprelim - Purely Business IncomeAshley VasquezNo ratings yet

- MAT and AMT ExplainedDocument17 pagesMAT and AMT ExplainedNitin ChoudharyNo ratings yet

- Optional Standard DeductionDocument3 pagesOptional Standard Deductionopep77No ratings yet

- It Goi Note On Mat and AmtDocument17 pagesIt Goi Note On Mat and AmtKapil AroraNo ratings yet

- TRAIN (Changes) ???? Pages 2, 5 - 7Document4 pagesTRAIN (Changes) ???? Pages 2, 5 - 7blackmail1No ratings yet

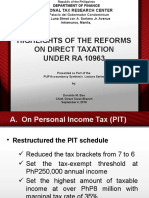

- Highlights of The Reforms On Direct Taxation UNDER RA 10963: National Tax Research CenterDocument33 pagesHighlights of The Reforms On Direct Taxation UNDER RA 10963: National Tax Research CenterCourt NanquilNo ratings yet

- Tax AmendmentsDocument109 pagesTax AmendmentsPrincess Hazel GriñoNo ratings yet

- Minimum Alternate TaxDocument8 pagesMinimum Alternate Taxjainrahul234No ratings yet

- Tax Reform For Acceleration and Inclusion LawDocument28 pagesTax Reform For Acceleration and Inclusion LawGloriosa SzeNo ratings yet

- 2.3 Tax On Income - Tax On IndividualsDocument14 pages2.3 Tax On Income - Tax On IndividualsfelixacctNo ratings yet

- Tax Intro - AmendmentsDocument8 pagesTax Intro - AmendmentsNombs NomNo ratings yet

- National Assembly passes tax amendment billDocument11 pagesNational Assembly passes tax amendment billMuhammad Hassan AliNo ratings yet

- IAET Tax Base FormulaDocument2 pagesIAET Tax Base FormulaMeghan Kaye LiwenNo ratings yet

- 11-134191-1987-Tio v. Videogram Regulatory BoardDocument9 pages11-134191-1987-Tio v. Videogram Regulatory Boarderic akoNo ratings yet

- Mat and Amt: Objective of Levying MATDocument17 pagesMat and Amt: Objective of Levying MATSamuel AnthrayoseNo ratings yet

- Module 07 Introduction To Regular Income TaxDocument21 pagesModule 07 Introduction To Regular Income TaxJeon KookieNo ratings yet

- Bir TaxDocument157 pagesBir TaxMubarrach MatabalaoNo ratings yet

- Module 07 Introduction To Regular Income Tax 3 2Document21 pagesModule 07 Introduction To Regular Income Tax 3 2Joshua BazarNo ratings yet

- A Simple 8-Step Social Media Content Creation ProcessDocument2 pagesA Simple 8-Step Social Media Content Creation ProcessDaveNo ratings yet

- Ita Imia 2023 BDDocument28 pagesIta Imia 2023 BDKishor YenepalliNo ratings yet

- MCQ Monopolistic & Oligopolistic Competition PDFDocument5 pagesMCQ Monopolistic & Oligopolistic Competition PDFAJAY KUMAR SAHUNo ratings yet

- Theories of RetailingDocument9 pagesTheories of Retailingsandra bonifusNo ratings yet

- Philippine Income Taxation QuizDocument4 pagesPhilippine Income Taxation QuizRezhel Vyrneth TurgoNo ratings yet

- Services MarketingDocument5 pagesServices MarketingSharmaNo ratings yet

- Copia de SustainableFashionandTextilesDesignJourneysbyKateFletcherEarthscan2008Document6 pagesCopia de SustainableFashionandTextilesDesignJourneysbyKateFletcherEarthscan2008martina torresNo ratings yet

- How HRD links to HRM and its focus areasDocument22 pagesHow HRD links to HRM and its focus areasMA ADNo ratings yet

- Todos Os Mercados (TM) and A Day in The Life of Henri Trouvé, Tuesday 26 January 2016Document3 pagesTodos Os Mercados (TM) and A Day in The Life of Henri Trouvé, Tuesday 26 January 2016LoraineNo ratings yet

- Customer Usage Intention of Mobile Commerce in India - An Empirical StudyDocument23 pagesCustomer Usage Intention of Mobile Commerce in India - An Empirical StudyDisha DateNo ratings yet

- Southwest Airlines Success: A Case Study Analysis: January 2011Document6 pagesSouthwest Airlines Success: A Case Study Analysis: January 2011Fabián RosalesNo ratings yet

- Sony Betamax Brand Failure: Hitesh BhasinDocument3 pagesSony Betamax Brand Failure: Hitesh Bhasinakash bathamNo ratings yet

- Chapter Eleven: Pricing in RetailingDocument30 pagesChapter Eleven: Pricing in RetailingJanny SaffNo ratings yet

- Islamic Banking and Finance Review (Vol. 2), 166-Article Text-412-1-10-20191121Document12 pagesIslamic Banking and Finance Review (Vol. 2), 166-Article Text-412-1-10-20191121UMT JournalsNo ratings yet

- B8AF100 CA BG - Irish Perfumes LTD - Oct 2020Document8 pagesB8AF100 CA BG - Irish Perfumes LTD - Oct 2020Filzah Ahmad Abd GarniNo ratings yet

- Wallstreetjournal 20160125 The Wall Street JournalDocument40 pagesWallstreetjournal 20160125 The Wall Street JournalstefanoNo ratings yet

- IC Brand Visual Identity Checklist 11225 - WORDDocument2 pagesIC Brand Visual Identity Checklist 11225 - WORDkokobrashNo ratings yet

- Draft RR Registration EOPT - For Public ConsultationDocument18 pagesDraft RR Registration EOPT - For Public ConsultationGennelyn OdulioNo ratings yet

- One To One MarketingDocument22 pagesOne To One MarketingSamuel HenriqueNo ratings yet

- Creating Strategic Advantages for NespressoDocument14 pagesCreating Strategic Advantages for NespressoAnkitpandya23No ratings yet

- HRmanualDocument6 pagesHRmanualNaman KediaNo ratings yet

- SBI Seeks Insolvency of Western Refrigeration over GuaranteeDocument16 pagesSBI Seeks Insolvency of Western Refrigeration over Guaranteeveer vikramNo ratings yet

- Wa0022.Document164 pagesWa0022.vartica100% (1)

- Valuation Report For 2 Storey BuildingDocument3 pagesValuation Report For 2 Storey BuildingAtnapaz JodNo ratings yet

- ABB Drives Life Cycle ManagementDocument10 pagesABB Drives Life Cycle Managementjose guadalupe rodriguez rodriguezNo ratings yet

- Staples Inc.Document6 pagesStaples Inc.sid lahoriNo ratings yet

- Digital Marketing ProjectDocument55 pagesDigital Marketing Projectsarah IsharatNo ratings yet

- 1 - 20.09.2018 - Corriogendum 1aDocument1 page1 - 20.09.2018 - Corriogendum 1achtrpNo ratings yet

- Final Copy of JH Final 08.01.19Document34 pagesFinal Copy of JH Final 08.01.19District Audit Officer DAONo ratings yet

- LEK sharing-CM - AmCham Healthcare Trends 2021 - 2021MAR23bDocument30 pagesLEK sharing-CM - AmCham Healthcare Trends 2021 - 2021MAR23bRishabh RajNo ratings yet